Hope Bancorp Business Model Canvas

Hope Bancorp Business Model Canvas: Actionable Blueprint for Investors & Executives

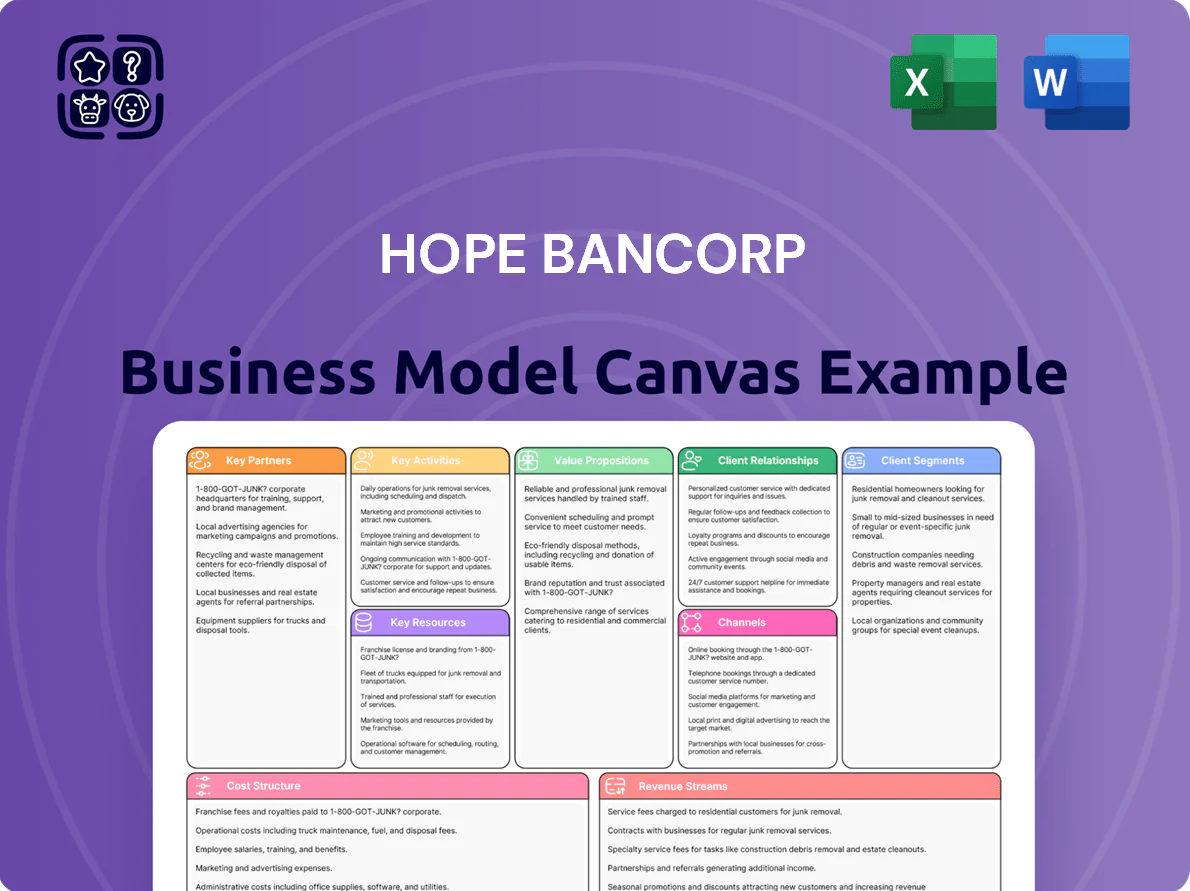

Unlock the full strategic blueprint behind Hope Bancorp’s business model—this in-depth Business Model Canvas maps value propositions, customer segments, key partnerships, and revenue streams to reveal how the bank wins market share and drives growth; ideal for investors, consultants, and executives seeking actionable insights and ready-to-use Word/Excel templates.

Partnerships

Strategic Fintech Collaborators

Hope Bancorp partners with fintechs to modernize digital banking and mobile payments, reducing in-house dev costs while scaling features; in 2024 it cited a 30% faster digital feature rollout and a 22% increase in mobile active users year-over-year.

Government and SBA Alliances

Hope Bancorp partners with the U.S. Small Business Administration to underwrite SBA-guaranteed loans, supporting ~$420m in SBA lending in 2024 and lowering credit risk via partial government guarantees.

These alliances let Hope offer looser collateral and longer terms to Korean-American and other minority entrepreneurs, boosting small-business approvals by ~18% year-over-year in 2024.

Correspondent Banking Networks

Hope Bancorp uses a network of international correspondent banks to handle US–South Korea trade finance and remittances, supporting roughly $4.2 billion in cross-border payments in 2024 and enabling FX execution and liquidity management for corporate clients.

Community and Cultural Organizations

The bank partners with Korean-American non-profits and professional associations to boost market penetration and meet Community Reinvestment Act goals, drawing on 2024 outreach that reached ~18,000 community members and supported $42.6M in CRA-eligible lending.

These ties help spot underserved segments and deliver culturally tailored financial literacy—over 120 workshops in 2024—and community leaders act as primary referrers for new deposits and loans.

- 2024 outreach: ~18,000 people

- CRA-eligible lending: $42.6M (2024)

- Workshops delivered: 120+ (2024)

- Primary referral channel: community leaders

Mortgage Servicing and Insurance Providers

Hope Bancorp partners with mortgage secondary market participants and third-party insurance underwriters to offer mortgages and wealth-protection products while shifting credit and insurance operational risks off balance sheet.

In 2025 the bank securitized roughly $320M in mortgage originations and cross-sold insurance on ~18% of retail deposits, improving fee income and positioning Hope as a one-stop homeownership and protection hub.

- 320M securitized mortgages (2025)

- 18% retail deposits cross-sold insurance

- reduces credit/ops risk via off‑balance arrangements

Hope Bancorp: Partnerships Fuel 30% Faster Digital Rollout, $4.2B Payments & $320M Securitization

Hope Bancorp’s key partnerships drive digital rollout (30% faster) and mobile growth (+22% MAU in 2024), support ~$420M SBA lending, enable ~$4.2B cross‑border payments, and fuel CRA outreach (18k reached; $42.6M CRA loans; 120+ workshops). In 2025 it securitized $320M mortgages and cross‑sold insurance on 18% of retail deposits, shifting credit/ops risk off balance sheet.

| Metric | Value |

|---|---|

| Digital rollout speed | +30% (2024) |

| Mobile MAU | +22% YoY (2024) |

| SBA lending | $420M (2024) |

| Cross‑border payments | $4.2B (2024) |

| CRA outreach | 18k people; $42.6M loans (2024) |

| Workshops | 120+ (2024) |

| Securitized mortgages | $320M (2025) |

| Insurance cross‑sell | 18% of retail deposits (2025) |

What is included in the product

A concise, investor-ready Business Model Canvas for Hope Bancorp detailing customer segments, channels, value propositions, key activities, resources, partnerships, cost structure, and revenue streams aligned with its commercial banking strategy and regional focus for presentations and strategic planning.

High-level, editable Business Model Canvas for Hope Bancorp that condenses strategy into a clean one-page snapshot—ideal for boardrooms, team collaboration, and quick comparison across banks while saving hours of formatting.

Activities

Commercial and Industrial Lending

Hope Bancorp focuses on underwriting and managing a diverse business loan portfolio—commercial real estate, equipment finance, and C&I loans—driving asset growth and net interest income (net interest margin was 3.10% in 2025 Q3). Staff perform rigorous credit analysis and risk assessment; nonperforming assets were 0.42% of loans as of 2025 Q3, supporting long-term loan-book stability.

Deposit Mobilization and Management

Hope Bancorp actively manages non-interest demand deposits and time deposits to keep stable funding, using competitive pricing and targeted marketing to grow core retail and business deposits; as of Q4 2025 it held $28.4 billion in total deposits, with core deposits ~75% of the mix. Efficient deposit mix and pricing protect net interest margin (NIM), which was 2.95% in FY 2025, helping cushion rate volatility.

International Trade Finance Services

The bank facilitates trans-Pacific commerce by issuing letters of credit, import/export loans, and documentary collections; these services supported $3.2bn in international trade flows for Hope Bancorp in FY2024, about 28% of commercial loan activity.

Delivering these requires expertise in Basel III rules, UCP 600 standards (uniform customs and practice for documentary credits), and OFAC/AML compliance, driving specialized staffing and compliance costs of roughly $12–15m annually.

Digital Transformation and Cybersecurity

Hope Bancorp invests in its digital platform to boost online and mobile banking, supporting a 21% YoY rise in digital logins and 35% of deposit growth in 2024.

It enforces multilayer cybersecurity—PCI-DSS, MFA, real-time fraud monitoring—cutting fraud losses 18% in 2024 and improving uptime to 99.95% for operational resilience.

- 21% YoY digital logins (2024)

- 35% of deposit growth via digital channels (2024)

- 18% reduction in fraud losses (2024)

- 99.95% system uptime (2024)

Regulatory Compliance and Risk Management

A large share of Hope Bancorp’s resources go to regulatory compliance—covering AML (anti-money laundering), BSA (Bank Secrecy Act), and state banking rules—with compliance headcount and tech spend forming about 5–7% of operating expenses in 2024.

The bank runs quarterly internal audits and annual CCAR-style stress tests; 2024 stress scenarios showed CET1 buffer remained >250 bps above regulatory minima, reducing legal and reputational risk.

- 5–7% of 2024 Opex spent on compliance

- Quarterly internal audits; annual stress tests

- CET1 buffer >250 basis points in 2024

- Focus: AML, BSA, state banking rules

Strong CRE/C&I loan growth, solid NIM 3.10% and deposits $28.4B with >250bps CET1

Underwrite/manage diverse commercial loan book (CRE, equipment, C&I) driving NII; NIM 3.10% (2025 Q3), NPA 0.42% (2025 Q3). Grow stable core deposits ($28.4B total deposits, ~75% core in Q4 2025) and digital channels (21% YoY logins, 35% deposit growth 2024). Compliance, cyber, and trade services cost ~ $12–15M + 5–7% Opex; CET1 buffer >250bps (2024).

| Metric | Value |

|---|---|

| NIM (2025 Q3) | 3.10% |

| NPA (2025 Q3) | 0.42% |

| Total deposits (Q4 2025) | $28.4B |

| Core mix | ~75% |

| Digital logins YoY (2024) | 21% |

| Deposit growth via digital (2024) | 35% |

| Compliance/cyber spend | $12–15M + 5–7% Opex |

| CET1 buffer (2024) | >250 bps |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Hope Bancorp Business Model Canvas you will receive after purchase—not a mockup or sample—and includes the same structured, editable content and layout shown here.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Hope Bancorp Business Model Canvas: Actionable Blueprint for Investors & Executives

Unlock the full strategic blueprint behind Hope Bancorp’s business model—this in-depth Business Model Canvas maps value propositions, customer segments, key partnerships, and revenue streams to reveal how the bank wins market share and drives growth; ideal for investors, consultants, and executives seeking actionable insights and ready-to-use Word/Excel templates.

Partnerships

Strategic Fintech Collaborators

Hope Bancorp partners with fintechs to modernize digital banking and mobile payments, reducing in-house dev costs while scaling features; in 2024 it cited a 30% faster digital feature rollout and a 22% increase in mobile active users year-over-year.

Government and SBA Alliances

Hope Bancorp partners with the U.S. Small Business Administration to underwrite SBA-guaranteed loans, supporting ~$420m in SBA lending in 2024 and lowering credit risk via partial government guarantees.

These alliances let Hope offer looser collateral and longer terms to Korean-American and other minority entrepreneurs, boosting small-business approvals by ~18% year-over-year in 2024.

Correspondent Banking Networks

Hope Bancorp uses a network of international correspondent banks to handle US–South Korea trade finance and remittances, supporting roughly $4.2 billion in cross-border payments in 2024 and enabling FX execution and liquidity management for corporate clients.

Community and Cultural Organizations

The bank partners with Korean-American non-profits and professional associations to boost market penetration and meet Community Reinvestment Act goals, drawing on 2024 outreach that reached ~18,000 community members and supported $42.6M in CRA-eligible lending.

These ties help spot underserved segments and deliver culturally tailored financial literacy—over 120 workshops in 2024—and community leaders act as primary referrers for new deposits and loans.

- 2024 outreach: ~18,000 people

- CRA-eligible lending: $42.6M (2024)

- Workshops delivered: 120+ (2024)

- Primary referral channel: community leaders

Mortgage Servicing and Insurance Providers

Hope Bancorp partners with mortgage secondary market participants and third-party insurance underwriters to offer mortgages and wealth-protection products while shifting credit and insurance operational risks off balance sheet.

In 2025 the bank securitized roughly $320M in mortgage originations and cross-sold insurance on ~18% of retail deposits, improving fee income and positioning Hope as a one-stop homeownership and protection hub.

- 320M securitized mortgages (2025)

- 18% retail deposits cross-sold insurance

- reduces credit/ops risk via off‑balance arrangements

Hope Bancorp: Partnerships Fuel 30% Faster Digital Rollout, $4.2B Payments & $320M Securitization

Hope Bancorp’s key partnerships drive digital rollout (30% faster) and mobile growth (+22% MAU in 2024), support ~$420M SBA lending, enable ~$4.2B cross‑border payments, and fuel CRA outreach (18k reached; $42.6M CRA loans; 120+ workshops). In 2025 it securitized $320M mortgages and cross‑sold insurance on 18% of retail deposits, shifting credit/ops risk off balance sheet.

| Metric | Value |

|---|---|

| Digital rollout speed | +30% (2024) |

| Mobile MAU | +22% YoY (2024) |

| SBA lending | $420M (2024) |

| Cross‑border payments | $4.2B (2024) |

| CRA outreach | 18k people; $42.6M loans (2024) |

| Workshops | 120+ (2024) |

| Securitized mortgages | $320M (2025) |

| Insurance cross‑sell | 18% of retail deposits (2025) |

What is included in the product

A concise, investor-ready Business Model Canvas for Hope Bancorp detailing customer segments, channels, value propositions, key activities, resources, partnerships, cost structure, and revenue streams aligned with its commercial banking strategy and regional focus for presentations and strategic planning.

High-level, editable Business Model Canvas for Hope Bancorp that condenses strategy into a clean one-page snapshot—ideal for boardrooms, team collaboration, and quick comparison across banks while saving hours of formatting.

Activities

Commercial and Industrial Lending

Hope Bancorp focuses on underwriting and managing a diverse business loan portfolio—commercial real estate, equipment finance, and C&I loans—driving asset growth and net interest income (net interest margin was 3.10% in 2025 Q3). Staff perform rigorous credit analysis and risk assessment; nonperforming assets were 0.42% of loans as of 2025 Q3, supporting long-term loan-book stability.

Deposit Mobilization and Management

Hope Bancorp actively manages non-interest demand deposits and time deposits to keep stable funding, using competitive pricing and targeted marketing to grow core retail and business deposits; as of Q4 2025 it held $28.4 billion in total deposits, with core deposits ~75% of the mix. Efficient deposit mix and pricing protect net interest margin (NIM), which was 2.95% in FY 2025, helping cushion rate volatility.

International Trade Finance Services

The bank facilitates trans-Pacific commerce by issuing letters of credit, import/export loans, and documentary collections; these services supported $3.2bn in international trade flows for Hope Bancorp in FY2024, about 28% of commercial loan activity.

Delivering these requires expertise in Basel III rules, UCP 600 standards (uniform customs and practice for documentary credits), and OFAC/AML compliance, driving specialized staffing and compliance costs of roughly $12–15m annually.

Digital Transformation and Cybersecurity

Hope Bancorp invests in its digital platform to boost online and mobile banking, supporting a 21% YoY rise in digital logins and 35% of deposit growth in 2024.

It enforces multilayer cybersecurity—PCI-DSS, MFA, real-time fraud monitoring—cutting fraud losses 18% in 2024 and improving uptime to 99.95% for operational resilience.

- 21% YoY digital logins (2024)

- 35% of deposit growth via digital channels (2024)

- 18% reduction in fraud losses (2024)

- 99.95% system uptime (2024)

Regulatory Compliance and Risk Management

A large share of Hope Bancorp’s resources go to regulatory compliance—covering AML (anti-money laundering), BSA (Bank Secrecy Act), and state banking rules—with compliance headcount and tech spend forming about 5–7% of operating expenses in 2024.

The bank runs quarterly internal audits and annual CCAR-style stress tests; 2024 stress scenarios showed CET1 buffer remained >250 bps above regulatory minima, reducing legal and reputational risk.

- 5–7% of 2024 Opex spent on compliance

- Quarterly internal audits; annual stress tests

- CET1 buffer >250 basis points in 2024

- Focus: AML, BSA, state banking rules

Strong CRE/C&I loan growth, solid NIM 3.10% and deposits $28.4B with >250bps CET1

Underwrite/manage diverse commercial loan book (CRE, equipment, C&I) driving NII; NIM 3.10% (2025 Q3), NPA 0.42% (2025 Q3). Grow stable core deposits ($28.4B total deposits, ~75% core in Q4 2025) and digital channels (21% YoY logins, 35% deposit growth 2024). Compliance, cyber, and trade services cost ~ $12–15M + 5–7% Opex; CET1 buffer >250bps (2024).

| Metric | Value |

|---|---|

| NIM (2025 Q3) | 3.10% |

| NPA (2025 Q3) | 0.42% |

| Total deposits (Q4 2025) | $28.4B |

| Core mix | ~75% |

| Digital logins YoY (2024) | 21% |

| Deposit growth via digital (2024) | 35% |

| Compliance/cyber spend | $12–15M + 5–7% Opex |

| CET1 buffer (2024) | >250 bps |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Hope Bancorp Business Model Canvas you will receive after purchase—not a mockup or sample—and includes the same structured, editable content and layout shown here.