Bank of Maharashtra Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

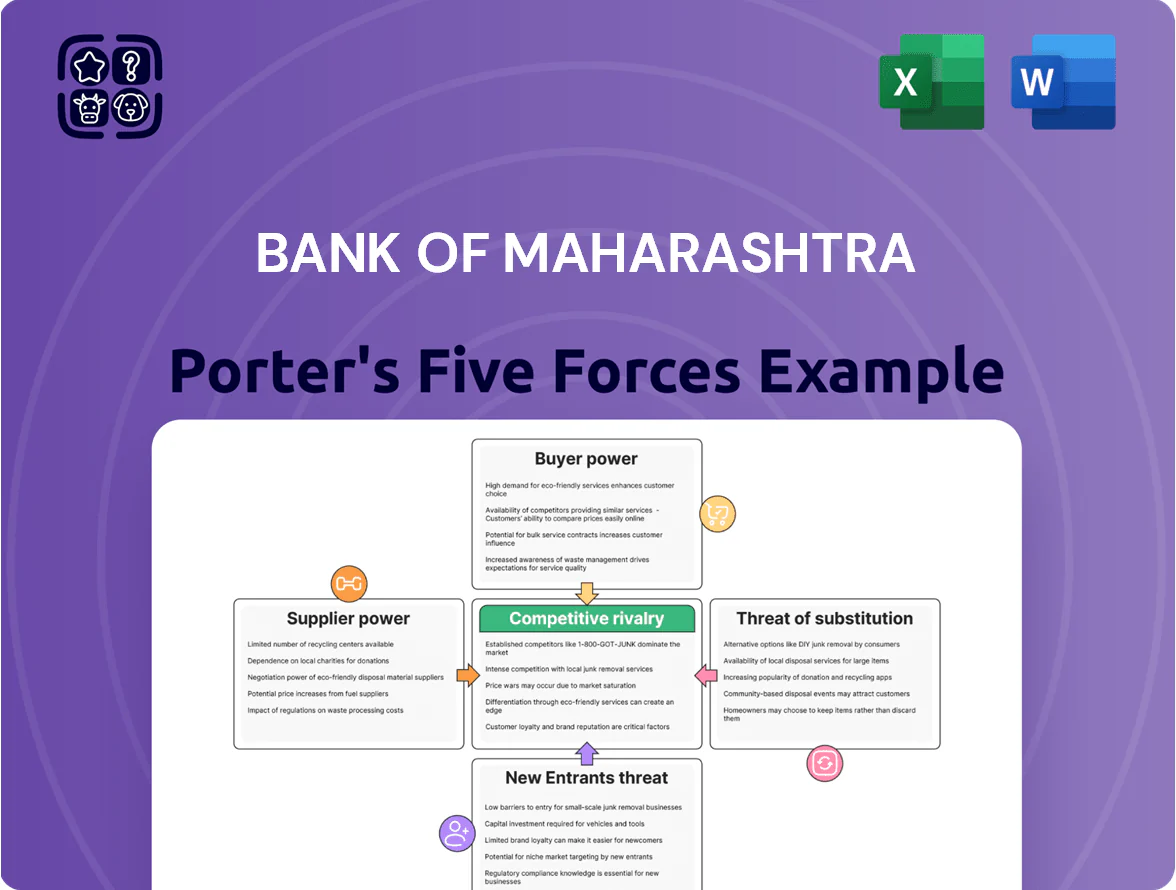

Bank of Maharashtra faces moderate buyer power, intense rivalry among public and private peers, and evolving regulatory pressures that shape margins and growth—while digital entrants and fintechs raise the threat of substitution.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank of Maharashtra’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

CASA Deposit Base Sensitivity

Individual and institutional depositors are the bank’s main capital suppliers; by end-2025 CASA (current and savings accounts) formed about 38% of Bank of Maharashtra’s deposits, keeping supplier power moderate as depositors demand higher rates amid 6–7% inflation.

To stem outflows—retail movement to 8–9% fixed deposits or higher-yield mutual funds—Bank of Maharashtra needs competitive savings/term rates and active liability mixes; a 50–100 bps rate gap would likely accelerate migration to private banks and NBFIs.

Regulatory Influence of RBI

The Reserve Bank of India (RBI) is a primary supplier of liquidity and rules, with repo rate at 6.50% and CRR at 4.00% as of Dec 2025, directly constraining Bank of Maharashtra’s funding costs and lending margins.

RBI-set SLR at 18.00% forces large government bond holdings, limiting balance-sheet flexibility; this oversight stabilizes the system but reduces the bank’s pricing and asset-allocation autonomy.

Technology and Fintech Partners

Suppliers of core banking systems and cybersecurity firms exert strong leverage over Bank of Maharashtra because their specialised platforms and threat intelligence sustain uptime and compliance; global core-banking market consolidation left top 5 vendors controlling ~60% of deployments in 2024.

With the 2025 push to digital-first services, BoM depends on these vendors for availability and rapid patching against rising Indian cyber incidents—India reported a 37% rise in banking cyberattacks in 2024—raising supplier bargaining power.

High switching costs for integrated financial software—often 12–24 months migration and >₹50–150 crore for mid-sized Indian banks—lock BoM in, giving tech partners substantial pricing and contract leverage.

Specialized Human Capital

By 2025 the demand for specialists in data analytics, risk management and digital transformation rose ~28% in Indian banking roles, boosting supplier power for Bank of Maharashtra as private banks and fintechs offer 20–40% higher pay.

High-tier hires now command premium packages and equity-like incentives, raising recruitment costs and retention risk for the bank during its modernization push.

Institutional Capital Markets

When Bank of Maharashtra raises Tier-I/II capital via equity or bonds, institutional investors — pension funds, insurance firms, mutual funds — set pricing and terms; end-2025 market yields (10-year G-Sec ~7.1%) and the bank’s CRISIL rating BBB- determine cost of capital.

Higher-quality investors may demand stricter governance or higher yields if asset quality shows stress: BoM GNPA 3.9% and CET1 ~12.8% at Sep 2025 raise negotiation leverage for suppliers.

- Institutional supply sets yield: linked to 10y G-Sec 7.1%

- Credit rating impact: BBB- implies higher spread

- Asset quality: GNPA 3.9% increases investor demands

- Governance covenants likely from large investors

Suppliers Tighten Costs: Funding, Tech & Talent Raise Pressure on Bank Margins

Suppliers exert moderate-to-strong power: depositors (CASA ~38% end‑2025) pressure rates amid 6–7% inflation; RBI liquidity tools (repo 6.50%, CRR 4.00%, SLR 18.00% as of Dec 2025) fix funding costs; tech/cyber vendors (top‑5 ~60% market share) and high‑tier talent (+28% hiring demand 2021–25; private pay +20–40%) raise switching and wage costs; investors set capital pricing vs 10y G‑Sec 7.1% and BoM BBB‑, GNPA 3.9%, CET1 12.8%.

| Metric | Value |

|---|---|

| CASA | 38% (end‑2025) |

| Repo / CRR / SLR | 6.50% / 4.00% / 18.00% (Dec 2025) |

| 10y G‑Sec | 7.1% (end‑2025) |

| Rating / GNPA / CET1 | BBB‑ / 3.9% (Sep‑2025) / 12.8% |

| Tech vendor share | Top‑5 ~60% (2024) |

| Talent demand | +28% (2021–25); pay +20–40% |

What is included in the product

Tailored Porter's Five Forces analysis for Bank of Maharashtra uncovering competitive intensity, customer and supplier bargaining power, threat of new entrants and substitutes, and strategic barriers that protect or expose the bank's market position.

A concise Porter's Five Forces snapshot for Bank of Maharashtra—quickly highlights competitive pressures, regulatory risks, and customer bargaining power to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Low Switching Costs in Digital Banking

By 2025, UPI transactions exceeded 100 billion annually in India, and interoperable banking apps let customers move funds instantly, so retail clients can switch banks within minutes; Bank of Maharashtra faces heightened consumer bargaining power as customers chase superior digital features or lower fees. With average monthly digital transactions per user rising ~40% from 2022–25, fee sensitivity and feature-driven churn materially pressure margins and product pricing.

Information Transparency and Rate Parity

Corporate Borrower Negotiation Leverage

Large corporates and institutions wield strong bargaining power over Bank of Maharashtra, as top 100 Indian corporates account for roughly 40% of organised corporate credit demand and routinely invite bids across public and private banks to lower spreads; in 2024 the bank lost several mandates where bid spreads undercut its offer by 25–75 bps. To retain these high-value clients the bank must provide tailored treasury, working-capital and covenant-light term loans, plus relationship pricing and cash-management bundling.

Standardization of Banking Products

By late 2025 most core banking products—personal loans, mortgages, savings accounts—are commoditized, shifting power to customers who now pick banks on service quality and brand; Bank of Maharashtra (BoM) faces higher churn risk as price/differentiation matter less.

BoM must boost CRM spending—customer analytics, digital channels, and branch service—to retain clients; example: banks with top-tier CRM cut churn by ~25% and lift cross-sell rates by 15% (2024–25 industry averages).

- Commoditization by 2025

- Buyer power rises vs price/differentiation

- CRM investment needed to reduce ~25% churn

- Cross-sell lift ~15% with strong CRM

Demand for Integrated Financial Ecosystems

Modern customers expect Bank of Maharashtra to offer a single digital ecosystem covering insurance, investments, and tax planning; 2025 surveys show 62% of Indian retail banking customers prefer unified platforms and 48% would switch banks for better integration.

Buyers now demand seamless APIs, robo-advisory, and bundled services beyond lending; failure to deliver risks migration to private peers—private banks grew digital account share by 7 percentage points to 54% in 2024–25.

- 62% prefer unified platforms (2025)

- 48% willing to switch for integration

- Private banks digital share +7 pp to 54% (2024–25)

UPI boom boosts customer power—banks must match rates and invest in CRM to cut churn

Customers hold high bargaining power vs Bank of Maharashtra: UPI >100B transactions (2025), 62% prefer unified platforms, 48% would switch for integration; price sensitivity forces rate matching within ±10 bps and churn rises unless CRM/digital spend cuts churn ~25% and lifts cross-sell ~15%.

| Metric | 2024–25 |

|---|---|

| UPI transactions | >100B (2025) |

| Unified platform preference | 62% |

| Switching for integration | 48% |

| Rate matching band | ±10 bps |

| Churn reduction with top CRM | ~25% |

| Cross-sell lift | ~15% |

Full Version Awaits

Bank of Maharashtra Porter's Five Forces Analysis

This preview shows the exact Bank of Maharashtra Porter’s Five Forces analysis you’ll receive upon purchase—no samples, no placeholders; the full, professionally formatted document is available for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Bank of Maharashtra faces moderate buyer power, intense rivalry among public and private peers, and evolving regulatory pressures that shape margins and growth—while digital entrants and fintechs raise the threat of substitution.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank of Maharashtra’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

CASA Deposit Base Sensitivity

Individual and institutional depositors are the bank’s main capital suppliers; by end-2025 CASA (current and savings accounts) formed about 38% of Bank of Maharashtra’s deposits, keeping supplier power moderate as depositors demand higher rates amid 6–7% inflation.

To stem outflows—retail movement to 8–9% fixed deposits or higher-yield mutual funds—Bank of Maharashtra needs competitive savings/term rates and active liability mixes; a 50–100 bps rate gap would likely accelerate migration to private banks and NBFIs.

Regulatory Influence of RBI

The Reserve Bank of India (RBI) is a primary supplier of liquidity and rules, with repo rate at 6.50% and CRR at 4.00% as of Dec 2025, directly constraining Bank of Maharashtra’s funding costs and lending margins.

RBI-set SLR at 18.00% forces large government bond holdings, limiting balance-sheet flexibility; this oversight stabilizes the system but reduces the bank’s pricing and asset-allocation autonomy.

Technology and Fintech Partners

Suppliers of core banking systems and cybersecurity firms exert strong leverage over Bank of Maharashtra because their specialised platforms and threat intelligence sustain uptime and compliance; global core-banking market consolidation left top 5 vendors controlling ~60% of deployments in 2024.

With the 2025 push to digital-first services, BoM depends on these vendors for availability and rapid patching against rising Indian cyber incidents—India reported a 37% rise in banking cyberattacks in 2024—raising supplier bargaining power.

High switching costs for integrated financial software—often 12–24 months migration and >₹50–150 crore for mid-sized Indian banks—lock BoM in, giving tech partners substantial pricing and contract leverage.

Specialized Human Capital

By 2025 the demand for specialists in data analytics, risk management and digital transformation rose ~28% in Indian banking roles, boosting supplier power for Bank of Maharashtra as private banks and fintechs offer 20–40% higher pay.

High-tier hires now command premium packages and equity-like incentives, raising recruitment costs and retention risk for the bank during its modernization push.

Institutional Capital Markets

When Bank of Maharashtra raises Tier-I/II capital via equity or bonds, institutional investors — pension funds, insurance firms, mutual funds — set pricing and terms; end-2025 market yields (10-year G-Sec ~7.1%) and the bank’s CRISIL rating BBB- determine cost of capital.

Higher-quality investors may demand stricter governance or higher yields if asset quality shows stress: BoM GNPA 3.9% and CET1 ~12.8% at Sep 2025 raise negotiation leverage for suppliers.

- Institutional supply sets yield: linked to 10y G-Sec 7.1%

- Credit rating impact: BBB- implies higher spread

- Asset quality: GNPA 3.9% increases investor demands

- Governance covenants likely from large investors

Suppliers Tighten Costs: Funding, Tech & Talent Raise Pressure on Bank Margins

Suppliers exert moderate-to-strong power: depositors (CASA ~38% end‑2025) pressure rates amid 6–7% inflation; RBI liquidity tools (repo 6.50%, CRR 4.00%, SLR 18.00% as of Dec 2025) fix funding costs; tech/cyber vendors (top‑5 ~60% market share) and high‑tier talent (+28% hiring demand 2021–25; private pay +20–40%) raise switching and wage costs; investors set capital pricing vs 10y G‑Sec 7.1% and BoM BBB‑, GNPA 3.9%, CET1 12.8%.

| Metric | Value |

|---|---|

| CASA | 38% (end‑2025) |

| Repo / CRR / SLR | 6.50% / 4.00% / 18.00% (Dec 2025) |

| 10y G‑Sec | 7.1% (end‑2025) |

| Rating / GNPA / CET1 | BBB‑ / 3.9% (Sep‑2025) / 12.8% |

| Tech vendor share | Top‑5 ~60% (2024) |

| Talent demand | +28% (2021–25); pay +20–40% |

What is included in the product

Tailored Porter's Five Forces analysis for Bank of Maharashtra uncovering competitive intensity, customer and supplier bargaining power, threat of new entrants and substitutes, and strategic barriers that protect or expose the bank's market position.

A concise Porter's Five Forces snapshot for Bank of Maharashtra—quickly highlights competitive pressures, regulatory risks, and customer bargaining power to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Low Switching Costs in Digital Banking

By 2025, UPI transactions exceeded 100 billion annually in India, and interoperable banking apps let customers move funds instantly, so retail clients can switch banks within minutes; Bank of Maharashtra faces heightened consumer bargaining power as customers chase superior digital features or lower fees. With average monthly digital transactions per user rising ~40% from 2022–25, fee sensitivity and feature-driven churn materially pressure margins and product pricing.

Information Transparency and Rate Parity

Corporate Borrower Negotiation Leverage

Large corporates and institutions wield strong bargaining power over Bank of Maharashtra, as top 100 Indian corporates account for roughly 40% of organised corporate credit demand and routinely invite bids across public and private banks to lower spreads; in 2024 the bank lost several mandates where bid spreads undercut its offer by 25–75 bps. To retain these high-value clients the bank must provide tailored treasury, working-capital and covenant-light term loans, plus relationship pricing and cash-management bundling.

Standardization of Banking Products

By late 2025 most core banking products—personal loans, mortgages, savings accounts—are commoditized, shifting power to customers who now pick banks on service quality and brand; Bank of Maharashtra (BoM) faces higher churn risk as price/differentiation matter less.

BoM must boost CRM spending—customer analytics, digital channels, and branch service—to retain clients; example: banks with top-tier CRM cut churn by ~25% and lift cross-sell rates by 15% (2024–25 industry averages).

- Commoditization by 2025

- Buyer power rises vs price/differentiation

- CRM investment needed to reduce ~25% churn

- Cross-sell lift ~15% with strong CRM

Demand for Integrated Financial Ecosystems

Modern customers expect Bank of Maharashtra to offer a single digital ecosystem covering insurance, investments, and tax planning; 2025 surveys show 62% of Indian retail banking customers prefer unified platforms and 48% would switch banks for better integration.

Buyers now demand seamless APIs, robo-advisory, and bundled services beyond lending; failure to deliver risks migration to private peers—private banks grew digital account share by 7 percentage points to 54% in 2024–25.

- 62% prefer unified platforms (2025)

- 48% willing to switch for integration

- Private banks digital share +7 pp to 54% (2024–25)

UPI boom boosts customer power—banks must match rates and invest in CRM to cut churn

Customers hold high bargaining power vs Bank of Maharashtra: UPI >100B transactions (2025), 62% prefer unified platforms, 48% would switch for integration; price sensitivity forces rate matching within ±10 bps and churn rises unless CRM/digital spend cuts churn ~25% and lifts cross-sell ~15%.

| Metric | 2024–25 |

|---|---|

| UPI transactions | >100B (2025) |

| Unified platform preference | 62% |

| Switching for integration | 48% |

| Rate matching band | ±10 bps |

| Churn reduction with top CRM | ~25% |

| Cross-sell lift | ~15% |

Full Version Awaits

Bank of Maharashtra Porter's Five Forces Analysis

This preview shows the exact Bank of Maharashtra Porter’s Five Forces analysis you’ll receive upon purchase—no samples, no placeholders; the full, professionally formatted document is available for immediate download and use.