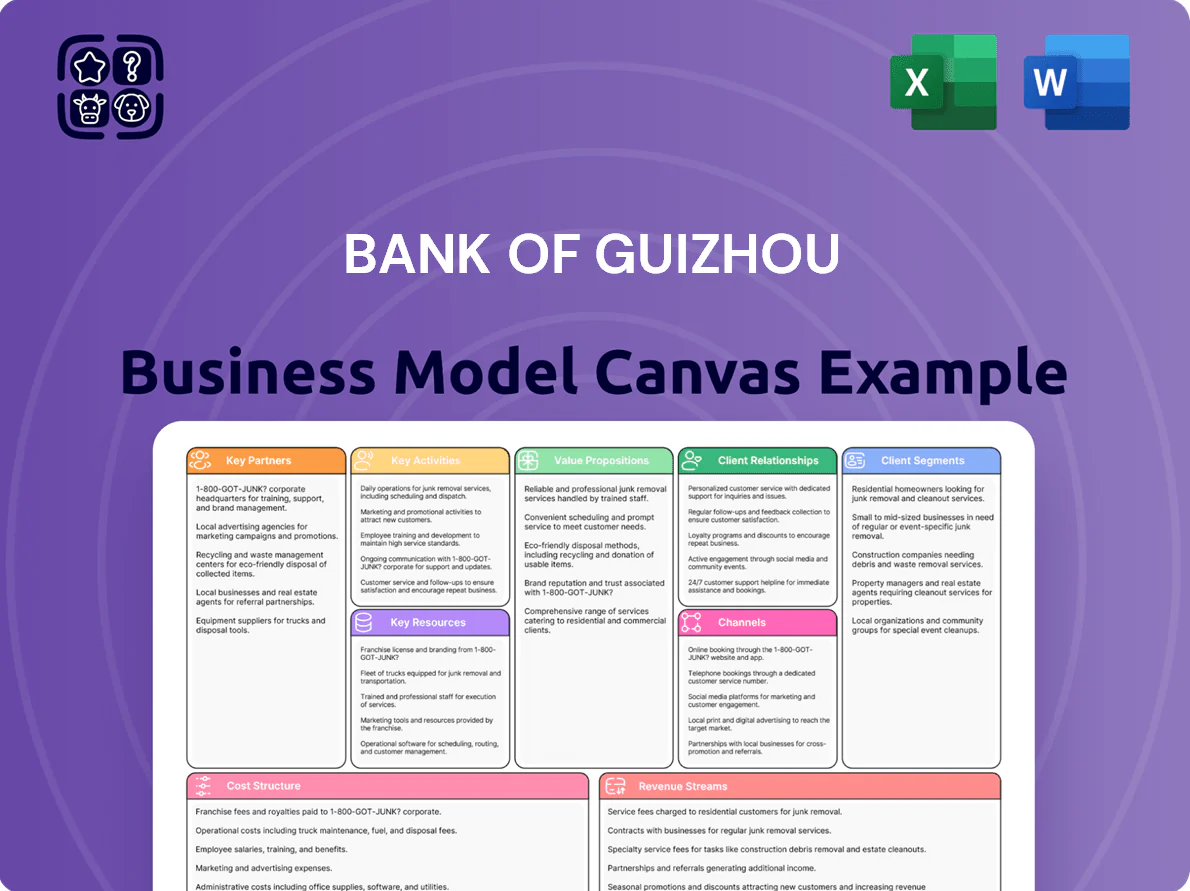

Bank of Guizhou Business Model Canvas

Bank of Guizhou BMC: Strategic Blueprint & Ready-to-Use Templates for Investors

Unlock the full strategic blueprint behind Bank of Guizhou’s business model—this in-depth Business Model Canvas reveals how the bank creates value, targets customer segments, and sustains competitive advantage; perfect for investors, consultants, and strategists seeking actionable insights and ready-to-use Word/Excel templates to benchmark or adapt its proven approach.

Partnerships

Guizhou Provincial Government

The bank’s strategic alliance with the Guizhou Provincial Government channels government-led infrastructure lending and mandates, accounting for roughly CNY 48.3 billion in public-sector loan originations and CNY 72.6 billion in government deposits through 2025, securing predictable funding and fee income.

Kweichow Moutai Group

As a major shareholder holding roughly 17% of Bank of Guizhou (2024 annual report), Kweichow Moutai Group supplies capital stability and brand prestige, boosting the bank’s Tier 1 capital and lowering funding costs. The tie enables joint finance for the liquor supply chain—Moutai’s 2024 revenue ¥122.3bn—improving loan origination and deposit flows and adds board seats that strengthen governance and liquidity oversight.

Interbank Financial Institutions

Collaborations with national banks like Industrial and Commercial Bank of China and international banks (eg. HSBC) let Bank of Guizhou manage liquidity—interbank lines grew 18% to CNY 32.4bn in 2024—while accessing global capital markets for FX and bond placement. By 2025 these alliances enable complex treasury ops, diversified investment products, risk sharing and integration with advanced CIPS and SWIFT gpi clearing/settlement rails.

Fintech and Technology Providers

The bank partners with leading tech firms—including Alibaba Cloud and Tencent Cloud in China—to accelerate digital transformation, supporting mobile banking, cloud-based services, and big-data credit scoring; by 2024 Bank of Guizhou reported a 38% year-on-year rise in digital transactions, driven by these vendor platforms.

- Cloud providers: Alibaba/Tencent — cloud hosting, security

- Cybersecurity vendors — PCI/DDoS protection

- Analytics firms — automated credit scoring, risk models

- Result: 38% rise in digital transactions (2024)

Agricultural and Rural Cooperatives

The bank partners with over 1,200 agricultural and rural cooperatives across Guizhou to channel micro-loans and deposits to remote farmers, supporting its rural revitalization mandate and covering areas where 62% of residents lack easy branch access.

Cooperatives serve as low-cost distribution points—handling KYC, loan screening, and collection—helping Bank of Guizhou originate ~RMB 4.3 billion in micro-loans to rural clients in 2024 and grow rural deposit balances by 18% year-over-year.

- 1,200+ cooperatives networked

- RMB 4.3 billion micro-loans (2024)

- Rural deposits +18% YoY (2024)

- Covers areas where 62% lack branch access

Strategic state, Moutai, banks & tech tie-ups: CNY liquidity, rural reach & digital growth

Strategic ties with Guizhou government (CNY48.3bn loans, CNY72.6bn deposits by 2025), Kweichow Moutai (17% shareholder) and major banks (interbank lines CNY32.4bn, +18% 2024) plus Alibaba/Tencent cloud and 1,200+ cooperatives (RMB4.3bn micro-loans, rural deposits +18% 2024) secure funding, brand, liquidity, tech and rural distribution.

| Partner | Key metric |

|---|---|

| Guizhou govt | CNY48.3bn loans/CNY72.6bn deposits |

| Kweichow Moutai | 17% ownership |

| Interbank | CNY32.4bn lines (+18% 2024) |

| Tech | Digital tx +38% 2024 |

| Cooperatives | 1,200+; RMB4.3bn micro-loans |

What is included in the product

A concise, pre-written Business Model Canvas for Bank of Guizhou detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance aligned to its regional commercial banking strategy.

High-level view of Bank of Guizhou’s business model with editable cells, helping teams quickly map revenue streams, customer segments, and risk controls to relieve strategic and operational pain points.

Activities

Credit and Risk Management

The bank prioritizes rigorous credit assessments for corporate and retail borrowers, using advanced data models and local market intel to keep NPLs low; Guizhou Bank reported a 0.9% NPL ratio in Q4 2025 and CET1 at 11.8% after provisioning. By end-2025 it deployed AI-driven risk tools for real-time monitoring across CNY 320bn in loans, cutting early-default alerts by 35% year-on-year.

Corporate and Retail Lending

Bank of Guizhou issues loans from RMB 10k consumer credits to RMB 2.5bn infrastructure financings, tailoring terms for energy, manufacturing and tourism clients in Guizhou; lending drove 67% of net interest income in 2024, with outstanding loans at RMB 312.4bn as of 31 Dec 2024.

Digital Banking Development

Continuous investment in mobile and online platforms is a top priority: Bank of Guizhou reported a 28% year‑on‑year increase in digital transactions in 2024, lowering branch footfall by 15% and cutting transaction costs ~18%. The bank automates routine payments and adds products—now 62% of retail deposits and 54% of loan applications flow via digital channels—meeting 24/7 demand from younger, tech‑savvy customers.

Treasury and Investment Operations

The bank manages liquidity and capital adequacy via active money‑market and bond trading, holding about RMB 120 billion in government and corporate securities (2025 YE) to earn yield on idle cash while meeting reserve requirements.

Strategic asset‑liability management (ALM) hedges interest‑rate risk, targets an LCR of ~130% and NIM preservation, and rebalances duration to stay resilient against volatility.

- RMB 120bn securities portfolio (2025 YE)

- LCR ~130%

- Focus: NIM preservation, duration rebalancing

Community and Rural Outreach

The bank runs mobile service points and monthly on-site visits to SMEs and farms, improving financial literacy for ~1.2 million rural customers and increasing rural deposit share to 27.4% in 2025, supporting credit to agriculture worth CNY 18.6 billion.

- Mobile units: 220 routes (2025)

- Rural customers reached: ~1.2M (2025)

- Rural deposits: 27.4% of total (2025)

- Agriculture credit: CNY 18.6B (2025)

AI-driven underwriting fuels digital growth: RMB312.4bn loans, 0.9% NPL, 28% txn rise

Key activities: disciplined credit underwriting and AI risk-monitoring across CNY 320bn loans (35% fewer early-default alerts y/y), targeted lending (RMB 10k–2.5bn) driving 67% of NII with loans at RMB 312.4bn (31 Dec 2024), digital growth (62% retail deposits via apps; 28% rise in digital txns 2024), RMB 120bn securities (2025 YE) and ALM targeting LCR ~130%.

| Metric | Value |

|---|---|

| NPL ratio (Q4 2025) | 0.9% |

| Loans outstanding (31‑Dec‑2024) | RMB 312.4bn |

| AI coverage | CNY 320bn loans |

| Digital txn growth (2024) | 28% |

| Rural customers (2025) | ~1.2M |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank of Guizhou Business Model Canvas—not a mockup or sample—and it reflects the exact content and layout you’ll receive after purchase.

Upon completing your order, you’ll get this same professional, ready-to-use file in editable formats, with all sections and pages included exactly as shown.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bank of Guizhou BMC: Strategic Blueprint & Ready-to-Use Templates for Investors

Unlock the full strategic blueprint behind Bank of Guizhou’s business model—this in-depth Business Model Canvas reveals how the bank creates value, targets customer segments, and sustains competitive advantage; perfect for investors, consultants, and strategists seeking actionable insights and ready-to-use Word/Excel templates to benchmark or adapt its proven approach.

Partnerships

Guizhou Provincial Government

The bank’s strategic alliance with the Guizhou Provincial Government channels government-led infrastructure lending and mandates, accounting for roughly CNY 48.3 billion in public-sector loan originations and CNY 72.6 billion in government deposits through 2025, securing predictable funding and fee income.

Kweichow Moutai Group

As a major shareholder holding roughly 17% of Bank of Guizhou (2024 annual report), Kweichow Moutai Group supplies capital stability and brand prestige, boosting the bank’s Tier 1 capital and lowering funding costs. The tie enables joint finance for the liquor supply chain—Moutai’s 2024 revenue ¥122.3bn—improving loan origination and deposit flows and adds board seats that strengthen governance and liquidity oversight.

Interbank Financial Institutions

Collaborations with national banks like Industrial and Commercial Bank of China and international banks (eg. HSBC) let Bank of Guizhou manage liquidity—interbank lines grew 18% to CNY 32.4bn in 2024—while accessing global capital markets for FX and bond placement. By 2025 these alliances enable complex treasury ops, diversified investment products, risk sharing and integration with advanced CIPS and SWIFT gpi clearing/settlement rails.

Fintech and Technology Providers

The bank partners with leading tech firms—including Alibaba Cloud and Tencent Cloud in China—to accelerate digital transformation, supporting mobile banking, cloud-based services, and big-data credit scoring; by 2024 Bank of Guizhou reported a 38% year-on-year rise in digital transactions, driven by these vendor platforms.

- Cloud providers: Alibaba/Tencent — cloud hosting, security

- Cybersecurity vendors — PCI/DDoS protection

- Analytics firms — automated credit scoring, risk models

- Result: 38% rise in digital transactions (2024)

Agricultural and Rural Cooperatives

The bank partners with over 1,200 agricultural and rural cooperatives across Guizhou to channel micro-loans and deposits to remote farmers, supporting its rural revitalization mandate and covering areas where 62% of residents lack easy branch access.

Cooperatives serve as low-cost distribution points—handling KYC, loan screening, and collection—helping Bank of Guizhou originate ~RMB 4.3 billion in micro-loans to rural clients in 2024 and grow rural deposit balances by 18% year-over-year.

- 1,200+ cooperatives networked

- RMB 4.3 billion micro-loans (2024)

- Rural deposits +18% YoY (2024)

- Covers areas where 62% lack branch access

Strategic state, Moutai, banks & tech tie-ups: CNY liquidity, rural reach & digital growth

Strategic ties with Guizhou government (CNY48.3bn loans, CNY72.6bn deposits by 2025), Kweichow Moutai (17% shareholder) and major banks (interbank lines CNY32.4bn, +18% 2024) plus Alibaba/Tencent cloud and 1,200+ cooperatives (RMB4.3bn micro-loans, rural deposits +18% 2024) secure funding, brand, liquidity, tech and rural distribution.

| Partner | Key metric |

|---|---|

| Guizhou govt | CNY48.3bn loans/CNY72.6bn deposits |

| Kweichow Moutai | 17% ownership |

| Interbank | CNY32.4bn lines (+18% 2024) |

| Tech | Digital tx +38% 2024 |

| Cooperatives | 1,200+; RMB4.3bn micro-loans |

What is included in the product

A concise, pre-written Business Model Canvas for Bank of Guizhou detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance aligned to its regional commercial banking strategy.

High-level view of Bank of Guizhou’s business model with editable cells, helping teams quickly map revenue streams, customer segments, and risk controls to relieve strategic and operational pain points.

Activities

Credit and Risk Management

The bank prioritizes rigorous credit assessments for corporate and retail borrowers, using advanced data models and local market intel to keep NPLs low; Guizhou Bank reported a 0.9% NPL ratio in Q4 2025 and CET1 at 11.8% after provisioning. By end-2025 it deployed AI-driven risk tools for real-time monitoring across CNY 320bn in loans, cutting early-default alerts by 35% year-on-year.

Corporate and Retail Lending

Bank of Guizhou issues loans from RMB 10k consumer credits to RMB 2.5bn infrastructure financings, tailoring terms for energy, manufacturing and tourism clients in Guizhou; lending drove 67% of net interest income in 2024, with outstanding loans at RMB 312.4bn as of 31 Dec 2024.

Digital Banking Development

Continuous investment in mobile and online platforms is a top priority: Bank of Guizhou reported a 28% year‑on‑year increase in digital transactions in 2024, lowering branch footfall by 15% and cutting transaction costs ~18%. The bank automates routine payments and adds products—now 62% of retail deposits and 54% of loan applications flow via digital channels—meeting 24/7 demand from younger, tech‑savvy customers.

Treasury and Investment Operations

The bank manages liquidity and capital adequacy via active money‑market and bond trading, holding about RMB 120 billion in government and corporate securities (2025 YE) to earn yield on idle cash while meeting reserve requirements.

Strategic asset‑liability management (ALM) hedges interest‑rate risk, targets an LCR of ~130% and NIM preservation, and rebalances duration to stay resilient against volatility.

- RMB 120bn securities portfolio (2025 YE)

- LCR ~130%

- Focus: NIM preservation, duration rebalancing

Community and Rural Outreach

The bank runs mobile service points and monthly on-site visits to SMEs and farms, improving financial literacy for ~1.2 million rural customers and increasing rural deposit share to 27.4% in 2025, supporting credit to agriculture worth CNY 18.6 billion.

- Mobile units: 220 routes (2025)

- Rural customers reached: ~1.2M (2025)

- Rural deposits: 27.4% of total (2025)

- Agriculture credit: CNY 18.6B (2025)

AI-driven underwriting fuels digital growth: RMB312.4bn loans, 0.9% NPL, 28% txn rise

Key activities: disciplined credit underwriting and AI risk-monitoring across CNY 320bn loans (35% fewer early-default alerts y/y), targeted lending (RMB 10k–2.5bn) driving 67% of NII with loans at RMB 312.4bn (31 Dec 2024), digital growth (62% retail deposits via apps; 28% rise in digital txns 2024), RMB 120bn securities (2025 YE) and ALM targeting LCR ~130%.

| Metric | Value |

|---|---|

| NPL ratio (Q4 2025) | 0.9% |

| Loans outstanding (31‑Dec‑2024) | RMB 312.4bn |

| AI coverage | CNY 320bn loans |

| Digital txn growth (2024) | 28% |

| Rural customers (2025) | ~1.2M |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank of Guizhou Business Model Canvas—not a mockup or sample—and it reflects the exact content and layout you’ll receive after purchase.

Upon completing your order, you’ll get this same professional, ready-to-use file in editable formats, with all sections and pages included exactly as shown.