Bank Of Ireland Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and regulatory change are shaping Bank Of Ireland Group’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists seeking actionable context; purchase the full analysis to unlock detailed risk assessments, scenario forecasts, and practical recommendations.

Political factors

Irish Government Housing Initiatives

Housing for All and related measures shape mortgage demand and development lending; in 2024 Irish mortgage approvals rose ~8% y/y to ~78,000, directly influencing Bank of Ireland Group’s residential loan book of €53.2bn (YE2024).

As a dominant mortgage lender with ~28% market share, the group faces political scrutiny over interest-rate pass-through and calls for affordable housing financing reforms.

Shifts in subsidies or housing targets—e.g., government aim for 300,000 new homes (2021–2030) and recent annual targets of ~33,000—could materially move BOI’s domestic lending volumes and risk profile.

Post-Brexit Regulatory Divergence

Operating in both Ireland and the UK forces Bank of Ireland Group to navigate two regulatory regimes; as of 2025 the UK plans over 70 post-Brexit financial rule changes, requiring the bank to adapt its UK Retail arm while preserving EU compliance for its €64bn+ Irish balance sheet.

European Banking Union Integration

As an SSM-supervised institution, Bank of Ireland Group is directly affected by EU-level political decisions on banking stability; SSM stress tests in 2024 showed EU banks require CET1 buffers averaging 12.5%, pressuring domestic capital planning. Ongoing Banking Union and Capital Markets Union talks shape the group’s capital and liquidity management—Bank of Ireland reported a CET1 ratio of 14.4% at end-2025 and LCR of 149%, leaving limited excess capacity. Political drive for pan-European resilience has recently translated into stricter oversight and higher prudential requirements, constraining dividend and buyback flexibility.

Bank Levies and Taxation Policies

The Irish government’s bank levy, reintroduced in 2010 and raising about €270m in 2023, can be increased or extended, directly reducing Bank of Ireland Group’s net profits—BoI reported group pre-tax profit of €1.5bn in 2024, so a 1% levy rise could cut earnings materially.

Political talk of corporate tax tweaks and targeted windfall taxes on high-rate interest income (discussed in 2024 budget debates) poses recurring downside risk to RoE and shareholder returns.

Maintaining proactive government relations and scenario planning is essential for BoI to anticipate fiscal shifts and protect dividend capacity and capital plans.

- 2023 bank levy revenue: ~€270m

- BoI 2024 pre-tax profit: €1.5bn

- 1% levy rise could significantly lower earnings and dividend capacity

Geopolitical Stability and Trade

Global political tensions strain Ireland's open economy, affecting Bank of Ireland Group clients—corporate lending exposure to trade-dependent sectors rose 6% in 2024 as revenues faced greater volatility.

Shifts in trade agreements or sanctions drove FX and market volatility in 2024, with FDI into Ireland falling 12% YoY to €24.5bn, influencing treasury client demand and credit risk.

The group actively monitors geopolitical risks to manage international corporate lending, maintaining CET1 ratio of 15.8% (2024) to buffer potential shocks.

- 6% rise in trade-dependent lending exposure (2024)

- FDI into Ireland €24.5bn, down 12% YoY (2024)

- CET1 ratio 15.8% as of 2024

Political pressures squeeze BoI: lending, capital and dividends under strain

Political drivers—housing targets (300k 2021–30), 2024 mortgage approvals ~78,000, bank levy ~€270m (2023), and EU SSM prudential moves (CET1 ~14.4–15.8% range 2024–25)—directly pressure Bank of Ireland’s lending volumes, capital, profitability and dividend capacity amid UK post‑Brexit rule changes and weaker FDI (€24.5bn, −12% YoY 2024).

| Metric | Value |

|---|---|

| Mortgage approvals 2024 | ~78,000 |

| Residential loan book YE2024 | €53.2bn |

| FDI into Ireland 2024 | €24.5bn (−12%) |

| Bank levy revenue 2023 | ~€270m |

| CET1 ratio | 14.4–15.8% (2024–25) |

What is included in the product

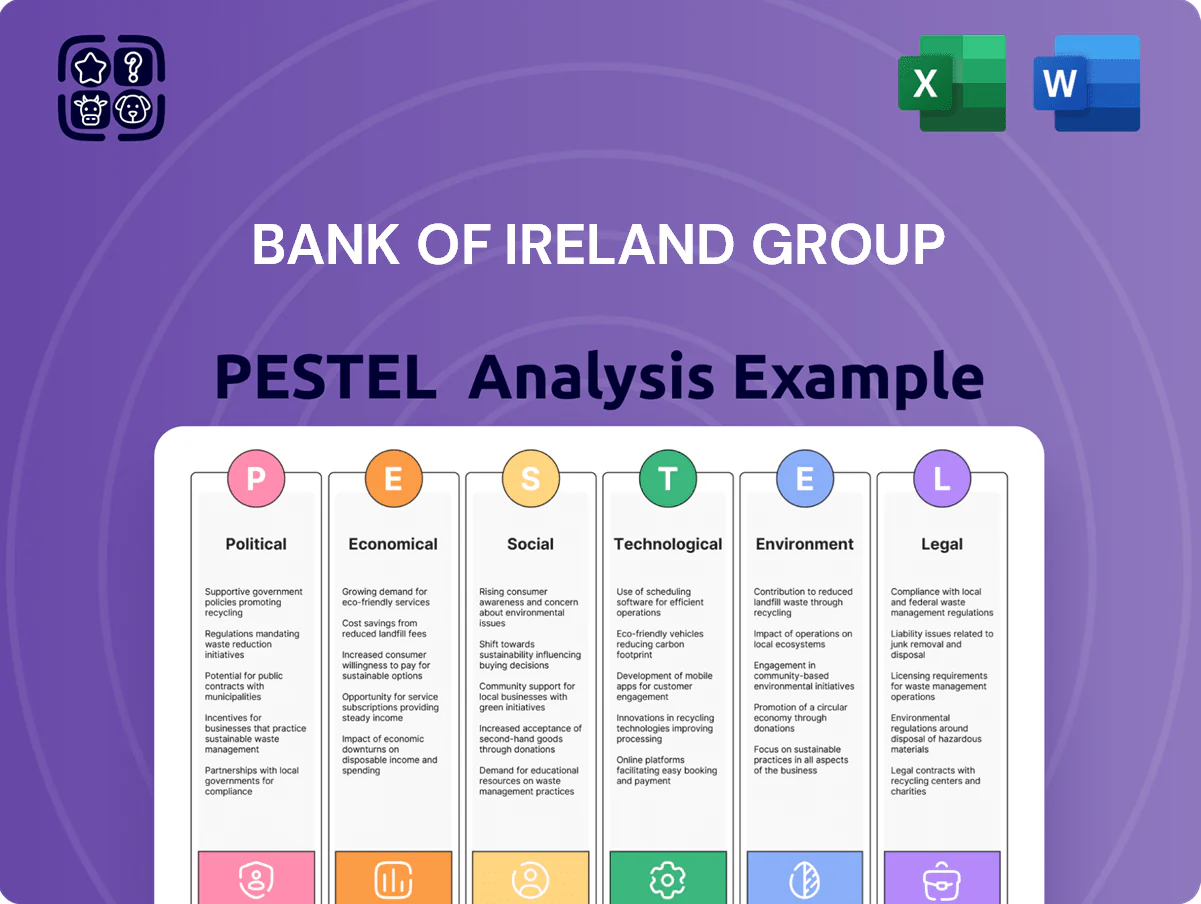

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Bank of Ireland Group, with data-backed trends and region-specific examples to identify threats and opportunities.

A concise, shareable Bank of Ireland Group PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or strategy packs, and editable for region- or business-line–specific notes to support risk discussions and cross-team alignment.

Economic factors

Interest Rate Environment Normalization

By end-2025 Bank of Ireland is adapting to a more stable rate backdrop after 2022–24 volatility; ECB deposit rate stood at 3.75% and BoE base rate at 5.25% in late 2025, easing headline rate shifts.

Net interest margin remains central—BoI reported NIM around 2.1% in H1 2025—while ECB/BoE policy pivots aim to balance 2% inflation targets with growth.

The group’s loan/deposit repricing capability, with a loan book ~€70bn and deposits ~€85bn in 2025, drives core revenue resilience in this mature rate cycle.

Irish GNI Growth and Resilience

The Bank of Ireland Group's asset quality is closely tied to Ireland's Modified Gross National Income (GNI*), which rose an estimated 6.1% in 2024, supporting lower non-performing loan ratios that fell to around 1.2% in H2 2024. Robust domestic demand and investment have bolstered lending across retail and corporate segments, while multinationals—over 1,500 headquartered or significant operations in Ireland—drive demand for wealth management and commercial services. Continued GNI* resilience underpins credit growth and fee income diversification.

Inflationary Impacts on Operating Costs

Persistent inflation in Ireland (CPI 2025 estimate ~3.8% after 2024’s 2.9%) raises Bank of Ireland Group’s operating costs via higher staff wage settlements and increased third‑party vendor fees, pressuring operating expenses (2024 cost/income ratio 56.7%).

While rising interest rates have expanded net interest margins—Group NIM improved to ~2.1% in 2024—higher living costs strain customers’ repayment capacity, elevating credit risk and impairing asset quality.

The bank must balance cost control (efficiency targets and digital outsourcing) with targeted customer support measures—payment breaks and mortgage relief—to manage defaults during volatile inflationary cycles.

Labor Market Dynamics

Ireland's near-full employment—unemployment at 4.6% in Q4 2025—supports Bank of Ireland's retail mortgage and consumer credit stability, reducing default risk.

High disposable incomes among professionals (2024 median household disposable income €39,000) boost demand for diversified products and wealth management services.

However, tight labor market raises competition for fintech and banking talent, pushing average sector salary growth to ~6% in 2024 and increasing recruitment costs.

- Unemployment 4.6% (Q4 2025)

- Median disposable income €39,000 (2024)

- Banking wage growth ~6% (2024)

Currency Volatility and Exchange Risks

With major operations in the Eurozone and the UK, Bank of Ireland Group faces EUR/GBP volatility that can swing reported UK earnings; GBP moved ~6% vs EUR in 2024 and volatility rose after 2023–24 rate divergences.

Exchange swings also impact cross-border clients’ competitiveness, potentially altering loan demand and credit risk; treasury hedging reduced FX translation exposure by about €0.3bn in H1 2025.

- EUR/GBP ~0.86–0.92 range in 2024–25

- ~€0.3bn hedged translation benefit H1 2025

- Treasury central to FX risk management

Rates Normalize, NIM ~2.1% as Inflation and Wages Squeeze Costs and Credit

Interest-rate normalization (ECB deposit 3.75%, BoE 5.25% late‑2025) lifted Group NIM to ~2.1% (H1 2025) while inflation (CPI ~3.8% 2025) and wage inflation (~6% 2024) push operating costs (cost/income 56.7% 2024) and credit risk despite low NPLs (~1.2% H2 2024); loan book ~€70bn, deposits ~€85bn, unemployment 4.6% Q4 2025; EUR/GBP ~0.86–0.92.

| Metric | Value |

|---|---|

| NIM | ~2.1% |

| Loan book | ~€70bn |

| Deposits | ~€85bn |

| Cost/Income | 56.7% |

| NPL | ~1.2% |

| Unemployment | 4.6% |

| EUR/GBP | 0.86–0.92 |

Same Document Delivered

Bank Of Ireland Group PESTLE Analysis

The preview shown here is the exact Bank of Ireland Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and regulatory change are shaping Bank Of Ireland Group’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists seeking actionable context; purchase the full analysis to unlock detailed risk assessments, scenario forecasts, and practical recommendations.

Political factors

Irish Government Housing Initiatives

Housing for All and related measures shape mortgage demand and development lending; in 2024 Irish mortgage approvals rose ~8% y/y to ~78,000, directly influencing Bank of Ireland Group’s residential loan book of €53.2bn (YE2024).

As a dominant mortgage lender with ~28% market share, the group faces political scrutiny over interest-rate pass-through and calls for affordable housing financing reforms.

Shifts in subsidies or housing targets—e.g., government aim for 300,000 new homes (2021–2030) and recent annual targets of ~33,000—could materially move BOI’s domestic lending volumes and risk profile.

Post-Brexit Regulatory Divergence

Operating in both Ireland and the UK forces Bank of Ireland Group to navigate two regulatory regimes; as of 2025 the UK plans over 70 post-Brexit financial rule changes, requiring the bank to adapt its UK Retail arm while preserving EU compliance for its €64bn+ Irish balance sheet.

European Banking Union Integration

As an SSM-supervised institution, Bank of Ireland Group is directly affected by EU-level political decisions on banking stability; SSM stress tests in 2024 showed EU banks require CET1 buffers averaging 12.5%, pressuring domestic capital planning. Ongoing Banking Union and Capital Markets Union talks shape the group’s capital and liquidity management—Bank of Ireland reported a CET1 ratio of 14.4% at end-2025 and LCR of 149%, leaving limited excess capacity. Political drive for pan-European resilience has recently translated into stricter oversight and higher prudential requirements, constraining dividend and buyback flexibility.

Bank Levies and Taxation Policies

The Irish government’s bank levy, reintroduced in 2010 and raising about €270m in 2023, can be increased or extended, directly reducing Bank of Ireland Group’s net profits—BoI reported group pre-tax profit of €1.5bn in 2024, so a 1% levy rise could cut earnings materially.

Political talk of corporate tax tweaks and targeted windfall taxes on high-rate interest income (discussed in 2024 budget debates) poses recurring downside risk to RoE and shareholder returns.

Maintaining proactive government relations and scenario planning is essential for BoI to anticipate fiscal shifts and protect dividend capacity and capital plans.

- 2023 bank levy revenue: ~€270m

- BoI 2024 pre-tax profit: €1.5bn

- 1% levy rise could significantly lower earnings and dividend capacity

Geopolitical Stability and Trade

Global political tensions strain Ireland's open economy, affecting Bank of Ireland Group clients—corporate lending exposure to trade-dependent sectors rose 6% in 2024 as revenues faced greater volatility.

Shifts in trade agreements or sanctions drove FX and market volatility in 2024, with FDI into Ireland falling 12% YoY to €24.5bn, influencing treasury client demand and credit risk.

The group actively monitors geopolitical risks to manage international corporate lending, maintaining CET1 ratio of 15.8% (2024) to buffer potential shocks.

- 6% rise in trade-dependent lending exposure (2024)

- FDI into Ireland €24.5bn, down 12% YoY (2024)

- CET1 ratio 15.8% as of 2024

Political pressures squeeze BoI: lending, capital and dividends under strain

Political drivers—housing targets (300k 2021–30), 2024 mortgage approvals ~78,000, bank levy ~€270m (2023), and EU SSM prudential moves (CET1 ~14.4–15.8% range 2024–25)—directly pressure Bank of Ireland’s lending volumes, capital, profitability and dividend capacity amid UK post‑Brexit rule changes and weaker FDI (€24.5bn, −12% YoY 2024).

| Metric | Value |

|---|---|

| Mortgage approvals 2024 | ~78,000 |

| Residential loan book YE2024 | €53.2bn |

| FDI into Ireland 2024 | €24.5bn (−12%) |

| Bank levy revenue 2023 | ~€270m |

| CET1 ratio | 14.4–15.8% (2024–25) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Bank of Ireland Group, with data-backed trends and region-specific examples to identify threats and opportunities.

A concise, shareable Bank of Ireland Group PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or strategy packs, and editable for region- or business-line–specific notes to support risk discussions and cross-team alignment.

Economic factors

Interest Rate Environment Normalization

By end-2025 Bank of Ireland is adapting to a more stable rate backdrop after 2022–24 volatility; ECB deposit rate stood at 3.75% and BoE base rate at 5.25% in late 2025, easing headline rate shifts.

Net interest margin remains central—BoI reported NIM around 2.1% in H1 2025—while ECB/BoE policy pivots aim to balance 2% inflation targets with growth.

The group’s loan/deposit repricing capability, with a loan book ~€70bn and deposits ~€85bn in 2025, drives core revenue resilience in this mature rate cycle.

Irish GNI Growth and Resilience

The Bank of Ireland Group's asset quality is closely tied to Ireland's Modified Gross National Income (GNI*), which rose an estimated 6.1% in 2024, supporting lower non-performing loan ratios that fell to around 1.2% in H2 2024. Robust domestic demand and investment have bolstered lending across retail and corporate segments, while multinationals—over 1,500 headquartered or significant operations in Ireland—drive demand for wealth management and commercial services. Continued GNI* resilience underpins credit growth and fee income diversification.

Inflationary Impacts on Operating Costs

Persistent inflation in Ireland (CPI 2025 estimate ~3.8% after 2024’s 2.9%) raises Bank of Ireland Group’s operating costs via higher staff wage settlements and increased third‑party vendor fees, pressuring operating expenses (2024 cost/income ratio 56.7%).

While rising interest rates have expanded net interest margins—Group NIM improved to ~2.1% in 2024—higher living costs strain customers’ repayment capacity, elevating credit risk and impairing asset quality.

The bank must balance cost control (efficiency targets and digital outsourcing) with targeted customer support measures—payment breaks and mortgage relief—to manage defaults during volatile inflationary cycles.

Labor Market Dynamics

Ireland's near-full employment—unemployment at 4.6% in Q4 2025—supports Bank of Ireland's retail mortgage and consumer credit stability, reducing default risk.

High disposable incomes among professionals (2024 median household disposable income €39,000) boost demand for diversified products and wealth management services.

However, tight labor market raises competition for fintech and banking talent, pushing average sector salary growth to ~6% in 2024 and increasing recruitment costs.

- Unemployment 4.6% (Q4 2025)

- Median disposable income €39,000 (2024)

- Banking wage growth ~6% (2024)

Currency Volatility and Exchange Risks

With major operations in the Eurozone and the UK, Bank of Ireland Group faces EUR/GBP volatility that can swing reported UK earnings; GBP moved ~6% vs EUR in 2024 and volatility rose after 2023–24 rate divergences.

Exchange swings also impact cross-border clients’ competitiveness, potentially altering loan demand and credit risk; treasury hedging reduced FX translation exposure by about €0.3bn in H1 2025.

- EUR/GBP ~0.86–0.92 range in 2024–25

- ~€0.3bn hedged translation benefit H1 2025

- Treasury central to FX risk management

Rates Normalize, NIM ~2.1% as Inflation and Wages Squeeze Costs and Credit

Interest-rate normalization (ECB deposit 3.75%, BoE 5.25% late‑2025) lifted Group NIM to ~2.1% (H1 2025) while inflation (CPI ~3.8% 2025) and wage inflation (~6% 2024) push operating costs (cost/income 56.7% 2024) and credit risk despite low NPLs (~1.2% H2 2024); loan book ~€70bn, deposits ~€85bn, unemployment 4.6% Q4 2025; EUR/GBP ~0.86–0.92.

| Metric | Value |

|---|---|

| NIM | ~2.1% |

| Loan book | ~€70bn |

| Deposits | ~€85bn |

| Cost/Income | 56.7% |

| NPL | ~1.2% |

| Unemployment | 4.6% |

| EUR/GBP | 0.86–0.92 |

Same Document Delivered

Bank Of Ireland Group PESTLE Analysis

The preview shown here is the exact Bank of Ireland Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.