Bank Of Jiangsu Business Model Canvas

Bank of Jiangsu: Complete Business Model Canvas & Templates for Investors and Strategists

Unlock the full strategic blueprint behind Bank Of Jiangsu’s business model—this in-depth Business Model Canvas exposes how the bank creates value, manages risk, and captures market share across retail, corporate, and digital channels; ideal for investors, consultants, and strategists seeking actionable insights and ready-to-use templates. Download the complete Word and Excel files to benchmark, plan, or pitch with confidence.

Partnerships

Strategic Local Government Alliances

The bank maintains deep-rooted connections with municipal and provincial government bodies across Jiangsu, managing over RMB 120 billion in public-sector deposits and handling 28% of the province’s government treasury flows as of 2024. These alliances finance large infrastructure projects—RMB 65 billion in transport and urban development loans in 2024—securing steady institutional revenue and reinforcing the bank’s central role in regional economic planning.

FinTech and Technology Collaborators

Collaboration with leading technology firms and FinTech startups keeps Bank of Jiangsu digitally competitive into late 2025, with partners supplying AI models, big-data analytics and cloud platforms that cut loan decision times by up to 45% and support mobile MAU growth of 28% year-on-year (2024–25).

Interbank and Financial Institution Networks

Bank of Jiangsu partners with domestic and international banks and clearing houses to support interbank lending and trade finance, managing liquidity via repo and CP lines that accounted for roughly CNY 120 billion of short-term funding in 2024. By joining SWIFT, China National Interbank Funding Center, and regional correspondent networks, the bank provides global settlement, diversified investment products, and access beyond its ~300-branch footprint.

Corporate and Industrial Ecosystem Partners

Bank of Jiangsu partners with top manufacturers and supply-chain leaders to embed financing in their business cycles, delivering supply-chain finance and B2B payments that in 2024 supported roughly CNY 120bn of corporate credit lines and raised commercial deposits by an estimated CNY 45bn.

Here’s the quick math…

- Integrated financing drives steady loan pipeline (~CNY 120bn, 2024)

- Boosts high-quality commercial deposits (~CNY 45bn, 2024)

- Focus: supply-chain finance, B2B payments, embedded services

Third Party Payment and Wealth Platforms

Partnerships with Alipay and China UnionPay embed Bank of Jiangsu into daily payments, supporting 2024 transaction volumes where UnionPay processed ~89% of China's card payments and Alipay held ~43% of mobile payments.

Collaborations with external fund managers and insurers expand wealth offerings—Bank of Jiangsu distributed third-party funds and insurance, boosting fee income and serving retail clients seeking one-stop financial services.

- Alipay ~43% mobile market share (2024)

- UnionPay ~89% card payment share (2024)

- Third-party wealth products increase fee income and retention

RMB 360bn funding & partners supercharge transactions: Alipay 43%, UnionPay 89%, mobile MAU +28%

Key partners supply public deposits (~RMB 120bn, 2024), short-term funding (~RMB 120bn repo/CP, 2024), and corporate credit (~RMB 120bn supply-chain finance, 2024), while Alipay (43% mobile, 2024) and UnionPay (89% card, 2024) drive transaction volume; tech partners cut loan decision time 45% and lifted mobile MAU 28% (2024–25).

| Partner / Metric | 2024–25 figure |

|---|---|

| Public-sector deposits | RMB 120bn |

| Repo/CP short-term funding | RMB 120bn |

| Supply-chain corporate credit | RMB 120bn |

| Commercial deposit lift | RMB 45bn |

| Alipay mobile share | 43% |

| UnionPay card share | 89% |

| Loan decision time cut | 45% |

| Mobile MAU growth | 28% YoY |

What is included in the product

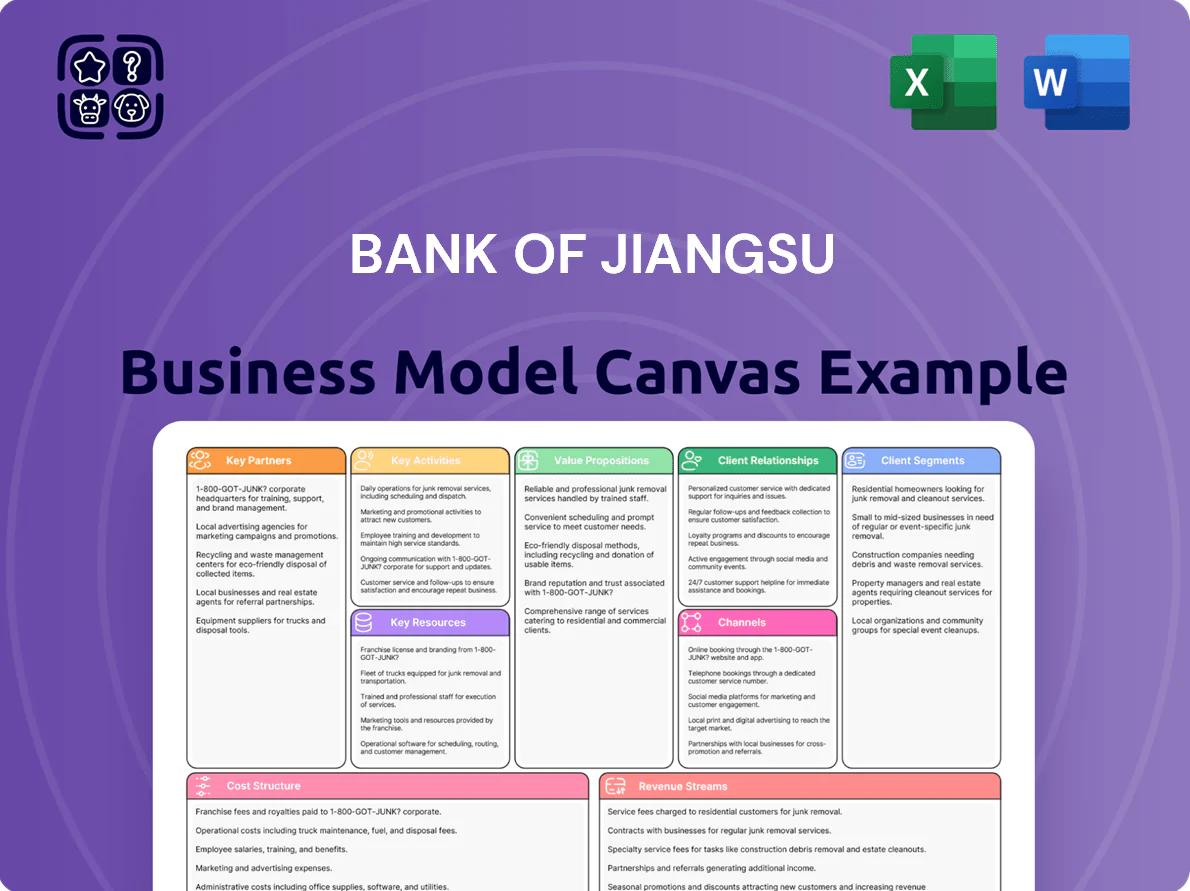

A concise, ready-made Business Model Canvas for Bank of Jiangsu detailing nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting the bank’s commercial and retail operations, competitive advantages, and strategic risks to support presentations, investor discussions, and analytical decision-making.

High-level view of Bank of Jiangsu’s business model with editable cells to pinpoint risk areas, streamline branch and digital channel strategies, and accelerate remediation planning.

Activities

Comprehensive Credit and Lending Operations

The bank underwrites and disburses retail and corporate loans—serving households, SMEs, and state-owned firms—with 2024 loan book at CNY 420 billion and annual new originations ~CNY 85 billion. It uses probabilistic risk models and stress testing (NPL ratio 1.9% in 2024) to limit credit exposure while prioritizing SME lending, which accounted for 28% of new loans, ensuring capital flows across Jiangsu and key cities like Nanjing and Suzhou.

Digital Banking and Platform Development

As of 2025, Bank of Jiangsu prioritizes digital banking and platform development, investing over CNY 1.2 billion in its digital ecosystem to expand mobile users to 28 million and cut average transaction time by 35%.

Projects include redesigned mobile apps, upgraded cybersecurity (reducing fraud losses 22% year-on-year), and RPA automation for 60% of routine processes to lower operating cost-to-income ratio.

Wealth Management and Advisory Services

Bank of Jiangsu manages a broad mix of investment products for retail and institutional clients, using market research and product structuring to target client risk-return profiles; as of 2025 its wealth AUM approached CNY 420 billion, up ~8% year-on-year. Dedicated advisory teams deliver personalized financial plans and launch new vehicles—including CNY-denominated private funds and structured notes—aligned with 2024–25 regulatory guidelines and market trends.

Risk Management and Regulatory Compliance

Ongoing monitoring of market, operational and credit risks is core, with stress tests and daily VaR runs; in 2024 Chinese banks' CET1 targets tightened to roughly 8.5–10% under CBIRC guidance, so Bank of Jiangsu tracks capital adequacy to ensure long-term stability.

Strict adherence to evolving China rules—capital buffers, AML (anti-money laundering) checks and reporting—plus robust internal audit and compliance frameworks protect shareholders and depositors; internal audits cover 100% of high-risk units annually.

- Daily VaR and monthly stress tests

- CET1 target ~8.5–10% (CBIRC 2024 guidance)

- 100% annual audit of high-risk units

- Continuous AML transaction monitoring and SAR reporting

Green Finance and Social Responsibility Initiatives

Bank of Jiangsu sharply ramped sustainable finance: by end-2024 it booked CNY 42.7 billion in green loans and issued CNY 10.2 billion in green bonds, prioritizing renewables and energy-efficiency with preferential rates 0.3–0.8ppt below market to support China’s carbon-neutrality targets.

- CNY 42.7B green loans (2024)

- CNY 10.2B green bonds issued

- Preferential rates 0.3–0.8ppt

- Targets renewables, EE projects

- Supports national net-zero goals

Robust growth: CNY420B loan book, 28M mobile users, strong green finance & capital targets

Underwrites CNY 420B loans (2024), CNY 85B new originations, NPL 1.9%; digital spend CNY 1.2B (2025) to reach 28M mobile users; wealth AUM CNY 420B (2025); green loans CNY 42.7B, green bonds CNY 10.2B; CET1 target 8.5–10%; daily VaR, monthly stress tests, 100% high-risk audits.

| Metric | 2024–25 |

|---|---|

| Loan book | CNY 420B |

| New originations | CNY 85B |

| NPL | 1.9% |

| Digital spend | CNY 1.2B |

| Mobile users | 28M |

| Wealth AUM | CNY 420B |

| Green loans | CNY 42.7B |

| Green bonds | CNY 10.2B |

| CET1 target | 8.5–10% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Bank of Jiangsu Business Model Canvas—not a mockup or sample—and it reflects the exact file you will receive after purchase.

When you complete your order, you’ll get full access to this same professionally formatted, ready-to-edit document in both Word and Excel, with all content and pages included.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bank of Jiangsu: Complete Business Model Canvas & Templates for Investors and Strategists

Unlock the full strategic blueprint behind Bank Of Jiangsu’s business model—this in-depth Business Model Canvas exposes how the bank creates value, manages risk, and captures market share across retail, corporate, and digital channels; ideal for investors, consultants, and strategists seeking actionable insights and ready-to-use templates. Download the complete Word and Excel files to benchmark, plan, or pitch with confidence.

Partnerships

Strategic Local Government Alliances

The bank maintains deep-rooted connections with municipal and provincial government bodies across Jiangsu, managing over RMB 120 billion in public-sector deposits and handling 28% of the province’s government treasury flows as of 2024. These alliances finance large infrastructure projects—RMB 65 billion in transport and urban development loans in 2024—securing steady institutional revenue and reinforcing the bank’s central role in regional economic planning.

FinTech and Technology Collaborators

Collaboration with leading technology firms and FinTech startups keeps Bank of Jiangsu digitally competitive into late 2025, with partners supplying AI models, big-data analytics and cloud platforms that cut loan decision times by up to 45% and support mobile MAU growth of 28% year-on-year (2024–25).

Interbank and Financial Institution Networks

Bank of Jiangsu partners with domestic and international banks and clearing houses to support interbank lending and trade finance, managing liquidity via repo and CP lines that accounted for roughly CNY 120 billion of short-term funding in 2024. By joining SWIFT, China National Interbank Funding Center, and regional correspondent networks, the bank provides global settlement, diversified investment products, and access beyond its ~300-branch footprint.

Corporate and Industrial Ecosystem Partners

Bank of Jiangsu partners with top manufacturers and supply-chain leaders to embed financing in their business cycles, delivering supply-chain finance and B2B payments that in 2024 supported roughly CNY 120bn of corporate credit lines and raised commercial deposits by an estimated CNY 45bn.

Here’s the quick math…

- Integrated financing drives steady loan pipeline (~CNY 120bn, 2024)

- Boosts high-quality commercial deposits (~CNY 45bn, 2024)

- Focus: supply-chain finance, B2B payments, embedded services

Third Party Payment and Wealth Platforms

Partnerships with Alipay and China UnionPay embed Bank of Jiangsu into daily payments, supporting 2024 transaction volumes where UnionPay processed ~89% of China's card payments and Alipay held ~43% of mobile payments.

Collaborations with external fund managers and insurers expand wealth offerings—Bank of Jiangsu distributed third-party funds and insurance, boosting fee income and serving retail clients seeking one-stop financial services.

- Alipay ~43% mobile market share (2024)

- UnionPay ~89% card payment share (2024)

- Third-party wealth products increase fee income and retention

RMB 360bn funding & partners supercharge transactions: Alipay 43%, UnionPay 89%, mobile MAU +28%

Key partners supply public deposits (~RMB 120bn, 2024), short-term funding (~RMB 120bn repo/CP, 2024), and corporate credit (~RMB 120bn supply-chain finance, 2024), while Alipay (43% mobile, 2024) and UnionPay (89% card, 2024) drive transaction volume; tech partners cut loan decision time 45% and lifted mobile MAU 28% (2024–25).

| Partner / Metric | 2024–25 figure |

|---|---|

| Public-sector deposits | RMB 120bn |

| Repo/CP short-term funding | RMB 120bn |

| Supply-chain corporate credit | RMB 120bn |

| Commercial deposit lift | RMB 45bn |

| Alipay mobile share | 43% |

| UnionPay card share | 89% |

| Loan decision time cut | 45% |

| Mobile MAU growth | 28% YoY |

What is included in the product

A concise, ready-made Business Model Canvas for Bank of Jiangsu detailing nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting the bank’s commercial and retail operations, competitive advantages, and strategic risks to support presentations, investor discussions, and analytical decision-making.

High-level view of Bank of Jiangsu’s business model with editable cells to pinpoint risk areas, streamline branch and digital channel strategies, and accelerate remediation planning.

Activities

Comprehensive Credit and Lending Operations

The bank underwrites and disburses retail and corporate loans—serving households, SMEs, and state-owned firms—with 2024 loan book at CNY 420 billion and annual new originations ~CNY 85 billion. It uses probabilistic risk models and stress testing (NPL ratio 1.9% in 2024) to limit credit exposure while prioritizing SME lending, which accounted for 28% of new loans, ensuring capital flows across Jiangsu and key cities like Nanjing and Suzhou.

Digital Banking and Platform Development

As of 2025, Bank of Jiangsu prioritizes digital banking and platform development, investing over CNY 1.2 billion in its digital ecosystem to expand mobile users to 28 million and cut average transaction time by 35%.

Projects include redesigned mobile apps, upgraded cybersecurity (reducing fraud losses 22% year-on-year), and RPA automation for 60% of routine processes to lower operating cost-to-income ratio.

Wealth Management and Advisory Services

Bank of Jiangsu manages a broad mix of investment products for retail and institutional clients, using market research and product structuring to target client risk-return profiles; as of 2025 its wealth AUM approached CNY 420 billion, up ~8% year-on-year. Dedicated advisory teams deliver personalized financial plans and launch new vehicles—including CNY-denominated private funds and structured notes—aligned with 2024–25 regulatory guidelines and market trends.

Risk Management and Regulatory Compliance

Ongoing monitoring of market, operational and credit risks is core, with stress tests and daily VaR runs; in 2024 Chinese banks' CET1 targets tightened to roughly 8.5–10% under CBIRC guidance, so Bank of Jiangsu tracks capital adequacy to ensure long-term stability.

Strict adherence to evolving China rules—capital buffers, AML (anti-money laundering) checks and reporting—plus robust internal audit and compliance frameworks protect shareholders and depositors; internal audits cover 100% of high-risk units annually.

- Daily VaR and monthly stress tests

- CET1 target ~8.5–10% (CBIRC 2024 guidance)

- 100% annual audit of high-risk units

- Continuous AML transaction monitoring and SAR reporting

Green Finance and Social Responsibility Initiatives

Bank of Jiangsu sharply ramped sustainable finance: by end-2024 it booked CNY 42.7 billion in green loans and issued CNY 10.2 billion in green bonds, prioritizing renewables and energy-efficiency with preferential rates 0.3–0.8ppt below market to support China’s carbon-neutrality targets.

- CNY 42.7B green loans (2024)

- CNY 10.2B green bonds issued

- Preferential rates 0.3–0.8ppt

- Targets renewables, EE projects

- Supports national net-zero goals

Robust growth: CNY420B loan book, 28M mobile users, strong green finance & capital targets

Underwrites CNY 420B loans (2024), CNY 85B new originations, NPL 1.9%; digital spend CNY 1.2B (2025) to reach 28M mobile users; wealth AUM CNY 420B (2025); green loans CNY 42.7B, green bonds CNY 10.2B; CET1 target 8.5–10%; daily VaR, monthly stress tests, 100% high-risk audits.

| Metric | 2024–25 |

|---|---|

| Loan book | CNY 420B |

| New originations | CNY 85B |

| NPL | 1.9% |

| Digital spend | CNY 1.2B |

| Mobile users | 28M |

| Wealth AUM | CNY 420B |

| Green loans | CNY 42.7B |

| Green bonds | CNY 10.2B |

| CET1 target | 8.5–10% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Bank of Jiangsu Business Model Canvas—not a mockup or sample—and it reflects the exact file you will receive after purchase.

When you complete your order, you’ll get full access to this same professionally formatted, ready-to-edit document in both Word and Excel, with all content and pages included.