Bank Of Jiangsu Marketing Mix

Ready-Made Marketing Analysis, Ready to Use

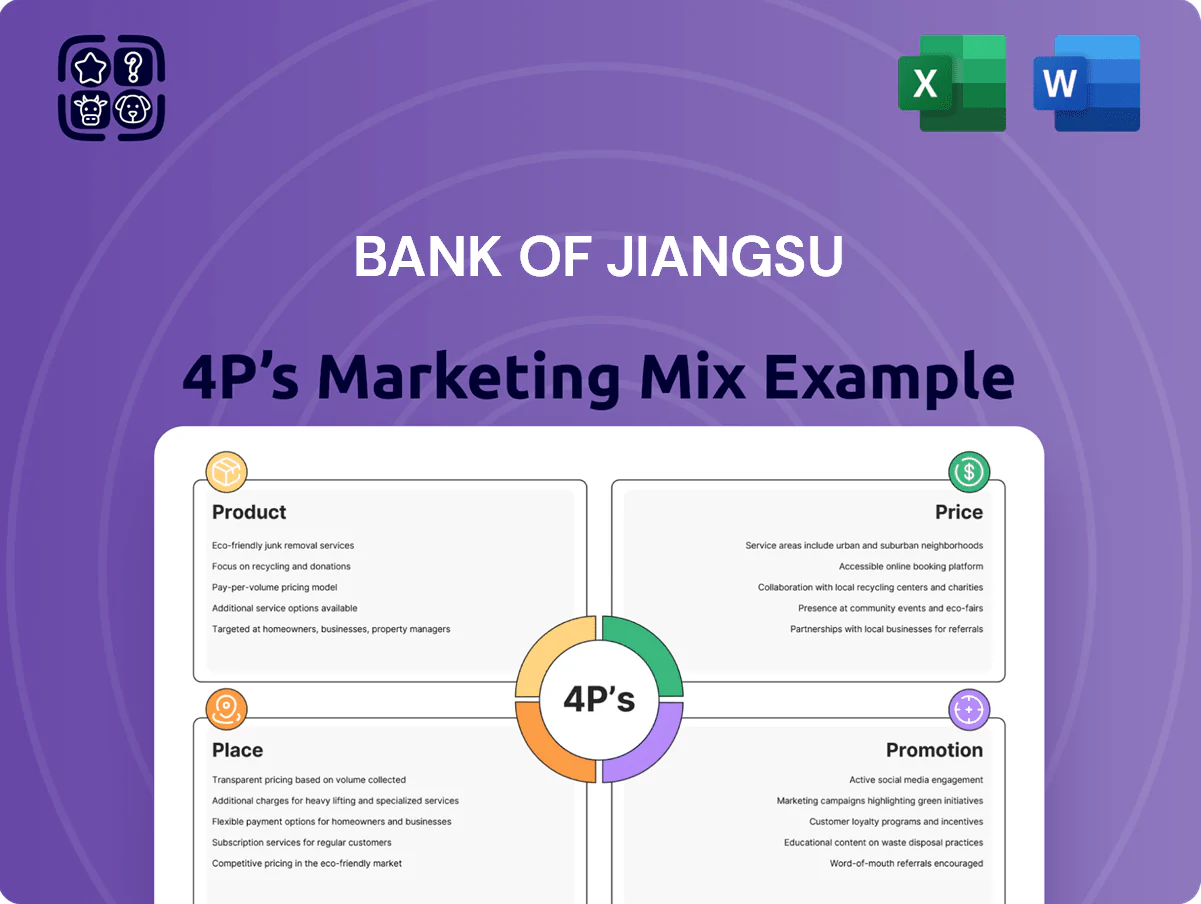

Bank of Jiangsu’s 4P’s reveal a customer-centric product suite, competitive tiered pricing, extensive branch and digital distribution, and targeted promotional outreach—yet the preview only hints at strategic nuance and executional detail.

Go beyond the summary—purchase the full, editable 4P’s Marketing Mix Analysis to get data-backed insights, ready-to-use slides, and actionable recommendations for benchmarking, strategy, or coursework.

Product

Diversified Corporate Banking Solutions

Bank of Jiangsu targets SMEs with tailored credit and trade-finance, funding over CNY 120 billion to 18,000 SMEs in 2025 and covering 42% of the bank’s corporate loan book.

By end-2025 the bank expanded supply-chain finance across Yangtze River Delta clusters, increasing SCF disbursements 38% year-on-year to CNY 65 billion.

Products include specialised loans for high-tech manufacturing and green energy, with CNY 15 billion earmarked for renewable projects in 2025, matching national industrial policy priorities.

Comprehensive Wealth Management Services

Under SuYin Wealth Management, Bank of Jiangsu offers mutual fund distribution, insurance brokerage, and proprietary structured products serving mass and HNW clients; assets under management reached about CNY 95 billion in 2024, up 12% year-on-year.

Products target risk-managed, stable returns—structured-note issuance totaled CNY 18.5 billion in 2024—and retail channels now include data-driven portfolio advisory tools with model portfolios showing average annualized returns of ~6.4% (2019–2024).

Advanced Digital Banking Ecosystem

As of 2025, Bank of Jiangsu’s mobile app is the central hub for retail and corporate banking, with AI-driven assistants handling 24/7 inquiries and automating routine tasks; monthly active users reached 8.2 million in 2024, up 28% year-over-year.

The digital suite offers instant consumer loans and virtual credit cards using big data credit models that approve scores in under 90 seconds; digital lending comprised 36% of new retail loans in 2024.

Seamless transaction capabilities—real-time payments, API connectivity for SMEs, and P2P transfers—cut transaction latency to <1 second for 72% of payments, boosting mobile transaction volume to CNY 1.4 trillion in 2024.

Specialized Green Finance Instruments

- Carbon-linked loans: CNY 4.2bn deployed (2024)

- Green bonds: CNY 4.5bn issued (2024)

- Includes APAC-standard reporting for emissions and use of proceeds

Retail Credit and Payment Products

- Mortgage share: ~28% of retail loans (2024)

- Card receivables growth: +12% (2024)

- Co-brand transactions up: +18% (2024)

- Retail credit delinquency: 1.6% (2024)

Bank of Jiangsu: SME & SCF-led growth, CNY185bn target, CNY95bn wealth AUM

Bank of Jiangsu’s product mix centers on SME credit and SCF (CNY 185bn corporate/SCF by end‑2025), green finance (CNY 8.7bn green by 2024), retail wealth AUM CNY 95bn (2024), digital lending 36% of new retail loans (2024), mobile MAU 8.2m (2024).

| Metric | Value |

|---|---|

| SME funding (2025) | CNY 120bn |

| SCF (2025) | CNY 65bn |

| Green finance (2024) | CNY 8.7bn |

| Wealth AUM (2024) | CNY 95bn |

What is included in the product

Delivers a concise, company-specific deep dive into Bank of Jiangsu’s Product, Price, Place, and Promotion strategies—ideal for managers and consultants needing a clear marketing positioning breakdown grounded in the bank’s actual practices and competitive context.

Condenses the Bank of Jiangsu 4P’s into a concise, at-a-glance summary to speed leadership alignment and decision-making, easily customizable for presentations, competitor comparisons, or workshop use.

Place

Strategic Regional Branch Network

The bank maintains a dominant physical presence across Jiangsu province with over 420 branches and outlets as of FY2024, ensuring high visibility in a region that contributed roughly 18% of its 2024 net profit (RMB 3.2bn of RMB 17.8bn). Beyond Jiangsu it runs strategic branches in Beijing, Shanghai and Shenzhen to win cross‑regional corporate clients and CNY 120bn in interregional deposits. Branches use smart‑branch tech—self‑service kiosks and digital onboarding—to cut teller traffic by ~35% and lift transaction throughput 28% year‑over‑year.

Integrated Mobile and Online Platforms

By end-2025 the digital channel will handle ~72% of Bank of Jiangsu's retail transactions, with the SuYin mobile app and upgraded web portal offering deposits, loans, payments, wealth products and e-KYC so customers rarely need branches; average digital NPS rose to 48 in 2024 and mobile monthly active users hit 6.4 million in Q4 2025, supporting consistent omni-channel UX focused on speed and convenience.

Community and Rural Service Points

Strategic Fintech and Third-Party Partnerships

Bank of Jiangsu partners with Baidu, Alibaba-affiliate Ant Group, and Tencent to embed its payment and lending into third-party apps, driving 28% of new retail loans via platform channels in 2024.

Integrations at e-commerce checkout and in-app finance place services at the point of need, cutting acquisition cost per user by about 35% versus bank-only channels.

Corporate and Institutional On-Site Banking

For large corporate and government clients, Bank of Jiangsu assigns dedicated relationship managers and on-site teams to handle payroll, liquidity and project funding, delivering high-touch service and embedding bankers within client finance departments.

This direct distribution model drives deep institutional integration; as of 2025 the bank reports ~28% of corporate deposits and 35% of large-ticket loan balances tied to on-site accounts, boosting retention and cross-sell.

Here’s the quick summary:

- Dedicated RMs and on-site teams

- Manage payroll, liquidity, project funding

- 28% corporate deposits via on-site (2025)

- 35% large-ticket loans via on-site (2025)

Bank of Jiangsu: 420+ branches, 6.4M MAU SuYin — 72% digital retail, 2.3M rural clients

Bank of Jiangsu uses 420+ branches, 1,200+ rural service points, and strategic city branches plus digital channels (SuYin app: 6.4M MAU Q4 2025) to reach 2.3M rural customers; digital handles ~72% retail transactions (end‑2025), partners (Baidu/Ant/Tencent) drove 28% new retail loans (2024), on‑site teams hold ~28% corporate deposits and 35% large loans (2025).

| Metric | Value |

|---|---|

| Branches/outlets (FY2024) | 420+ |

| Rural service points (2025) | 1,200+ |

| Digital retail tx share (end‑2025) | ~72% |

| SuYin MAU (Q4 2025) | 6.4M |

| Rural customers served | 2.3M |

| Partner-driven new retail loans (2024) | 28% |

| Corporate deposits via on-site (2025) | ~28% |

| Large-ticket loans via on-site (2025) | ~35% |

Full Version Awaits

Bank Of Jiangsu 4P's Marketing Mix Analysis

The preview shown here is the actual Bank of Jiangsu 4P's Marketing Mix analysis you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Ready-Made Marketing Analysis, Ready to Use

Bank of Jiangsu’s 4P’s reveal a customer-centric product suite, competitive tiered pricing, extensive branch and digital distribution, and targeted promotional outreach—yet the preview only hints at strategic nuance and executional detail.

Go beyond the summary—purchase the full, editable 4P’s Marketing Mix Analysis to get data-backed insights, ready-to-use slides, and actionable recommendations for benchmarking, strategy, or coursework.

Product

Diversified Corporate Banking Solutions

Bank of Jiangsu targets SMEs with tailored credit and trade-finance, funding over CNY 120 billion to 18,000 SMEs in 2025 and covering 42% of the bank’s corporate loan book.

By end-2025 the bank expanded supply-chain finance across Yangtze River Delta clusters, increasing SCF disbursements 38% year-on-year to CNY 65 billion.

Products include specialised loans for high-tech manufacturing and green energy, with CNY 15 billion earmarked for renewable projects in 2025, matching national industrial policy priorities.

Comprehensive Wealth Management Services

Under SuYin Wealth Management, Bank of Jiangsu offers mutual fund distribution, insurance brokerage, and proprietary structured products serving mass and HNW clients; assets under management reached about CNY 95 billion in 2024, up 12% year-on-year.

Products target risk-managed, stable returns—structured-note issuance totaled CNY 18.5 billion in 2024—and retail channels now include data-driven portfolio advisory tools with model portfolios showing average annualized returns of ~6.4% (2019–2024).

Advanced Digital Banking Ecosystem

As of 2025, Bank of Jiangsu’s mobile app is the central hub for retail and corporate banking, with AI-driven assistants handling 24/7 inquiries and automating routine tasks; monthly active users reached 8.2 million in 2024, up 28% year-over-year.

The digital suite offers instant consumer loans and virtual credit cards using big data credit models that approve scores in under 90 seconds; digital lending comprised 36% of new retail loans in 2024.

Seamless transaction capabilities—real-time payments, API connectivity for SMEs, and P2P transfers—cut transaction latency to <1 second for 72% of payments, boosting mobile transaction volume to CNY 1.4 trillion in 2024.

Specialized Green Finance Instruments

- Carbon-linked loans: CNY 4.2bn deployed (2024)

- Green bonds: CNY 4.5bn issued (2024)

- Includes APAC-standard reporting for emissions and use of proceeds

Retail Credit and Payment Products

- Mortgage share: ~28% of retail loans (2024)

- Card receivables growth: +12% (2024)

- Co-brand transactions up: +18% (2024)

- Retail credit delinquency: 1.6% (2024)

Bank of Jiangsu: SME & SCF-led growth, CNY185bn target, CNY95bn wealth AUM

Bank of Jiangsu’s product mix centers on SME credit and SCF (CNY 185bn corporate/SCF by end‑2025), green finance (CNY 8.7bn green by 2024), retail wealth AUM CNY 95bn (2024), digital lending 36% of new retail loans (2024), mobile MAU 8.2m (2024).

| Metric | Value |

|---|---|

| SME funding (2025) | CNY 120bn |

| SCF (2025) | CNY 65bn |

| Green finance (2024) | CNY 8.7bn |

| Wealth AUM (2024) | CNY 95bn |

What is included in the product

Delivers a concise, company-specific deep dive into Bank of Jiangsu’s Product, Price, Place, and Promotion strategies—ideal for managers and consultants needing a clear marketing positioning breakdown grounded in the bank’s actual practices and competitive context.

Condenses the Bank of Jiangsu 4P’s into a concise, at-a-glance summary to speed leadership alignment and decision-making, easily customizable for presentations, competitor comparisons, or workshop use.

Place

Strategic Regional Branch Network

The bank maintains a dominant physical presence across Jiangsu province with over 420 branches and outlets as of FY2024, ensuring high visibility in a region that contributed roughly 18% of its 2024 net profit (RMB 3.2bn of RMB 17.8bn). Beyond Jiangsu it runs strategic branches in Beijing, Shanghai and Shenzhen to win cross‑regional corporate clients and CNY 120bn in interregional deposits. Branches use smart‑branch tech—self‑service kiosks and digital onboarding—to cut teller traffic by ~35% and lift transaction throughput 28% year‑over‑year.

Integrated Mobile and Online Platforms

By end-2025 the digital channel will handle ~72% of Bank of Jiangsu's retail transactions, with the SuYin mobile app and upgraded web portal offering deposits, loans, payments, wealth products and e-KYC so customers rarely need branches; average digital NPS rose to 48 in 2024 and mobile monthly active users hit 6.4 million in Q4 2025, supporting consistent omni-channel UX focused on speed and convenience.

Community and Rural Service Points

Strategic Fintech and Third-Party Partnerships

Bank of Jiangsu partners with Baidu, Alibaba-affiliate Ant Group, and Tencent to embed its payment and lending into third-party apps, driving 28% of new retail loans via platform channels in 2024.

Integrations at e-commerce checkout and in-app finance place services at the point of need, cutting acquisition cost per user by about 35% versus bank-only channels.

Corporate and Institutional On-Site Banking

For large corporate and government clients, Bank of Jiangsu assigns dedicated relationship managers and on-site teams to handle payroll, liquidity and project funding, delivering high-touch service and embedding bankers within client finance departments.

This direct distribution model drives deep institutional integration; as of 2025 the bank reports ~28% of corporate deposits and 35% of large-ticket loan balances tied to on-site accounts, boosting retention and cross-sell.

Here’s the quick summary:

- Dedicated RMs and on-site teams

- Manage payroll, liquidity, project funding

- 28% corporate deposits via on-site (2025)

- 35% large-ticket loans via on-site (2025)

Bank of Jiangsu: 420+ branches, 6.4M MAU SuYin — 72% digital retail, 2.3M rural clients

Bank of Jiangsu uses 420+ branches, 1,200+ rural service points, and strategic city branches plus digital channels (SuYin app: 6.4M MAU Q4 2025) to reach 2.3M rural customers; digital handles ~72% retail transactions (end‑2025), partners (Baidu/Ant/Tencent) drove 28% new retail loans (2024), on‑site teams hold ~28% corporate deposits and 35% large loans (2025).

| Metric | Value |

|---|---|

| Branches/outlets (FY2024) | 420+ |

| Rural service points (2025) | 1,200+ |

| Digital retail tx share (end‑2025) | ~72% |

| SuYin MAU (Q4 2025) | 6.4M |

| Rural customers served | 2.3M |

| Partner-driven new retail loans (2024) | 28% |

| Corporate deposits via on-site (2025) | ~28% |

| Large-ticket loans via on-site (2025) | ~35% |

Full Version Awaits

Bank Of Jiangsu 4P's Marketing Mix Analysis

The preview shown here is the actual Bank of Jiangsu 4P's Marketing Mix analysis you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.