Hope Bancorp Porter's Five Forces Analysis

Don't Miss the Bigger Picture

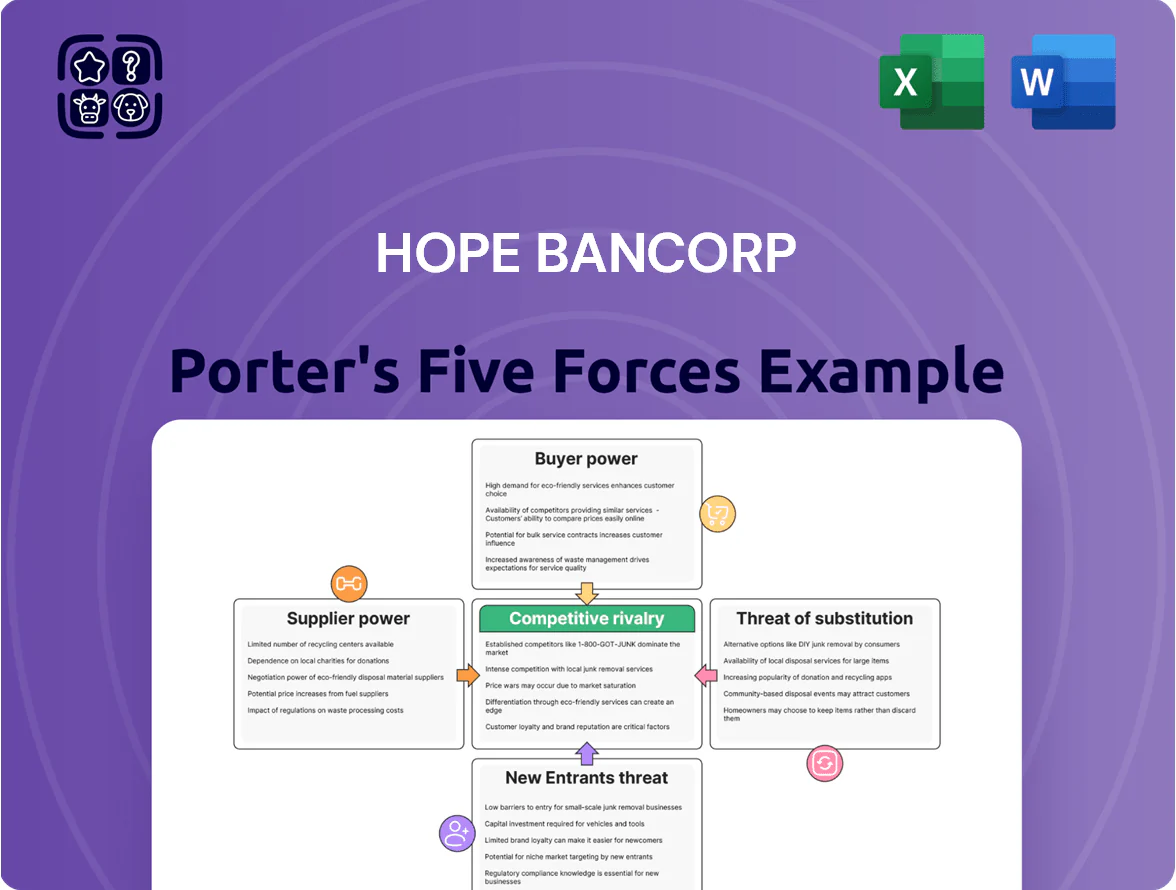

Hope Bancorp faces moderate competitive intensity driven by regional rivals, regulatory constraints, and concentrated commercial clients, while digital disruptors and margin pressure from larger banks pose notable threats to growth and profitability.

Suppliers Bargaining Power

Cost of Deposits and Interest Rate Sensitivity

Availability of Specialized Human Capital

The supply of bilingual Korean-English commercial bankers and compliance officers is tight: USC estimated in 2024 that LA County needs 12% more bilingual financial professionals, and New York shows similar shortfalls, boosting employee leverage.

High demand for experienced commercial lenders and compliance officers raises wage pressure; industry median commercial banker pay rose 8% to $145,000 in 2024, increasing bargaining power.

Hope Bancorp must match regional and national offers—total comp, signing bonuses, and retention grants—to retain staff and avoid costly turnover.

Dependence on Core Banking Technology Providers

Technology vendors supplying core banking platforms and cybersecurity tools command strong leverage over Hope Bancorp as it modernizes for 2026; global core banking market consolidation left top 5 vendors with ~60% share in 2024, concentrating choice and pricing power.

Switching core systems often exceeds $50–150 million and 18–36 months for regional banks, so Hope’s reliance on a few specialist firms creates high switching costs and supplier pricing power.

Access to Wholesale Funding Markets

Institutional liquidity providers like the Federal Home Loan Bank and secondary credit markets act as key secondary suppliers; in 2025 HCB reported borrowing capacity with FHLB lines exceeding $3.2bn, which buffers deposits but raises dependence on wholesale markets.

Hope Bancorp’s CET1 ratio of ~11.8% and LCR near 110% in 2025 leave room, but any credit-tightening that lifts wholesale spreads directly raises funding costs and compresses net interest margin.

The expense of wholesale funding constrains the pace of large commercial loan growth—each 25bp rise in wholesale spread can cut NIM by ~3–5bps, lowering EPS and ROA on growth initiatives.

- FHLB capacity > $3.2bn (2025)

- CET1 ~11.8%, LCR ~110% (2025)

- 25bp wholesale spread → NIM −3–5bps

Regulatory and Legal Service Requirements

Legal firms and regulatory consultants are essential for Hope Bancorp in 2025, as AML (anti-money laundering) fines across US regional banks rose 28% in 2024 and regulators pushed higher liquidity and capital buffers after 2023 stress, making these services nonnegotiable.

High demand lets providers charge premium fees—industry surveys show compliance advisory fees up 22% y/y in 2024—and they set strict contracts, raising supplier bargaining power and increasing Hope Bancorp’s operational costs.

- AML fines +28% in 2024

- Compliance fees +22% y/y (2024)

- Providers set strict contract terms

- Higher costs squeeze regional bank margins

High bargaining power squeezes Hope Bancorp: NIM ~2.6%, tougher loan/profit tradeoffs

| Metric | Value (2025) |

|---|---|

| NIM | ≈2.6% |

| CET1 | ≈11.8% |

| FHLB capacity | >$3.2bn |

| 25bp → NIM | −3–5bps |

What is included in the product

Tailored Porter's Five Forces analysis for Hope Bancorp that uncovers competitive drivers, customer and supplier bargaining power, entry barriers, substitute threats, and strategic vulnerabilities shaping its regional banking position.

Hope Bancorp Porter's Five Forces—condensed, one-sheet analysis that clarifies competitive pressures for faster strategic decisions and investor presentations.

Customers Bargaining Power

Price Sensitivity of Commercial Borrowers

Small and medium-sized business (SMB) clients, Hope Bancorp’s core, show high price sensitivity to loan rates; 2024 S&P Global data found 62% of SMBs shopped lenders for better rates before borrowing.

SMBs routinely compare offers across ethnic and mainstream banks to cut debt service, raising effective bargaining power and pressuring net interest margins.

Low Switching Costs for Individual Depositors

Retail depositors face low switching costs as 85% of US bank customers use mobile banking and 56% cite ease of transfers as the main reason they switched in 2024, so Hope Bancorp risks rapid outflows if rates or convenience lag peers.

Demand for Specialized Multi-Ethnic Services

Customers in the Korean-American market expect high-touch, culturally nuanced services—language, business networks, and cross-border remittance—giving them strong bargaining power; Hope Bancorp reported 2024 Korean-client deposits of $6.2 billion, so losing culturally specific offerings risks material outflows.

That demand lets customers insist on tailored loans and international trade finance; industry data shows 28% of Asian-American SMEs in 2023 used ethnic banks for cross-border services, so failure to meet expectations drives switches to competitors.

Information Transparency and Digital Comparison

By end-2025, financial aggregators let customers compare rates in real time, cutting information asymmetry and shifting bargaining power toward depositors and borrowers.

Hope Bancorp faces customers who cite market averages—national retail deposit rate 0.45% and average small-business loan spread 2.1% in 2025—to negotiate better yields and lower margins.

- Real-time rate visibility

- National deposit avg 0.45% (2025)

- SMB loan spread avg 2.1% (2025)

Availability of Alternative Financing Sources

The rise of non-bank lenders and fintechs—US private credit AUM reached about $1.5 trillion in 2024—gives Hope Bancorp commercial customers clear alternatives to traditional loans.

If Hope’s credit standards stay tight or approval times exceed industry norms (bank median commercial loan approval ~10–15 days), firms often choose private credit or fintechs for speed and tailored covenants.

That expanded capital choice erodes Hope’s pricing power and cross-sell leverage with mid-market borrowers.

- Private credit AUM ~1.5T (2024)

- Bank loan approval median ~10–15 days

- Fintechs offer faster, more flexible terms

Competitive pressure squeezes Hope Bancorp: savvy SMBs, mobile switching, tight spreads

Customers hold strong bargaining power: SMBs price-shop (62% in 2024), retail depositors switch easily (85% use mobile banking; 56% cite transfers, 2024), Korean-client deposits $6.2B (2024) raise demands for tailored cross-border services, and private credit AUM ~$1.5T (2024) plus real-time rate visibility (2025 national deposit avg 0.45%; SMB loan spread 2.1%) compress Hope Bancorp margins.

| Metric | Value |

|---|---|

| SMBs who shopped lenders (2024) | 62% |

| Mobile banking users (US, 2024) | 85% |

| Korean-client deposits (Hope, 2024) | $6.2B |

| Private credit AUM (2024) | $1.5T |

| Natl deposit avg (2025) | 0.45% |

| SMB loan spread avg (2025) | 2.1% |

What You See Is What You Get

Hope Bancorp Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Hope Bancorp you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Hope Bancorp faces moderate competitive intensity driven by regional rivals, regulatory constraints, and concentrated commercial clients, while digital disruptors and margin pressure from larger banks pose notable threats to growth and profitability.

Suppliers Bargaining Power

Cost of Deposits and Interest Rate Sensitivity

Availability of Specialized Human Capital

The supply of bilingual Korean-English commercial bankers and compliance officers is tight: USC estimated in 2024 that LA County needs 12% more bilingual financial professionals, and New York shows similar shortfalls, boosting employee leverage.

High demand for experienced commercial lenders and compliance officers raises wage pressure; industry median commercial banker pay rose 8% to $145,000 in 2024, increasing bargaining power.

Hope Bancorp must match regional and national offers—total comp, signing bonuses, and retention grants—to retain staff and avoid costly turnover.

Dependence on Core Banking Technology Providers

Technology vendors supplying core banking platforms and cybersecurity tools command strong leverage over Hope Bancorp as it modernizes for 2026; global core banking market consolidation left top 5 vendors with ~60% share in 2024, concentrating choice and pricing power.

Switching core systems often exceeds $50–150 million and 18–36 months for regional banks, so Hope’s reliance on a few specialist firms creates high switching costs and supplier pricing power.

Access to Wholesale Funding Markets

Institutional liquidity providers like the Federal Home Loan Bank and secondary credit markets act as key secondary suppliers; in 2025 HCB reported borrowing capacity with FHLB lines exceeding $3.2bn, which buffers deposits but raises dependence on wholesale markets.

Hope Bancorp’s CET1 ratio of ~11.8% and LCR near 110% in 2025 leave room, but any credit-tightening that lifts wholesale spreads directly raises funding costs and compresses net interest margin.

The expense of wholesale funding constrains the pace of large commercial loan growth—each 25bp rise in wholesale spread can cut NIM by ~3–5bps, lowering EPS and ROA on growth initiatives.

- FHLB capacity > $3.2bn (2025)

- CET1 ~11.8%, LCR ~110% (2025)

- 25bp wholesale spread → NIM −3–5bps

Regulatory and Legal Service Requirements

Legal firms and regulatory consultants are essential for Hope Bancorp in 2025, as AML (anti-money laundering) fines across US regional banks rose 28% in 2024 and regulators pushed higher liquidity and capital buffers after 2023 stress, making these services nonnegotiable.

High demand lets providers charge premium fees—industry surveys show compliance advisory fees up 22% y/y in 2024—and they set strict contracts, raising supplier bargaining power and increasing Hope Bancorp’s operational costs.

- AML fines +28% in 2024

- Compliance fees +22% y/y (2024)

- Providers set strict contract terms

- Higher costs squeeze regional bank margins

High bargaining power squeezes Hope Bancorp: NIM ~2.6%, tougher loan/profit tradeoffs

| Metric | Value (2025) |

|---|---|

| NIM | ≈2.6% |

| CET1 | ≈11.8% |

| FHLB capacity | >$3.2bn |

| 25bp → NIM | −3–5bps |

What is included in the product

Tailored Porter's Five Forces analysis for Hope Bancorp that uncovers competitive drivers, customer and supplier bargaining power, entry barriers, substitute threats, and strategic vulnerabilities shaping its regional banking position.

Hope Bancorp Porter's Five Forces—condensed, one-sheet analysis that clarifies competitive pressures for faster strategic decisions and investor presentations.

Customers Bargaining Power

Price Sensitivity of Commercial Borrowers

Small and medium-sized business (SMB) clients, Hope Bancorp’s core, show high price sensitivity to loan rates; 2024 S&P Global data found 62% of SMBs shopped lenders for better rates before borrowing.

SMBs routinely compare offers across ethnic and mainstream banks to cut debt service, raising effective bargaining power and pressuring net interest margins.

Low Switching Costs for Individual Depositors

Retail depositors face low switching costs as 85% of US bank customers use mobile banking and 56% cite ease of transfers as the main reason they switched in 2024, so Hope Bancorp risks rapid outflows if rates or convenience lag peers.

Demand for Specialized Multi-Ethnic Services

Customers in the Korean-American market expect high-touch, culturally nuanced services—language, business networks, and cross-border remittance—giving them strong bargaining power; Hope Bancorp reported 2024 Korean-client deposits of $6.2 billion, so losing culturally specific offerings risks material outflows.

That demand lets customers insist on tailored loans and international trade finance; industry data shows 28% of Asian-American SMEs in 2023 used ethnic banks for cross-border services, so failure to meet expectations drives switches to competitors.

Information Transparency and Digital Comparison

By end-2025, financial aggregators let customers compare rates in real time, cutting information asymmetry and shifting bargaining power toward depositors and borrowers.

Hope Bancorp faces customers who cite market averages—national retail deposit rate 0.45% and average small-business loan spread 2.1% in 2025—to negotiate better yields and lower margins.

- Real-time rate visibility

- National deposit avg 0.45% (2025)

- SMB loan spread avg 2.1% (2025)

Availability of Alternative Financing Sources

The rise of non-bank lenders and fintechs—US private credit AUM reached about $1.5 trillion in 2024—gives Hope Bancorp commercial customers clear alternatives to traditional loans.

If Hope’s credit standards stay tight or approval times exceed industry norms (bank median commercial loan approval ~10–15 days), firms often choose private credit or fintechs for speed and tailored covenants.

That expanded capital choice erodes Hope’s pricing power and cross-sell leverage with mid-market borrowers.

- Private credit AUM ~1.5T (2024)

- Bank loan approval median ~10–15 days

- Fintechs offer faster, more flexible terms

Competitive pressure squeezes Hope Bancorp: savvy SMBs, mobile switching, tight spreads

Customers hold strong bargaining power: SMBs price-shop (62% in 2024), retail depositors switch easily (85% use mobile banking; 56% cite transfers, 2024), Korean-client deposits $6.2B (2024) raise demands for tailored cross-border services, and private credit AUM ~$1.5T (2024) plus real-time rate visibility (2025 national deposit avg 0.45%; SMB loan spread 2.1%) compress Hope Bancorp margins.

| Metric | Value |

|---|---|

| SMBs who shopped lenders (2024) | 62% |

| Mobile banking users (US, 2024) | 85% |

| Korean-client deposits (Hope, 2024) | $6.2B |

| Private credit AUM (2024) | $1.5T |

| Natl deposit avg (2025) | 0.45% |

| SMB loan spread avg (2025) | 2.1% |

What You See Is What You Get

Hope Bancorp Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Hope Bancorp you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.