Baguio Green Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

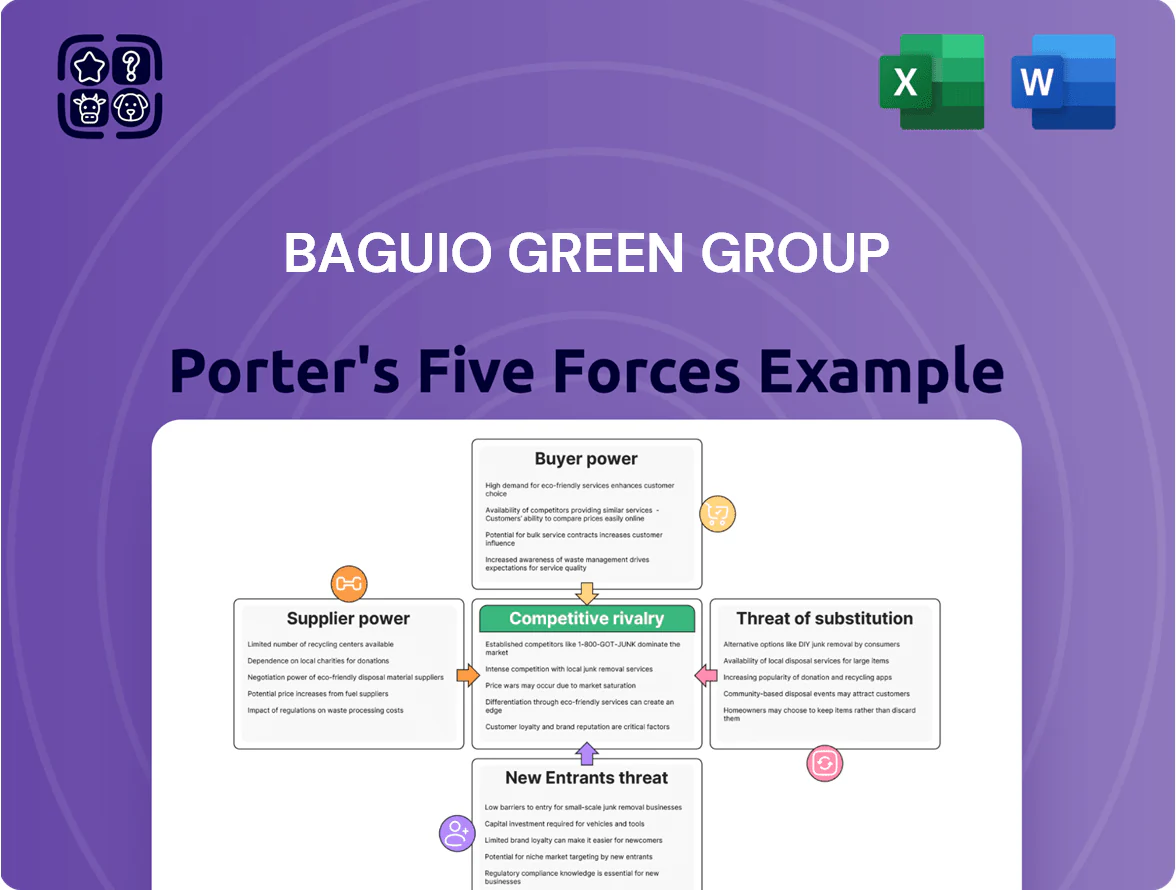

Baguio Green Group faces moderate buyer power and supplier concentration, while regulatory shifts and capital intensity raise entry barriers; competitive rivalry is high among diversified waste-to-energy and recycling players, and substitutes pressure margins from traditional waste services and emerging circular solutions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Baguio Green Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Equipment and Consumable Market

Primary inputs for Baguio Green Group—cleaning chemicals, protective gear, and specialized waste-collection vehicles—are largely standardized and supplied by numerous global and regional manufacturers, so vendor switching is straightforward.

Market fragmentation keeps supplier concentration low: top 5 global chemical suppliers held about 28% market share in 2024, so no single supplier can dictate terms, limiting upward price pressure on Baguio Green’s input costs.

Dependence on Specialized Technology Providers

As Baguio Green Group shifts into advanced recycling and waste-to-energy, it depends more on specialized tech suppliers whose patented machinery and IP raise switching costs; global waste-to-energy equipment spend hit about $8.4bn in 2024, so alternatives are scarce and pricey.

Labor Market Dynamics and Costs

Labor is central to Baguio Green Group’s environmental hygiene and horticulture work in Hong Kong, where 2024 median wage pressures—HKD 40–50 per hour in manual services—and a 3.6% citywide labor shortage in low-skilled roles raise supplier-side costs. Statutory minimum wage increases (last raised to HKD 40.5/hr on 1 May 2023) and tight recruitment push total labor spend higher, so the firm offsets through automation, productivity improvements, and route optimization to protect margins.

Fuel and Energy Price Volatility

Operating a large fleet makes Baguio Green Group highly exposed to global fuel swings; Brent crude averaged 85 USD/barrel in 2025, so a 10% rise raises diesel costs ~6–8% for fleet ops.

Energy is a traded commodity beyond Baguio’s control; local utility tariffs in the Philippines climbed 4.3% year-on-year in 2024, showing regulator limits to price relief.

Sudden spikes cut operating margins unless hedged; a simple hedge covering 50% of fuel needs could cap cost exposure but costs ~2–3% of annual fuel spend to implement.

- Brent 2025 avg: 85 USD/barrel

- PH utility tariffs +4.3% in 2024

- 10% fuel rise → ~6–8% diesel cost rise

- 50% hedge costs ~2–3% of fuel spend

Availability of Land and Waste Facilities

Access to waste transfer stations and processing facilities in Hong Kong is dominated by government bodies and a few major operators, who in 2024 controlled over 80% of licensed non-inert waste sites, giving them pricing and scheduling leverage over firms like Baguio Green Group.

Hong Kong’s land supply is tight—total land area 1,104 km2 with built-up land expansion under strict limits—so space for recycling is scarce; limited site availability raises fixed costs and gate fees for recyclers.

Scarcity of sites translates to operational risk: operators managing facilities can prioritize clients, set throughput windows, and impose fees, increasing supplier bargaining power and compressing margins for waste management firms.

- 80%+ licensed site concentration (2024)

- Hong Kong land area 1,104 km2 (statutory)

- Higher gate fees raise OPEX and capex needs

- Facility control enables prioritization, scheduling leverage

Supply squeeze: site concentration, wage & fuel pressure bite margins; hedges trim risk

Suppliers have mixed power: commoditized inputs (chemicals, PPE) keep prices competitive, but specialized waste‑to‑energy equipment, scarce HK transfer sites (80%+ control in 2024), rising local wages (HKD 40.5/hr min since 1 May 2023) and fuel volatility (Brent ~85 USD/bbl in 2025) raise switching costs and squeeze margins; partial hedges (~2–3% of fuel spend) can cap exposure.

| Metric | Value |

|---|---|

| Site concentration (HK, 2024) | 80%+ |

| Min wage HK | HKD 40.5/hr (1 May 2023) |

| Brent (2025 avg) | 85 USD/bbl |

| Hedge cost | 2–3% fuel spend |

What is included in the product

Tailored Porter's Five Forces analysis for Baguio Green Group revealing competitive pressures, buyer/supplier power, threats from substitutes and new entrants, and strategic levers that protect or erode its market position.

A concise Porter's Five Forces snapshot for Baguio Green Group—translate complex competitive dynamics into quick strategic actions to relieve analysis bottlenecks.

Customers Bargaining Power

Concentration of Government Contracts

Price Sensitivity in Private Sector Cleaning

Commercial and residential clients, including property managers, treat cleaning as a commodity, making price the main purchase driver; industry surveys show 62% of facility managers prioritized cost in 2024 procurement decisions.

High price sensitivity means a 3–5% lower bid can trigger switching; churn rose 14% in UK/EU cleaning markets in 2023 when discounting increased.

Baguio Green must show measurable service quality—SLA uptime, audit scores—or tech like IoT sensors and digital reporting to justify 8–12% price premiums.

Low Switching Costs for Standardized Services

For basic environmental hygiene and landscaping, switching from Baguio Green Group to a rival is inexpensive—procurement surveys show average switching costs under US$500 per contract for mid‑size buildings in 2024, and 62% of facility managers report price and service speed drive changes.

There are minimal proprietary barriers—no exclusive tech or long equipment lock‑ins—so churn risk rises at contract expiry unless performance stays high; BGG saw renewal rates fall from 78% in 2022 to 71% in 2024 when response times slipped.

Increasing Demand for ESG Compliance

Corporate clients now tie 40–60% of supplier selection to ESG scores, pushing Baguio Green Group to supply granular sustainability reports and third-party verified emissions data to keep contracts.

Customers use procurement levers to require lower Scope 1–3 emissions, circular product uptake, and transparent recycling KPIs, forcing providers to invest in greener tech and traceability.

Baguio must meet these demands—else risk losing large accounts worth an estimated 30–45% of annual revenue—to stay a preferred partner.

- 40–60% supplier ESG weight

- 30–45% revenue at risk

- require Scope 1–3 data

- mandate circularity & KPIs

Tendering and Periodic Contract Cycles

The bulk of Baguio Green Group’s revenue comes from fixed-term contracts re-tendered every 2–5 years, giving customers routine chances to renegotiate or switch suppliers; in 2024 roughly 68% of group revenue was tied to such contracts.

Frequent bidding cycles and transparent procurement—public tenders and sealed bids common in the Philippines—keep pricing pressure high and shift negotiating leverage to buyers, compressing margins during renewal periods.

Buyers’ leverage: tenders, price pressure & ESG put 30–45% of Baguio revenue at risk

Buyers hold strong leverage: public clients (≈35% revenue FY2024) use competitive tenders with ~12% average discount, while 68% of revenue comes from 2–5 year re‑tendered contracts; price-driven commercial clients (62% prioritize cost) swap on 3–5% price gaps; ESG now counts 40–60% in selections, putting 30–45% of revenue at risk if Baguio fails to supply Scope 1–3 data and circularity KPIs.

| Metric | Value (2024) |

|---|---|

| Public client share | ≈35% |

| Revenue from fixed-term contracts | ≈68% |

| Avg public procurement discount | ~12% |

| Cost-priority buyers | 62% |

| ESG weight in selection | 40–60% |

| Revenue at ESG risk | 30–45% |

Full Version Awaits

Baguio Green Group Porter's Five Forces Analysis

This preview shows the exact Baguio Green Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written analysis you'll get—fully formatted and ready for download and use the moment you buy.

No mockups or samples; this is the final, ready-to-use file and you’ll have instant access to this exact document once payment is completed.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Baguio Green Group faces moderate buyer power and supplier concentration, while regulatory shifts and capital intensity raise entry barriers; competitive rivalry is high among diversified waste-to-energy and recycling players, and substitutes pressure margins from traditional waste services and emerging circular solutions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Baguio Green Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Equipment and Consumable Market

Primary inputs for Baguio Green Group—cleaning chemicals, protective gear, and specialized waste-collection vehicles—are largely standardized and supplied by numerous global and regional manufacturers, so vendor switching is straightforward.

Market fragmentation keeps supplier concentration low: top 5 global chemical suppliers held about 28% market share in 2024, so no single supplier can dictate terms, limiting upward price pressure on Baguio Green’s input costs.

Dependence on Specialized Technology Providers

As Baguio Green Group shifts into advanced recycling and waste-to-energy, it depends more on specialized tech suppliers whose patented machinery and IP raise switching costs; global waste-to-energy equipment spend hit about $8.4bn in 2024, so alternatives are scarce and pricey.

Labor Market Dynamics and Costs

Labor is central to Baguio Green Group’s environmental hygiene and horticulture work in Hong Kong, where 2024 median wage pressures—HKD 40–50 per hour in manual services—and a 3.6% citywide labor shortage in low-skilled roles raise supplier-side costs. Statutory minimum wage increases (last raised to HKD 40.5/hr on 1 May 2023) and tight recruitment push total labor spend higher, so the firm offsets through automation, productivity improvements, and route optimization to protect margins.

Fuel and Energy Price Volatility

Operating a large fleet makes Baguio Green Group highly exposed to global fuel swings; Brent crude averaged 85 USD/barrel in 2025, so a 10% rise raises diesel costs ~6–8% for fleet ops.

Energy is a traded commodity beyond Baguio’s control; local utility tariffs in the Philippines climbed 4.3% year-on-year in 2024, showing regulator limits to price relief.

Sudden spikes cut operating margins unless hedged; a simple hedge covering 50% of fuel needs could cap cost exposure but costs ~2–3% of annual fuel spend to implement.

- Brent 2025 avg: 85 USD/barrel

- PH utility tariffs +4.3% in 2024

- 10% fuel rise → ~6–8% diesel cost rise

- 50% hedge costs ~2–3% of fuel spend

Availability of Land and Waste Facilities

Access to waste transfer stations and processing facilities in Hong Kong is dominated by government bodies and a few major operators, who in 2024 controlled over 80% of licensed non-inert waste sites, giving them pricing and scheduling leverage over firms like Baguio Green Group.

Hong Kong’s land supply is tight—total land area 1,104 km2 with built-up land expansion under strict limits—so space for recycling is scarce; limited site availability raises fixed costs and gate fees for recyclers.

Scarcity of sites translates to operational risk: operators managing facilities can prioritize clients, set throughput windows, and impose fees, increasing supplier bargaining power and compressing margins for waste management firms.

- 80%+ licensed site concentration (2024)

- Hong Kong land area 1,104 km2 (statutory)

- Higher gate fees raise OPEX and capex needs

- Facility control enables prioritization, scheduling leverage

Supply squeeze: site concentration, wage & fuel pressure bite margins; hedges trim risk

Suppliers have mixed power: commoditized inputs (chemicals, PPE) keep prices competitive, but specialized waste‑to‑energy equipment, scarce HK transfer sites (80%+ control in 2024), rising local wages (HKD 40.5/hr min since 1 May 2023) and fuel volatility (Brent ~85 USD/bbl in 2025) raise switching costs and squeeze margins; partial hedges (~2–3% of fuel spend) can cap exposure.

| Metric | Value |

|---|---|

| Site concentration (HK, 2024) | 80%+ |

| Min wage HK | HKD 40.5/hr (1 May 2023) |

| Brent (2025 avg) | 85 USD/bbl |

| Hedge cost | 2–3% fuel spend |

What is included in the product

Tailored Porter's Five Forces analysis for Baguio Green Group revealing competitive pressures, buyer/supplier power, threats from substitutes and new entrants, and strategic levers that protect or erode its market position.

A concise Porter's Five Forces snapshot for Baguio Green Group—translate complex competitive dynamics into quick strategic actions to relieve analysis bottlenecks.

Customers Bargaining Power

Concentration of Government Contracts

Price Sensitivity in Private Sector Cleaning

Commercial and residential clients, including property managers, treat cleaning as a commodity, making price the main purchase driver; industry surveys show 62% of facility managers prioritized cost in 2024 procurement decisions.

High price sensitivity means a 3–5% lower bid can trigger switching; churn rose 14% in UK/EU cleaning markets in 2023 when discounting increased.

Baguio Green must show measurable service quality—SLA uptime, audit scores—or tech like IoT sensors and digital reporting to justify 8–12% price premiums.

Low Switching Costs for Standardized Services

For basic environmental hygiene and landscaping, switching from Baguio Green Group to a rival is inexpensive—procurement surveys show average switching costs under US$500 per contract for mid‑size buildings in 2024, and 62% of facility managers report price and service speed drive changes.

There are minimal proprietary barriers—no exclusive tech or long equipment lock‑ins—so churn risk rises at contract expiry unless performance stays high; BGG saw renewal rates fall from 78% in 2022 to 71% in 2024 when response times slipped.

Increasing Demand for ESG Compliance

Corporate clients now tie 40–60% of supplier selection to ESG scores, pushing Baguio Green Group to supply granular sustainability reports and third-party verified emissions data to keep contracts.

Customers use procurement levers to require lower Scope 1–3 emissions, circular product uptake, and transparent recycling KPIs, forcing providers to invest in greener tech and traceability.

Baguio must meet these demands—else risk losing large accounts worth an estimated 30–45% of annual revenue—to stay a preferred partner.

- 40–60% supplier ESG weight

- 30–45% revenue at risk

- require Scope 1–3 data

- mandate circularity & KPIs

Tendering and Periodic Contract Cycles

The bulk of Baguio Green Group’s revenue comes from fixed-term contracts re-tendered every 2–5 years, giving customers routine chances to renegotiate or switch suppliers; in 2024 roughly 68% of group revenue was tied to such contracts.

Frequent bidding cycles and transparent procurement—public tenders and sealed bids common in the Philippines—keep pricing pressure high and shift negotiating leverage to buyers, compressing margins during renewal periods.

Buyers’ leverage: tenders, price pressure & ESG put 30–45% of Baguio revenue at risk

Buyers hold strong leverage: public clients (≈35% revenue FY2024) use competitive tenders with ~12% average discount, while 68% of revenue comes from 2–5 year re‑tendered contracts; price-driven commercial clients (62% prioritize cost) swap on 3–5% price gaps; ESG now counts 40–60% in selections, putting 30–45% of revenue at risk if Baguio fails to supply Scope 1–3 data and circularity KPIs.

| Metric | Value (2024) |

|---|---|

| Public client share | ≈35% |

| Revenue from fixed-term contracts | ≈68% |

| Avg public procurement discount | ~12% |

| Cost-priority buyers | 62% |

| ESG weight in selection | 40–60% |

| Revenue at ESG risk | 30–45% |

Full Version Awaits

Baguio Green Group Porter's Five Forces Analysis

This preview shows the exact Baguio Green Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written analysis you'll get—fully formatted and ready for download and use the moment you buy.

No mockups or samples; this is the final, ready-to-use file and you’ll have instant access to this exact document once payment is completed.