Bank Of Ireland Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

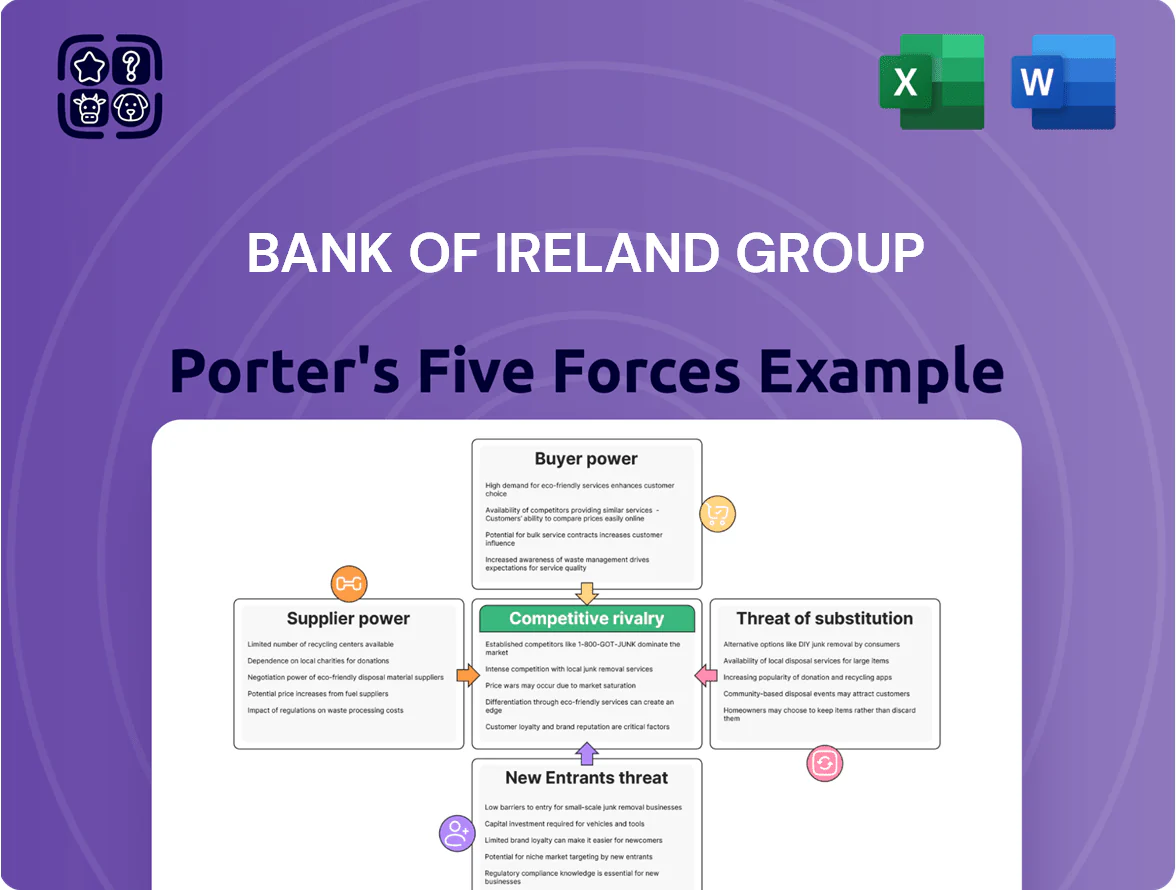

Bank of Ireland faces moderate competitive rivalry, regulatory pressure, and digital disruption that collectively shape its profitability and strategic choices.

Buyer bargaining remains significant as retail and corporate clients demand better rates and digital services, while substitute fintechs and challenger banks elevate the threat level.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank Of Ireland Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Technology and Cloud Infrastructure Providers

Competition for Specialized Financial and Tech Talent

The tight supply of cybersecurity, data science and compliance talent in Ireland and the UK—vacancy rates for tech roles hit ~3.8% in 2024 in Ireland—gives specialists strong bargaining power; Bank of Ireland’s digital push competes directly with Big Tech and fintechs, raising median tech salaries by ~12–18% in 2023–25 and forcing higher personnel costs plus retention programs (sign-on bonuses, equity-like awards, training pathways) to hold critical staff.

Influence of Central Banks and Regulatory Authorities

Regulatory bodies act as non-traditional suppliers by supplying the legal framework and ECB liquidity lines; by Q4 2025 ECB-driven CET1 and MREL guidance lifted Bank of Ireland Group's capital and loss-absorbing targets, raising compliance costs by an estimated €120–150m annually.

Volatility in Wholesale Funding Markets

While retail deposits provide a stable base, Bank of Ireland remains sensitive to wholesale funding pricing from institutional investors; in 2024 the group held €27.9bn of wholesale funding, so small spreads moves hit funding costs materially.

Downgrades or market shifts raise yields on debt and Tier 1 instruments quickly; after mid-2023 stress, Irish bank bond spreads widened ~120–180bp, pushing cost of new issuance higher.

Institutions demand higher yields in uncertainty, compressing the bank’s net interest margin—BoI reported a 2024 NIM of ~1.30%, down from 1.45% in 2022, reflecting higher wholesale costs.

- Wholesale funding €27.9bn (2024)

- Bond spread moves: +120–180 basis points (post-2023 stress)

- NIM fell to ~1.30% (2024) from 1.45% (2022)

Dependency on Global Payment Networks

Bank of Ireland depends on Visa and Mastercard for card clearing and access; these networks form an oligopoly, limiting the bank's leverage on interchange and scheme fees.

With UK/Ireland digital transactions rising—card volumes grew ~9% in 2024 and global card payments hit $29.6 trillion in 2024—these networks' bargaining power strengthened into 2025.

- Oligopoly: Visa, Mastercard dominate

- Limited fee negotiation for Bank of Ireland

- Card volumes +9% (UK/Ireland 2024)

- Global card spend $29.6T (2024)

High supplier power: concentrated cloud, costly switches, tight margins & funding risk

| Metric | Value |

|---|---|

| Cloud concentration | 70–85% |

| Switch cost / time | €200–600m / 18–36m |

| Tech vacancy (IE 2024) | 3.8% |

| Wholesale funding (2024) | €27.9bn |

| NIM (2024) | ~1.30% |

| Card volume growth (UK/IE 2024) | +9% |

What is included in the product

Tailored Porter's Five Forces analysis for Bank Of Ireland Group, uncovering competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot for Bank of Ireland—perfect for rapid strategic decisions and board briefings, with editable pressure levels to reflect regulatory shifts or competitive moves.

Customers Bargaining Power

Low Switching Costs in Digital Banking

By 2025, open banking adoption (over 70% of EU retail banks supporting APIs per European Banking Authority data) and automated digital switching have cut customer switching time to under 48 hours, sharply lowering switching costs for Bank of Ireland Group retail clients.

This mobility pushed Irish retail deposit rates down 15–25 basis points industry-wide in 2024 as banks competed on price and UX; Bank of Ireland must match or exceed these moves to avoid churn.

Customer retention now hinges on seamless mobile experiences and targeted pricing—failure risks migration to agile challengers offering instant transfers and personalized savings nudges.

Increased Price Transparency via Aggregator Platforms

Financial comparison sites and aggregators let customers compare Bank of Ireland mortgage rates, savings yields, and loan terms in real time; in 2024 UK/Ireland aggregator visits rose ~12% YoY to 230m, boosting shopper price sensitivity.

That transparency gives retail and corporate clients leverage to demand top market rates, so Bank of Ireland must match aggressive offers—mortgage rate gaps under 20 bps often drive wins.

Negotiation Leverage of Large Corporate Clients

Large corporate clients in Bank of Ireland Group’s Corporate & Treasury arm wield strong leverage—top 1% clients generate roughly 40% of corporate deposits—so they can shift credit lines or €billions in payroll to global banks; in 2024 the bank reported €21bn corporate lending, forcing bespoke credit structures and fee discounts to retain accounts, with bespoke deals cutting standard fees by 10–30% to prevent defections.

Heightened Expectations for Integrated Digital Experiences

Customers now expect bank apps and branches to work together like Big Tech; 73% of EU consumers (2024 EY survey) say they would switch banks for better digital service.

If Bank of Ireland Group lags in speed or features by end-2025, churn risk rises—Irish fintechs gained 12% retail deposits YoY in 2024—so customers force faster tech spend.

- 73% EU customers would switch (EY 2024)

- 12% YoY fintech deposit growth in Ireland (2024)

- Customer demand sets tech-investment timeline

Consumer Protection and Regulatory Advocacy

- Clearer dispute resolution: faster complaints handling

- Fee transparency: restrictions on hidden charges

- Compliance cost: €23m penalties 2019–2024

- Power shift: consumers gain leverage in pricing and terms

Customers Hold the Power: Rapid Switching, Fintech Rise, Corporate Concentration

By 2025 customers hold high bargaining power: open banking + <48h switching, 73% willing to switch (EY 2024), fintech deposits +12% YoY (Ireland 2024). Top 1% corporates supply ~40% of deposits; Bank of Ireland had €21bn corporate lending (2024). Compliance costs and €23m penalties (2019–2024) raise conduct sensitivity—mortgage gaps <20bps often trigger defections.

| Metric | Value |

|---|---|

| Switch time | <48 hours |

| Switch intent | 73% (EY 2024) |

| Fintech deposit growth | +12% YoY (2024) |

| Corp lending | €21bn (2024) |

| Penalties | €23m (2019–24) |

What You See Is What You Get

Bank Of Ireland Group Porter's Five Forces Analysis

This preview shows the exact Bank of Ireland Group Porter's Five Forces analysis you'll receive—no placeholders, no samples—ready for immediate download after purchase.

The document displayed is the professionally written, fully formatted final file; once you complete payment you’ll get instant access to this identical deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Bank of Ireland faces moderate competitive rivalry, regulatory pressure, and digital disruption that collectively shape its profitability and strategic choices.

Buyer bargaining remains significant as retail and corporate clients demand better rates and digital services, while substitute fintechs and challenger banks elevate the threat level.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank Of Ireland Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Technology and Cloud Infrastructure Providers

Competition for Specialized Financial and Tech Talent

The tight supply of cybersecurity, data science and compliance talent in Ireland and the UK—vacancy rates for tech roles hit ~3.8% in 2024 in Ireland—gives specialists strong bargaining power; Bank of Ireland’s digital push competes directly with Big Tech and fintechs, raising median tech salaries by ~12–18% in 2023–25 and forcing higher personnel costs plus retention programs (sign-on bonuses, equity-like awards, training pathways) to hold critical staff.

Influence of Central Banks and Regulatory Authorities

Regulatory bodies act as non-traditional suppliers by supplying the legal framework and ECB liquidity lines; by Q4 2025 ECB-driven CET1 and MREL guidance lifted Bank of Ireland Group's capital and loss-absorbing targets, raising compliance costs by an estimated €120–150m annually.

Volatility in Wholesale Funding Markets

While retail deposits provide a stable base, Bank of Ireland remains sensitive to wholesale funding pricing from institutional investors; in 2024 the group held €27.9bn of wholesale funding, so small spreads moves hit funding costs materially.

Downgrades or market shifts raise yields on debt and Tier 1 instruments quickly; after mid-2023 stress, Irish bank bond spreads widened ~120–180bp, pushing cost of new issuance higher.

Institutions demand higher yields in uncertainty, compressing the bank’s net interest margin—BoI reported a 2024 NIM of ~1.30%, down from 1.45% in 2022, reflecting higher wholesale costs.

- Wholesale funding €27.9bn (2024)

- Bond spread moves: +120–180 basis points (post-2023 stress)

- NIM fell to ~1.30% (2024) from 1.45% (2022)

Dependency on Global Payment Networks

Bank of Ireland depends on Visa and Mastercard for card clearing and access; these networks form an oligopoly, limiting the bank's leverage on interchange and scheme fees.

With UK/Ireland digital transactions rising—card volumes grew ~9% in 2024 and global card payments hit $29.6 trillion in 2024—these networks' bargaining power strengthened into 2025.

- Oligopoly: Visa, Mastercard dominate

- Limited fee negotiation for Bank of Ireland

- Card volumes +9% (UK/Ireland 2024)

- Global card spend $29.6T (2024)

High supplier power: concentrated cloud, costly switches, tight margins & funding risk

| Metric | Value |

|---|---|

| Cloud concentration | 70–85% |

| Switch cost / time | €200–600m / 18–36m |

| Tech vacancy (IE 2024) | 3.8% |

| Wholesale funding (2024) | €27.9bn |

| NIM (2024) | ~1.30% |

| Card volume growth (UK/IE 2024) | +9% |

What is included in the product

Tailored Porter's Five Forces analysis for Bank Of Ireland Group, uncovering competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot for Bank of Ireland—perfect for rapid strategic decisions and board briefings, with editable pressure levels to reflect regulatory shifts or competitive moves.

Customers Bargaining Power

Low Switching Costs in Digital Banking

By 2025, open banking adoption (over 70% of EU retail banks supporting APIs per European Banking Authority data) and automated digital switching have cut customer switching time to under 48 hours, sharply lowering switching costs for Bank of Ireland Group retail clients.

This mobility pushed Irish retail deposit rates down 15–25 basis points industry-wide in 2024 as banks competed on price and UX; Bank of Ireland must match or exceed these moves to avoid churn.

Customer retention now hinges on seamless mobile experiences and targeted pricing—failure risks migration to agile challengers offering instant transfers and personalized savings nudges.

Increased Price Transparency via Aggregator Platforms

Financial comparison sites and aggregators let customers compare Bank of Ireland mortgage rates, savings yields, and loan terms in real time; in 2024 UK/Ireland aggregator visits rose ~12% YoY to 230m, boosting shopper price sensitivity.

That transparency gives retail and corporate clients leverage to demand top market rates, so Bank of Ireland must match aggressive offers—mortgage rate gaps under 20 bps often drive wins.

Negotiation Leverage of Large Corporate Clients

Large corporate clients in Bank of Ireland Group’s Corporate & Treasury arm wield strong leverage—top 1% clients generate roughly 40% of corporate deposits—so they can shift credit lines or €billions in payroll to global banks; in 2024 the bank reported €21bn corporate lending, forcing bespoke credit structures and fee discounts to retain accounts, with bespoke deals cutting standard fees by 10–30% to prevent defections.

Heightened Expectations for Integrated Digital Experiences

Customers now expect bank apps and branches to work together like Big Tech; 73% of EU consumers (2024 EY survey) say they would switch banks for better digital service.

If Bank of Ireland Group lags in speed or features by end-2025, churn risk rises—Irish fintechs gained 12% retail deposits YoY in 2024—so customers force faster tech spend.

- 73% EU customers would switch (EY 2024)

- 12% YoY fintech deposit growth in Ireland (2024)

- Customer demand sets tech-investment timeline

Consumer Protection and Regulatory Advocacy

- Clearer dispute resolution: faster complaints handling

- Fee transparency: restrictions on hidden charges

- Compliance cost: €23m penalties 2019–2024

- Power shift: consumers gain leverage in pricing and terms

Customers Hold the Power: Rapid Switching, Fintech Rise, Corporate Concentration

By 2025 customers hold high bargaining power: open banking + <48h switching, 73% willing to switch (EY 2024), fintech deposits +12% YoY (Ireland 2024). Top 1% corporates supply ~40% of deposits; Bank of Ireland had €21bn corporate lending (2024). Compliance costs and €23m penalties (2019–2024) raise conduct sensitivity—mortgage gaps <20bps often trigger defections.

| Metric | Value |

|---|---|

| Switch time | <48 hours |

| Switch intent | 73% (EY 2024) |

| Fintech deposit growth | +12% YoY (2024) |

| Corp lending | €21bn (2024) |

| Penalties | €23m (2019–24) |

What You See Is What You Get

Bank Of Ireland Group Porter's Five Forces Analysis

This preview shows the exact Bank of Ireland Group Porter's Five Forces analysis you'll receive—no placeholders, no samples—ready for immediate download after purchase.

The document displayed is the professionally written, fully formatted final file; once you complete payment you’ll get instant access to this identical deliverable.