Bankinter Business Model Canvas

Bankinter Business Model Canvas: Digital-first strategy, partners & templates for investors

Unlock Bankinter’s strategic playbook with our concise Business Model Canvas—see how targeted customer segments, digital-first value propositions, and agile partnerships drive revenue and competitive edge; ideal for investors, consultants, and founders seeking actionable insight and ready-to-use Word/Excel templates to benchmark or adapt the model.

Partnerships

Strategic Insurance Alliances

Bankinter partners with major insurers (Mapfre, Allianz, Línea Directa) to sell life, property and P&C products, earning fee income while avoiding underwriting risk; in 2024 insurance commissions contributed ~€145m (≈6% of non-interest income). Integrated into Bankinter's apps and online banking, these alliances lift cross-sell rates—insurance attach rising to ~18% of new retail customers in 2024—improving revenue per client without extra capital strain.

Fintech and Innovation Collaborators

Bankinter partners with fintech startups and incubators—including investments via Bankinter Innovation Foundation—to integrate AI-driven financial planning and automated credit scoring, cutting time-to-market by about 30%; in 2024 Bankinter reported 18% year-on-year growth in digital customers to 1.9 million, reflecting this push. These collaborations keep development lean, outsourcing specialized tech while Bankinter retains product leadership and regulatory oversight.

European Institutional Funding Partners

Collaborations with bodies like the European Investment Bank (EIB) let Bankinter channel targeted credit lines to SMEs, enabling loans at submarket rates—Bankinter drew €450m in EIB-backed facilities in 2024 to support 8,200 SME clients. These partnerships improve liquidity buffers (liquid assets up 6.2% y/y in 2024) and reinforce Bankinter’s role as a leading SME lender across Spain and Portugal.

Global Payment Network Providers

Partnerships with Visa and Mastercard power Bankinter’s card issuance and acceptance globally, supporting ~€9.6bn in annual card transaction volume in 2024 and embedding EMV, tokenization, and 3DS security.

Network data improves fraud models and spending analytics, reducing card-fraud losses by an estimated 18% year-on-year and enabling targeted loyalty offers that lift card spend ~6%.

- Enables global acceptance and co-branded cards

- Provides security: EMV, tokenization, 3DS

- Feeds data for fraud reduction (~18% YoY)

- Supports loyalty programs boosting spend (~6%)

- Drives €9.6bn card transaction volume (2024)

External Agent and Broker Networks

Bankinter uses independent financial advisors and real estate brokers to source HNW clients and mortgage seekers, driving 18% of new retail mortgage originations and 22% of private banking inflows in 2024 across Spain, Portugal, and Ireland.

This variable-cost channel lets Bankinter scale acquisition efficiently—partner commissions rose 12% YoY while cost-per-acquisition fell 9% in 2024.

- 18% of 2024 retail mortgages

- 22% of 2024 private banking inflows

- Partner commissions +12% YoY (2024)

- CPA -9% YoY (2024)

Bankinter partners fuel fees, digital growth & €9.6bn card volumes

Bankinter’s key partners (insurers, fintechs, EIB, Visa/Mastercard, advisors) drive fee income, tech scale, SME lending and card volumes—insurance commissions ~€145m (2024), digital customers 1.9m (+18% YoY), EIB facilities €450m, card volume €9.6bn, mortgage originations via partners 18% (2024).

| Metric | 2024 |

|---|---|

| Insurance commissions | €145m |

| Digital customers | 1.9m |

| EIB facilities | €450m |

| Card volume | €9.6bn |

| Partner mortgage share | 18% |

What is included in the product

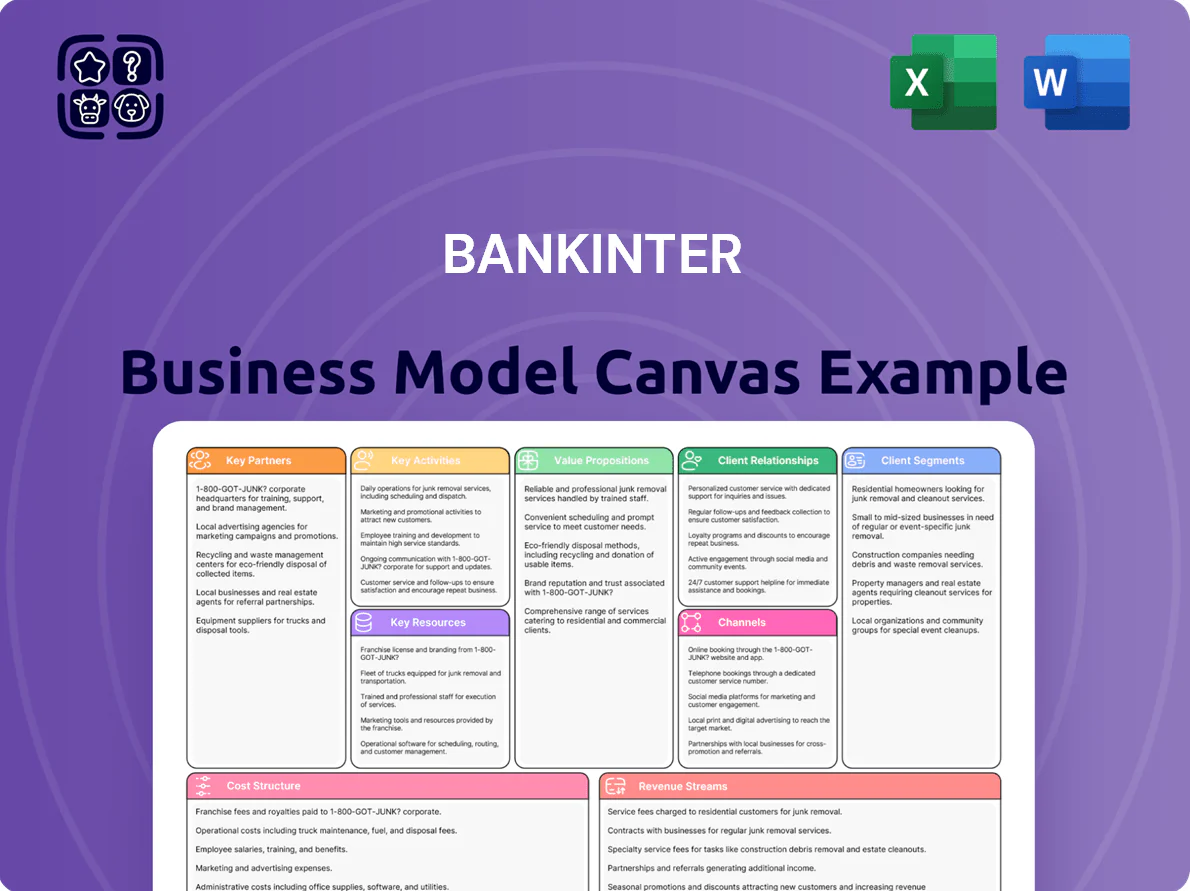

A concise, pre-written Business Model Canvas for Bankinter that maps nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with the bank’s retail, digital and corporate strategy.

High-level view of Bankinter’s business model with editable cells, saving hours of formatting while delivering a clean, shareable snapshot for boardrooms, teams, or quick competitive comparisons.

Activities

Digital Platform Maintenance and Evolution

Bankinter continuously improves its mobile and web banking to boost engagement, rolling out 120+ feature releases in 2024 and driving a 28% year-on-year rise in active digital users to 1.9 million as of Dec 2024.

The bank prioritizes cybersecurity and 99.98% system uptime, plus regular updates that simplify complex transactions and use analytics to deliver personalized offers—over 3.2 million tailored recommendations sent in 2024.

Credit Risk Assessment and Management

Bankinter runs credit risk assessment and management using advanced models and strict credit reviews; as of FY2024 its NPL ratio stood at 0.7% (Dec 2024), supporting balance-sheet stability. The bank pairs targeted lending to fintech, SMEs, and mortgages with conservative buffers—CET1 ratio 13.2% (Dec 2024)—to optimize capital allocation and sustain risk-adjusted growth.

Wealth Management and Advisory Services

Providing tailored financial advice to private and personal banking clients is a core activity, with Bankinter managing €74bn in customer funds (2024) and offering continuous market monitoring, regular portfolio rebalancing, and bespoke investment strategies to meet diverse goals.

Advisors use advanced tools—risk profiling, scenario stress tests, and transparent performance reporting—serving high-value segments that generated 45% of 2024 fee income, improving retention and measurable portfolio outcomes.

Regulatory Compliance and Reporting

Bankinter dedicates large teams and €120m annual compliance spend (2024) to navigate Eurozone rules, covering AML (anti-money laundering), consumer protection, and CRR/CRD IV capital adequacy to keep its banking licence and market access.

Here’s the quick math: regulatory costs ≈1.8% of 2024 operating expenses; compliance incidents fell 22% year-on-year, supporting investor trust and cross-border business.

- €120m compliance budget (2024)

- AML, consumer protection, capital adequacy

- Compliance costs ≈1.8% operating expenses

- Incidents down 22% YoY

- License and reputation preservation

Targeted Marketing and Customer Acquisition

Bankinter runs data-driven campaigns targeting high-earning professionals and profitable SMEs, emphasizing high-yield payroll accounts (promo rates up to 1.2% in 2025) and fast digital onboarding (avg. account opening 12 minutes in 2024).

Behavioral analytics cut CAC by ~18% year-on-year and shift spend to channels that raise customer lifetime value; Bankinter reported net new deposits of €3.1bn in 2024, driven partly by targeted offers.

- Targets: high earners, SMEs

- Value props: 1.2% payroll yields, 12-min onboarding

- Efficiency: CAC down ~18% YoY

- Impact: €3.1bn net new deposits in 2024

Bankinter 2024: 1.9M digital users, €74bn AUM, 120+ releases, €3.1bn deposits, CET1 13.2%

Bankinter upgrades digital channels (120+ releases in 2024) to reach 1.9M active users, sends 3.2M personalized offers, maintains 99.98% uptime, manages NPL 0.7% and CET1 13.2% (Dec 2024), oversees €74bn assets under management, spent €120m on compliance (≈1.8% opex) and delivered €3.1bn net new deposits in 2024.

| Metric | 2024 |

|---|---|

| Active digital users | 1.9M |

| Feature releases | 120+ |

| Personalized offers | 3.2M |

| Uptime | 99.98% |

| NPL ratio | 0.7% |

| CET1 | 13.2% |

| AUM | €74bn |

| Compliance spend | €120m |

| Net new deposits | €3.1bn |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual Bankinter Business Model Canvas deliverable, not a mockup or marketing sample; it’s a direct snapshot of the file you’ll receive after purchase.

When you complete your order, you’ll instantly download this same professional, fully editable document, formatted and structured exactly as shown for Word and Excel use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bankinter Business Model Canvas: Digital-first strategy, partners & templates for investors

Unlock Bankinter’s strategic playbook with our concise Business Model Canvas—see how targeted customer segments, digital-first value propositions, and agile partnerships drive revenue and competitive edge; ideal for investors, consultants, and founders seeking actionable insight and ready-to-use Word/Excel templates to benchmark or adapt the model.

Partnerships

Strategic Insurance Alliances

Bankinter partners with major insurers (Mapfre, Allianz, Línea Directa) to sell life, property and P&C products, earning fee income while avoiding underwriting risk; in 2024 insurance commissions contributed ~€145m (≈6% of non-interest income). Integrated into Bankinter's apps and online banking, these alliances lift cross-sell rates—insurance attach rising to ~18% of new retail customers in 2024—improving revenue per client without extra capital strain.

Fintech and Innovation Collaborators

Bankinter partners with fintech startups and incubators—including investments via Bankinter Innovation Foundation—to integrate AI-driven financial planning and automated credit scoring, cutting time-to-market by about 30%; in 2024 Bankinter reported 18% year-on-year growth in digital customers to 1.9 million, reflecting this push. These collaborations keep development lean, outsourcing specialized tech while Bankinter retains product leadership and regulatory oversight.

European Institutional Funding Partners

Collaborations with bodies like the European Investment Bank (EIB) let Bankinter channel targeted credit lines to SMEs, enabling loans at submarket rates—Bankinter drew €450m in EIB-backed facilities in 2024 to support 8,200 SME clients. These partnerships improve liquidity buffers (liquid assets up 6.2% y/y in 2024) and reinforce Bankinter’s role as a leading SME lender across Spain and Portugal.

Global Payment Network Providers

Partnerships with Visa and Mastercard power Bankinter’s card issuance and acceptance globally, supporting ~€9.6bn in annual card transaction volume in 2024 and embedding EMV, tokenization, and 3DS security.

Network data improves fraud models and spending analytics, reducing card-fraud losses by an estimated 18% year-on-year and enabling targeted loyalty offers that lift card spend ~6%.

- Enables global acceptance and co-branded cards

- Provides security: EMV, tokenization, 3DS

- Feeds data for fraud reduction (~18% YoY)

- Supports loyalty programs boosting spend (~6%)

- Drives €9.6bn card transaction volume (2024)

External Agent and Broker Networks

Bankinter uses independent financial advisors and real estate brokers to source HNW clients and mortgage seekers, driving 18% of new retail mortgage originations and 22% of private banking inflows in 2024 across Spain, Portugal, and Ireland.

This variable-cost channel lets Bankinter scale acquisition efficiently—partner commissions rose 12% YoY while cost-per-acquisition fell 9% in 2024.

- 18% of 2024 retail mortgages

- 22% of 2024 private banking inflows

- Partner commissions +12% YoY (2024)

- CPA -9% YoY (2024)

Bankinter partners fuel fees, digital growth & €9.6bn card volumes

Bankinter’s key partners (insurers, fintechs, EIB, Visa/Mastercard, advisors) drive fee income, tech scale, SME lending and card volumes—insurance commissions ~€145m (2024), digital customers 1.9m (+18% YoY), EIB facilities €450m, card volume €9.6bn, mortgage originations via partners 18% (2024).

| Metric | 2024 |

|---|---|

| Insurance commissions | €145m |

| Digital customers | 1.9m |

| EIB facilities | €450m |

| Card volume | €9.6bn |

| Partner mortgage share | 18% |

What is included in the product

A concise, pre-written Business Model Canvas for Bankinter that maps nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with the bank’s retail, digital and corporate strategy.

High-level view of Bankinter’s business model with editable cells, saving hours of formatting while delivering a clean, shareable snapshot for boardrooms, teams, or quick competitive comparisons.

Activities

Digital Platform Maintenance and Evolution

Bankinter continuously improves its mobile and web banking to boost engagement, rolling out 120+ feature releases in 2024 and driving a 28% year-on-year rise in active digital users to 1.9 million as of Dec 2024.

The bank prioritizes cybersecurity and 99.98% system uptime, plus regular updates that simplify complex transactions and use analytics to deliver personalized offers—over 3.2 million tailored recommendations sent in 2024.

Credit Risk Assessment and Management

Bankinter runs credit risk assessment and management using advanced models and strict credit reviews; as of FY2024 its NPL ratio stood at 0.7% (Dec 2024), supporting balance-sheet stability. The bank pairs targeted lending to fintech, SMEs, and mortgages with conservative buffers—CET1 ratio 13.2% (Dec 2024)—to optimize capital allocation and sustain risk-adjusted growth.

Wealth Management and Advisory Services

Providing tailored financial advice to private and personal banking clients is a core activity, with Bankinter managing €74bn in customer funds (2024) and offering continuous market monitoring, regular portfolio rebalancing, and bespoke investment strategies to meet diverse goals.

Advisors use advanced tools—risk profiling, scenario stress tests, and transparent performance reporting—serving high-value segments that generated 45% of 2024 fee income, improving retention and measurable portfolio outcomes.

Regulatory Compliance and Reporting

Bankinter dedicates large teams and €120m annual compliance spend (2024) to navigate Eurozone rules, covering AML (anti-money laundering), consumer protection, and CRR/CRD IV capital adequacy to keep its banking licence and market access.

Here’s the quick math: regulatory costs ≈1.8% of 2024 operating expenses; compliance incidents fell 22% year-on-year, supporting investor trust and cross-border business.

- €120m compliance budget (2024)

- AML, consumer protection, capital adequacy

- Compliance costs ≈1.8% operating expenses

- Incidents down 22% YoY

- License and reputation preservation

Targeted Marketing and Customer Acquisition

Bankinter runs data-driven campaigns targeting high-earning professionals and profitable SMEs, emphasizing high-yield payroll accounts (promo rates up to 1.2% in 2025) and fast digital onboarding (avg. account opening 12 minutes in 2024).

Behavioral analytics cut CAC by ~18% year-on-year and shift spend to channels that raise customer lifetime value; Bankinter reported net new deposits of €3.1bn in 2024, driven partly by targeted offers.

- Targets: high earners, SMEs

- Value props: 1.2% payroll yields, 12-min onboarding

- Efficiency: CAC down ~18% YoY

- Impact: €3.1bn net new deposits in 2024

Bankinter 2024: 1.9M digital users, €74bn AUM, 120+ releases, €3.1bn deposits, CET1 13.2%

Bankinter upgrades digital channels (120+ releases in 2024) to reach 1.9M active users, sends 3.2M personalized offers, maintains 99.98% uptime, manages NPL 0.7% and CET1 13.2% (Dec 2024), oversees €74bn assets under management, spent €120m on compliance (≈1.8% opex) and delivered €3.1bn net new deposits in 2024.

| Metric | 2024 |

|---|---|

| Active digital users | 1.9M |

| Feature releases | 120+ |

| Personalized offers | 3.2M |

| Uptime | 99.98% |

| NPL ratio | 0.7% |

| CET1 | 13.2% |

| AUM | €74bn |

| Compliance spend | €120m |

| Net new deposits | €3.1bn |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual Bankinter Business Model Canvas deliverable, not a mockup or marketing sample; it’s a direct snapshot of the file you’ll receive after purchase.

When you complete your order, you’ll instantly download this same professional, fully editable document, formatted and structured exactly as shown for Word and Excel use.