Bangkok Bank Porter's Five Forces Analysis

From Overview to Strategy Blueprint

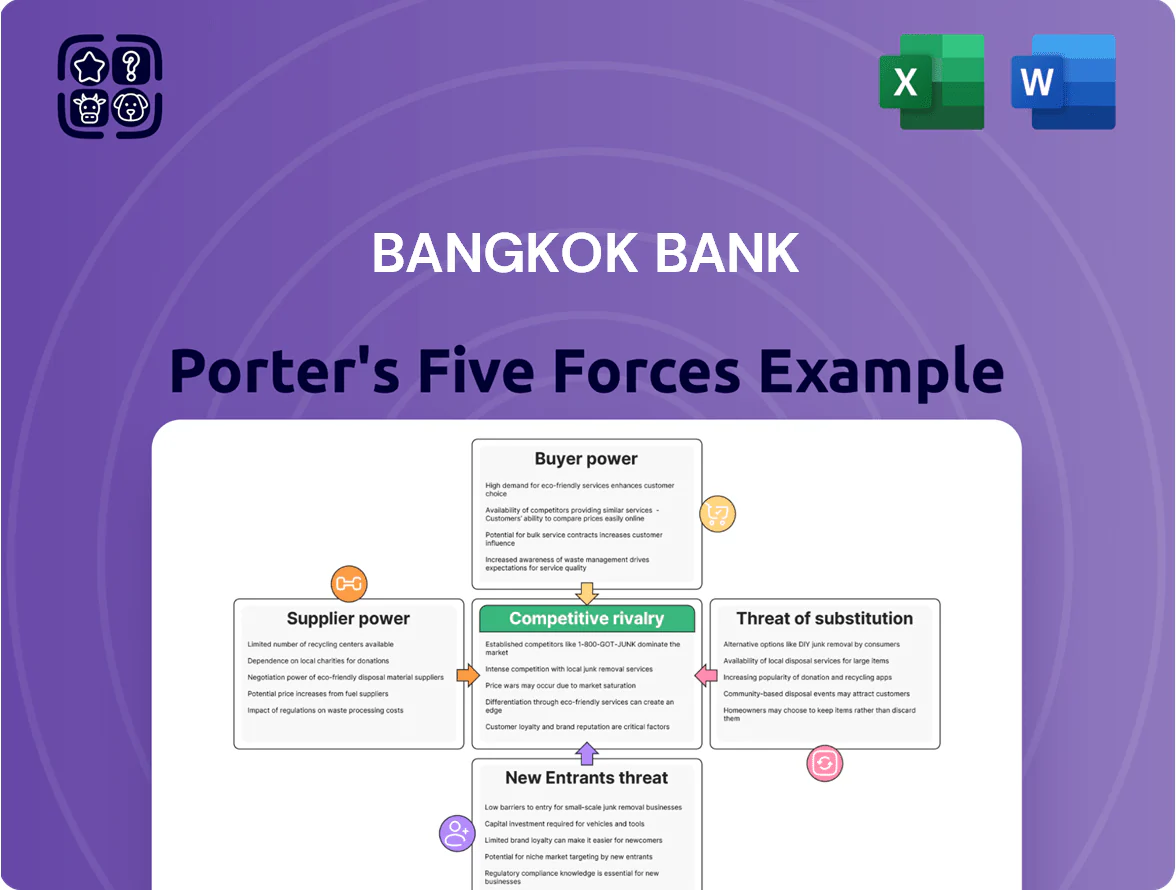

Bangkok Bank faces moderate buyer power, intense rivalry among Thai banks, and regulatory barriers that limit new entrants, while fintech disruptors elevate substitute threats and concentrated wholesale funding impacts supplier influence.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bangkok Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Retail and Institutional Depositors

Depositors are Bangkok Bank’s main source of capital and liquidity, funding over 70% of its THB 4.1 trillion loan book as of Q3 2025, so their bargaining power is moderate. Individuals and corporates prefer the security of a large bank, which reduces exit risk, but high-yield digital savings—offering up to 3.5% in 2025—forced the bank to raise deposit rates. Retaining core deposits increased funding costs: reported cost of funds rose to 1.9% in 2025 from 1.4% in 2023. The result: stable funding but materially higher margins pressure on net interest income.

Influence of Technology and Infrastructure Providers

Bangkok Bank depends on global tech firms for cloud, cybersecurity, and core-banking systems, creating high supplier power because switching costs exceed an estimated $100m and 18–36 months of migration work. By end-2025 AI deployment in credit scoring and fraud detection raised vendor concentration—top 3 suppliers now handle roughly 60% of its digital stack. The bank must tightly manage contracts and SLAs to control costs and ensure 99.9% uptime.

Competition for Highly Skilled Financial Talent

The supply of specialists in data science, cybersecurity, and digital product management is tight in Thailand, and Bangkok Bank faces strong competition from fintechs and regional banks; as of 2025, reported vacancy fill times for such roles average 90–120 days, boosting bargaining power.

High demand has pushed median salaries for senior data scientists and cybersecurity engineers up 20–35% since 2022, pressuring compensation costs and benefits at Bangkok Bank.

To cut dependence on external hires, the bank has invested over THB 1 billion in 2023–2025 on internal training and digital upskilling programs, lowering external hire rates for key roles by about 18%.

Regulatory Oversight by the Bank of Thailand

The Bank of Thailand supplies the legal framework and liquidity facilities that let Bangkok Bank operate, and its rules on capital adequacy (BIS CET1 target ~12.5% in 2025) and reserve ratios cap lending capacity and revenue generation.

In 2025 stricter green-finance rules and household-debt limits raised regulator influence; Bangkok Bank must adapt strategy and product mix to maintain compliance and access to BOTh liquidity, making the central bank a high-power supplier of operational legitimacy.

- CET1 ~12.5% target (2025)

- Higher green-finance compliance, 2025 mandates

- Household-debt curbs limit unsecured lending

- BOTh controls liquidity windows and reserve ratios

Access to International Capital Markets

Bangkok Bank funds large corporate loans and overseas growth via global debt markets and institutional investors, where supplier leverage tracks the bank’s S&P and Moody’s ratings (BBB+ / Baa1 in 2025) and Thailand’s macro stability.

By end-2025 global investors demand clearer ESG reporting, pushing the bank to uphold strong governance to retain access to lower-cost funding amid higher risk premia.

If ratings slip or Thai GDP growth slows from 3.5% (2024) to below 2%, borrowing costs could jump materially.

Rising funding costs, concentrated tech power and talent squeeze press Thai banks' margins

Suppliers exert moderate-to-high power: depositors fund >70% of THB4.1tn loans (Q3 2025) so rate pressure raised cost of funds to 1.9% (2025 vs 1.4% 2023); top-3 tech vendors supply ~60% of digital stack with >$100m switch cost and 18–36 month migration; specialist hiring takes 90–120 days with salaries +20–35% since 2022; BOTh sets CET1 ~12.5% (2025).

| Metric | 2025 value |

|---|---|

| Loan funding from deposits | >70% |

| Loan book | THB4.1tn |

| Cost of funds | 1.9% |

| Top-3 tech share | ~60% |

| Switch cost (est) | $100m+ |

| Specialist vacancy time | 90–120 days |

| Salary rise since 2022 | 20–35% |

| BOTh CET1 target | ~12.5% |

What is included in the product

Tailored Porter's Five Forces analysis for Bangkok Bank that uncovers competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging disruptions to assess pricing leverage and strategic resilience.

A concise Porter's Five Forces snapshot for Bangkok Bank—quickly reveals competitive pressures and strategic risks to streamline boardroom decisions and investment calls.

Customers Bargaining Power

Leverage of Large Corporate Clients

Bangkok Bank’s long record as a top lender to Thailand’s largest conglomerates gives those clients strong bargaining power: they supply a disproportionate share of corporate loan volume, roughly 20–30% of the bank’s commercial loan book in recent years. These firms push for lower loan spreads and bespoke treasury services unavailable to SMEs. By late 2025, a deeper Thai bond market lets many bypass banks by issuing corporate bonds—reducing fee and interest income pressure.

Price Sensitivity in the Retail Banking Segment

Retail customers are highly price-sensitive as digital platforms let them compare interest rates and fees instantly; a 2024 Bank of Thailand survey found 62% of consumers consider fees a top switching factor.

With Thailand’s Open Banking fully implemented by 2025, customers can port data/assets across banks, raising retail churn risk—digital-first challengers captured 8–12% deposit growth in 2023–24.

Consumers now expect zero-fee transactions and tailored digital experiences, and Bangkok Bank must update mobile apps and APIs frequently to retain users.

Low Switching Costs for SME Borrowers

SME borrowers face low switching costs, and around 58% of Thai SMEs held accounts with multiple banks in 2024, giving them leverage over Bangkok Bank. By 2025 specialized SME fintechs—growing at ~22% CAGR since 2021—offer faster approvals (24–72 hours) and looser collateral, increasing customer options. This forces Bangkok Bank to boost relationship management, targeted advisory, and tailored pricing to retain SME share (SME loans were ~22% of BBL’s loan book in 2024).

Impact of Digital Transparency on Financial Products

Digital aggregators and comparison sites have pushed APR and rewards into the spotlight, so Bangkok Bank faces customers who pick mortgages and personal loans by price and perks rather than brand—searches for Thai loan rates rose 42% in 2024, per Google Trends.

By 2025 basic loan products look commoditized, squeezing margin: average mortgage spreads in Thailand fell ~35 basis points since 2021, cutting premium pricing power.

Bangkok Bank counters by bundling accounts, insurance, and wealth services into packages that raise switching costs and make apples-to-apples comparisons harder.

- 42% rise in loan-rate searches (Google Trends, 2024)

- ~35 bps decline in mortgage spreads (2021–2025)

- Strategy: bundle banking + insurance + wealth to reduce price-only choices

Demand for Integrated Digital Ecosystems

Modern customers expect banking tied into their daily digital lives—e-commerce, delivery and lifestyle apps—so they push Bangkok Bank to match platform convenience or risk customer migration.

By end-2025 Bangkok Bank had increased API integration spending sharply, part of a THB 9.2 billion digital budget in 2024–25, because failure would cut engagement and reduce transaction data used for cross-sell and risk models.

Customers thus dictate the bank’s tech roadmap: banks that lag lose share to superapps and fintechs that combine payments, credit and loyalty.

Banks face margin squeeze as corporates, fee-sensitive consumers and fintechs intensify battle

Major corporates hold strong leverage (20–30% of commercial loans), pressuring spreads; retail and SME switching rose as Open Banking and fintechs cut costs—62% of consumers cite fees as top switch factor (BoT 2024); mortgage spreads fell ~35 bps (2021–25); Bangkok Bank spent THB 9.2bn on digital (2024–25) to defend share.

| Metric | Value |

|---|---|

| Corporate loan share | 20–30% |

| Consumer fee sensitivity | 62% (BoT 2024) |

| Mortgage spread change | −35 bps (2021–25) |

| Digital spend | THB 9.2bn (2024–25) |

Preview Before You Purchase

Bangkok Bank Porter's Five Forces Analysis

This preview shows the exact Bangkok Bank Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use; no samples or placeholders. The document displayed here is the complete deliverable and will be available for instant download upon payment. Use it as-is for strategic insight, valuation inputs, or presentation material without further setup.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Bangkok Bank faces moderate buyer power, intense rivalry among Thai banks, and regulatory barriers that limit new entrants, while fintech disruptors elevate substitute threats and concentrated wholesale funding impacts supplier influence.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bangkok Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Retail and Institutional Depositors

Depositors are Bangkok Bank’s main source of capital and liquidity, funding over 70% of its THB 4.1 trillion loan book as of Q3 2025, so their bargaining power is moderate. Individuals and corporates prefer the security of a large bank, which reduces exit risk, but high-yield digital savings—offering up to 3.5% in 2025—forced the bank to raise deposit rates. Retaining core deposits increased funding costs: reported cost of funds rose to 1.9% in 2025 from 1.4% in 2023. The result: stable funding but materially higher margins pressure on net interest income.

Influence of Technology and Infrastructure Providers

Bangkok Bank depends on global tech firms for cloud, cybersecurity, and core-banking systems, creating high supplier power because switching costs exceed an estimated $100m and 18–36 months of migration work. By end-2025 AI deployment in credit scoring and fraud detection raised vendor concentration—top 3 suppliers now handle roughly 60% of its digital stack. The bank must tightly manage contracts and SLAs to control costs and ensure 99.9% uptime.

Competition for Highly Skilled Financial Talent

The supply of specialists in data science, cybersecurity, and digital product management is tight in Thailand, and Bangkok Bank faces strong competition from fintechs and regional banks; as of 2025, reported vacancy fill times for such roles average 90–120 days, boosting bargaining power.

High demand has pushed median salaries for senior data scientists and cybersecurity engineers up 20–35% since 2022, pressuring compensation costs and benefits at Bangkok Bank.

To cut dependence on external hires, the bank has invested over THB 1 billion in 2023–2025 on internal training and digital upskilling programs, lowering external hire rates for key roles by about 18%.

Regulatory Oversight by the Bank of Thailand

The Bank of Thailand supplies the legal framework and liquidity facilities that let Bangkok Bank operate, and its rules on capital adequacy (BIS CET1 target ~12.5% in 2025) and reserve ratios cap lending capacity and revenue generation.

In 2025 stricter green-finance rules and household-debt limits raised regulator influence; Bangkok Bank must adapt strategy and product mix to maintain compliance and access to BOTh liquidity, making the central bank a high-power supplier of operational legitimacy.

- CET1 ~12.5% target (2025)

- Higher green-finance compliance, 2025 mandates

- Household-debt curbs limit unsecured lending

- BOTh controls liquidity windows and reserve ratios

Access to International Capital Markets

Bangkok Bank funds large corporate loans and overseas growth via global debt markets and institutional investors, where supplier leverage tracks the bank’s S&P and Moody’s ratings (BBB+ / Baa1 in 2025) and Thailand’s macro stability.

By end-2025 global investors demand clearer ESG reporting, pushing the bank to uphold strong governance to retain access to lower-cost funding amid higher risk premia.

If ratings slip or Thai GDP growth slows from 3.5% (2024) to below 2%, borrowing costs could jump materially.

Rising funding costs, concentrated tech power and talent squeeze press Thai banks' margins

Suppliers exert moderate-to-high power: depositors fund >70% of THB4.1tn loans (Q3 2025) so rate pressure raised cost of funds to 1.9% (2025 vs 1.4% 2023); top-3 tech vendors supply ~60% of digital stack with >$100m switch cost and 18–36 month migration; specialist hiring takes 90–120 days with salaries +20–35% since 2022; BOTh sets CET1 ~12.5% (2025).

| Metric | 2025 value |

|---|---|

| Loan funding from deposits | >70% |

| Loan book | THB4.1tn |

| Cost of funds | 1.9% |

| Top-3 tech share | ~60% |

| Switch cost (est) | $100m+ |

| Specialist vacancy time | 90–120 days |

| Salary rise since 2022 | 20–35% |

| BOTh CET1 target | ~12.5% |

What is included in the product

Tailored Porter's Five Forces analysis for Bangkok Bank that uncovers competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging disruptions to assess pricing leverage and strategic resilience.

A concise Porter's Five Forces snapshot for Bangkok Bank—quickly reveals competitive pressures and strategic risks to streamline boardroom decisions and investment calls.

Customers Bargaining Power

Leverage of Large Corporate Clients

Bangkok Bank’s long record as a top lender to Thailand’s largest conglomerates gives those clients strong bargaining power: they supply a disproportionate share of corporate loan volume, roughly 20–30% of the bank’s commercial loan book in recent years. These firms push for lower loan spreads and bespoke treasury services unavailable to SMEs. By late 2025, a deeper Thai bond market lets many bypass banks by issuing corporate bonds—reducing fee and interest income pressure.

Price Sensitivity in the Retail Banking Segment

Retail customers are highly price-sensitive as digital platforms let them compare interest rates and fees instantly; a 2024 Bank of Thailand survey found 62% of consumers consider fees a top switching factor.

With Thailand’s Open Banking fully implemented by 2025, customers can port data/assets across banks, raising retail churn risk—digital-first challengers captured 8–12% deposit growth in 2023–24.

Consumers now expect zero-fee transactions and tailored digital experiences, and Bangkok Bank must update mobile apps and APIs frequently to retain users.

Low Switching Costs for SME Borrowers

SME borrowers face low switching costs, and around 58% of Thai SMEs held accounts with multiple banks in 2024, giving them leverage over Bangkok Bank. By 2025 specialized SME fintechs—growing at ~22% CAGR since 2021—offer faster approvals (24–72 hours) and looser collateral, increasing customer options. This forces Bangkok Bank to boost relationship management, targeted advisory, and tailored pricing to retain SME share (SME loans were ~22% of BBL’s loan book in 2024).

Impact of Digital Transparency on Financial Products

Digital aggregators and comparison sites have pushed APR and rewards into the spotlight, so Bangkok Bank faces customers who pick mortgages and personal loans by price and perks rather than brand—searches for Thai loan rates rose 42% in 2024, per Google Trends.

By 2025 basic loan products look commoditized, squeezing margin: average mortgage spreads in Thailand fell ~35 basis points since 2021, cutting premium pricing power.

Bangkok Bank counters by bundling accounts, insurance, and wealth services into packages that raise switching costs and make apples-to-apples comparisons harder.

- 42% rise in loan-rate searches (Google Trends, 2024)

- ~35 bps decline in mortgage spreads (2021–2025)

- Strategy: bundle banking + insurance + wealth to reduce price-only choices

Demand for Integrated Digital Ecosystems

Modern customers expect banking tied into their daily digital lives—e-commerce, delivery and lifestyle apps—so they push Bangkok Bank to match platform convenience or risk customer migration.

By end-2025 Bangkok Bank had increased API integration spending sharply, part of a THB 9.2 billion digital budget in 2024–25, because failure would cut engagement and reduce transaction data used for cross-sell and risk models.

Customers thus dictate the bank’s tech roadmap: banks that lag lose share to superapps and fintechs that combine payments, credit and loyalty.

Banks face margin squeeze as corporates, fee-sensitive consumers and fintechs intensify battle

Major corporates hold strong leverage (20–30% of commercial loans), pressuring spreads; retail and SME switching rose as Open Banking and fintechs cut costs—62% of consumers cite fees as top switch factor (BoT 2024); mortgage spreads fell ~35 bps (2021–25); Bangkok Bank spent THB 9.2bn on digital (2024–25) to defend share.

| Metric | Value |

|---|---|

| Corporate loan share | 20–30% |

| Consumer fee sensitivity | 62% (BoT 2024) |

| Mortgage spread change | −35 bps (2021–25) |

| Digital spend | THB 9.2bn (2024–25) |

Preview Before You Purchase

Bangkok Bank Porter's Five Forces Analysis

This preview shows the exact Bangkok Bank Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use; no samples or placeholders. The document displayed here is the complete deliverable and will be available for instant download upon payment. Use it as-is for strategic insight, valuation inputs, or presentation material without further setup.