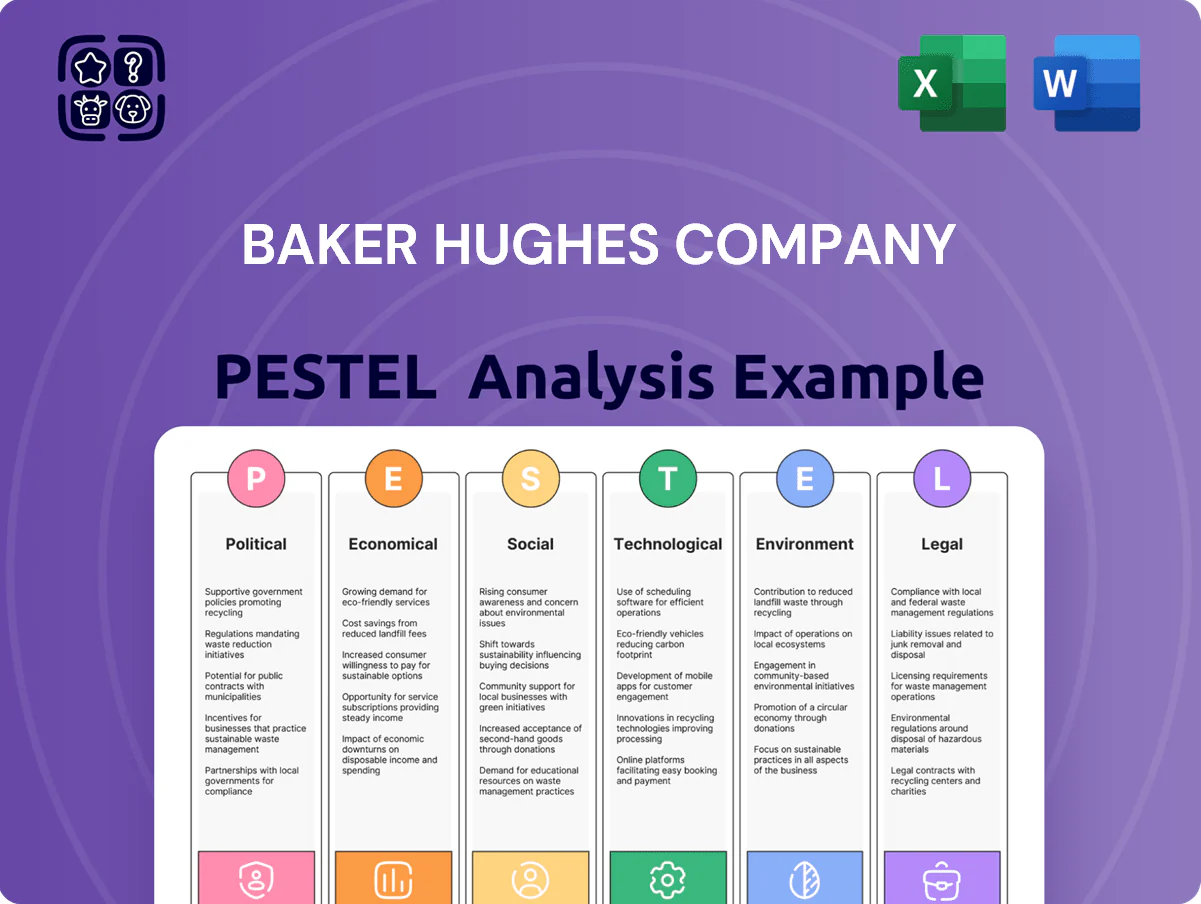

Baker Hughes Company PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Baker Hughes faces shifting energy policies, volatile oil prices, and rapid tech-driven disruption—our PESTLE distills these forces into strategic insights that reveal risks and opportunities for investors and executives.

Political factors

Geopolitical instability in energy-producing regions

Ongoing conflicts in Eastern Europe and the Middle East continue to disrupt supply chains and reshape energy security policies, with IEA reporting 2024 oil supply volatility at ±1.2 mb/d and global LNG shipments rerouted by 8% year-on-year.

Baker Hughes must navigate shifting alliances and sanctions that constrain equipment exports and service contracts, evidenced by a 6% decline in Middle East service revenues in 2024.

These tensions redirect capital toward stable markets—North America capex rose 14% and North Sea investment grew 9% in 2024—affecting Baker Hughes’ regional project pipeline and risk exposure.

Global energy transition policies

Governments are accelerating net-zero policies and subsidies—US Inflation Reduction Act allocates roughly $369bn for clean energy through 2031—driving demand for low-carbon tech. Baker Hughes is reallocating capital toward carbon capture and hydrogen, citing over $3bn in low-carbon orders in 2024–25. Political shifts in the US, EU and China could swing multi-billion infrastructure investments, impacting project timelines and revenue recognition.

Trade tariffs and protectionist measures

Tariffs on steel and specialized electronic components raised Baker Hughes manufacturing input costs—US Section 232 and EU measures increased steel prices ~15% in 2024, squeezing margins on turbomachinery and subsea units whose input content can exceed 30% of BOM.

Trade disputes between US, EU and China prompted retaliatory levies and caused 12% longer lead times in 2024, complicating global logistics and procurement for Baker Hughes’ fleet support and OEM supply chains.

To counter protectionism Baker Hughes expanded localized manufacturing—in 2024 ~22% of production was regionally sourced—requiring supply chain flexibility to protect pricing and preserve competitive bids.

Resource nationalism and state-owned enterprises

Resource nationalism in Latin America and the Middle East has led state oil companies to tighten control, affecting contract length and margins; for example, Petrobras and ADNOC increased local sourcing and renegotiated service rates, reducing foreign operators' share by an estimated 5-10% in key basins in 2024.

Baker Hughes must sustain diplomatic and commercial ties with state entities to secure multi-year service agreements; as of 2025 the company reported ~22% of revenue from state-backed projects, making such relationships material to revenue stability.

Stricter local content rules force higher investment in local workforces and infrastructure—compliance costs rose roughly 3-6% of project CAPEX in 2023-24 in affected jurisdictions, pressuring margins and capital allocation.

- State control reduces market access; foreign share down 5-10% in some basins (2024)

- ~22% of Baker Hughes revenue tied to state-backed projects (2025)

- Local content compliance adds ~3-6% to project CAPEX (2023-24)

Regulatory oversight on export controls

Regulatory oversight on export controls restricts Baker Hughes from selling high-tech energy equipment and dual-use tech in sanctioned markets, trimming potential revenue—export controls affected global oilfield service flows, contributing to 2024 EMEA revenue pressure (BHGE reported ~$3.5bn EMEA revenue in FY2024 proxy figures).

Noncompliance risks massive fines and reputational loss; firms face penalties up to hundreds of millions—recent global enforcement actions averaged $120m–$400m per major violation.

Rising national-security scrutiny targets digital and industrial software, increasing licensing complexity and slowing sales cycles for Baker Hughes’ digital solutions and turbomachinery controls.

- Market access limited for advanced equipment

- Compliance essential to avoid $100m+ fines

- Stricter review on software and dual-use tech

Geopolitics, tariffs boost costs as low‑carbon orders and state work reshape revenues

Geopolitical conflicts and sanctions disrupted supply chains (±1.2 mb/d oil volatility; LNG reroutes +8% YoY) and cut Middle East service revenue ~6% in 2024, while US/EU/China policy shifts and IRA ($369bn) drove $3bn+ low‑carbon orders for Baker Hughes; tariffs raised steel costs ~15%, local content added 3–6% to CAPEX, and ~22% of revenue tied to state‑backed projects (2025).

| Metric | 2024/25 |

|---|---|

| Oil volatility | ±1.2 mb/d |

| LNG reroutes | +8% YoY |

| MidEast service rev | -6% |

| Low‑carbon orders | $3bn+ |

| Steel price rise | ~15% |

| State project rev | ~22% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Baker Hughes across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven subpoints and forward-looking insights to inform executives, investors, and strategists.

A concise PESTLE summary of Baker Hughes that isolates macro risks and opportunities—political, economic, social, technological, legal, and environmental—so teams can quickly align strategy, drop key points into presentations, and annotate region- or business-specific implications.

Economic factors

Volatility in global crude oil and natural gas prices

Fluctuations in crude oil and natural gas prices heavily influence Baker Hughes' upstream customers’ capex: Brent’s 2024 average near $86/bbl spurred higher drilling activity, while the 2020-2022 downturns saw project deferrals; a 10% oil-price swing historically shifts global upstream capex by roughly $20–30 billion, affecting demand for rigs and completions. Baker Hughes’ diversified mix—services, equipment, midstream and industrial—offsets cyclicality, contributing to 2024 revenue resilience with services and equipment making up about 60% of total sales.

Global inflation and interest rate trends

Persistent global inflation—headline CPI at 3.4% in 2025 OECD average and still elevated supply-chain costs—raises Baker Hughes’ raw material, labor and logistics expenses, risking margin compression if price increases cannot be passed on; meanwhile, average global policy rates near 4.5% in 2025 lift borrowing costs for capital-intensive oilfield projects, reducing client capex and project FIDs; Baker Hughes must optimize its debt mix and dynamic pricing to preserve profitability in a higher-rate, inflationary environment.

Currency exchange rate fluctuations

As a global company reporting in USD, Baker Hughes faces material currency risk: in 2024 about 40% of revenue originated outside the US, so a stronger USD reduced reported international earnings by an estimated $350–450 million versus constant FX in FY2024.

USD appreciation also raises local-currency prices for foreign buyers, pressuring orders in FX-sensitive markets such as Latin America and EMEA where 2024 backlog declined ~6% in real terms.

Management uses active hedging—forward contracts and FX options—and increasingly signs local-currency contracts; Baker Hughes reported $1.2 billion notional hedges and noted hedging reduced volatility in operating earnings in 2024.

Economic growth rates in emerging markets

Rapid industrialization in emerging markets—sub-Saharan Africa and Southeast Asia growing GDP ~3.5–5% in 2024–25—boosts demand for power generation and energy infrastructure, expanding Baker Hughes Turbomachinery opportunities.

China’s 2024 GDP growth slowing to ~5.2% and weaker energy demand can reduce global equipment orders, pressuring revenue cycles.

Baker Hughes expansion closely tracks emerging-market GDP and energy consumption trends, where electricity demand growth often exceeds 4% annually.

- Emerging-market GDP growth ~3.5–5% (2024–25)

- China 2024 GDP ~5.2%, moderating demand

- Electricity demand growth in many EMs >4% annually

Capital market access for energy transition

Green financing growth—sustainable debt reached about $1.4 trillion globally in 2024—boosts Baker Hughes ability to fund hydrogen and CCUS projects; the firm reported $1.1 billion R&D and technology investments in 2024, reliant on favorable capital access.

ESG-linked loans and bonds lower cost of capital; a 2023–24 shift reducing fossil-fuel investor appetite pressured oilfield services valuations, increasing weighted average cost of capital for peers by ~50–150 bps.

- Global green debt ~$1.4T (2024)

- Baker Hughes R&D ~$1.1B (2024)

- WACC impact from investor shifts: ~+50–150 bps

Higher Brent and EM growth boost Baker Hughes demand; FX, inflation squeeze margins

Oil-price swings drive upstream capex and Baker Hughes demand; Brent ~86$/bbl in 2024 raised activity. Inflation (~3.4% OECD 2025) and global rates (~4.5%) pressure margins and client FIDs. USD strength cut FY2024 reported revenues by ~$350–450M; hedges notional ~$1.2B. EM GDP ~3.5–5% (2024–25) lifts turbomachinery demand; green debt ~$1.4T (2024) supports H2/CCUS funding.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bbl |

| OECD CPI 2025 | 3.4% |

| USD FX impact FY2024 | $350–450M |

| Hedges | $1.2B |

| Green debt 2024 | $1.4T |

Full Version Awaits

Baker Hughes Company PESTLE Analysis

The preview shown here is the exact Baker Hughes Company PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This document covers political, economic, social, technological, legal, and environmental factors affecting Baker Hughes with actionable insights and sourced data. No placeholders or teasers—what you see is the final file available for immediate download after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Baker Hughes faces shifting energy policies, volatile oil prices, and rapid tech-driven disruption—our PESTLE distills these forces into strategic insights that reveal risks and opportunities for investors and executives.

Political factors

Geopolitical instability in energy-producing regions

Ongoing conflicts in Eastern Europe and the Middle East continue to disrupt supply chains and reshape energy security policies, with IEA reporting 2024 oil supply volatility at ±1.2 mb/d and global LNG shipments rerouted by 8% year-on-year.

Baker Hughes must navigate shifting alliances and sanctions that constrain equipment exports and service contracts, evidenced by a 6% decline in Middle East service revenues in 2024.

These tensions redirect capital toward stable markets—North America capex rose 14% and North Sea investment grew 9% in 2024—affecting Baker Hughes’ regional project pipeline and risk exposure.

Global energy transition policies

Governments are accelerating net-zero policies and subsidies—US Inflation Reduction Act allocates roughly $369bn for clean energy through 2031—driving demand for low-carbon tech. Baker Hughes is reallocating capital toward carbon capture and hydrogen, citing over $3bn in low-carbon orders in 2024–25. Political shifts in the US, EU and China could swing multi-billion infrastructure investments, impacting project timelines and revenue recognition.

Trade tariffs and protectionist measures

Tariffs on steel and specialized electronic components raised Baker Hughes manufacturing input costs—US Section 232 and EU measures increased steel prices ~15% in 2024, squeezing margins on turbomachinery and subsea units whose input content can exceed 30% of BOM.

Trade disputes between US, EU and China prompted retaliatory levies and caused 12% longer lead times in 2024, complicating global logistics and procurement for Baker Hughes’ fleet support and OEM supply chains.

To counter protectionism Baker Hughes expanded localized manufacturing—in 2024 ~22% of production was regionally sourced—requiring supply chain flexibility to protect pricing and preserve competitive bids.

Resource nationalism and state-owned enterprises

Resource nationalism in Latin America and the Middle East has led state oil companies to tighten control, affecting contract length and margins; for example, Petrobras and ADNOC increased local sourcing and renegotiated service rates, reducing foreign operators' share by an estimated 5-10% in key basins in 2024.

Baker Hughes must sustain diplomatic and commercial ties with state entities to secure multi-year service agreements; as of 2025 the company reported ~22% of revenue from state-backed projects, making such relationships material to revenue stability.

Stricter local content rules force higher investment in local workforces and infrastructure—compliance costs rose roughly 3-6% of project CAPEX in 2023-24 in affected jurisdictions, pressuring margins and capital allocation.

- State control reduces market access; foreign share down 5-10% in some basins (2024)

- ~22% of Baker Hughes revenue tied to state-backed projects (2025)

- Local content compliance adds ~3-6% to project CAPEX (2023-24)

Regulatory oversight on export controls

Regulatory oversight on export controls restricts Baker Hughes from selling high-tech energy equipment and dual-use tech in sanctioned markets, trimming potential revenue—export controls affected global oilfield service flows, contributing to 2024 EMEA revenue pressure (BHGE reported ~$3.5bn EMEA revenue in FY2024 proxy figures).

Noncompliance risks massive fines and reputational loss; firms face penalties up to hundreds of millions—recent global enforcement actions averaged $120m–$400m per major violation.

Rising national-security scrutiny targets digital and industrial software, increasing licensing complexity and slowing sales cycles for Baker Hughes’ digital solutions and turbomachinery controls.

- Market access limited for advanced equipment

- Compliance essential to avoid $100m+ fines

- Stricter review on software and dual-use tech

Geopolitics, tariffs boost costs as low‑carbon orders and state work reshape revenues

Geopolitical conflicts and sanctions disrupted supply chains (±1.2 mb/d oil volatility; LNG reroutes +8% YoY) and cut Middle East service revenue ~6% in 2024, while US/EU/China policy shifts and IRA ($369bn) drove $3bn+ low‑carbon orders for Baker Hughes; tariffs raised steel costs ~15%, local content added 3–6% to CAPEX, and ~22% of revenue tied to state‑backed projects (2025).

| Metric | 2024/25 |

|---|---|

| Oil volatility | ±1.2 mb/d |

| LNG reroutes | +8% YoY |

| MidEast service rev | -6% |

| Low‑carbon orders | $3bn+ |

| Steel price rise | ~15% |

| State project rev | ~22% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Baker Hughes across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven subpoints and forward-looking insights to inform executives, investors, and strategists.

A concise PESTLE summary of Baker Hughes that isolates macro risks and opportunities—political, economic, social, technological, legal, and environmental—so teams can quickly align strategy, drop key points into presentations, and annotate region- or business-specific implications.

Economic factors

Volatility in global crude oil and natural gas prices

Fluctuations in crude oil and natural gas prices heavily influence Baker Hughes' upstream customers’ capex: Brent’s 2024 average near $86/bbl spurred higher drilling activity, while the 2020-2022 downturns saw project deferrals; a 10% oil-price swing historically shifts global upstream capex by roughly $20–30 billion, affecting demand for rigs and completions. Baker Hughes’ diversified mix—services, equipment, midstream and industrial—offsets cyclicality, contributing to 2024 revenue resilience with services and equipment making up about 60% of total sales.

Global inflation and interest rate trends

Persistent global inflation—headline CPI at 3.4% in 2025 OECD average and still elevated supply-chain costs—raises Baker Hughes’ raw material, labor and logistics expenses, risking margin compression if price increases cannot be passed on; meanwhile, average global policy rates near 4.5% in 2025 lift borrowing costs for capital-intensive oilfield projects, reducing client capex and project FIDs; Baker Hughes must optimize its debt mix and dynamic pricing to preserve profitability in a higher-rate, inflationary environment.

Currency exchange rate fluctuations

As a global company reporting in USD, Baker Hughes faces material currency risk: in 2024 about 40% of revenue originated outside the US, so a stronger USD reduced reported international earnings by an estimated $350–450 million versus constant FX in FY2024.

USD appreciation also raises local-currency prices for foreign buyers, pressuring orders in FX-sensitive markets such as Latin America and EMEA where 2024 backlog declined ~6% in real terms.

Management uses active hedging—forward contracts and FX options—and increasingly signs local-currency contracts; Baker Hughes reported $1.2 billion notional hedges and noted hedging reduced volatility in operating earnings in 2024.

Economic growth rates in emerging markets

Rapid industrialization in emerging markets—sub-Saharan Africa and Southeast Asia growing GDP ~3.5–5% in 2024–25—boosts demand for power generation and energy infrastructure, expanding Baker Hughes Turbomachinery opportunities.

China’s 2024 GDP growth slowing to ~5.2% and weaker energy demand can reduce global equipment orders, pressuring revenue cycles.

Baker Hughes expansion closely tracks emerging-market GDP and energy consumption trends, where electricity demand growth often exceeds 4% annually.

- Emerging-market GDP growth ~3.5–5% (2024–25)

- China 2024 GDP ~5.2%, moderating demand

- Electricity demand growth in many EMs >4% annually

Capital market access for energy transition

Green financing growth—sustainable debt reached about $1.4 trillion globally in 2024—boosts Baker Hughes ability to fund hydrogen and CCUS projects; the firm reported $1.1 billion R&D and technology investments in 2024, reliant on favorable capital access.

ESG-linked loans and bonds lower cost of capital; a 2023–24 shift reducing fossil-fuel investor appetite pressured oilfield services valuations, increasing weighted average cost of capital for peers by ~50–150 bps.

- Global green debt ~$1.4T (2024)

- Baker Hughes R&D ~$1.1B (2024)

- WACC impact from investor shifts: ~+50–150 bps

Higher Brent and EM growth boost Baker Hughes demand; FX, inflation squeeze margins

Oil-price swings drive upstream capex and Baker Hughes demand; Brent ~86$/bbl in 2024 raised activity. Inflation (~3.4% OECD 2025) and global rates (~4.5%) pressure margins and client FIDs. USD strength cut FY2024 reported revenues by ~$350–450M; hedges notional ~$1.2B. EM GDP ~3.5–5% (2024–25) lifts turbomachinery demand; green debt ~$1.4T (2024) supports H2/CCUS funding.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bbl |

| OECD CPI 2025 | 3.4% |

| USD FX impact FY2024 | $350–450M |

| Hedges | $1.2B |

| Green debt 2024 | $1.4T |

Full Version Awaits

Baker Hughes Company PESTLE Analysis

The preview shown here is the exact Baker Hughes Company PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This document covers political, economic, social, technological, legal, and environmental factors affecting Baker Hughes with actionable insights and sourced data. No placeholders or teasers—what you see is the final file available for immediate download after payment.