Bahnhof Porter's Five Forces Analysis

Don't Miss the Bigger Picture

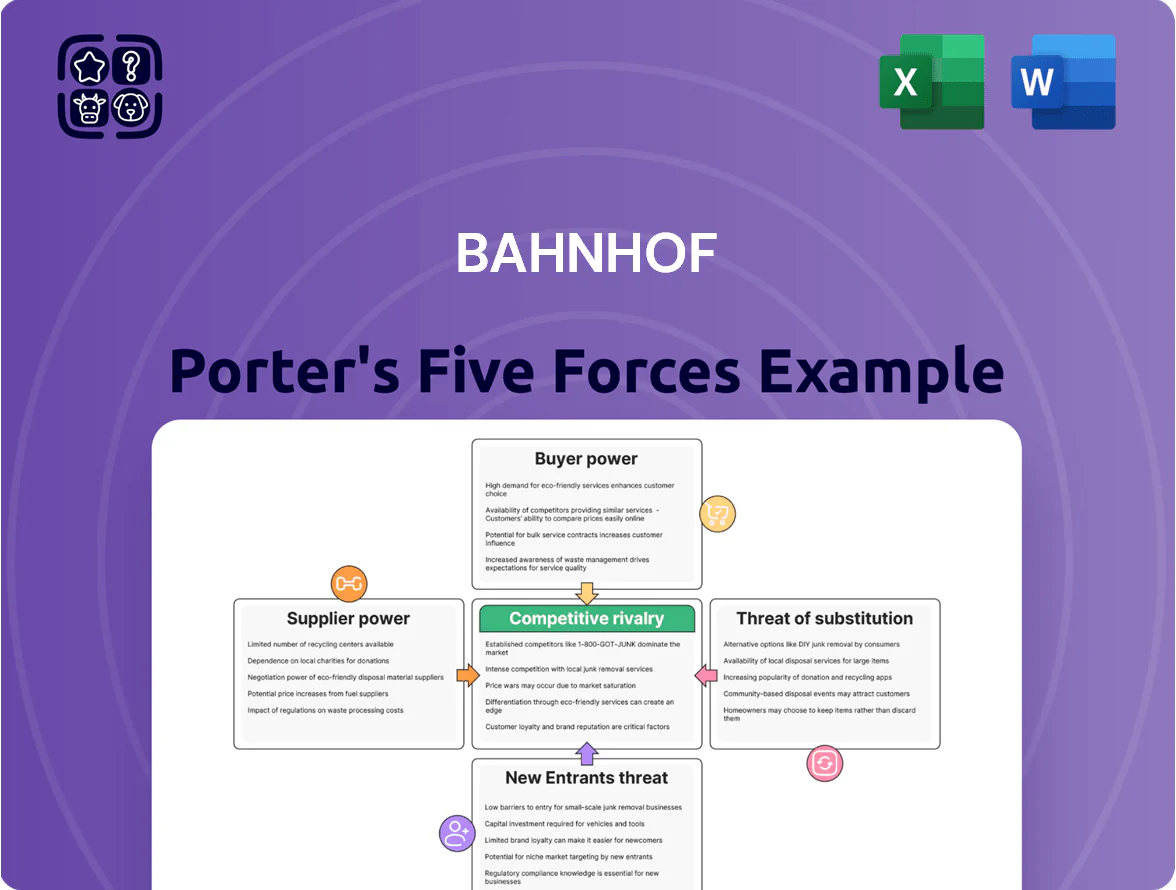

Bahnhof faces intense competitive pressure from large telecom incumbents and disruptive cloud providers, while strong buyer demand for privacy and high-speed connectivity shapes pricing power.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bahnhof’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Infrastructure Hardware Vendors

Bahnhof relies on a handful of global suppliers for high-end routers and optical gear, tying its 100G/400G rollout to vendors’ tech roadmaps; Cisco, Juniper and Ciena control ~60–70% of core routing/packet-optical market (2024 IDC).

High switching costs—typical multi-year interoperability and migration spend of €10–30m for backbone upgrades—keep supplier leverage high.

To mitigate supply shocks and price volatility seen in 2021–24 (chip shortages, freight spikes), Bahnhof needs multi-year supply contracts and volume commitments to secure capacity and favorable pricing.

Dependency on Municipal Fiber Networks

A large share of Bahnhof’s residential customers use Sweden’s municipal fiber networks (stadsnät), many of which act as local monopolies and set wholesale access prices and SLAs. In 2024 roughly 60% of Swedish fiber households connected via stadsnät, so Bahnhof faces limited negotiating leverage on infrastructure costs. Those fixed wholesale tariffs compress ISP gross margins and transfer pricing risk to retail providers, boosting supplier power over Bahnhof’s profitability.

Energy Costs and Data Center Utility Providers

Operating high-density sites like Pionen makes Bahnhof highly dependent on utility providers; electricity typically accounts for 25–35% of colocation OPEX, so suppliers hold strong leverage.

Nordic power volatility in 2025 saw quarterly wholesale prices spike to about EUR 180/MWh in Jan 2025 vs EUR 45/MWh a year earlier, underscoring supplier influence on margins.

Bahnhof’s green-energy sourcing supports branding, but no immediate large-scale alternatives (on-site generation/storage) exist, keeping supplier power high.

Tier-1 IP Transit Providers

Bahnhof must buy IP transit from global Tier-1 carriers to keep low latency and worldwide reach, exposing it to those carriers’ pricing despite Bahnhof’s strong backbone.

Market competition (many carriers, 2024 global IP transit market ~USD 19.5B) limits price setting, but transit remains non-substitutable for international reach.

- Depends on Tier-1 for global reach

- 2024 market ~USD 19.5B

- Robust backbone lowers but doesn’t remove dependence

- Competition softens but service is essential

Specialized Cybersecurity Software Licenses

Bahnhof’s privacy-first network depends on specialized cybersecurity licenses—encryption, endpoint and SIEM tools—from a few dominant vendors, giving suppliers strong bargaining power as of 2025.

With ransomware incidents up 58% in 2024 and enterprise security spend rising to an estimated €150–€200 per user annually, timely updates and threat intelligence are non-negotiable; switching carries high risk and integration cost.

- Concentrated vendors raise price and terms risk

- Switching costs: integration, testing, compliance

- 2024: ransomware +58%; security spend €150–€200/user

High supplier power: 60–70% vendor control, costly backbones, rising colo OPEX

Supplier power is high: core routing/optical vendors (Cisco, Juniper, Ciena) control ~60–70% (IDC 2024), backbone upgrades cost €10–30m, stadsnät serve ~60% of Swedish fiber homes (2024) compressing wholesale margins, electricity is 25–35% of colo OPEX with Jan 2025 peak ~EUR180/MWh, and global IP transit market ~USD19.5B (2024) remains essential.

| Metric | Value |

|---|---|

| Routing/optical share | 60–70% (IDC 2024) |

| Backbone upgrade cost | €10–30m |

| Swedish fiber via stadsnät | ~60% (2024) |

| Colo electricity | 25–35% OPEX; EUR180/MWh Jan 2025 |

| IP transit market | ~USD19.5B (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Bahnhof that uncovers competitive drivers, supplier and buyer power, entry barriers, substitution risks, and emerging threats—delivering strategic insights to assess pricing power, profitability, and defensive opportunities within its market.

A concise, one-sheet Porter's Five Forces summary for Bahnhof that highlights competitive pressures and relief levers—ideal for quick strategic decisions and slide decks.

Customers Bargaining Power

Low Switching Costs for Residential Users

The Swedish broadband market has high transparency and low switching friction, especially in open fiber areas where 70% of households could swap ISPs via operator portals in 2024; that ease forces Bahnhof to keep prices competitive and SLAs tight to avoid churn.

High Price Sensitivity in the Consumer Market

Corporate Demand for Custom SLAs

Business and enterprise clients demand custom SLAs specifying uptime (often 99.99%) and sub-hour support response times; these contracts can represent 40–60% of Bahnhof’s recurring revenue for large accounts as of 2025.

Because losing a single corporate client can cut annual recurring revenue by millions SEK, these customers wield strong bargaining power and push for price, penalties, and tailored security clauses.

Bahnhof must therefore offer flexible, high-availability packages and enterprise-grade SLAs to retain accounts and protect margins.

Niche Loyalty Based on Privacy Advocacy

- Less price-sensitive, high retention but high expectations

- Vocal: drives media and social backlash

- Churn risk: could hit double-digit % among advocates

- Financial impact: SEK ~2,400 ARPU x lost accounts = material

Information Symmetry and Comparison Tools

In 2025, online comparison platforms let customers instantly compare Bahnhof with Telia, Telenor, and Tele2, increasing information symmetry and constraining Bahnhof’s ability to hide price hikes or service gaps.

Customers use public metrics—average latency, uptime, and CSAT—plus price-per-Mbps; 62% of Swedish broadband shoppers reported switching after checking comparisons in 2024, boosting bargaining power.

- Instant price/service comparisons

- 62% of switchers after checks (2024 survey)

- Public uptime/latency metrics raise churn risk

- Limits on opaque pricing or hidden fees

Swedish customers wield strong pricing power—70% swap ISPs, 56% driven by price

Customers in Sweden have strong bargaining power: 70% can swap ISPs via open fiber portals (2024), 62% switch after online comparisons, and price drives ~56% of choices; Bahnhof faces discounting by Telia/Com Hem up to 40% (2024) and ARPU risk (SEK 2,400), while enterprise contracts (40–60% recurring revenue) demand 99.99% SLAs.

| Metric | 2024–25 |

|---|---|

| Open-fiber swap | 70% |

| Switch after compare | 62% |

| Price-driven buyers | 56% |

| Max competitor discount | 40% |

| Retail ARPU | SEK 2,400 |

| Enterprise share | 40–60% |

What You See Is What You Get

Bahnhof Porter's Five Forces Analysis

This preview shows the exact Bahnhof Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written file; once you complete your purchase, you’ll get instant access to this same deliverable for immediate application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Bahnhof faces intense competitive pressure from large telecom incumbents and disruptive cloud providers, while strong buyer demand for privacy and high-speed connectivity shapes pricing power.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bahnhof’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Infrastructure Hardware Vendors

Bahnhof relies on a handful of global suppliers for high-end routers and optical gear, tying its 100G/400G rollout to vendors’ tech roadmaps; Cisco, Juniper and Ciena control ~60–70% of core routing/packet-optical market (2024 IDC).

High switching costs—typical multi-year interoperability and migration spend of €10–30m for backbone upgrades—keep supplier leverage high.

To mitigate supply shocks and price volatility seen in 2021–24 (chip shortages, freight spikes), Bahnhof needs multi-year supply contracts and volume commitments to secure capacity and favorable pricing.

Dependency on Municipal Fiber Networks

A large share of Bahnhof’s residential customers use Sweden’s municipal fiber networks (stadsnät), many of which act as local monopolies and set wholesale access prices and SLAs. In 2024 roughly 60% of Swedish fiber households connected via stadsnät, so Bahnhof faces limited negotiating leverage on infrastructure costs. Those fixed wholesale tariffs compress ISP gross margins and transfer pricing risk to retail providers, boosting supplier power over Bahnhof’s profitability.

Energy Costs and Data Center Utility Providers

Operating high-density sites like Pionen makes Bahnhof highly dependent on utility providers; electricity typically accounts for 25–35% of colocation OPEX, so suppliers hold strong leverage.

Nordic power volatility in 2025 saw quarterly wholesale prices spike to about EUR 180/MWh in Jan 2025 vs EUR 45/MWh a year earlier, underscoring supplier influence on margins.

Bahnhof’s green-energy sourcing supports branding, but no immediate large-scale alternatives (on-site generation/storage) exist, keeping supplier power high.

Tier-1 IP Transit Providers

Bahnhof must buy IP transit from global Tier-1 carriers to keep low latency and worldwide reach, exposing it to those carriers’ pricing despite Bahnhof’s strong backbone.

Market competition (many carriers, 2024 global IP transit market ~USD 19.5B) limits price setting, but transit remains non-substitutable for international reach.

- Depends on Tier-1 for global reach

- 2024 market ~USD 19.5B

- Robust backbone lowers but doesn’t remove dependence

- Competition softens but service is essential

Specialized Cybersecurity Software Licenses

Bahnhof’s privacy-first network depends on specialized cybersecurity licenses—encryption, endpoint and SIEM tools—from a few dominant vendors, giving suppliers strong bargaining power as of 2025.

With ransomware incidents up 58% in 2024 and enterprise security spend rising to an estimated €150–€200 per user annually, timely updates and threat intelligence are non-negotiable; switching carries high risk and integration cost.

- Concentrated vendors raise price and terms risk

- Switching costs: integration, testing, compliance

- 2024: ransomware +58%; security spend €150–€200/user

High supplier power: 60–70% vendor control, costly backbones, rising colo OPEX

Supplier power is high: core routing/optical vendors (Cisco, Juniper, Ciena) control ~60–70% (IDC 2024), backbone upgrades cost €10–30m, stadsnät serve ~60% of Swedish fiber homes (2024) compressing wholesale margins, electricity is 25–35% of colo OPEX with Jan 2025 peak ~EUR180/MWh, and global IP transit market ~USD19.5B (2024) remains essential.

| Metric | Value |

|---|---|

| Routing/optical share | 60–70% (IDC 2024) |

| Backbone upgrade cost | €10–30m |

| Swedish fiber via stadsnät | ~60% (2024) |

| Colo electricity | 25–35% OPEX; EUR180/MWh Jan 2025 |

| IP transit market | ~USD19.5B (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Bahnhof that uncovers competitive drivers, supplier and buyer power, entry barriers, substitution risks, and emerging threats—delivering strategic insights to assess pricing power, profitability, and defensive opportunities within its market.

A concise, one-sheet Porter's Five Forces summary for Bahnhof that highlights competitive pressures and relief levers—ideal for quick strategic decisions and slide decks.

Customers Bargaining Power

Low Switching Costs for Residential Users

The Swedish broadband market has high transparency and low switching friction, especially in open fiber areas where 70% of households could swap ISPs via operator portals in 2024; that ease forces Bahnhof to keep prices competitive and SLAs tight to avoid churn.

High Price Sensitivity in the Consumer Market

Corporate Demand for Custom SLAs

Business and enterprise clients demand custom SLAs specifying uptime (often 99.99%) and sub-hour support response times; these contracts can represent 40–60% of Bahnhof’s recurring revenue for large accounts as of 2025.

Because losing a single corporate client can cut annual recurring revenue by millions SEK, these customers wield strong bargaining power and push for price, penalties, and tailored security clauses.

Bahnhof must therefore offer flexible, high-availability packages and enterprise-grade SLAs to retain accounts and protect margins.

Niche Loyalty Based on Privacy Advocacy

- Less price-sensitive, high retention but high expectations

- Vocal: drives media and social backlash

- Churn risk: could hit double-digit % among advocates

- Financial impact: SEK ~2,400 ARPU x lost accounts = material

Information Symmetry and Comparison Tools

In 2025, online comparison platforms let customers instantly compare Bahnhof with Telia, Telenor, and Tele2, increasing information symmetry and constraining Bahnhof’s ability to hide price hikes or service gaps.

Customers use public metrics—average latency, uptime, and CSAT—plus price-per-Mbps; 62% of Swedish broadband shoppers reported switching after checking comparisons in 2024, boosting bargaining power.

- Instant price/service comparisons

- 62% of switchers after checks (2024 survey)

- Public uptime/latency metrics raise churn risk

- Limits on opaque pricing or hidden fees

Swedish customers wield strong pricing power—70% swap ISPs, 56% driven by price

Customers in Sweden have strong bargaining power: 70% can swap ISPs via open fiber portals (2024), 62% switch after online comparisons, and price drives ~56% of choices; Bahnhof faces discounting by Telia/Com Hem up to 40% (2024) and ARPU risk (SEK 2,400), while enterprise contracts (40–60% recurring revenue) demand 99.99% SLAs.

| Metric | 2024–25 |

|---|---|

| Open-fiber swap | 70% |

| Switch after compare | 62% |

| Price-driven buyers | 56% |

| Max competitor discount | 40% |

| Retail ARPU | SEK 2,400 |

| Enterprise share | 40–60% |

What You See Is What You Get

Bahnhof Porter's Five Forces Analysis

This preview shows the exact Bahnhof Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written file; once you complete your purchase, you’ll get instant access to this same deliverable for immediate application.