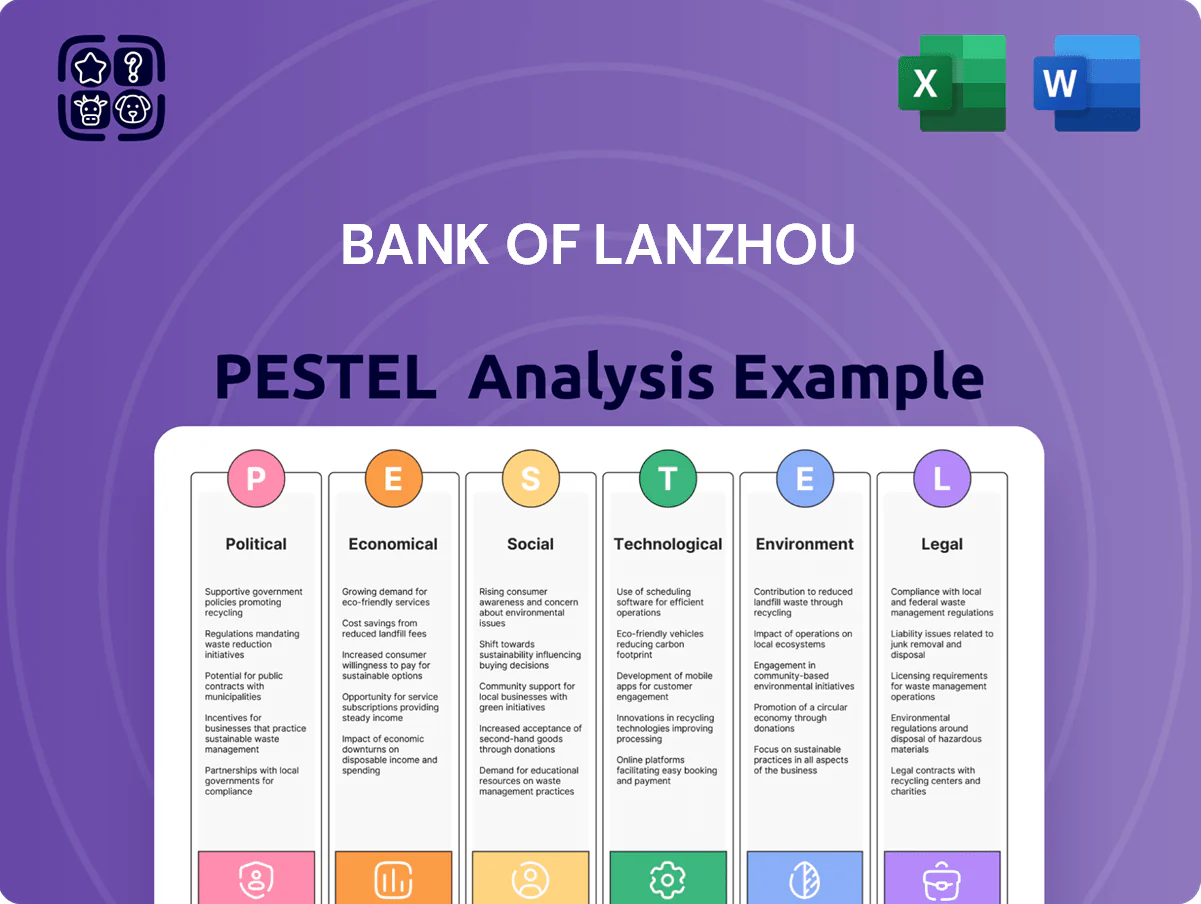

Bank of Lanzhou PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE analysis pinpoints how regulatory shifts, regional economic trends, and digital banking innovations specifically shape Bank of Lanzhou's strategic risks and opportunities—essential reading for investors and strategists. Buy the full report to access data-driven insights, ready-to-use recommendations, and editable charts to inform your next move.

Political factors

Western Development Strategy

Bank of Lanzhou benefits from Beijing’s Great Western Development Strategy, which since 2015 has directed over CNY 1.8 trillion to western infrastructure; Gansu received CNY ~120 billion in central transfers in 2023, boosting regional credit demand.

As a leading regional lender, the bank aligns lending with state mandates to secure preferential access to large projects, capturing a growing share of provincial infrastructure loans (estimated >30% of its corporate book in 2024).

Political alignment ensures steady institutional business but raises concentration risk: exposure to state-directed investment could amplify losses if policy priorities shift, with non-performing loans in infrastructure-sensitive sectors up 0.6 ppt in 2024.

Belt and Road Initiative Integration

Lanzhou, as a key logistics hub on the Silk Road Economic Belt, positions Bank of Lanzhou to capture cross-border trade finance—Gansu handled 2024 trade flows of about $12.6 billion with Central Asia, boosting demand for letters of credit and supply-chain financing.

Government investments—Gansu’s infrastructure spending rose 8.2% in 2023–24—spur need for FX services and syndicated loans as firms expand into Central Asian markets.

The bank must manage geopolitical risks from tariffs and sanctions while aligning with provincial goals to be a transit powerhouse; success hinges on maintained relationships with local authorities and national trade bodies such as China Council for the Promotion of International Trade.

Regulatory Oversight and Stability

By end-2025 the National Financial Regulatory Administration intensified oversight of regional banks to curb local-debt systemic risk, prompting Bank of Lanzhou to undergo stricter inspections of capital adequacy—notably CET1 targets rising toward 10.5%—and transparency of off-balance-sheet items totaling about CNY 12–15 billion.

Rural Revitalization Mandates

Chinese rural revitalization drives compel Bank of Lanzhou to extend low-interest credit to agriculture and cooperatives, aligning with central targets to halve rural-urban income gaps; by 2024 rural credit support rose ~12% provincially, increasing the bank's agri-loan book but compressing NIMs in those portfolios.

Such mandates boost the bank’s social standing and regulatory goodwill but raise operating costs and lower segment ROA; agricultural lending typically yields 1–2 percentage points below corporate rates, straining profitability amid rising compliance expenses.

Balancing mandated social objectives with commercial returns remains a persistent management challenge, as sustaining mandated interest concessions while meeting 2024–25 capital and NPL targets requires targeted subsidies or cross-subsidization strategies.

- Rural credit growth ~12% (2024 provincial data)

- Agricultural lending yields 1–2 ppt below corporate rates

- Mandates increase OPEX and compress ROA/NIM

- Requires subsidies or cross-subsidization to protect capital ratios

Local Government Influence

As a regional commercial bank, Bank of Lanzhou remains strongly influenced by Lanzhou municipal and Gansu provincial governments; about 38% of its corporate loan book (2024) is tied to state-owned enterprises, linking the bank's strategy to local fiscal priorities.

This proximity enables deep market penetration but raises conflict-of-interest risks in credit assessment for government-backed projects; Gansu's 2023 fiscal deficit was 2.6% of provincial GDP, tying bank stability to regional political and fiscal health.

- 38% of corporate loans tied to SOEs (2024)

- Gansu fiscal deficit 2.6% of GDP (2023)

- High dependency on local policy for loan origination and risk tolerance

Bank of Lanzhou: SOE-heavy, infra-driven growth amid margin squeeze and higher CET1

Bank of Lanzhou gains from central western-development transfers (Gansu CNY ~120bn in 2023) and holds ~38% corporate exposure to SOEs (2024), driving >30% of corporate book into infrastructure; rural credit rose ~12% (2024) while agri-yields are 1–2 ppt below corporate rates, squeezing NIMs; intensified NFRA oversight raised CET1 targets toward ~10.5% and off-balance items ~CNY 12–15bn.

| Metric | Value |

|---|---|

| Gansu central transfers (2023) | CNY ~120bn |

| SOE share of corporate loans (2024) | ~38% |

| Infrastructure share of corporate book (2024) | >30% |

| Rural credit growth (2024) | ~12% |

| Agricultural yield gap | 1–2 ppt lower |

| CET1 target (post-2025 guidance) | ~10.5% |

| Off-balance-sheet items | CNY 12–15bn |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces uniquely influence Bank of Lanzhou, with data-backed trends, region-specific examples, and forward-looking insights to inform strategy, risk management, and investor communications.

Condenses the Bank of Lanzhou PESTLE into a concise, shareable summary that eases discussion of regulatory, economic, and technological risks during planning sessions.

Economic factors

Gansu Provincial GDP Trends

The Bank of Lanzhou's performance tracks Gansu GDP, which grew 4.8% in 2024 versus national 5.2%, still below coastal provinces but buoyed by 2024 energy output worth ¥420 billion; by Q3 2025 renewable and high-tech investment rose 18% YoY, opening credit avenues for the bank.

Any downturn in Gansu's industrial output—secondary sector fell 1.2% in 2024—raises the bank's NPL risk (regional NPL ratio ~2.9% in 2024); close monitoring of local PMI, fiscal transfers, and energy capex is essential to adjust risk appetite and capital allocation.

Interest Rate Environment

The People's Bank of China eased policy in 2024-25, pushing the Loan Prime Rate down to 3.65% (1Y LPR, Apr 2025), compressing regional net interest margins—China's small banks saw NIMs fall toward 1.3%–1.6% in 2024.

Bank of Lanzhou must optimize liability mix—shift to low-cost current/deposit balances and wholesale funding—while boosting fee income (wealth management, transaction fees) to offset shrinking loan-deposit spreads.

Deposit competition remains intense; retail rates rose ~30–50 bps in 2024 in many provinces, forcing higher funding costs; flexible pricing and dynamic repricing are required to protect profitability amid economic volatility.

Local Government Debt Exposure

The high stock of LGFV debt in Northwest China—estimated at over CNY 3.2 trillion in 2024 for provincial and municipal vehicles—creates a material credit risk for Bank of Lanzhou; concentrated exposure could trigger defaults or forced restructurings. Beijing’s debt-for-bond swaps reducing coupon costs (average swap yields fell from ~6.8% to ~4.2% in 2024) compress projected interest income. Rigorous stress tests and greater loan diversification are essential to absorb regional fiscal shocks.

SME Sector Resilience

Small and medium-sized enterprises account for roughly 65% of Lanzhou’s employment and 58% of local GDP, making them primary borrowers for Bank of Lanzhou’s commercial loan book.

Economic swings and 2023–2025 supply-chain disruptions raised SME nonperforming loan rates to about 2.9% regionally, increasing the bank’s credit risk exposure.

Government support programs and the bank’s digital lending platforms have expanded SME loan outreach by ~18% YoY, aiding recovery and underwriting efficiency.

The bank’s SME credit assessment accuracy—measured by default prediction AUC—directly influences asset quality and provisioning levels.

- SMEs: ~65% employment, ~58% GDP

- Regional SME NPLs: ~2.9% (2023–25)

- Digital lending growth: ~18% YoY

- Credit model performance drives provisioning and asset quality

Inflation and Consumer Spending

Fluctuating 2025 inflation—projected at 2.8–3.6% in Gansu province as of Q1 2025—erodes retail customers’ purchasing power and raises personal loan delinquency risk, while rising food and energy prices cut discretionary savings and slow deposit growth.

Conversely, if inflation stabilizes near 3% consumers are likelier to borrow for mortgages and consumption; Bank of Lanzhou must monitor CPI, wage growth, and unemployment to adjust wealth management and consumer credit offerings.

- CPI Gansu Q1 2025: ~3.2%

- Household savings rate trend: downward vs 2024

- Personal loan delinquency sensitive to real wage changes

Gansu 2024: 4.8% GDP, rising SME digital lending, NW LGFV debt ¥3.2tn+; CPI 3.2%

Gansu GDP grew 4.8% in 2024; 1Y LPR 3.65% (Apr 2025); regional NPLs ~2.9%; LGFV debt NW China >CNY3.2tn (2024); SME share: 65% employment, 58% GDP; digital SME lending +18% YoY; Gansu CPI Q1 2025 ~3.2%.

| Metric | Value |

|---|---|

| Gansu GDP growth (2024) | 4.8% |

| 1Y LPR (Apr 2025) | 3.65% |

| Regional NPLs | 2.9% |

| LGFV NW debt (2024) | ¥3.2tn+ |

Same Document Delivered

Bank of Lanzhou PESTLE Analysis

The preview shown here is the exact Bank of Lanzhou PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real file shown, and after payment you’ll be able to download this exact version immediately.

The content, layout, and structure visible in the preview are identical to the final deliverable, so there are no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE analysis pinpoints how regulatory shifts, regional economic trends, and digital banking innovations specifically shape Bank of Lanzhou's strategic risks and opportunities—essential reading for investors and strategists. Buy the full report to access data-driven insights, ready-to-use recommendations, and editable charts to inform your next move.

Political factors

Western Development Strategy

Bank of Lanzhou benefits from Beijing’s Great Western Development Strategy, which since 2015 has directed over CNY 1.8 trillion to western infrastructure; Gansu received CNY ~120 billion in central transfers in 2023, boosting regional credit demand.

As a leading regional lender, the bank aligns lending with state mandates to secure preferential access to large projects, capturing a growing share of provincial infrastructure loans (estimated >30% of its corporate book in 2024).

Political alignment ensures steady institutional business but raises concentration risk: exposure to state-directed investment could amplify losses if policy priorities shift, with non-performing loans in infrastructure-sensitive sectors up 0.6 ppt in 2024.

Belt and Road Initiative Integration

Lanzhou, as a key logistics hub on the Silk Road Economic Belt, positions Bank of Lanzhou to capture cross-border trade finance—Gansu handled 2024 trade flows of about $12.6 billion with Central Asia, boosting demand for letters of credit and supply-chain financing.

Government investments—Gansu’s infrastructure spending rose 8.2% in 2023–24—spur need for FX services and syndicated loans as firms expand into Central Asian markets.

The bank must manage geopolitical risks from tariffs and sanctions while aligning with provincial goals to be a transit powerhouse; success hinges on maintained relationships with local authorities and national trade bodies such as China Council for the Promotion of International Trade.

Regulatory Oversight and Stability

By end-2025 the National Financial Regulatory Administration intensified oversight of regional banks to curb local-debt systemic risk, prompting Bank of Lanzhou to undergo stricter inspections of capital adequacy—notably CET1 targets rising toward 10.5%—and transparency of off-balance-sheet items totaling about CNY 12–15 billion.

Rural Revitalization Mandates

Chinese rural revitalization drives compel Bank of Lanzhou to extend low-interest credit to agriculture and cooperatives, aligning with central targets to halve rural-urban income gaps; by 2024 rural credit support rose ~12% provincially, increasing the bank's agri-loan book but compressing NIMs in those portfolios.

Such mandates boost the bank’s social standing and regulatory goodwill but raise operating costs and lower segment ROA; agricultural lending typically yields 1–2 percentage points below corporate rates, straining profitability amid rising compliance expenses.

Balancing mandated social objectives with commercial returns remains a persistent management challenge, as sustaining mandated interest concessions while meeting 2024–25 capital and NPL targets requires targeted subsidies or cross-subsidization strategies.

- Rural credit growth ~12% (2024 provincial data)

- Agricultural lending yields 1–2 ppt below corporate rates

- Mandates increase OPEX and compress ROA/NIM

- Requires subsidies or cross-subsidization to protect capital ratios

Local Government Influence

As a regional commercial bank, Bank of Lanzhou remains strongly influenced by Lanzhou municipal and Gansu provincial governments; about 38% of its corporate loan book (2024) is tied to state-owned enterprises, linking the bank's strategy to local fiscal priorities.

This proximity enables deep market penetration but raises conflict-of-interest risks in credit assessment for government-backed projects; Gansu's 2023 fiscal deficit was 2.6% of provincial GDP, tying bank stability to regional political and fiscal health.

- 38% of corporate loans tied to SOEs (2024)

- Gansu fiscal deficit 2.6% of GDP (2023)

- High dependency on local policy for loan origination and risk tolerance

Bank of Lanzhou: SOE-heavy, infra-driven growth amid margin squeeze and higher CET1

Bank of Lanzhou gains from central western-development transfers (Gansu CNY ~120bn in 2023) and holds ~38% corporate exposure to SOEs (2024), driving >30% of corporate book into infrastructure; rural credit rose ~12% (2024) while agri-yields are 1–2 ppt below corporate rates, squeezing NIMs; intensified NFRA oversight raised CET1 targets toward ~10.5% and off-balance items ~CNY 12–15bn.

| Metric | Value |

|---|---|

| Gansu central transfers (2023) | CNY ~120bn |

| SOE share of corporate loans (2024) | ~38% |

| Infrastructure share of corporate book (2024) | >30% |

| Rural credit growth (2024) | ~12% |

| Agricultural yield gap | 1–2 ppt lower |

| CET1 target (post-2025 guidance) | ~10.5% |

| Off-balance-sheet items | CNY 12–15bn |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces uniquely influence Bank of Lanzhou, with data-backed trends, region-specific examples, and forward-looking insights to inform strategy, risk management, and investor communications.

Condenses the Bank of Lanzhou PESTLE into a concise, shareable summary that eases discussion of regulatory, economic, and technological risks during planning sessions.

Economic factors

Gansu Provincial GDP Trends

The Bank of Lanzhou's performance tracks Gansu GDP, which grew 4.8% in 2024 versus national 5.2%, still below coastal provinces but buoyed by 2024 energy output worth ¥420 billion; by Q3 2025 renewable and high-tech investment rose 18% YoY, opening credit avenues for the bank.

Any downturn in Gansu's industrial output—secondary sector fell 1.2% in 2024—raises the bank's NPL risk (regional NPL ratio ~2.9% in 2024); close monitoring of local PMI, fiscal transfers, and energy capex is essential to adjust risk appetite and capital allocation.

Interest Rate Environment

The People's Bank of China eased policy in 2024-25, pushing the Loan Prime Rate down to 3.65% (1Y LPR, Apr 2025), compressing regional net interest margins—China's small banks saw NIMs fall toward 1.3%–1.6% in 2024.

Bank of Lanzhou must optimize liability mix—shift to low-cost current/deposit balances and wholesale funding—while boosting fee income (wealth management, transaction fees) to offset shrinking loan-deposit spreads.

Deposit competition remains intense; retail rates rose ~30–50 bps in 2024 in many provinces, forcing higher funding costs; flexible pricing and dynamic repricing are required to protect profitability amid economic volatility.

Local Government Debt Exposure

The high stock of LGFV debt in Northwest China—estimated at over CNY 3.2 trillion in 2024 for provincial and municipal vehicles—creates a material credit risk for Bank of Lanzhou; concentrated exposure could trigger defaults or forced restructurings. Beijing’s debt-for-bond swaps reducing coupon costs (average swap yields fell from ~6.8% to ~4.2% in 2024) compress projected interest income. Rigorous stress tests and greater loan diversification are essential to absorb regional fiscal shocks.

SME Sector Resilience

Small and medium-sized enterprises account for roughly 65% of Lanzhou’s employment and 58% of local GDP, making them primary borrowers for Bank of Lanzhou’s commercial loan book.

Economic swings and 2023–2025 supply-chain disruptions raised SME nonperforming loan rates to about 2.9% regionally, increasing the bank’s credit risk exposure.

Government support programs and the bank’s digital lending platforms have expanded SME loan outreach by ~18% YoY, aiding recovery and underwriting efficiency.

The bank’s SME credit assessment accuracy—measured by default prediction AUC—directly influences asset quality and provisioning levels.

- SMEs: ~65% employment, ~58% GDP

- Regional SME NPLs: ~2.9% (2023–25)

- Digital lending growth: ~18% YoY

- Credit model performance drives provisioning and asset quality

Inflation and Consumer Spending

Fluctuating 2025 inflation—projected at 2.8–3.6% in Gansu province as of Q1 2025—erodes retail customers’ purchasing power and raises personal loan delinquency risk, while rising food and energy prices cut discretionary savings and slow deposit growth.

Conversely, if inflation stabilizes near 3% consumers are likelier to borrow for mortgages and consumption; Bank of Lanzhou must monitor CPI, wage growth, and unemployment to adjust wealth management and consumer credit offerings.

- CPI Gansu Q1 2025: ~3.2%

- Household savings rate trend: downward vs 2024

- Personal loan delinquency sensitive to real wage changes

Gansu 2024: 4.8% GDP, rising SME digital lending, NW LGFV debt ¥3.2tn+; CPI 3.2%

Gansu GDP grew 4.8% in 2024; 1Y LPR 3.65% (Apr 2025); regional NPLs ~2.9%; LGFV debt NW China >CNY3.2tn (2024); SME share: 65% employment, 58% GDP; digital SME lending +18% YoY; Gansu CPI Q1 2025 ~3.2%.

| Metric | Value |

|---|---|

| Gansu GDP growth (2024) | 4.8% |

| 1Y LPR (Apr 2025) | 3.65% |

| Regional NPLs | 2.9% |

| LGFV NW debt (2024) | ¥3.2tn+ |

Same Document Delivered

Bank of Lanzhou PESTLE Analysis

The preview shown here is the exact Bank of Lanzhou PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real file shown, and after payment you’ll be able to download this exact version immediately.

The content, layout, and structure visible in the preview are identical to the final deliverable, so there are no surprises.