Bank of Qingdao Business Model Canvas

Bank of Qingdao: Quick Business Model Canvas—Value, Customers & Revenue Revealed

Unlock the full strategic blueprint behind Bank of Qingdao's business model—this concise Business Model Canvas uncovers its core value propositions, customer segments, key partners, and revenue drivers to reveal how it competes and scales in China’s banking market.

Partnerships

Strategic Local Government Alliances

The bank partners closely with Qingdao municipal and Shandong provincial governments to underwrite and distribute government-backed loans—about CNY 38.6 billion in public-sector credit and CNY 12.4 billion in municipal deposits managed in 2024—supporting infrastructure and urban development projects. By aligning with local policy targets, Bank of Qingdao secures recurring institutional fee income and a steady flow of state-related deposits, reinforcing its role as a regional economic pillar.

Fintech and Technology Providers

Collaborations with Chinese tech firms (e.g., Tencent, Alibaba Cloud) let Bank of Qingdao embed AI, big data, and cloud; by 2024 these partnerships supported a 28% year-on-year rise in mobile transactions and helped scale Blue Ocean Finance, which served ~1.2 million users in 2024. Such alliances cut manual processing by ~35% via automation, keeping the bank competitive against digital-first challengers.

Interbank and Financial Institution Partners

Bank of Qingdao works with domestic and international banks to support interbank lending, FX swaps, and trade finance, securing liquidity lines that covered about CNY 120 billion in 2024 and reduced short-term funding gaps by 18% year-on-year. These partners let the bank offer diversified investment products and join syndicated loans—co-lending with national banks on projects exceeding CNY 10 billion in Shandong, including 2024 infrastructure financings.

Strategic Corporate Alliances

By allying with regional industrial groups and supply‑chain leaders, Bank of Qingdao taps ecosystems of 1,200+ vendors and distributors, enabling tailored supply‑chain finance that cut receivables days by ~18% and lower default rates vs SME loans.

These partnerships let the bank penetrate niche sectors (manufacturing, logistics), boost fee income, and deepen C‑level relationships for longer client lifetime value.

- Access: 1,200+ vendors/distributors

- Impact: receivables days −18%

- Risk: default rates below SME average

- Focus: manufacturing, logistics niches

- Benefit: higher fee income, longer CLV

Regulatory and Central Bank Bodies

Proactive engagement with the People’s Bank of China and the National Financial Regulatory Administration lets Bank of Qingdao adapt ahead of policy shifts that affect its reserve requirements and loan-to-deposit ratios; in 2024 China cut the reserve requirement ratio by 25 bps, easing liquidity pressure on regional banks.

These regulators set capital adequacy and lending caps—BoQ monitors CET1 and CAR targets (BoQ reported a 2024 CET1 ratio of ~9.8%) and holds regular dialogues to manage reform risks and preserve stability.

- Keeps CET1/CAR aligned with regulator guidance

- Responds quickly to RRR and policy rate moves (e.g., 25 bps RRR cut, 2024)

- Reduces compliance lag via frequent regulator meetings

Strategic partners drive liquidity, tech growth and 18% working‑capital gains in 2024

Key partners: Qingdao/Shandong governments (CNY 38.6bn public credit, CNY 12.4bn municipal deposits in 2024), Tencent/Alibaba Cloud (28% mobile tx growth, Blue Ocean 1.2m users, 35% automation cut), interbank lines (CNY 120bn liquidity, −18% funding gap), 1,200+ supply‑chain partners (receivables −18%).

| Partner | 2024 metric |

|---|---|

| Governments | CNY 38.6bn credit; CNY 12.4bn deposits |

| Tech firms | 28% mobile growth; 1.2m users |

| Interbank | CNY 120bn lines; −18% gap |

| Supply‑chain | 1,200+ vendors; receivables −18% |

What is included in the product

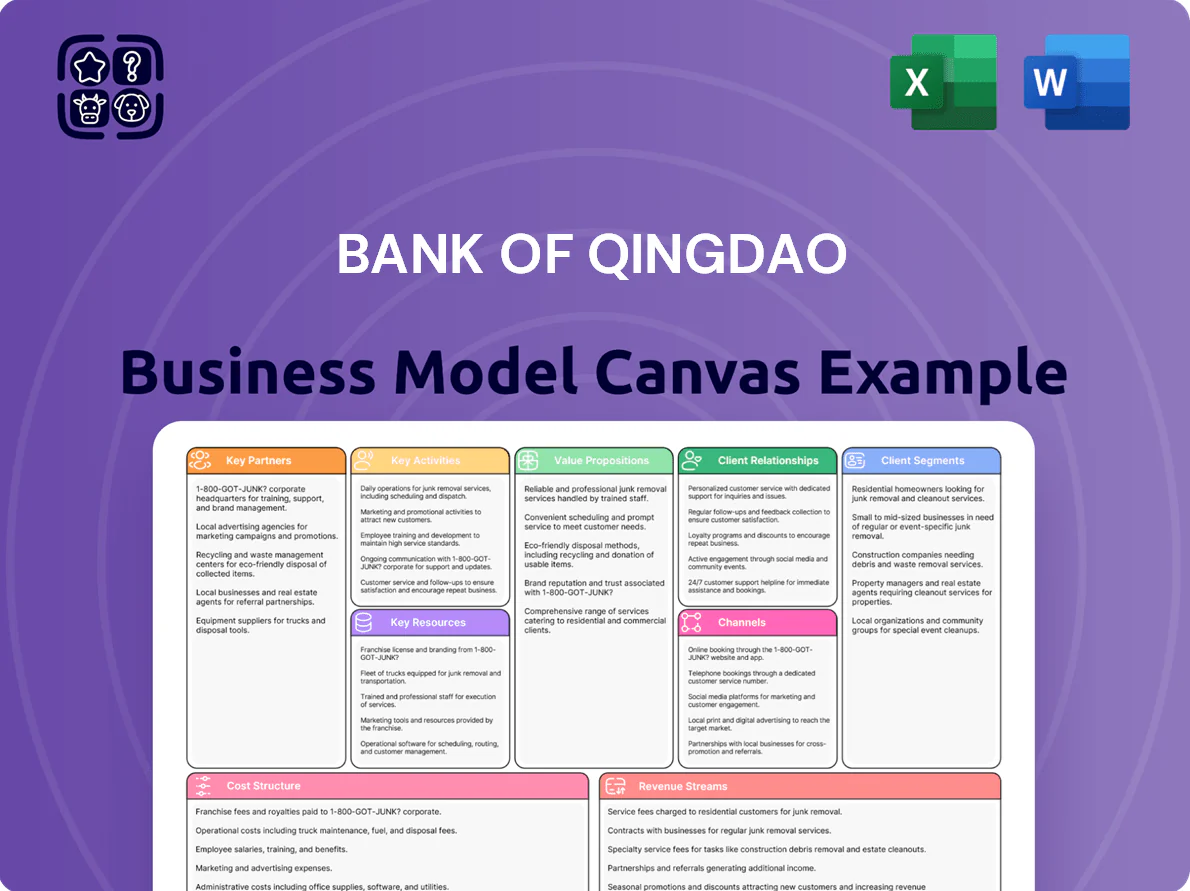

A concise, pre-written Business Model Canvas for Bank of Qingdao detailing its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—reflecting real-world operations, competitive advantages, SWOT-linked insights, and polished narrative for presentations, investor discussions, and strategic decision-making.

High-level view of Bank of Qingdao’s business model with editable cells, condensing its retail, corporate, and digital banking strategies into a single pain-point relieving snapshot for quick analysis and decision-making.

Activities

Credit Granting and Loan Management

The bank conducts rigorous assessment and distribution of credit to corporates, SMEs, and retail borrowers, handling end-to-end loan lifecycles from application and risk underwriting to monitoring and repayment; as of 2024 Bank of Qingdao reported a gross loan balance of CNY 481.2 billion and NPL ratio of 1.22% (2024 annual report). Effective loan-book management sustains asset quality and protects net interest margin, which stood at 2.15% in 2024.

Digital Banking and Tech Innovation

Bank of Qingdao invests in continuous digital platform upgrades—mobile apps and web banking—allocating roughly CNY 450–500 million in IT capex in 2024 to boost UX, add wealth-management and payment features, and cut branch costs; cybersecurity enhancements follow 2023’s 28% rise in detected threats, and digital users grew 17% Y/Y to 6.8 million in 2024, driving fee income and lowering per-customer branch overhead.

Wealth Management and Investment Services

Bank of Qingdao designs, markets, and manages investment products from conservative wealth schemes to aggressive capital-market instruments, using market analysis and asset-allocation models to target competitive returns for retail and institutional clients.

Professional fund management produced fee income of RMB 3.2 billion in 2024, about 14% of non-interest income, and helps diversify revenue and boost AUM, which stood at RMB 420 billion at end-2024.

Risk Assessment and Compliance Monitoring

Dedicated teams at Bank of Qingdao run continuous credit, market, and operational risk monitoring, using advanced analytics that cut nonperforming loan (NPL) exposure—NPL ratio 2024: 1.12%—and protect capital and reputation.

They deploy predictive models for default probability and enforce AML and KYC rules; strong internal controls supported regulatory capital: CET1 ratio 2024: 11.8%.

- Continuous monitoring of credit, market, operational risk

- Predictive analytics to lower defaults (NPL 1.12% in 2024)

- Strict AML/KYC enforcement on all transactions

- Robust internal controls; CET1 11.8% in 2024

Customer Acquisition and Relationship Management

The bank runs targeted marketing and personalized outreach to expand customers across retail, SME and corporates, using relationship managers for HNW (high-net-worth) and corporate clients; in 2024 Bank of Qingdao reported a 7.8% YoY retail customer growth and a 12% increase in wealth-management AUM to RMB 148.3 billion.

Focus on satisfaction and cross-selling lifts lifetime value and retention—customer NPS rose to 28 in 2024 and income from fee-based products grew 15% YoY, supporting higher per-client ROA.

- Retail growth 7.8% (2024)

- Wealth AUM RMB 148.3bn (2024)

- NPS 28 (2024)

- Fee-income +15% YoY (2024)

Robust loan growth, digital surge and strong capital: 2024 highlights

Key activities: credit origination and loan management (gross loans CNY 481.2bn; NPL 1.22% in 2024), digital platform and cybersecurity investment (IT capex CNY 450–500m; 6.8m digital users, +17% Y/Y), wealth product management (AUM CNY 420bn; fee income CNY 3.2bn), and risk/control functions (CET1 11.8%).

| Metric | 2024 |

|---|---|

| Gross loans | CNY 481.2bn |

| NPL ratio | 1.22% |

| IT capex | CNY 450–500m |

| Digital users | 6.8m (+17% Y/Y) |

| AUM | CNY 420bn |

| Fee income (funds) | CNY 3.2bn |

| CET1 | 11.8% |

What You See Is What You Get

Business Model Canvas

The preview shown is the actual Bank of Qingdao Business Model Canvas document, not a sample or mockup; it reflects the exact content and layout you will receive after purchase.

After completing your order you’ll download this same ready-to-edit file—fully formatted and complete—so there are no surprises and you can use it immediately.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bank of Qingdao: Quick Business Model Canvas—Value, Customers & Revenue Revealed

Unlock the full strategic blueprint behind Bank of Qingdao's business model—this concise Business Model Canvas uncovers its core value propositions, customer segments, key partners, and revenue drivers to reveal how it competes and scales in China’s banking market.

Partnerships

Strategic Local Government Alliances

The bank partners closely with Qingdao municipal and Shandong provincial governments to underwrite and distribute government-backed loans—about CNY 38.6 billion in public-sector credit and CNY 12.4 billion in municipal deposits managed in 2024—supporting infrastructure and urban development projects. By aligning with local policy targets, Bank of Qingdao secures recurring institutional fee income and a steady flow of state-related deposits, reinforcing its role as a regional economic pillar.

Fintech and Technology Providers

Collaborations with Chinese tech firms (e.g., Tencent, Alibaba Cloud) let Bank of Qingdao embed AI, big data, and cloud; by 2024 these partnerships supported a 28% year-on-year rise in mobile transactions and helped scale Blue Ocean Finance, which served ~1.2 million users in 2024. Such alliances cut manual processing by ~35% via automation, keeping the bank competitive against digital-first challengers.

Interbank and Financial Institution Partners

Bank of Qingdao works with domestic and international banks to support interbank lending, FX swaps, and trade finance, securing liquidity lines that covered about CNY 120 billion in 2024 and reduced short-term funding gaps by 18% year-on-year. These partners let the bank offer diversified investment products and join syndicated loans—co-lending with national banks on projects exceeding CNY 10 billion in Shandong, including 2024 infrastructure financings.

Strategic Corporate Alliances

By allying with regional industrial groups and supply‑chain leaders, Bank of Qingdao taps ecosystems of 1,200+ vendors and distributors, enabling tailored supply‑chain finance that cut receivables days by ~18% and lower default rates vs SME loans.

These partnerships let the bank penetrate niche sectors (manufacturing, logistics), boost fee income, and deepen C‑level relationships for longer client lifetime value.

- Access: 1,200+ vendors/distributors

- Impact: receivables days −18%

- Risk: default rates below SME average

- Focus: manufacturing, logistics niches

- Benefit: higher fee income, longer CLV

Regulatory and Central Bank Bodies

Proactive engagement with the People’s Bank of China and the National Financial Regulatory Administration lets Bank of Qingdao adapt ahead of policy shifts that affect its reserve requirements and loan-to-deposit ratios; in 2024 China cut the reserve requirement ratio by 25 bps, easing liquidity pressure on regional banks.

These regulators set capital adequacy and lending caps—BoQ monitors CET1 and CAR targets (BoQ reported a 2024 CET1 ratio of ~9.8%) and holds regular dialogues to manage reform risks and preserve stability.

- Keeps CET1/CAR aligned with regulator guidance

- Responds quickly to RRR and policy rate moves (e.g., 25 bps RRR cut, 2024)

- Reduces compliance lag via frequent regulator meetings

Strategic partners drive liquidity, tech growth and 18% working‑capital gains in 2024

Key partners: Qingdao/Shandong governments (CNY 38.6bn public credit, CNY 12.4bn municipal deposits in 2024), Tencent/Alibaba Cloud (28% mobile tx growth, Blue Ocean 1.2m users, 35% automation cut), interbank lines (CNY 120bn liquidity, −18% funding gap), 1,200+ supply‑chain partners (receivables −18%).

| Partner | 2024 metric |

|---|---|

| Governments | CNY 38.6bn credit; CNY 12.4bn deposits |

| Tech firms | 28% mobile growth; 1.2m users |

| Interbank | CNY 120bn lines; −18% gap |

| Supply‑chain | 1,200+ vendors; receivables −18% |

What is included in the product

A concise, pre-written Business Model Canvas for Bank of Qingdao detailing its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—reflecting real-world operations, competitive advantages, SWOT-linked insights, and polished narrative for presentations, investor discussions, and strategic decision-making.

High-level view of Bank of Qingdao’s business model with editable cells, condensing its retail, corporate, and digital banking strategies into a single pain-point relieving snapshot for quick analysis and decision-making.

Activities

Credit Granting and Loan Management

The bank conducts rigorous assessment and distribution of credit to corporates, SMEs, and retail borrowers, handling end-to-end loan lifecycles from application and risk underwriting to monitoring and repayment; as of 2024 Bank of Qingdao reported a gross loan balance of CNY 481.2 billion and NPL ratio of 1.22% (2024 annual report). Effective loan-book management sustains asset quality and protects net interest margin, which stood at 2.15% in 2024.

Digital Banking and Tech Innovation

Bank of Qingdao invests in continuous digital platform upgrades—mobile apps and web banking—allocating roughly CNY 450–500 million in IT capex in 2024 to boost UX, add wealth-management and payment features, and cut branch costs; cybersecurity enhancements follow 2023’s 28% rise in detected threats, and digital users grew 17% Y/Y to 6.8 million in 2024, driving fee income and lowering per-customer branch overhead.

Wealth Management and Investment Services

Bank of Qingdao designs, markets, and manages investment products from conservative wealth schemes to aggressive capital-market instruments, using market analysis and asset-allocation models to target competitive returns for retail and institutional clients.

Professional fund management produced fee income of RMB 3.2 billion in 2024, about 14% of non-interest income, and helps diversify revenue and boost AUM, which stood at RMB 420 billion at end-2024.

Risk Assessment and Compliance Monitoring

Dedicated teams at Bank of Qingdao run continuous credit, market, and operational risk monitoring, using advanced analytics that cut nonperforming loan (NPL) exposure—NPL ratio 2024: 1.12%—and protect capital and reputation.

They deploy predictive models for default probability and enforce AML and KYC rules; strong internal controls supported regulatory capital: CET1 ratio 2024: 11.8%.

- Continuous monitoring of credit, market, operational risk

- Predictive analytics to lower defaults (NPL 1.12% in 2024)

- Strict AML/KYC enforcement on all transactions

- Robust internal controls; CET1 11.8% in 2024

Customer Acquisition and Relationship Management

The bank runs targeted marketing and personalized outreach to expand customers across retail, SME and corporates, using relationship managers for HNW (high-net-worth) and corporate clients; in 2024 Bank of Qingdao reported a 7.8% YoY retail customer growth and a 12% increase in wealth-management AUM to RMB 148.3 billion.

Focus on satisfaction and cross-selling lifts lifetime value and retention—customer NPS rose to 28 in 2024 and income from fee-based products grew 15% YoY, supporting higher per-client ROA.

- Retail growth 7.8% (2024)

- Wealth AUM RMB 148.3bn (2024)

- NPS 28 (2024)

- Fee-income +15% YoY (2024)

Robust loan growth, digital surge and strong capital: 2024 highlights

Key activities: credit origination and loan management (gross loans CNY 481.2bn; NPL 1.22% in 2024), digital platform and cybersecurity investment (IT capex CNY 450–500m; 6.8m digital users, +17% Y/Y), wealth product management (AUM CNY 420bn; fee income CNY 3.2bn), and risk/control functions (CET1 11.8%).

| Metric | 2024 |

|---|---|

| Gross loans | CNY 481.2bn |

| NPL ratio | 1.22% |

| IT capex | CNY 450–500m |

| Digital users | 6.8m (+17% Y/Y) |

| AUM | CNY 420bn |

| Fee income (funds) | CNY 3.2bn |

| CET1 | 11.8% |

What You See Is What You Get

Business Model Canvas

The preview shown is the actual Bank of Qingdao Business Model Canvas document, not a sample or mockup; it reflects the exact content and layout you will receive after purchase.

After completing your order you’ll download this same ready-to-edit file—fully formatted and complete—so there are no surprises and you can use it immediately.