Bajaj Finserv SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Bajaj Finserv’s diversified financial services portfolio, strong brand, and tech-led distribution drive robust growth, while credit risk, regulatory shifts, and competition pose challenges; digital partnerships and rural expansion are key growth levers. Discover the full SWOT analysis for actionable insights, financial context, and editable deliverables to support investing, planning, and pitches—purchase now for the complete report.

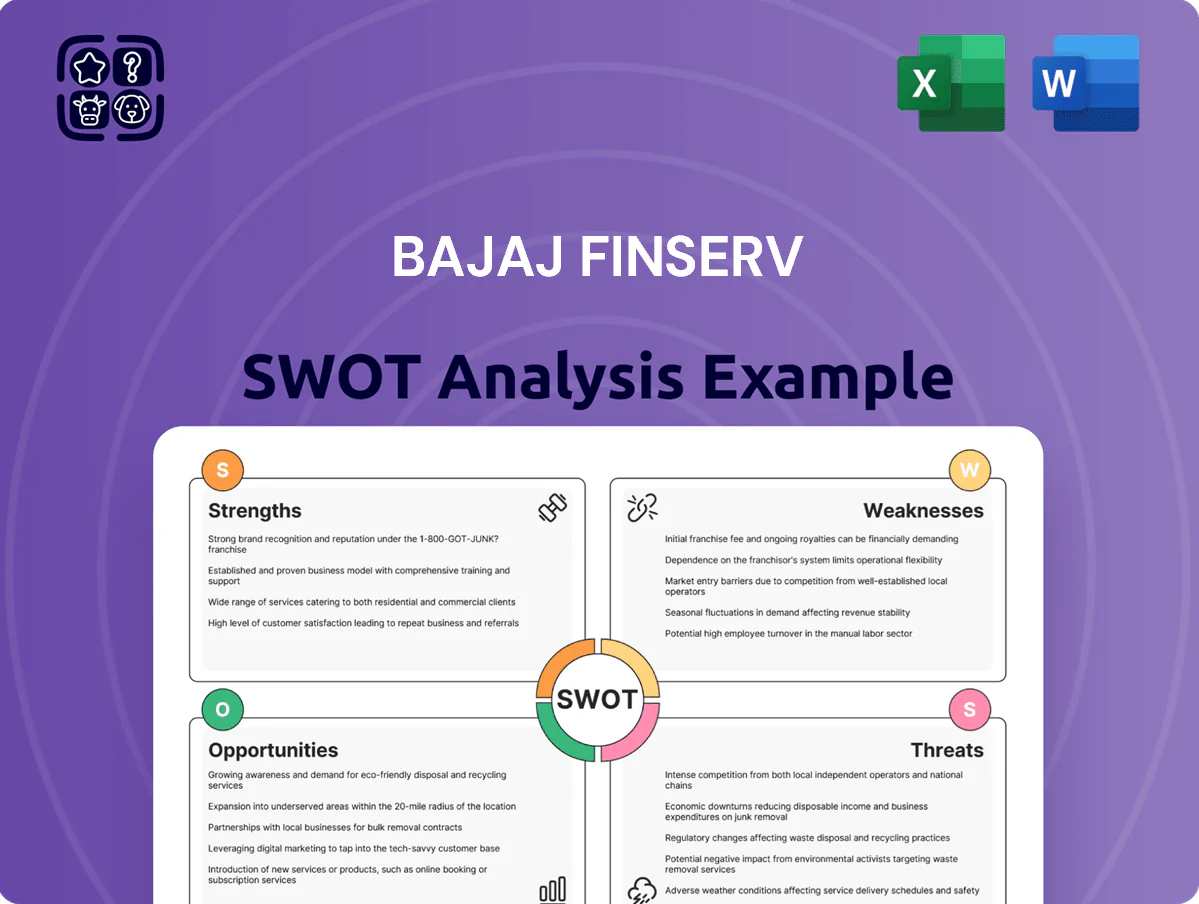

Strengths

Diversified Financial Services Portfolio

Bajaj Finserv’s subsidiaries span lending, general insurance (Bajaj Allianz General Insurance joint venture), and life insurance (Bajaj Life Insurance), giving it multiple revenue streams and lower sector concentration risk; FY2024 consolidated AUM exceeded INR 1.2 trillion and NBFC lending grew ~18% YoY.

Dominant Market Position of Bajaj Finance

Bajaj Finance, the lending arm of Bajaj Finserv, leads India’s NBFC consumer finance with a 2025 AUM of about INR 1.35 lakh crore, serving over 80 million customers; this scale fuels dominant share in consumer durable finance and personal loans and feeds rich behavioral data to the parent. Its market position and cost of capital advantage create a high barrier to entry for smaller NBFCs and new fintechs, limiting their ability to match reach and pricing.

Advanced Tech-Driven Ecosystem

Strong Brand Equity and Trust

The Bajaj brand has decades of trust across India, boosting customer confidence in lending and insurance; Bajaj Finserv reported a 16% YoY increase in active customers to 43.2 million in FY2025, helping steady deposit flows and policy renewals.

This reputation lowers acquisition costs versus digital-only rivals—company data shows customer acquisition cost 28% below the segment median in 2025—supporting higher retention and cross-sell rates.

- 43.2 million active customers (FY2025)

- 16% YoY active-customer growth

- 28% lower customer acquisition cost vs segment median (2025)

- Higher insurance renewal and deposit stability

Robust Capital Adequacy and Liquidity

Bajaj Finserv reports capital adequacy ratios comfortably above RBI norms—Consolidated CRAR ~26% and CET1 ~18% as of Sept 30, 2025—giving a large financial cushion to pursue growth and absorb shocks.

Strong liquidity (liquid assets covering >120 days of funding needs; liquidity coverage ratio ~1.6x) lets the firm fund strategic investments in insurance, BNPL, and fintech partnerships without stress.

- CRAR ~26% (Sept 30, 2025)

- CET1 ~18% (Sept 30, 2025)

- Liquid assets cover >120 days

- Liquidity coverage ~1.6x

Bajaj Finserv: INR1.35T AUM, 80M customers, 26% CAR, 1.9% GNPA, 28% lower CAC

Bajaj Finserv’s diversified financial ecosystem (lending, insurance, wealth) gave FY2025 consolidated AUM ~INR 1.35 trillion, 80m+ customers, GNPA 1.9% (Q3 FY2025), CRAR ~26% (Sept 30, 2025), and 28% lower CAC vs segment median—supporting scale, cross-sell, liquidity, and tech-led margin gains.

| Metric | Value |

|---|---|

| Consolidated AUM FY2025 | INR 1.35T |

| Active customers | 80m+ |

| GNPA Q3 FY2025 | 1.9% |

| CRAR (Sept 30, 2025) | ~26% |

| CAC vs median (2025) | -28% |

What is included in the product

Delivers a strategic overview of Bajaj Finserv’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position and future growth prospects.

Provides a concise SWOT snapshot of Bajaj Finserv for rapid strategic alignment and executive briefings.

Weaknesses

Heavy Reliance on Bajaj Finance

A substantial share of Bajaj Finserv’s consolidated PAT—about 68% in FY2024—comes from Bajaj Finance, creating concentration risk; a shock to the NBFC (non-banking financial company) lending book would hit group profit hard.

Regulatory moves like tighter RBI norms or an NBFC liquidity squeeze could cut margins and growth; during FY2023 stress, NBFC credit costs rose ~120 bps, showing sensitivity.

Management still struggles to lift insurance and wealth management contribution, which together made only ~22% of group PAT in FY2024, limiting revenue diversification.

Exposure to Unsecured Lending Risks

Bajaj Finserv holds a large unsecured loan book—personal and consumer loans made up about 42% of its AUM (FY2024), so these loans are highly sensitive to economic cycles; a GDP slowdown or rising unemployment could push GNPA higher—unsecured GNPA rose to 3.1% in FY2023 in India’s NBFC sector during the last slowdown. Managing this requires continuous monitoring and advanced risk models, plus dynamic provisioning.

High Operational Complexity

Geographic Concentration in India

Despite its massive scale, Bajaj Finserv remains almost entirely dependent on India, with over 95% of consolidated revenue and 100% of retail lending exposure tied to the domestic market as of FY2024 (total consolidated revenue ₹52,000 crore, retail loan book ~₹1.8 trillion).

This lack of international diversification raises vulnerability to Indian-specific systemic risks, RBI policy shifts, or macro slowdowns; a 1% GDP growth slowdown could cut retail demand materially.

While India’s financial services growth is strong (GDP +7.2% in 2024), no global footprint limits hedging options against local shocks and currency diversification benefits.

- ~95% revenue from India (FY2024)

- Retail loan book ~₹1.8 trillion

- RBI policy risk concentrates earnings volatility

Rising Customer Acquisition Costs in Insurance

High concentration risk: Bajaj Finance drives 68% PAT; India-heavy, unsecured loans surge

Concentration risk: ~68% group PAT from Bajaj Finance (FY2024); unsecured retail loans ~42% of AUM (~₹1.8T). Domestic concentration: ~95% revenue India; consolidated revenue ₹52,000 crore (FY2024). Operational complexity: group assets ₹2.5 lakh crore, 60+ entities; slower product rollout. Insurance margin squeeze: marketing +12–15% (2024), premiums +10% YoY.

| Metric | Value |

|---|---|

| Group PAT share (Bajaj Finance) | ~68% (FY2024) |

| Retail loan book | ~₹1.8T |

| Revenue from India | ~95% (FY2024) |

| Consol revenue | ₹52,000 cr (FY2024) |

| Marketing spend (insurance) | +12–15% (2024) |

Full Version Awaits

Bajaj Finserv SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report on Bajaj Finserv, and the complete, editable version becomes available immediately after checkout. You’re viewing a live excerpt of the real file, structured for strategic use by investors and analysts. Unlock the full, detailed SWOT when you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Bajaj Finserv’s diversified financial services portfolio, strong brand, and tech-led distribution drive robust growth, while credit risk, regulatory shifts, and competition pose challenges; digital partnerships and rural expansion are key growth levers. Discover the full SWOT analysis for actionable insights, financial context, and editable deliverables to support investing, planning, and pitches—purchase now for the complete report.

Strengths

Diversified Financial Services Portfolio

Bajaj Finserv’s subsidiaries span lending, general insurance (Bajaj Allianz General Insurance joint venture), and life insurance (Bajaj Life Insurance), giving it multiple revenue streams and lower sector concentration risk; FY2024 consolidated AUM exceeded INR 1.2 trillion and NBFC lending grew ~18% YoY.

Dominant Market Position of Bajaj Finance

Bajaj Finance, the lending arm of Bajaj Finserv, leads India’s NBFC consumer finance with a 2025 AUM of about INR 1.35 lakh crore, serving over 80 million customers; this scale fuels dominant share in consumer durable finance and personal loans and feeds rich behavioral data to the parent. Its market position and cost of capital advantage create a high barrier to entry for smaller NBFCs and new fintechs, limiting their ability to match reach and pricing.

Advanced Tech-Driven Ecosystem

Strong Brand Equity and Trust

The Bajaj brand has decades of trust across India, boosting customer confidence in lending and insurance; Bajaj Finserv reported a 16% YoY increase in active customers to 43.2 million in FY2025, helping steady deposit flows and policy renewals.

This reputation lowers acquisition costs versus digital-only rivals—company data shows customer acquisition cost 28% below the segment median in 2025—supporting higher retention and cross-sell rates.

- 43.2 million active customers (FY2025)

- 16% YoY active-customer growth

- 28% lower customer acquisition cost vs segment median (2025)

- Higher insurance renewal and deposit stability

Robust Capital Adequacy and Liquidity

Bajaj Finserv reports capital adequacy ratios comfortably above RBI norms—Consolidated CRAR ~26% and CET1 ~18% as of Sept 30, 2025—giving a large financial cushion to pursue growth and absorb shocks.

Strong liquidity (liquid assets covering >120 days of funding needs; liquidity coverage ratio ~1.6x) lets the firm fund strategic investments in insurance, BNPL, and fintech partnerships without stress.

- CRAR ~26% (Sept 30, 2025)

- CET1 ~18% (Sept 30, 2025)

- Liquid assets cover >120 days

- Liquidity coverage ~1.6x

Bajaj Finserv: INR1.35T AUM, 80M customers, 26% CAR, 1.9% GNPA, 28% lower CAC

Bajaj Finserv’s diversified financial ecosystem (lending, insurance, wealth) gave FY2025 consolidated AUM ~INR 1.35 trillion, 80m+ customers, GNPA 1.9% (Q3 FY2025), CRAR ~26% (Sept 30, 2025), and 28% lower CAC vs segment median—supporting scale, cross-sell, liquidity, and tech-led margin gains.

| Metric | Value |

|---|---|

| Consolidated AUM FY2025 | INR 1.35T |

| Active customers | 80m+ |

| GNPA Q3 FY2025 | 1.9% |

| CRAR (Sept 30, 2025) | ~26% |

| CAC vs median (2025) | -28% |

What is included in the product

Delivers a strategic overview of Bajaj Finserv’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position and future growth prospects.

Provides a concise SWOT snapshot of Bajaj Finserv for rapid strategic alignment and executive briefings.

Weaknesses

Heavy Reliance on Bajaj Finance

A substantial share of Bajaj Finserv’s consolidated PAT—about 68% in FY2024—comes from Bajaj Finance, creating concentration risk; a shock to the NBFC (non-banking financial company) lending book would hit group profit hard.

Regulatory moves like tighter RBI norms or an NBFC liquidity squeeze could cut margins and growth; during FY2023 stress, NBFC credit costs rose ~120 bps, showing sensitivity.

Management still struggles to lift insurance and wealth management contribution, which together made only ~22% of group PAT in FY2024, limiting revenue diversification.

Exposure to Unsecured Lending Risks

Bajaj Finserv holds a large unsecured loan book—personal and consumer loans made up about 42% of its AUM (FY2024), so these loans are highly sensitive to economic cycles; a GDP slowdown or rising unemployment could push GNPA higher—unsecured GNPA rose to 3.1% in FY2023 in India’s NBFC sector during the last slowdown. Managing this requires continuous monitoring and advanced risk models, plus dynamic provisioning.

High Operational Complexity

Geographic Concentration in India

Despite its massive scale, Bajaj Finserv remains almost entirely dependent on India, with over 95% of consolidated revenue and 100% of retail lending exposure tied to the domestic market as of FY2024 (total consolidated revenue ₹52,000 crore, retail loan book ~₹1.8 trillion).

This lack of international diversification raises vulnerability to Indian-specific systemic risks, RBI policy shifts, or macro slowdowns; a 1% GDP growth slowdown could cut retail demand materially.

While India’s financial services growth is strong (GDP +7.2% in 2024), no global footprint limits hedging options against local shocks and currency diversification benefits.

- ~95% revenue from India (FY2024)

- Retail loan book ~₹1.8 trillion

- RBI policy risk concentrates earnings volatility

Rising Customer Acquisition Costs in Insurance

High concentration risk: Bajaj Finance drives 68% PAT; India-heavy, unsecured loans surge

Concentration risk: ~68% group PAT from Bajaj Finance (FY2024); unsecured retail loans ~42% of AUM (~₹1.8T). Domestic concentration: ~95% revenue India; consolidated revenue ₹52,000 crore (FY2024). Operational complexity: group assets ₹2.5 lakh crore, 60+ entities; slower product rollout. Insurance margin squeeze: marketing +12–15% (2024), premiums +10% YoY.

| Metric | Value |

|---|---|

| Group PAT share (Bajaj Finance) | ~68% (FY2024) |

| Retail loan book | ~₹1.8T |

| Revenue from India | ~95% (FY2024) |

| Consol revenue | ₹52,000 cr (FY2024) |

| Marketing spend (insurance) | +12–15% (2024) |

Full Version Awaits

Bajaj Finserv SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report on Bajaj Finserv, and the complete, editable version becomes available immediately after checkout. You’re viewing a live excerpt of the real file, structured for strategic use by investors and analysts. Unlock the full, detailed SWOT when you buy.