Bank of Guizhou PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Understand how political oversight, regional economic growth, and rapid fintech adoption shape Bank of Guizhou's trajectory—our concise PESTLE highlights regulatory risks, macroeconomic drivers, and technological opportunities that matter to investors and strategists; purchase the full analysis to access detailed, ready-to-use insights and actionable recommendations.

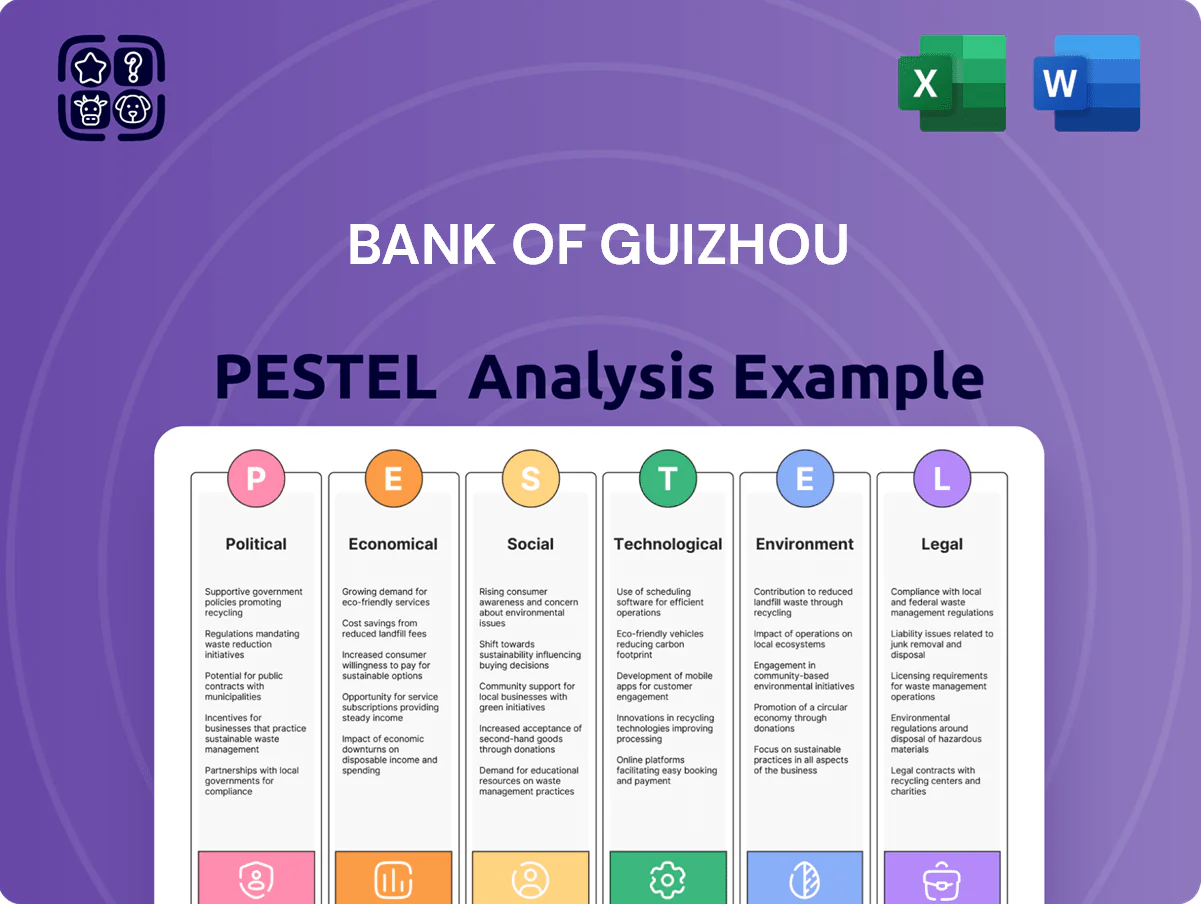

Political factors

Support for National Regional Development

Bank of Guizhou serves as a primary vehicle for China’s Western Development and Rural Revitalization in Guizhou, channeling roughly CNY 120–150 billion (2024–25) toward provincial infrastructure and agricultural loans, per provincial financing disclosures.

By aligning its loan book with state-mandated projects—transport, water, and specialty agriculture—the bank sustains close ties with provincial authorities and local SOEs.

This strategic alignment secures preferential policy support, including priority access to re-lending and relief measures, keeping the bank central to Guizhou’s socio-economic goals through 2026.

Local Government Debt Management

As a provincial lender, Bank of Guizhou is shaped by national directives on LGFV debt restructuring: China’s 2023–25 push cut implicit local guarantees, and provincial swap pilots reached Rmb1.2 trillion nationally by end-2024, forcing the bank to weigh political loyalty against asset-quality deterioration; tighter central oversight—fiscal stress ratios rising in 2024—means active participation in debt-swap programs is vital to preserve liquidity and limit systemic risk in Guizhou’s financial network.

Regulatory Alignment with Central Authorities

The bank must comply with NFRA directives on risk management and a phased capital adequacy target—CAR maintained above 11.5% as of 2025—while central policy emphasizes stability over expansion.

Political pressure to lend to SMEs conflicts with stricter NPL ratios limits; Guizhou Bank reported an NPL ratio of 1.9% in 2024, constraining aggressive SME credit growth.

Influence of State Ownership

The Guizhou Provincial Finance Bureau and state-owned enterprises held about 33% of Bank of Guizhou’s shares as of 2024, ensuring close Communist Party oversight of strategic decisions and board appointments.

This ownership offers a stability buffer during market stress—state backing aided liquidity in 2022–2023—but can prompt directed, non-commercial lending to support local employment and social projects.

Investors should price in the bank’s hybrid role: commercial return targets tempered by regional policy objectives and potential contingent liabilities.

- State shareholding ~33% (2024)

- Provides political oversight and stability support

- Raises risk of policy-driven non-commercial lending

- Investors must factor dual commercial/public mandate

Geopolitical Trade and Investment Impacts

Geopolitical trade policies shaping liquor and mining exports materially affect Bank of Guizhou’s corporate borrowers; Guizhou liquor accounted for about 10% of provincial industrial output in 2024, making trade shifts significant for credit demand.

Changes in China’s international relations and FDI flows into Western China—FDI in Guizhou rose ~6% in 2024—can alter asset quality across industrial loans and mining exposure.

Continuous monitoring of macro-political trends is essential to forecast sectoral NPL risk and long-term asset performance.

- 10% provincial output: liquor (2024)

- FDI into Guizhou +6% (2024)

- Trade/relations affect export demand, corporate credit quality

Bank of Guizhou deploys CNY120–150bn to provincial projects; CAR>11.5%, NPL 1.9%

Bank of Guizhou channels CNY 120–150bn (2024–25) to provincial projects, with state shareholding ~33% (2024) and CAR >11.5% (2025); NPL 1.9% (2024) limits SME lending while LGFV swaps (national Rmb1.2trn end-2024) and +6% FDI (Guizhou 2024) shape asset risk and policy-directed credit.

| Metric | Value |

|---|---|

| Provincial lending | CNY 120–150bn |

| State ownership | 33% |

| NPL ratio | 1.9% |

| CAR | >11.5% |

| LGFV swap (national) | Rmb1.2trn |

| FDI Guizhou | +6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Bank of Guizhou across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and investors identify risks, opportunities, and strategic responses tailored to the bank’s regional market and regulatory context.

A concise PESTLE snapshot of Bank of Guizhou that highlights regulatory, economic, social, technological, environmental, and legal factors for quick reference in meetings or presentations.

Economic factors

Provincial GDP Growth and Industrial Shift

Guizhou's GDP grew 7.2% in 2024 as the province shifts from heavy industry to big data and green energy, with the digital economy accounting for 18% of provincial GDP and renewables investment rising 24% YoY.

For Bank of Guizhou this creates lending opportunities in cloud, AI and wind/solar projects but reduces demand for high-speed infrastructure financing.

The bank must reprice long-term credit risks—NPL exposure to traditional sectors fell to 3.1% while tech-sector lending grew 31%—and design tailored credit, leasing and VC-style products for a diversified economy.

Net Interest Margin Compression

Bank of Guizhou faces net interest margin compression as the People’s Bank of China kept loan prime rates near record lows in 2024–25, squeezing loan yields; China's average NIM for small banks fell to ~2.0% in 2024, pressuring regional peers. With rising competition for stable deposits, profitability hinges on optimizing liability mix and duration. Management is boosting fee income and wealth-management products, which rose ~18% YoY in 2024 to partly offset narrowing lending spreads.

Real Estate Market Stabilization

The ongoing correction in China’s property sector has pressured Bank of Guizhou’s mortgage book and developer exposure, with national home prices down about 2.5% YoY in 2024 and provincial declines larger in second-tier cities, reducing collateral values.

Provincial support measures, including 2024 liquidity facilities and targeted bond issuances, have stabilized transactions but residual valuation risk remains for the bank’s real estate-linked loans.

Proactive provisioning—loan-loss reserves rising to 1.8% of total loans by mid-2025 in similar regional banks—and tighter lending to developers and construction projects are prudent to limit balance-sheet stress from potential defaults.

Inflationary Trends and Purchasing Power

Regional CPI in Guizhou rose 2.6% year-on-year in 2025, affecting Bank of Guizhou’s operating costs and borrowers’ loan-servicing capacity; moderate inflation supports nominal loan and deposit growth while volatile food and energy (food inflation spiked 5.1% in 2025) compresses retail disposable income.

The bank monitors CPI and PPI monthly to recalibrate consumer product pricing and interest-rate models for 2026 to manage credit risk and margin pressure.

- 2025 CPI Guizhou: 2.6% YoY

- Food inflation 2025: 5.1% YoY

- Action: monthly CPI/PPI monitoring; adjust pricing and credit policies for 2026

LGFV Exposure and Asset Quality

The economic health of LGFVs is pivotal for Bank of Guizhou’s asset quality; as of 2024 provincial LGFV debt in Guizhou-linked projects exceeded RMB 320bn, raising default and restructuring risks amid slower local GDP growth of 5.1% in 2024.

Local slowdowns can strain LGFV repayments, prompting extensions—47% of the bank’s project loans tied to municipal financing need close monitoring to avoid provisioning pressure.

Investors track the bank’s capacity to absorb LGFV losses without capital erosion; Bank of Guizhou’s CET1-like ratio stood near 9.8% in 2024, a key resilience metric.

- RMB 320bn+ Guizhou LGFV-linked debt (2024)

- Guizhou GDP growth 5.1% (2024)

- 47% of project loans tied to municipal financing

- CET1-like ratio ~9.8% (2024)

Guizhou 2024: 7.2% GDP, digital 18%, renewables +24%—banks face NIM squeeze, tech lending surges

Guizhou GDP 2024: 7.2%; digital economy 18% of GDP; renewables investment +24% YoY. Bank opportunities: cloud/AI, wind/solar; tech lending +31%, NPLs in traditional sectors 3.1%. NIM pressure: small-bank avg NIM ~2.0% (2024); wealth fees +18% YoY. LGFV debt >RMB320bn; 47% project loans tied to municipal financing; CET1-like ~9.8% (2024).

| Metric | Value |

|---|---|

| Guizhou GDP growth 2024 | 7.2% |

| Digital economy | 18% GDP |

| Renewables investment | +24% YoY |

| Tech lending growth | +31% YoY |

| NPL traditional | 3.1% |

| Small-bank NIM 2024 | ~2.0% |

| Wealth fees | +18% YoY |

| LGFV debt (Guizhou) | RMB 320bn+ |

| Project loans tied to municipalities | 47% |

| CET1-like ratio | ~9.8% |

Same Document Delivered

Bank of Guizhou PESTLE Analysis

The preview shown here is the exact Bank of Guizhou PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Understand how political oversight, regional economic growth, and rapid fintech adoption shape Bank of Guizhou's trajectory—our concise PESTLE highlights regulatory risks, macroeconomic drivers, and technological opportunities that matter to investors and strategists; purchase the full analysis to access detailed, ready-to-use insights and actionable recommendations.

Political factors

Support for National Regional Development

Bank of Guizhou serves as a primary vehicle for China’s Western Development and Rural Revitalization in Guizhou, channeling roughly CNY 120–150 billion (2024–25) toward provincial infrastructure and agricultural loans, per provincial financing disclosures.

By aligning its loan book with state-mandated projects—transport, water, and specialty agriculture—the bank sustains close ties with provincial authorities and local SOEs.

This strategic alignment secures preferential policy support, including priority access to re-lending and relief measures, keeping the bank central to Guizhou’s socio-economic goals through 2026.

Local Government Debt Management

As a provincial lender, Bank of Guizhou is shaped by national directives on LGFV debt restructuring: China’s 2023–25 push cut implicit local guarantees, and provincial swap pilots reached Rmb1.2 trillion nationally by end-2024, forcing the bank to weigh political loyalty against asset-quality deterioration; tighter central oversight—fiscal stress ratios rising in 2024—means active participation in debt-swap programs is vital to preserve liquidity and limit systemic risk in Guizhou’s financial network.

Regulatory Alignment with Central Authorities

The bank must comply with NFRA directives on risk management and a phased capital adequacy target—CAR maintained above 11.5% as of 2025—while central policy emphasizes stability over expansion.

Political pressure to lend to SMEs conflicts with stricter NPL ratios limits; Guizhou Bank reported an NPL ratio of 1.9% in 2024, constraining aggressive SME credit growth.

Influence of State Ownership

The Guizhou Provincial Finance Bureau and state-owned enterprises held about 33% of Bank of Guizhou’s shares as of 2024, ensuring close Communist Party oversight of strategic decisions and board appointments.

This ownership offers a stability buffer during market stress—state backing aided liquidity in 2022–2023—but can prompt directed, non-commercial lending to support local employment and social projects.

Investors should price in the bank’s hybrid role: commercial return targets tempered by regional policy objectives and potential contingent liabilities.

- State shareholding ~33% (2024)

- Provides political oversight and stability support

- Raises risk of policy-driven non-commercial lending

- Investors must factor dual commercial/public mandate

Geopolitical Trade and Investment Impacts

Geopolitical trade policies shaping liquor and mining exports materially affect Bank of Guizhou’s corporate borrowers; Guizhou liquor accounted for about 10% of provincial industrial output in 2024, making trade shifts significant for credit demand.

Changes in China’s international relations and FDI flows into Western China—FDI in Guizhou rose ~6% in 2024—can alter asset quality across industrial loans and mining exposure.

Continuous monitoring of macro-political trends is essential to forecast sectoral NPL risk and long-term asset performance.

- 10% provincial output: liquor (2024)

- FDI into Guizhou +6% (2024)

- Trade/relations affect export demand, corporate credit quality

Bank of Guizhou deploys CNY120–150bn to provincial projects; CAR>11.5%, NPL 1.9%

Bank of Guizhou channels CNY 120–150bn (2024–25) to provincial projects, with state shareholding ~33% (2024) and CAR >11.5% (2025); NPL 1.9% (2024) limits SME lending while LGFV swaps (national Rmb1.2trn end-2024) and +6% FDI (Guizhou 2024) shape asset risk and policy-directed credit.

| Metric | Value |

|---|---|

| Provincial lending | CNY 120–150bn |

| State ownership | 33% |

| NPL ratio | 1.9% |

| CAR | >11.5% |

| LGFV swap (national) | Rmb1.2trn |

| FDI Guizhou | +6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Bank of Guizhou across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and investors identify risks, opportunities, and strategic responses tailored to the bank’s regional market and regulatory context.

A concise PESTLE snapshot of Bank of Guizhou that highlights regulatory, economic, social, technological, environmental, and legal factors for quick reference in meetings or presentations.

Economic factors

Provincial GDP Growth and Industrial Shift

Guizhou's GDP grew 7.2% in 2024 as the province shifts from heavy industry to big data and green energy, with the digital economy accounting for 18% of provincial GDP and renewables investment rising 24% YoY.

For Bank of Guizhou this creates lending opportunities in cloud, AI and wind/solar projects but reduces demand for high-speed infrastructure financing.

The bank must reprice long-term credit risks—NPL exposure to traditional sectors fell to 3.1% while tech-sector lending grew 31%—and design tailored credit, leasing and VC-style products for a diversified economy.

Net Interest Margin Compression

Bank of Guizhou faces net interest margin compression as the People’s Bank of China kept loan prime rates near record lows in 2024–25, squeezing loan yields; China's average NIM for small banks fell to ~2.0% in 2024, pressuring regional peers. With rising competition for stable deposits, profitability hinges on optimizing liability mix and duration. Management is boosting fee income and wealth-management products, which rose ~18% YoY in 2024 to partly offset narrowing lending spreads.

Real Estate Market Stabilization

The ongoing correction in China’s property sector has pressured Bank of Guizhou’s mortgage book and developer exposure, with national home prices down about 2.5% YoY in 2024 and provincial declines larger in second-tier cities, reducing collateral values.

Provincial support measures, including 2024 liquidity facilities and targeted bond issuances, have stabilized transactions but residual valuation risk remains for the bank’s real estate-linked loans.

Proactive provisioning—loan-loss reserves rising to 1.8% of total loans by mid-2025 in similar regional banks—and tighter lending to developers and construction projects are prudent to limit balance-sheet stress from potential defaults.

Inflationary Trends and Purchasing Power

Regional CPI in Guizhou rose 2.6% year-on-year in 2025, affecting Bank of Guizhou’s operating costs and borrowers’ loan-servicing capacity; moderate inflation supports nominal loan and deposit growth while volatile food and energy (food inflation spiked 5.1% in 2025) compresses retail disposable income.

The bank monitors CPI and PPI monthly to recalibrate consumer product pricing and interest-rate models for 2026 to manage credit risk and margin pressure.

- 2025 CPI Guizhou: 2.6% YoY

- Food inflation 2025: 5.1% YoY

- Action: monthly CPI/PPI monitoring; adjust pricing and credit policies for 2026

LGFV Exposure and Asset Quality

The economic health of LGFVs is pivotal for Bank of Guizhou’s asset quality; as of 2024 provincial LGFV debt in Guizhou-linked projects exceeded RMB 320bn, raising default and restructuring risks amid slower local GDP growth of 5.1% in 2024.

Local slowdowns can strain LGFV repayments, prompting extensions—47% of the bank’s project loans tied to municipal financing need close monitoring to avoid provisioning pressure.

Investors track the bank’s capacity to absorb LGFV losses without capital erosion; Bank of Guizhou’s CET1-like ratio stood near 9.8% in 2024, a key resilience metric.

- RMB 320bn+ Guizhou LGFV-linked debt (2024)

- Guizhou GDP growth 5.1% (2024)

- 47% of project loans tied to municipal financing

- CET1-like ratio ~9.8% (2024)

Guizhou 2024: 7.2% GDP, digital 18%, renewables +24%—banks face NIM squeeze, tech lending surges

Guizhou GDP 2024: 7.2%; digital economy 18% of GDP; renewables investment +24% YoY. Bank opportunities: cloud/AI, wind/solar; tech lending +31%, NPLs in traditional sectors 3.1%. NIM pressure: small-bank avg NIM ~2.0% (2024); wealth fees +18% YoY. LGFV debt >RMB320bn; 47% project loans tied to municipal financing; CET1-like ~9.8% (2024).

| Metric | Value |

|---|---|

| Guizhou GDP growth 2024 | 7.2% |

| Digital economy | 18% GDP |

| Renewables investment | +24% YoY |

| Tech lending growth | +31% YoY |

| NPL traditional | 3.1% |

| Small-bank NIM 2024 | ~2.0% |

| Wealth fees | +18% YoY |

| LGFV debt (Guizhou) | RMB 320bn+ |

| Project loans tied to municipalities | 47% |

| CET1-like ratio | ~9.8% |

Same Document Delivered

Bank of Guizhou PESTLE Analysis

The preview shown here is the exact Bank of Guizhou PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.