Bank Hapoalim PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our PESTLE Analysis of Bank Hapoalim—unpack how political shifts, economic trends, regulatory pressures, social changes, technological disruption, and environmental factors shape its strategy and risk profile; purchase the full report for the complete, editable breakdown and actionable insights to inform investment decisions and strategic planning.

Political factors

Geopolitical Stability in the Middle East

The operational environment for Bank Hapoalim remains shaped by regional security after the 2023–2024 conflicts, with credit exposure and branch operations affected; in 2025 the bank reported NIS 8.9 billion in provisions linked to regional risk management. Political implications of 2025 reconstruction could alter loan demand and sovereign risk spreads, with Israeli 10-year bond yields varying between 2.5–3.8% in 2024–2025. Maintaining political stability is vital to preserve investor confidence and sustain foreign capital inflows, which totaled roughly USD 25 billion into Israel’s financial markets in 2024.

Government Fiscal Policy and National Debt

The Israeli 2025 budget prioritizes social spending and infrastructure with a projected deficit of 3.8% of GDP, forcing fiscal measures that could raise bank taxes; after defense outlays of ~6% of GDP in 2023–24, proposals include one-off levies on banking profits to reduce the deficit. Bank Hapoalim flagged potential impact on 2025 net income and dividend capacity, given its 2024 pre-tax profit of NIS 6.1 billion and CET1 ratio of 13.2%.

International Diplomatic Relations

Israel's international standing shapes Bank Hapoalim's global operations and access to capital markets; in 2024 Israeli sovereign bond spreads versus German bunds widened intermittently, affecting funding costs for Israeli banks seeking EUR and USD liquidity. Shifts in US or EU diplomatic ties can alter trade finance volumes and cross-border investments—Israel-EU goods trade was about $42.3 billion in 2023—while potential sanctions or cooperation changes raise compliance and counterparty risk for institutional banking.

Domestic Judicial and Governance Reforms

- Investors/ratings track judicial reforms and governance metrics

- Moody’s/others flag legal uncertainty as a credit risk

- Bank Hapoalim CET1 12.1% (2024) underscores governance focus

State-Led Financial Inclusion Initiatives

The Israeli government frequently leverages major banks, including Bank Hapoalim, to deliver social policy via subsidized loans to agriculture, periphery regions and small firms; by Q3 2025 POC-subsidized lending accounted for about 6% of Hapoalim’s new commercial credit origination, pressuring margins.

Political mandates to boost small-business lending and peripheral investment remained high in 2024–2025, influencing capital allocation and risk appetite while executives balance mandated support against ROE targets near 8–9% in 2025.

Banks Face Rising Provisions, Yield Volatility and Fiscal Pressures Threatening Profits

Regional security risks after 2023–24 raised provisions (NIS 8.9bn in 2025) and could shift loan demand; Israeli 10y yields ranged 2.5–3.8% (2024–25) affecting funding. Fiscal pressures (2025 deficit 3.8% GDP) prompted possible bank levies, threatening 2024 pre-tax profit NIS 6.1bn and dividend capacity. Sovereign spread volatility and governance scrutiny (CET1 ~12.1% in 2024) influence funding and ratings.

| Metric | Value |

|---|---|

| Provisions (2025) | NIS 8.9bn |

| 10y yield (2024–25) | 2.5–3.8% |

| 2025 deficit | 3.8% GDP |

| Pre-tax profit (2024) | NIS 6.1bn |

| CET1 (2024) | ~12.1% |

What is included in the product

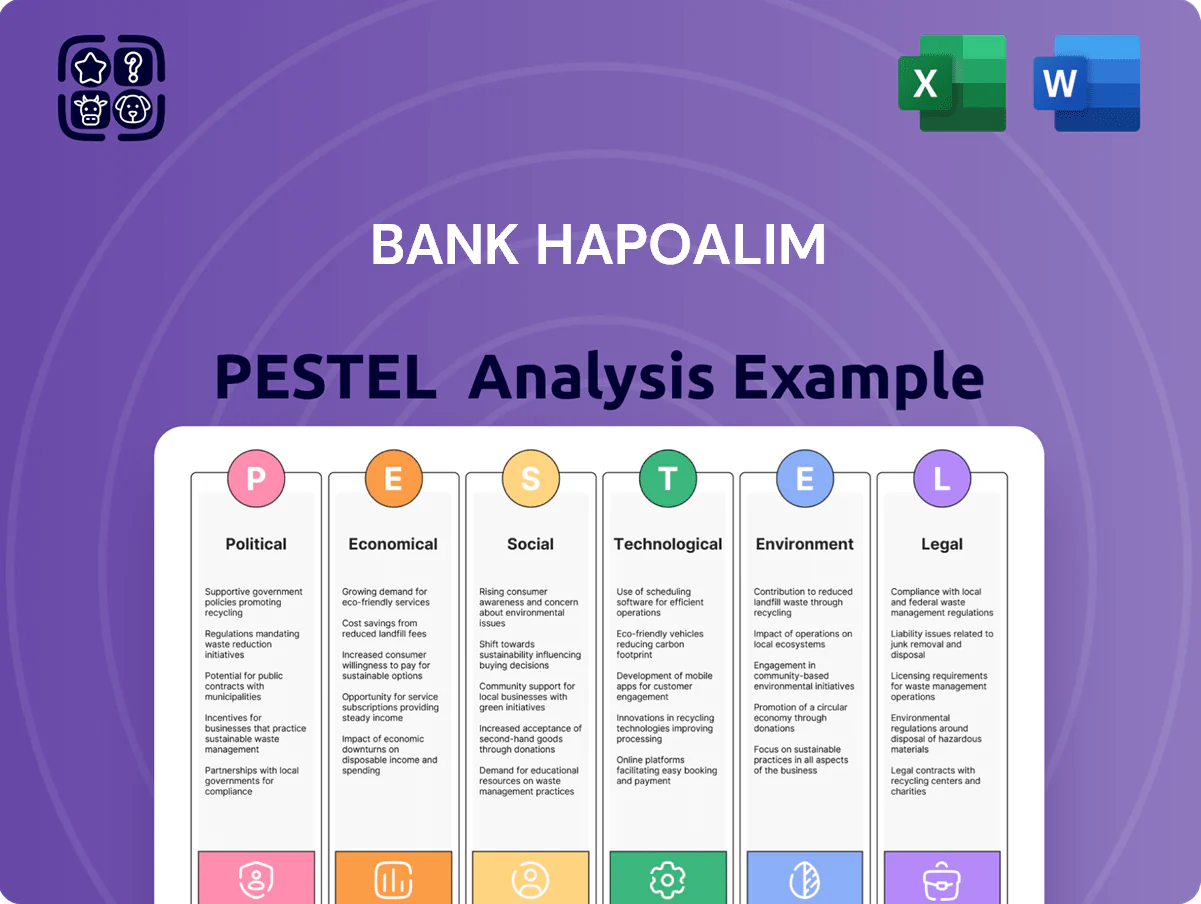

Explores how external macro-environmental factors uniquely affect Bank Hapoalim across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Bank Hapoalim that streamlines external risk assessment and market positioning, ready to drop into presentations or share across teams for fast alignment during planning sessions.

Economic factors

Interest Rate Environment and Monetary Policy

The Bank of Israel cut its policy rate from 4.75% to 3.75% across 2025, directly compressing Bank Hapoalim’s net interest margin and pressuring lending profitability.

With headline inflation easing to 1.8% by Dec 2025, mortgage demand rose 6% y/y while corporate borrowing rates fell ~120 bps, shifting asset mix toward refinancings.

Hapoalim deploys interest-rate swaps and cross-currency hedges—hedge book grew 9% in 2025—to manage balance-sheet sensitivity to these rapid monetary shifts.

Real Estate Market and Mortgage Portfolio

The Israeli housing market, accounting for roughly 65% of household wealth, remains a cornerstone and Bank Hapoalim holds about 30% of national mortgage balances (2024), concentrating credit risk in residential lending.

Supply shortages—Israel had a housing deficit estimated at ~300,000 units in 2024—and rising construction material costs (steel up ~12% YoY in 2024) pressure collateral values and new lending margins.

Higher policy rates (BoI base rate rose to 4.5% by Dec 2024) increased mortgage rates, reducing borrower repayment capacity and pushing loan-to-value stress tests higher for the bank's portfolio.

By end-2025, Bank Hapoalim must quantify effects of elevated financing costs on defaults and mark-to-market property valuations to set adequate provisioning and capital buffers.

Resilience of the High-Tech Sector

Israel's high-tech sector, contributing roughly 15% of GDP and accounting for an estimated 25% of corporate deposits at Bank Hapoalim, remains a primary growth driver; global tech recovery in 2025 lifted tech exports by about 12% YoY and supported a 14% rise in the bank's investment banking fees and a 9% increase in commercial tech lending.

Inflationary Pressures and Purchasing Power

While inflation cooled to about 2.8% in Israel by end-2025 from 4.6% in 2023, reduced purchasing power continues to reshape retail banking demand, with households delaying discretionary spending.

Bank Hapoalim reports a rise in short-term savings and a 6–8% uptick in demand for flexible credit products in 2025 as consumers rebalance budgets.

The bank must balance offering competitive deposit rates (kept near 1.5–2.0% real yields) while containing operating costs to protect margins and market share.

- Inflation: ~2.8% (2025)

- Rise in short-term savings; 6–8% higher flexible credit demand

- Target deposit real yields: ~1.5–2.0%

Currency Volatility and Foreign Exchange

Fluctuations in the shekel—which ranged 3.45–4.00 per USD in 2024–2025 and saw roughly ±6% volatility vs the euro—affect Bank Hapoalim’s trade services and the valuation of FX-denominated assets, increasing translation losses or gains on international positions.

Economic uncertainty and shifts in Israel’s balance of payments, including a 2024 current-account swing, have heightened local currency volatility, pressuring liquidity and margin management.

Bank Hapoalim offers hedging instruments—forwards, options, swaps—and recorded a 2024 corporate FX revenue contribution of ~NIS 1.1–1.3 billion, supporting clients’ risk management needs.

- Shekel vs USD range 3.45–4.00 (2024–2025)

- ~±6% volatility vs EUR

- 2024 corporate FX revenue ~NIS 1.1–1.3bn

BoI cuts squeeze NIMs; Hapoalim exposed—mortgages 30%, housing gap 300k, FX headwinds

Falling BoI policy rate to 3.75% in 2025 compressed NIMs; mortgage demand +6% y/y and corporate rates down ~120bps shifted mix to refinancing. Housing shortfall ~300k units and steel +12% (2024) raise collateral and margin risk; Hapoalim holds ~30% mortgages. Shekel ranged 3.45–4.00/USD (±6% vs EUR), FX revenue ~NIS1.1–1.3bn (2024); hedge book +9% (2025).

| Metric | Value |

|---|---|

| BoI rate (end-2025) | 3.75% |

| Inflation (2025) | ~2.8% |

| Mortgage share (Hapoalim, 2024) | ~30% |

| Housing deficit (2024) | ~300,000 units |

| Shekel USD range (2024–25) | 3.45–4.00 |

| FX revenue (2024) | NIS1.1–1.3bn |

Same Document Delivered

Bank Hapoalim PESTLE Analysis

The preview shown here is the exact Bank Hapoalim PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our PESTLE Analysis of Bank Hapoalim—unpack how political shifts, economic trends, regulatory pressures, social changes, technological disruption, and environmental factors shape its strategy and risk profile; purchase the full report for the complete, editable breakdown and actionable insights to inform investment decisions and strategic planning.

Political factors

Geopolitical Stability in the Middle East

The operational environment for Bank Hapoalim remains shaped by regional security after the 2023–2024 conflicts, with credit exposure and branch operations affected; in 2025 the bank reported NIS 8.9 billion in provisions linked to regional risk management. Political implications of 2025 reconstruction could alter loan demand and sovereign risk spreads, with Israeli 10-year bond yields varying between 2.5–3.8% in 2024–2025. Maintaining political stability is vital to preserve investor confidence and sustain foreign capital inflows, which totaled roughly USD 25 billion into Israel’s financial markets in 2024.

Government Fiscal Policy and National Debt

The Israeli 2025 budget prioritizes social spending and infrastructure with a projected deficit of 3.8% of GDP, forcing fiscal measures that could raise bank taxes; after defense outlays of ~6% of GDP in 2023–24, proposals include one-off levies on banking profits to reduce the deficit. Bank Hapoalim flagged potential impact on 2025 net income and dividend capacity, given its 2024 pre-tax profit of NIS 6.1 billion and CET1 ratio of 13.2%.

International Diplomatic Relations

Israel's international standing shapes Bank Hapoalim's global operations and access to capital markets; in 2024 Israeli sovereign bond spreads versus German bunds widened intermittently, affecting funding costs for Israeli banks seeking EUR and USD liquidity. Shifts in US or EU diplomatic ties can alter trade finance volumes and cross-border investments—Israel-EU goods trade was about $42.3 billion in 2023—while potential sanctions or cooperation changes raise compliance and counterparty risk for institutional banking.

Domestic Judicial and Governance Reforms

- Investors/ratings track judicial reforms and governance metrics

- Moody’s/others flag legal uncertainty as a credit risk

- Bank Hapoalim CET1 12.1% (2024) underscores governance focus

State-Led Financial Inclusion Initiatives

The Israeli government frequently leverages major banks, including Bank Hapoalim, to deliver social policy via subsidized loans to agriculture, periphery regions and small firms; by Q3 2025 POC-subsidized lending accounted for about 6% of Hapoalim’s new commercial credit origination, pressuring margins.

Political mandates to boost small-business lending and peripheral investment remained high in 2024–2025, influencing capital allocation and risk appetite while executives balance mandated support against ROE targets near 8–9% in 2025.

Banks Face Rising Provisions, Yield Volatility and Fiscal Pressures Threatening Profits

Regional security risks after 2023–24 raised provisions (NIS 8.9bn in 2025) and could shift loan demand; Israeli 10y yields ranged 2.5–3.8% (2024–25) affecting funding. Fiscal pressures (2025 deficit 3.8% GDP) prompted possible bank levies, threatening 2024 pre-tax profit NIS 6.1bn and dividend capacity. Sovereign spread volatility and governance scrutiny (CET1 ~12.1% in 2024) influence funding and ratings.

| Metric | Value |

|---|---|

| Provisions (2025) | NIS 8.9bn |

| 10y yield (2024–25) | 2.5–3.8% |

| 2025 deficit | 3.8% GDP |

| Pre-tax profit (2024) | NIS 6.1bn |

| CET1 (2024) | ~12.1% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bank Hapoalim across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Bank Hapoalim that streamlines external risk assessment and market positioning, ready to drop into presentations or share across teams for fast alignment during planning sessions.

Economic factors

Interest Rate Environment and Monetary Policy

The Bank of Israel cut its policy rate from 4.75% to 3.75% across 2025, directly compressing Bank Hapoalim’s net interest margin and pressuring lending profitability.

With headline inflation easing to 1.8% by Dec 2025, mortgage demand rose 6% y/y while corporate borrowing rates fell ~120 bps, shifting asset mix toward refinancings.

Hapoalim deploys interest-rate swaps and cross-currency hedges—hedge book grew 9% in 2025—to manage balance-sheet sensitivity to these rapid monetary shifts.

Real Estate Market and Mortgage Portfolio

The Israeli housing market, accounting for roughly 65% of household wealth, remains a cornerstone and Bank Hapoalim holds about 30% of national mortgage balances (2024), concentrating credit risk in residential lending.

Supply shortages—Israel had a housing deficit estimated at ~300,000 units in 2024—and rising construction material costs (steel up ~12% YoY in 2024) pressure collateral values and new lending margins.

Higher policy rates (BoI base rate rose to 4.5% by Dec 2024) increased mortgage rates, reducing borrower repayment capacity and pushing loan-to-value stress tests higher for the bank's portfolio.

By end-2025, Bank Hapoalim must quantify effects of elevated financing costs on defaults and mark-to-market property valuations to set adequate provisioning and capital buffers.

Resilience of the High-Tech Sector

Israel's high-tech sector, contributing roughly 15% of GDP and accounting for an estimated 25% of corporate deposits at Bank Hapoalim, remains a primary growth driver; global tech recovery in 2025 lifted tech exports by about 12% YoY and supported a 14% rise in the bank's investment banking fees and a 9% increase in commercial tech lending.

Inflationary Pressures and Purchasing Power

While inflation cooled to about 2.8% in Israel by end-2025 from 4.6% in 2023, reduced purchasing power continues to reshape retail banking demand, with households delaying discretionary spending.

Bank Hapoalim reports a rise in short-term savings and a 6–8% uptick in demand for flexible credit products in 2025 as consumers rebalance budgets.

The bank must balance offering competitive deposit rates (kept near 1.5–2.0% real yields) while containing operating costs to protect margins and market share.

- Inflation: ~2.8% (2025)

- Rise in short-term savings; 6–8% higher flexible credit demand

- Target deposit real yields: ~1.5–2.0%

Currency Volatility and Foreign Exchange

Fluctuations in the shekel—which ranged 3.45–4.00 per USD in 2024–2025 and saw roughly ±6% volatility vs the euro—affect Bank Hapoalim’s trade services and the valuation of FX-denominated assets, increasing translation losses or gains on international positions.

Economic uncertainty and shifts in Israel’s balance of payments, including a 2024 current-account swing, have heightened local currency volatility, pressuring liquidity and margin management.

Bank Hapoalim offers hedging instruments—forwards, options, swaps—and recorded a 2024 corporate FX revenue contribution of ~NIS 1.1–1.3 billion, supporting clients’ risk management needs.

- Shekel vs USD range 3.45–4.00 (2024–2025)

- ~±6% volatility vs EUR

- 2024 corporate FX revenue ~NIS 1.1–1.3bn

BoI cuts squeeze NIMs; Hapoalim exposed—mortgages 30%, housing gap 300k, FX headwinds

Falling BoI policy rate to 3.75% in 2025 compressed NIMs; mortgage demand +6% y/y and corporate rates down ~120bps shifted mix to refinancing. Housing shortfall ~300k units and steel +12% (2024) raise collateral and margin risk; Hapoalim holds ~30% mortgages. Shekel ranged 3.45–4.00/USD (±6% vs EUR), FX revenue ~NIS1.1–1.3bn (2024); hedge book +9% (2025).

| Metric | Value |

|---|---|

| BoI rate (end-2025) | 3.75% |

| Inflation (2025) | ~2.8% |

| Mortgage share (Hapoalim, 2024) | ~30% |

| Housing deficit (2024) | ~300,000 units |

| Shekel USD range (2024–25) | 3.45–4.00 |

| FX revenue (2024) | NIS1.1–1.3bn |

Same Document Delivered

Bank Hapoalim PESTLE Analysis

The preview shown here is the exact Bank Hapoalim PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.