Baioo Family Interactive SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Baioo Family Interactive shows niche strengths in family-focused content and agile digital distribution, but faces scalability and monetization headwinds amid fierce competition; our full SWOT unpacks these dynamics with financial context and strategic options. Purchase the complete analysis for a professionally formatted Word report and editable Excel tools to support investment decisions, pitches, or strategic planning.

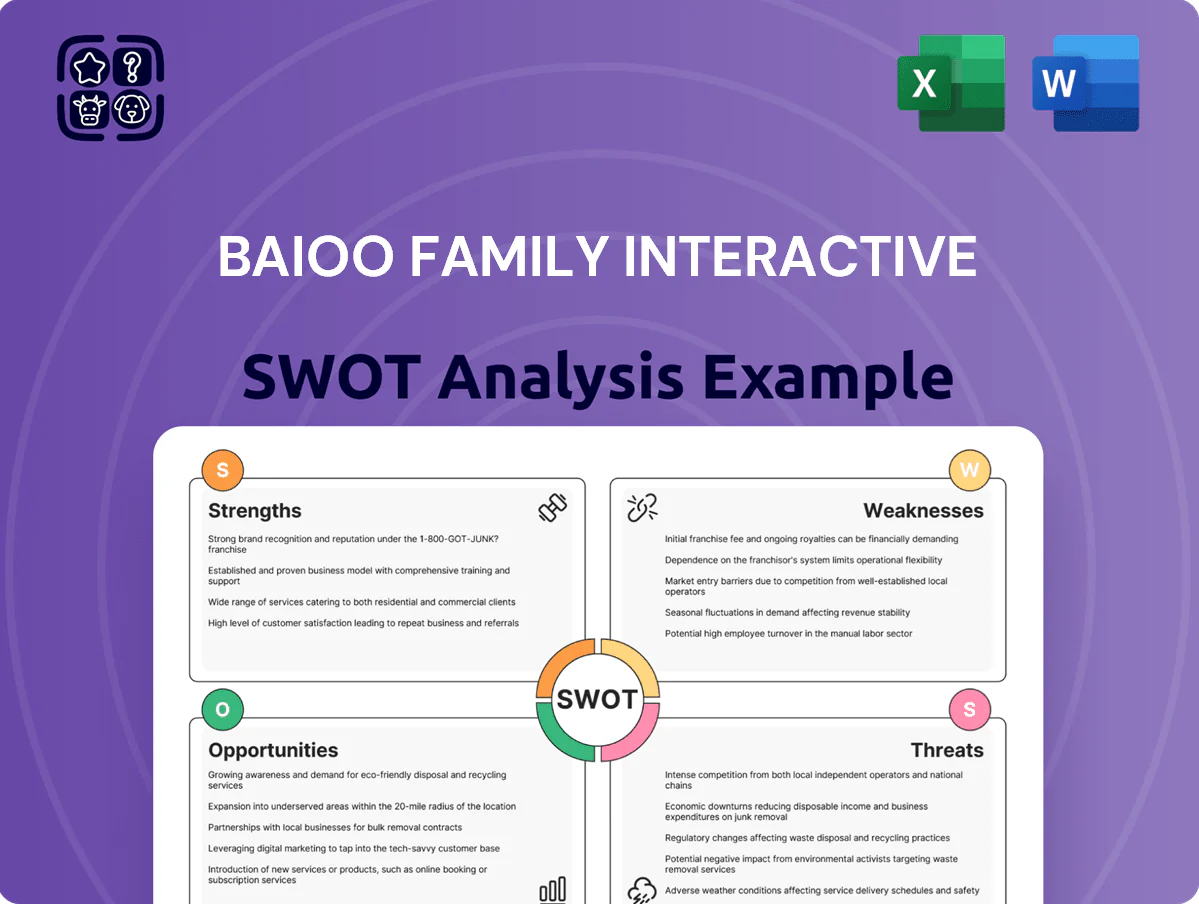

Strengths

Dominance in Niche ACGN Genres

Baioo Family Interactive holds a dominant niche in pet-collection and female-focused ACGN (anime, comics, games, novels) titles, with 2024 ARPDAU roughly 3–4x higher than its casual portfolio and 65% of paying users in nijigen games, according to company filings.

This focus yields stronger retention: 30-day retention near 22% for nijigen titles vs 12% for mass-market, enabling targeted UA that cut CPI by ~40% in 2024 campaigns.

Strong Intellectual Property Portfolio

Baioo Family Interactive owns durable IPs—Aola Star, Legend of Aoqi, and Foodie Yao—that date back over a decade and moved from PC to mobile, with mobile versions reporting combined lifetime downloads exceeding 25 million as of 2025 and annual in‑game revenue exceeding $8.5M in 2024.

Effective Multi-Platform Distribution Strategy

Baioo Family Interactive runs an effective multi-platform distribution strategy, operating on PC and mobile to cover 95%+ of China's gamer base; in 2024 mobile accounted for ~62% of its active users while PC contributed ~28%, boosting total MAU to ~12.4M. The firm mixes owned channels with third-party app stores and platforms like TapTap and Bilibili, cutting user-acquisition cost by ~18% year-over-year. This dual approach reduces exposure if one hardware ecosystem dips.

High User Retention and Community Engagement

- Retention >60%

- Churn ~4% monthly

- DAU ~420k (2024)

- ARPU +12% YoY

- In-game sales ~78% revenue

Robust R&D and Creative Capabilities

Baioo Family Interactive’s internal development keeps art style and narrative depth aligned with ACGN (anime, comics, games, novels) expectations, supporting titles that drove 2024 paid-conversion rates up to 6.2% in top IP launches.

Heavy R&D spending—reported at RMB 82.4 million in FY2024—focuses on game mechanics and performance, cutting bug-cycle time by ~35% and improving DAU retention metrics.

Internal expertise enables rapid iteration and fast responses to player trends; patch and content cadence shortened to weekly updates for key live-service titles.

- 2024 R&D spend: RMB 82.4m

- Top-IP paid conversion: 6.2%

- Bug-cycle reduction: ~35%

- Weekly update cadence for live titles

Baioo’s ACGN edge: 12.4M MAU, 420k DAU, 65% payers, ~3–4x ARPDAU vs casual

Baioo’s niche ACGN focus yields high monetization: 2024 ARPDAU 3–4x casual, 65% payers in nijigen; 30-day retention ~22% vs 12% mass-market; DAU ~420k and MAU ~12.4M; in‑game sales ~78% revenue; 2024 R&D RMB 82.4m; top-IP paid conversion 6.2%; churn ~4% monthly.

| Metric | 2024 Value |

|---|---|

| DAU | ~420k |

| MAU | ~12.4M |

| In‑game sales | ~78% rev |

| R&D spend | RMB 82.4m |

| 30‑day retention (nijigen) | ~22% |

| Paid conversion (top IP) | 6.2% |

What is included in the product

Provides a concise SWOT overview of Baioo Family Interactive, highlighting its core strengths and weaknesses, market opportunities, and external threats shaping strategic decisions.

Delivers a concise SWOT snapshot of Baioo Family Interactive to speed strategic alignment and stakeholder briefings.

Weaknesses

High Revenue Concentration on Core Titles

Limited Geographic Diversification

The company earns over 80% of revenue from Mainland China (2024 annual report), concentrating exposure to local economic slowdowns and tighter gaming regulations after the 2021 play-time curbs and 2023 licensing shifts.

International revenue stayed under 15% in FY2024, small versus Tencent and NetEase, so Baioo cannot sufficiently offset domestic downturns with offshore growth.

Dependence on Third-Party Distribution Platforms

Baioo depends on app stores and social platforms for most user acquisition and payments; in 2024 about 62% of its downloads came via Google Play and Apple App Store, exposing it to 15–30% commission fees that compress mobile title margins.

Algorithm or TOS shifts can cut visibility fast—platform policy changes in 2023 raised average cost-per-install by ~22%, and a similar tweak could spike Baioo’s CAC and reduce ARPU.

Slower Adaptation to Emerging Gaming Technologies

Modest Brand Awareness Outside Core Niche

Baioo is strong in ACGN subculture but lacks the broad recognition of giants like Tencent (2024 revenue US$77.1B) or NetEase (2024 revenue US$15.6B), limiting appeal to casual gamers outside its niche.

Lower brand equity raises customer-acquisition cost; industry CAC for mobile games averaged US$3.50 in 2024, so scaling reach needs heavy marketing spend with uncertain ROI.

Expanding beyond core fans will likely require targeted campaigns, partnerships, or IP licensing to move past niche saturation.

- Known within ACGN, not mainstream

- Competes with Tencent/NetEase brand reach

- High CAC (~US$3.50 mobile, 2024)

- Scaling needs costly marketing or partnerships

Concentrated China-heavy games biz: top title MAU -12%, weak R&D & international

| Metric | Value (2024) |

|---|---|

| Revenue concentration | 68% from 2 titles |

| Top title MAU change | -12% YoY Q3 |

| China revenue | >80% |

| International revenue | <15% |

| R&D to 3D/cloud | ~12% |

| Peer R&D range | 25–35% |

| Estimated CAPEX | $6–12M (2025–26) |

| Mobile CAC | US$3.50 avg |

What You See Is What You Get

Baioo Family Interactive SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and this excerpt is editable and ready to use. You’re viewing a live preview of the real file; buy now to unlock the complete, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Baioo Family Interactive shows niche strengths in family-focused content and agile digital distribution, but faces scalability and monetization headwinds amid fierce competition; our full SWOT unpacks these dynamics with financial context and strategic options. Purchase the complete analysis for a professionally formatted Word report and editable Excel tools to support investment decisions, pitches, or strategic planning.

Strengths

Dominance in Niche ACGN Genres

Baioo Family Interactive holds a dominant niche in pet-collection and female-focused ACGN (anime, comics, games, novels) titles, with 2024 ARPDAU roughly 3–4x higher than its casual portfolio and 65% of paying users in nijigen games, according to company filings.

This focus yields stronger retention: 30-day retention near 22% for nijigen titles vs 12% for mass-market, enabling targeted UA that cut CPI by ~40% in 2024 campaigns.

Strong Intellectual Property Portfolio

Baioo Family Interactive owns durable IPs—Aola Star, Legend of Aoqi, and Foodie Yao—that date back over a decade and moved from PC to mobile, with mobile versions reporting combined lifetime downloads exceeding 25 million as of 2025 and annual in‑game revenue exceeding $8.5M in 2024.

Effective Multi-Platform Distribution Strategy

Baioo Family Interactive runs an effective multi-platform distribution strategy, operating on PC and mobile to cover 95%+ of China's gamer base; in 2024 mobile accounted for ~62% of its active users while PC contributed ~28%, boosting total MAU to ~12.4M. The firm mixes owned channels with third-party app stores and platforms like TapTap and Bilibili, cutting user-acquisition cost by ~18% year-over-year. This dual approach reduces exposure if one hardware ecosystem dips.

High User Retention and Community Engagement

- Retention >60%

- Churn ~4% monthly

- DAU ~420k (2024)

- ARPU +12% YoY

- In-game sales ~78% revenue

Robust R&D and Creative Capabilities

Baioo Family Interactive’s internal development keeps art style and narrative depth aligned with ACGN (anime, comics, games, novels) expectations, supporting titles that drove 2024 paid-conversion rates up to 6.2% in top IP launches.

Heavy R&D spending—reported at RMB 82.4 million in FY2024—focuses on game mechanics and performance, cutting bug-cycle time by ~35% and improving DAU retention metrics.

Internal expertise enables rapid iteration and fast responses to player trends; patch and content cadence shortened to weekly updates for key live-service titles.

- 2024 R&D spend: RMB 82.4m

- Top-IP paid conversion: 6.2%

- Bug-cycle reduction: ~35%

- Weekly update cadence for live titles

Baioo’s ACGN edge: 12.4M MAU, 420k DAU, 65% payers, ~3–4x ARPDAU vs casual

Baioo’s niche ACGN focus yields high monetization: 2024 ARPDAU 3–4x casual, 65% payers in nijigen; 30-day retention ~22% vs 12% mass-market; DAU ~420k and MAU ~12.4M; in‑game sales ~78% revenue; 2024 R&D RMB 82.4m; top-IP paid conversion 6.2%; churn ~4% monthly.

| Metric | 2024 Value |

|---|---|

| DAU | ~420k |

| MAU | ~12.4M |

| In‑game sales | ~78% rev |

| R&D spend | RMB 82.4m |

| 30‑day retention (nijigen) | ~22% |

| Paid conversion (top IP) | 6.2% |

What is included in the product

Provides a concise SWOT overview of Baioo Family Interactive, highlighting its core strengths and weaknesses, market opportunities, and external threats shaping strategic decisions.

Delivers a concise SWOT snapshot of Baioo Family Interactive to speed strategic alignment and stakeholder briefings.

Weaknesses

High Revenue Concentration on Core Titles

Limited Geographic Diversification

The company earns over 80% of revenue from Mainland China (2024 annual report), concentrating exposure to local economic slowdowns and tighter gaming regulations after the 2021 play-time curbs and 2023 licensing shifts.

International revenue stayed under 15% in FY2024, small versus Tencent and NetEase, so Baioo cannot sufficiently offset domestic downturns with offshore growth.

Dependence on Third-Party Distribution Platforms

Baioo depends on app stores and social platforms for most user acquisition and payments; in 2024 about 62% of its downloads came via Google Play and Apple App Store, exposing it to 15–30% commission fees that compress mobile title margins.

Algorithm or TOS shifts can cut visibility fast—platform policy changes in 2023 raised average cost-per-install by ~22%, and a similar tweak could spike Baioo’s CAC and reduce ARPU.

Slower Adaptation to Emerging Gaming Technologies

Modest Brand Awareness Outside Core Niche

Baioo is strong in ACGN subculture but lacks the broad recognition of giants like Tencent (2024 revenue US$77.1B) or NetEase (2024 revenue US$15.6B), limiting appeal to casual gamers outside its niche.

Lower brand equity raises customer-acquisition cost; industry CAC for mobile games averaged US$3.50 in 2024, so scaling reach needs heavy marketing spend with uncertain ROI.

Expanding beyond core fans will likely require targeted campaigns, partnerships, or IP licensing to move past niche saturation.

- Known within ACGN, not mainstream

- Competes with Tencent/NetEase brand reach

- High CAC (~US$3.50 mobile, 2024)

- Scaling needs costly marketing or partnerships

Concentrated China-heavy games biz: top title MAU -12%, weak R&D & international

| Metric | Value (2024) |

|---|---|

| Revenue concentration | 68% from 2 titles |

| Top title MAU change | -12% YoY Q3 |

| China revenue | >80% |

| International revenue | <15% |

| R&D to 3D/cloud | ~12% |

| Peer R&D range | 25–35% |

| Estimated CAPEX | $6–12M (2025–26) |

| Mobile CAC | US$3.50 avg |

What You See Is What You Get

Baioo Family Interactive SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and this excerpt is editable and ready to use. You’re viewing a live preview of the real file; buy now to unlock the complete, detailed version immediately after checkout.