BAIC Motor PESTLE Analysis

Your Shortcut to Market Insight Starts Here

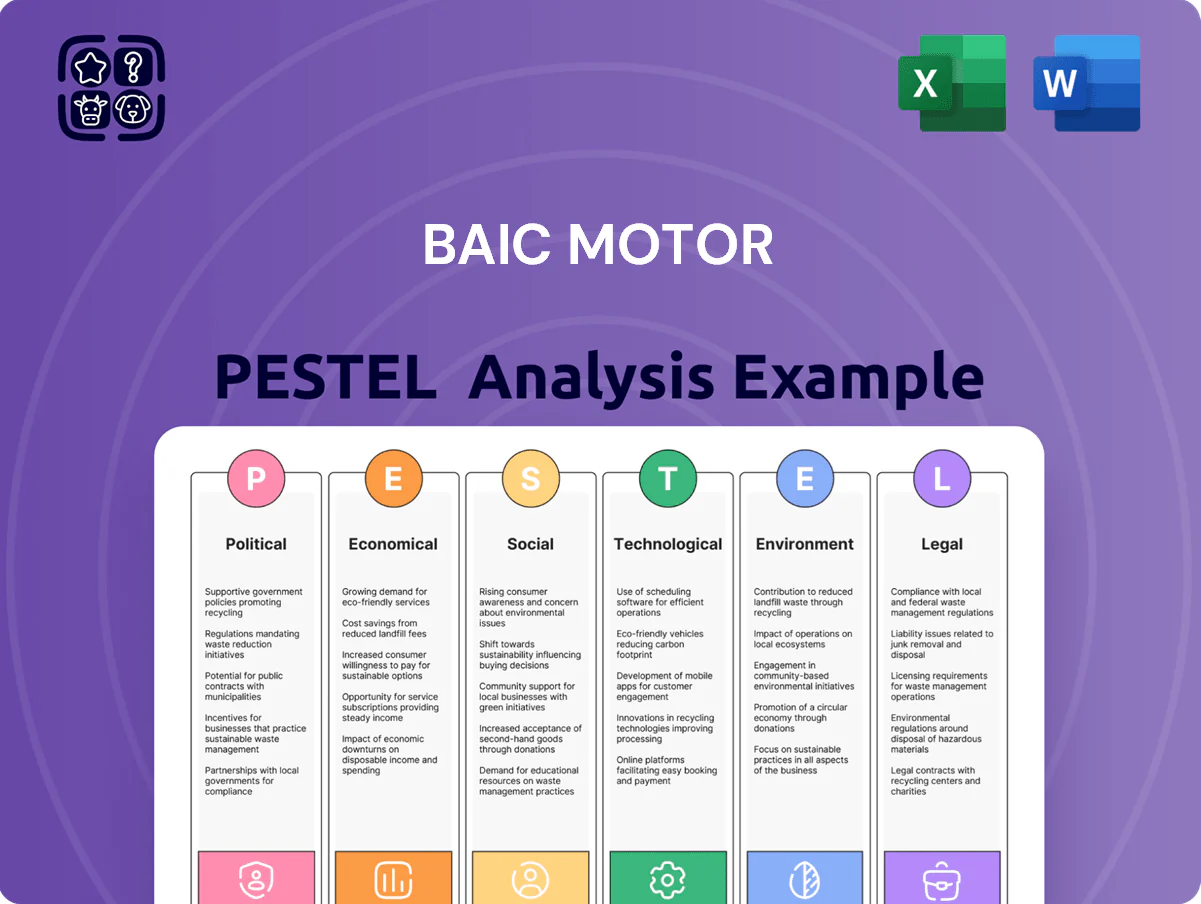

Navigate BAIC Motor’s external landscape with our concise PESTLE snapshot—identify regulatory risks, economic headwinds, technological shifts, social trends, and environmental pressures shaping its strategy; for investors and strategists needing depth, buy the full PESTLE analysis to access actionable, fully sourced insights and editable deliverables ready for decision-making.

Political factors

State Ownership and Government Alignment

As a Beijing Municipal state-owned enterprise, BAIC Motor leverages alignment with national industrial policy, aiding access to land and capital—BAIC reported RMB 18.2 billion cash and equivalents in 2024, supporting investments in Beijing–Tianjin–Hebei projects—and benefits from preferential infrastructure ties within the cluster. This state link also imposes political mandates, risking directives favoring social stability or national EV targets over short-term profitability, affecting ROE and dividend policies.

Geopolitical Trade Barriers and Tariffs

BAIC Motor faces rising international trade restrictions—EU and US tariffs on Chinese-made EVs reached up to 25% in 2024, squeezing margins and reducing export competitiveness; BAIC exported only 3.2% of 2024 vehicle volumes to Europe/US combined.

These protectionist barriers force strategic shifts toward localized production or assembly in neutral markets like Mexico or ASEAN; localized plants can cut tariff impact and transport costs by an estimated 10–15% per vehicle.

Management must balance tariff mitigation with preserving Chinese cost advantages—domestic COGS remain ~20–30% lower than Western peers—prompting joint ventures, CKD assembly, and capex reallocation to overseas facilities.

Evolution of NEV Subsidy Policies

China phased out national NEV purchase subsidies by end-2023, shifting funding to charging infrastructure and R&D grants; central and provincial programs allocated over CNY 120 billion for grid and charging deployment in 2024–25, favoring tech leadership over volume incentives.

BAIC must rework financial models—capital expenditure toward EV platforms, software and battery R&D—anticipating lower unit-margin relief but higher long-term IP value; assume R&D spend rising by ~15–20% vs 2023.

Continued reliance on favorable local policies remains critical: Beijing and Hebei offered targeted support packages worth over CNY 8–12 billion in 2024 to sustain local NEV producers, directly impacting BAIC’s competitiveness and plant-level economics.

Strategic International Partnerships

The stability of BAIC Motor's joint ventures, notably the long-standing Beijing Benz partnership that contributed roughly RMB 18.6 billion in 2024 revenue to BAIC Group, underpins both sales and technology gains.

As China-West geopolitical tensions ebb and flow, maintaining a balanced relationship with German partners like Mercedes-Benz is essential to secure technology transfer and continued investment commitments.

Bilateral diplomatic relations directly affect licensing, components supply chains and prospective R&D funding, risking delays to EV platform rollouts and capital inflows if relations sour.

- 2024 Beijing Benz revenue approx RMB 18.6bn to BAIC Group

- JV performance tied to China-Germany diplomatic climate

- Political shifts can constrain tech transfer, R&D and investment

Belt and Road Initiative Integration

BAIC Motor leverages the Belt and Road Initiative to expand in Southeast Asia, the Middle East and Africa, where Chinese FDI rose to USD 41.6bn in 2024, easing entry and supporting exports of excess capacity from its 2023 global output of ~1.1m vehicles.

The company aligns export strategies with Beijing’s infrastructure financing—ADB/Chinese-backed projects increased market access—securing preferential procurement and long-term supply contracts in target markets.

- 2024 Chinese FDI in BRI regions: USD 41.6bn

- BAIC global production 2023: ~1.1m vehicles

- Favorable political climate vs. Western markets: higher procurement of Chinese autos

BAIC: Strong state cash and JV support vs. 25% EU/US EV tariffs, low exports

BAIC benefits from state backing (RMB 18.2bn cash 2024) and local support (CNY 8–12bn packages), but faces 2024 EU/US EV tariffs up to 25% and exported 3.2% of 2024 volumes; China phased national NEV subsidies end-2023, shifting CNY 120bn+ to charging/R&D; Beijing Benz JV contributed ~RMB 18.6bn 2024, tying tech access to China‑Germany ties.

| Metric | Value |

|---|---|

| Cash (2024) | RMB 18.2bn |

| Beijing Benz rev | RMB 18.6bn |

| Exports to EU/US | 3.2% |

| EU/US tariffs 2024 | up to 25% |

| Charging/R&D funding 2024–25 | CNY 120bn+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect BAIC Motor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable BAIC Motor PESTLE snapshot that highlights regulatory, economic, and technological risks and opportunities for quick alignment in meetings or investor decks.

Economic factors

Domestic Market Saturation and Price Wars

The Chinese automotive market has entered intense competition with OEMs engaging in price wars that compressed industry gross margins to ~12% in 2024, squeezing incumbents like BAIC Motor (2024 net margin ~1.8%).

Economic cooling—GDP growth slowing to ~5.2% in 2024 and weaker auto sales (-2.5% y/y nationally)—has damped consumer spending, forcing BAIC to streamline costs and cut capex.

Through 2025 BAIC faces the tradeoff of defending market share amid ~20% EV/NEV discounting pressures while restoring sustainable profitability via mix improvement and efficiency gains.

Fluctuations in Raw Material Costs

Volatility in lithium, cobalt and nickel prices directly raises BAIC Motor’s NEV production costs; lithium carbonate surged ~120% from 2020–2023 before easing 2024–25, keeping input-cost risk elevated. Supply chains have stabilized versus 2021–22 shortages, yet a sharp geopolitical shock or FX swing could spike costs. BAIC mitigates risk via strategic hedging and multi-year supply contracts covering an estimated 60–70% of critical material needs.

Interest Rate and Financing Environment

People's Bank of China rate cuts and policy easing directly lower BAIC Motor's borrowing costs and make auto loans cheaper; after the PBOC cut the 1-year LPR to 3.45% in Aug 2024, consumer loan affordability improved and China auto sales rose ~5% YoY in H2 2024. Lower rates boost BAIC's retail demand, so the company adjusts captive financing rates and extended loan tenors while targeting net debt reduction from RMB 48.2bn in 2023.

Currency Exchange Rate Volatility

As BAIC Motor expands international sales and global sourcing, Renminbi volatility versus the US Dollar and Euro poses financial risk; RMB fell about 4.8% versus USD in 2024, widening margins uncertainty for exports and imports.

A weaker RMB boosts export competitiveness but raises costs for imported technology and premium parts, which represented roughly 12% of COGS in 2023–2024 for Chinese automakers.

BAIC uses currency derivatives and local-currency billing in markets like Russia and Southeast Asia to hedge exposure, reducing FX-driven earnings volatility by an estimated 30–40% in recent hedge accounting periods.

- RMB -4.8% vs USD in 2024: export competitiveness up

- Imported tech/premium parts ≈12% of COGS increases with weaker RMB

- Hedging/local billing cut FX earnings volatility ~30–40%

Economic Growth and Consumer Confidence

China's GDP growth slowed to an estimated 4.2% in 2025, directly influencing passenger vehicle demand across segments and pressuring premium sales.

Macroeconomic softness shifted buyers toward value models; EV and compact SUV sales rose 6.8% while luxury volumes fell ~9% year-on-year in 2025.

BAIC Motor must pivot product mix and pricing agility to match reduced purchasing power, emphasizing affordable EVs and financing offers to protect volumes.

- 2025 GDP ~4.2% — premium demand down ~9%

- Value/compact EVs +6.8% in sales

- Focus: affordable EVs, flexible financing, product-mix shift

Economic slowdown, margin squeeze: BAIC struggles with thin profits and rising NEV costs

Economic slowdown (GDP 2024~5.2%; 2025~4.2%) and price wars cut industry gross margins to ~12% (2024); BAIC net margin ~1.8% (2024), net debt RMB48.2bn (2023). NEV input-cost risk: lithium surge 2020–23 +120%; hedges cover 60–70% inputs, cutting FX volatility ~30–40%. H2 2024 sales +5% after LPR 1yr →3.45%.

| Metric | Value |

|---|---|

| GDP 2025 | 4.2% |

| Industry gross margin 2024 | ~12% |

| BAIC net margin 2024 | ~1.8% |

| Net debt 2023 | RMB48.2bn |

Full Version Awaits

BAIC Motor PESTLE Analysis

The preview shown here is the exact BAIC Motor PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The content and structure visible in this sample are identical to the downloadable file delivered upon payment, with no placeholders or surprises.

Everything displayed is part of the final, professionally structured document you’ll instantly own after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Navigate BAIC Motor’s external landscape with our concise PESTLE snapshot—identify regulatory risks, economic headwinds, technological shifts, social trends, and environmental pressures shaping its strategy; for investors and strategists needing depth, buy the full PESTLE analysis to access actionable, fully sourced insights and editable deliverables ready for decision-making.

Political factors

State Ownership and Government Alignment

As a Beijing Municipal state-owned enterprise, BAIC Motor leverages alignment with national industrial policy, aiding access to land and capital—BAIC reported RMB 18.2 billion cash and equivalents in 2024, supporting investments in Beijing–Tianjin–Hebei projects—and benefits from preferential infrastructure ties within the cluster. This state link also imposes political mandates, risking directives favoring social stability or national EV targets over short-term profitability, affecting ROE and dividend policies.

Geopolitical Trade Barriers and Tariffs

BAIC Motor faces rising international trade restrictions—EU and US tariffs on Chinese-made EVs reached up to 25% in 2024, squeezing margins and reducing export competitiveness; BAIC exported only 3.2% of 2024 vehicle volumes to Europe/US combined.

These protectionist barriers force strategic shifts toward localized production or assembly in neutral markets like Mexico or ASEAN; localized plants can cut tariff impact and transport costs by an estimated 10–15% per vehicle.

Management must balance tariff mitigation with preserving Chinese cost advantages—domestic COGS remain ~20–30% lower than Western peers—prompting joint ventures, CKD assembly, and capex reallocation to overseas facilities.

Evolution of NEV Subsidy Policies

China phased out national NEV purchase subsidies by end-2023, shifting funding to charging infrastructure and R&D grants; central and provincial programs allocated over CNY 120 billion for grid and charging deployment in 2024–25, favoring tech leadership over volume incentives.

BAIC must rework financial models—capital expenditure toward EV platforms, software and battery R&D—anticipating lower unit-margin relief but higher long-term IP value; assume R&D spend rising by ~15–20% vs 2023.

Continued reliance on favorable local policies remains critical: Beijing and Hebei offered targeted support packages worth over CNY 8–12 billion in 2024 to sustain local NEV producers, directly impacting BAIC’s competitiveness and plant-level economics.

Strategic International Partnerships

The stability of BAIC Motor's joint ventures, notably the long-standing Beijing Benz partnership that contributed roughly RMB 18.6 billion in 2024 revenue to BAIC Group, underpins both sales and technology gains.

As China-West geopolitical tensions ebb and flow, maintaining a balanced relationship with German partners like Mercedes-Benz is essential to secure technology transfer and continued investment commitments.

Bilateral diplomatic relations directly affect licensing, components supply chains and prospective R&D funding, risking delays to EV platform rollouts and capital inflows if relations sour.

- 2024 Beijing Benz revenue approx RMB 18.6bn to BAIC Group

- JV performance tied to China-Germany diplomatic climate

- Political shifts can constrain tech transfer, R&D and investment

Belt and Road Initiative Integration

BAIC Motor leverages the Belt and Road Initiative to expand in Southeast Asia, the Middle East and Africa, where Chinese FDI rose to USD 41.6bn in 2024, easing entry and supporting exports of excess capacity from its 2023 global output of ~1.1m vehicles.

The company aligns export strategies with Beijing’s infrastructure financing—ADB/Chinese-backed projects increased market access—securing preferential procurement and long-term supply contracts in target markets.

- 2024 Chinese FDI in BRI regions: USD 41.6bn

- BAIC global production 2023: ~1.1m vehicles

- Favorable political climate vs. Western markets: higher procurement of Chinese autos

BAIC: Strong state cash and JV support vs. 25% EU/US EV tariffs, low exports

BAIC benefits from state backing (RMB 18.2bn cash 2024) and local support (CNY 8–12bn packages), but faces 2024 EU/US EV tariffs up to 25% and exported 3.2% of 2024 volumes; China phased national NEV subsidies end-2023, shifting CNY 120bn+ to charging/R&D; Beijing Benz JV contributed ~RMB 18.6bn 2024, tying tech access to China‑Germany ties.

| Metric | Value |

|---|---|

| Cash (2024) | RMB 18.2bn |

| Beijing Benz rev | RMB 18.6bn |

| Exports to EU/US | 3.2% |

| EU/US tariffs 2024 | up to 25% |

| Charging/R&D funding 2024–25 | CNY 120bn+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect BAIC Motor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable BAIC Motor PESTLE snapshot that highlights regulatory, economic, and technological risks and opportunities for quick alignment in meetings or investor decks.

Economic factors

Domestic Market Saturation and Price Wars

The Chinese automotive market has entered intense competition with OEMs engaging in price wars that compressed industry gross margins to ~12% in 2024, squeezing incumbents like BAIC Motor (2024 net margin ~1.8%).

Economic cooling—GDP growth slowing to ~5.2% in 2024 and weaker auto sales (-2.5% y/y nationally)—has damped consumer spending, forcing BAIC to streamline costs and cut capex.

Through 2025 BAIC faces the tradeoff of defending market share amid ~20% EV/NEV discounting pressures while restoring sustainable profitability via mix improvement and efficiency gains.

Fluctuations in Raw Material Costs

Volatility in lithium, cobalt and nickel prices directly raises BAIC Motor’s NEV production costs; lithium carbonate surged ~120% from 2020–2023 before easing 2024–25, keeping input-cost risk elevated. Supply chains have stabilized versus 2021–22 shortages, yet a sharp geopolitical shock or FX swing could spike costs. BAIC mitigates risk via strategic hedging and multi-year supply contracts covering an estimated 60–70% of critical material needs.

Interest Rate and Financing Environment

People's Bank of China rate cuts and policy easing directly lower BAIC Motor's borrowing costs and make auto loans cheaper; after the PBOC cut the 1-year LPR to 3.45% in Aug 2024, consumer loan affordability improved and China auto sales rose ~5% YoY in H2 2024. Lower rates boost BAIC's retail demand, so the company adjusts captive financing rates and extended loan tenors while targeting net debt reduction from RMB 48.2bn in 2023.

Currency Exchange Rate Volatility

As BAIC Motor expands international sales and global sourcing, Renminbi volatility versus the US Dollar and Euro poses financial risk; RMB fell about 4.8% versus USD in 2024, widening margins uncertainty for exports and imports.

A weaker RMB boosts export competitiveness but raises costs for imported technology and premium parts, which represented roughly 12% of COGS in 2023–2024 for Chinese automakers.

BAIC uses currency derivatives and local-currency billing in markets like Russia and Southeast Asia to hedge exposure, reducing FX-driven earnings volatility by an estimated 30–40% in recent hedge accounting periods.

- RMB -4.8% vs USD in 2024: export competitiveness up

- Imported tech/premium parts ≈12% of COGS increases with weaker RMB

- Hedging/local billing cut FX earnings volatility ~30–40%

Economic Growth and Consumer Confidence

China's GDP growth slowed to an estimated 4.2% in 2025, directly influencing passenger vehicle demand across segments and pressuring premium sales.

Macroeconomic softness shifted buyers toward value models; EV and compact SUV sales rose 6.8% while luxury volumes fell ~9% year-on-year in 2025.

BAIC Motor must pivot product mix and pricing agility to match reduced purchasing power, emphasizing affordable EVs and financing offers to protect volumes.

- 2025 GDP ~4.2% — premium demand down ~9%

- Value/compact EVs +6.8% in sales

- Focus: affordable EVs, flexible financing, product-mix shift

Economic slowdown, margin squeeze: BAIC struggles with thin profits and rising NEV costs

Economic slowdown (GDP 2024~5.2%; 2025~4.2%) and price wars cut industry gross margins to ~12% (2024); BAIC net margin ~1.8% (2024), net debt RMB48.2bn (2023). NEV input-cost risk: lithium surge 2020–23 +120%; hedges cover 60–70% inputs, cutting FX volatility ~30–40%. H2 2024 sales +5% after LPR 1yr →3.45%.

| Metric | Value |

|---|---|

| GDP 2025 | 4.2% |

| Industry gross margin 2024 | ~12% |

| BAIC net margin 2024 | ~1.8% |

| Net debt 2023 | RMB48.2bn |

Full Version Awaits

BAIC Motor PESTLE Analysis

The preview shown here is the exact BAIC Motor PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The content and structure visible in this sample are identical to the downloadable file delivered upon payment, with no placeholders or surprises.

Everything displayed is part of the final, professionally structured document you’ll instantly own after checkout.