BankUnited Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

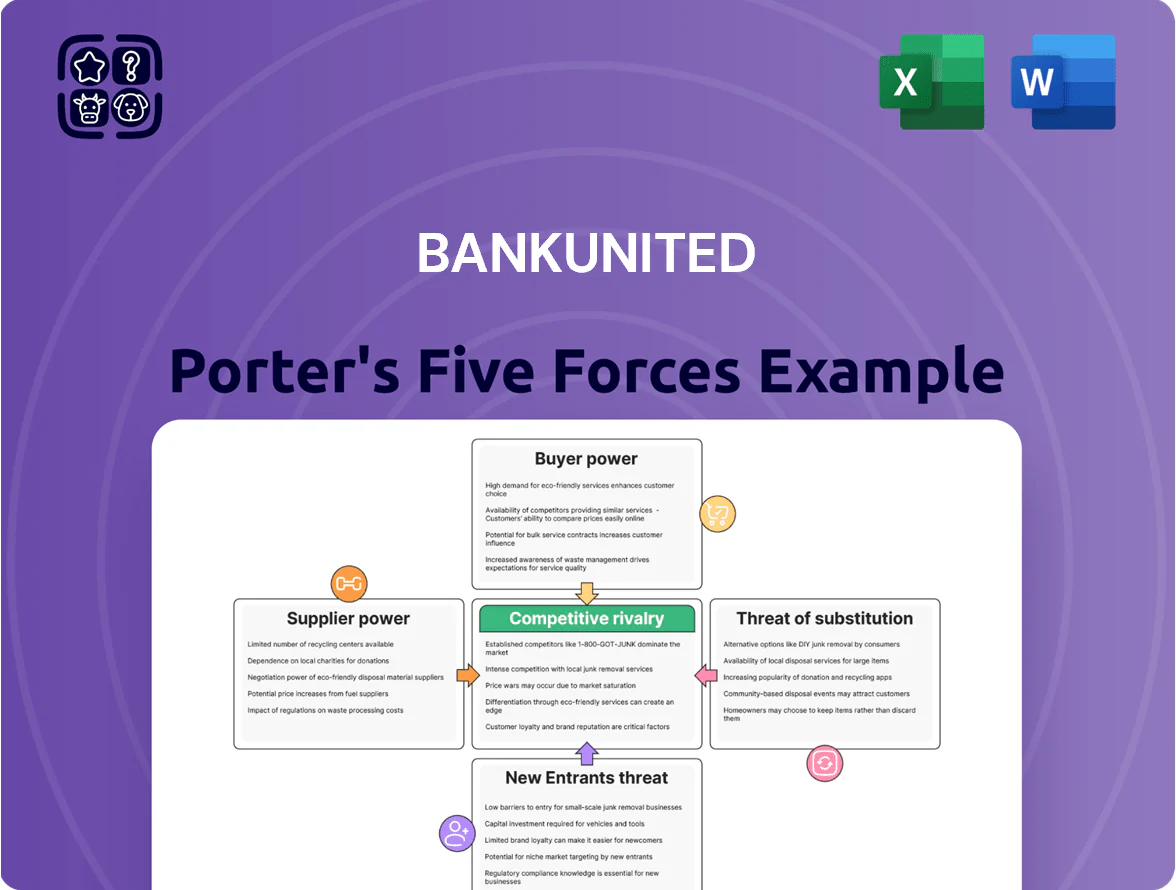

BankUnited faces moderate competitive pressure: strong regional rivals and regulatory costs limit margins, while a focused deposit base and digital initiatives bolster customer retention.

This snapshot highlights buyer sensitivity to rates and moderate threat of substitutes from fintechs; supply-side risks are muted by diversified funding, but new entrants could disrupt niche segments.

This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy tailored to BankUnited.

Suppliers Bargaining Power

Cost of Financial Capital

The primary suppliers for BankUnited are depositors and wholesale funding providers such as the Federal Home Loan Bank; as of Q4 2025, deposits funded ~78% of assets while FHLB borrowings stood at $6.2 billion, giving suppliers moderate-to-high leverage. Elevated rate expectations in 2025 pushed average deposit betas toward 55–65%, forcing BankUnited to lift yields and compress net interest margin to about 2.45% in Q4 2025. Competitive liquidity markets and tight secondary funding raise replacement costs and shorten tenor, increasing funding risk. If core deposit retention slips, margin and ROA could decline materially.

Technology and Fintech Vendors

BankUnited depends on third-party core-banking, cybersecurity, and digital-platform vendors, creating high supplier power since switching core systems often costs tens of millions and 12–24 months; major players like FIS, Fiserv, and Jack Henry dominate ~70% of US bank core market (2024 estimate).

Regulatory and Compliance Entities

Regulatory bodies like the FDIC and OCC act as non-market suppliers of the legal framework and mandates BankUnited must follow, forcing non‑negotiable compliance spending—BankUnited reported $218 million in regulatory and legal expenses in 2024, a material fixed cost. Changes in capital ratios (e.g., higher CET1 targets) or tighter FDIC/OCC exams reduce strategic flexibility and raise funding costs; a 100 bps capital hike can cut 2025 ROE by ~1.2 percentage points.

Skilled Labor and Executive Talent

The market for specialized commercial-lending and risk-management professionals in Miami and New York is tight; BankUnited competes with JPMorgan Chase, Bank of America, and regional peers, pushing median commercial-banking base salaries up ~12–18% vs. national averages (2024 Bureau of Labor Statistics and industry surveys).

Scarcity of experienced commercial bankers in Florida and NY raises workforce bargaining power, increasing total compensation costs and retention spend; BankUnited’s 2024 compensation-to-revenue ratio rose ~1.5 percentage points year-over-year.

Credit Rating Agencies

Credit rating agencies like Moody’s and S&P set ratings that directly affect BankUnited’s institutional borrowing costs; as of Q4 2025, a one-notch downgrade typically raises senior unsecured spreads by ~60–120 bps, raising funding costs materially.

The oligopolistic market for ratings means their opinions strongly constrain BankUnited’s capital-market access; a downgrade would shrink strategic flexibility by increasing cost of funds and limiting repo and bond issuance capacity.

- Moody’s/S&P concentration: 70–80% market share

- One-notch downgrade ≈ +60–120 bps funding spread

- Higher spreads reduce ROE and limit bond issuance

High supplier power squeezes margins: deposits, FHLB, vendors & regulator costs

Suppliers exert moderate-to-high power: depositors funded ~78% of assets (Q4 2025) and FHLB borrowings were $6.2B, forcing deposit betas to ~55–65% and NIM to ~2.45% (Q4 2025); core-banking vendors (FIS, Fiserv, Jack Henry ~70% market share) raise switching costs; regulators (FDIC/OCC) drove $218M compliance spend in 2024; ratings moves add ~60–120 bps to funding on a one-notch downgrade.

What is included in the product

Tailored Porter's Five Forces analysis for BankUnited that uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and emerging threats to its market position—ready for integration into investor decks or strategy reports.

Concise Porter's Five Forces snapshot for BankUnited—quickly assess competitive pressures and regulatory risk to inform strategic moves.

Customers Bargaining Power

Low Switching Costs for Retail Depositors

Retail depositors now shift funds quickly via apps and ACH; 2024 data shows 46% of US consumers switched primary banks or considered switching in the prior 12 months, raising customer leverage over BankUnited.

Low switching costs force BankUnited to compete on rates and UX; online banks like Ally and Marcus offered savings yields up to 4.5% in 2025, pressuring margins and retention.

Price Sensitivity in Commercial Lending

BankUnited’s commercial clients—midmarket firms and CRE borrowers—are sophisticated and often have multiple bids; 2024 LPC data shows 68% of middle-market loans saw price compression from competing offers, pressuring margins.

Borrowers use competing regional and national bank offers to push rates and covenants down; BankUnited’s 2025 Q1 commercial loan yield of ~4.2% vs. peers’ 4.0% reflects tightened spreads to stay competitive.

Demand for Integrated Digital Experiences

Modern customers expect seamless integration across mobile, web, and branches, and 81% of US bank customers (2024 Deloitte survey) say they would switch after a single poor digital experience; if BankUnited lags, customers can migrate to competitors—JPMorgan and Chase reported 6% digital-driven deposit growth in 2024—making digital capability a mandatory retention factor tied directly to deposit flows and fee income.

Concentration of Large Commercial Accounts

A significant share of BankUnited’s loan portfolio—about 28% of total loans as of FY 2024-end ($19.2bn of $68.6bn total loans)—comes from large commercial and industrial borrowers, concentrating credit risk and revenue exposure. Losing a handful of high-value corporate clients could cut net interest income materially and pressure capital ratios given those accounts’ outsized balances. This concentration lets large borrowers demand customized structures and lower yields, squeezing margins and raising negotiation leverage. Banks often offer bespoke pricing to retain >$100m obligors.

- 28% of loans from large commercial accounts (FY 2024)

- $19.2bn in large C&I loans vs $68.6bn total loans

- High-value client loss can materially hit NII and capital

- Large borrowers secure bespoke products and preferential pricing

Availability of Information and Comparison Tools

The rise of financial comparison sites and apps lets retail and commercial clients track deposit, loan, and fee rates in real time; in 2024, 62% of US consumers used at least one comparison tool for banking choices, narrowing information asymmetry versus BankUnited.

That transparency limits BankUnited’s relationship pricing power, compressing net interest margins (US regional banks’ median NIM fell to 2.6% in 2024) and enabling customers to dispute fees and demand added value.

- 62% of consumers used comparison tools in 2024

- Median regional bank NIM 2.6% in 2024

- Real-time rate feeds reduce pricing leverage

- Higher fee pressure from informed clients

BankUnited under margin pressure as digital churn and concentrated C&I loans raise risk

Customers hold high bargaining power: 46% considered switching banks in 2024, 62% used comparison tools, and digital expectations (81% switch after one bad experience) force BankUnited to match rates and UX; 28% of loans ( $19.2bn of $68.6bn in FY2024) concentrate commercial leverage, while regional median NIM fell to 2.6% in 2024, squeezing pricing power.

| Metric | Value |

|---|---|

| Consumers considering switch (2024) | 46% |

| Comparison-tool users (2024) | 62% |

| Digital churn trigger (Deloitte 2024) | 81% |

| BankUnited large C&I loans (FY2024) | $19.2bn (28%) |

| Regional bank median NIM (2024) | 2.6% |

Preview Before You Purchase

BankUnited Porter's Five Forces Analysis

This preview shows the exact BankUnited Porter’s Five Forces analysis you'll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

BankUnited faces moderate competitive pressure: strong regional rivals and regulatory costs limit margins, while a focused deposit base and digital initiatives bolster customer retention.

This snapshot highlights buyer sensitivity to rates and moderate threat of substitutes from fintechs; supply-side risks are muted by diversified funding, but new entrants could disrupt niche segments.

This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy tailored to BankUnited.

Suppliers Bargaining Power

Cost of Financial Capital

The primary suppliers for BankUnited are depositors and wholesale funding providers such as the Federal Home Loan Bank; as of Q4 2025, deposits funded ~78% of assets while FHLB borrowings stood at $6.2 billion, giving suppliers moderate-to-high leverage. Elevated rate expectations in 2025 pushed average deposit betas toward 55–65%, forcing BankUnited to lift yields and compress net interest margin to about 2.45% in Q4 2025. Competitive liquidity markets and tight secondary funding raise replacement costs and shorten tenor, increasing funding risk. If core deposit retention slips, margin and ROA could decline materially.

Technology and Fintech Vendors

BankUnited depends on third-party core-banking, cybersecurity, and digital-platform vendors, creating high supplier power since switching core systems often costs tens of millions and 12–24 months; major players like FIS, Fiserv, and Jack Henry dominate ~70% of US bank core market (2024 estimate).

Regulatory and Compliance Entities

Regulatory bodies like the FDIC and OCC act as non-market suppliers of the legal framework and mandates BankUnited must follow, forcing non‑negotiable compliance spending—BankUnited reported $218 million in regulatory and legal expenses in 2024, a material fixed cost. Changes in capital ratios (e.g., higher CET1 targets) or tighter FDIC/OCC exams reduce strategic flexibility and raise funding costs; a 100 bps capital hike can cut 2025 ROE by ~1.2 percentage points.

Skilled Labor and Executive Talent

The market for specialized commercial-lending and risk-management professionals in Miami and New York is tight; BankUnited competes with JPMorgan Chase, Bank of America, and regional peers, pushing median commercial-banking base salaries up ~12–18% vs. national averages (2024 Bureau of Labor Statistics and industry surveys).

Scarcity of experienced commercial bankers in Florida and NY raises workforce bargaining power, increasing total compensation costs and retention spend; BankUnited’s 2024 compensation-to-revenue ratio rose ~1.5 percentage points year-over-year.

Credit Rating Agencies

Credit rating agencies like Moody’s and S&P set ratings that directly affect BankUnited’s institutional borrowing costs; as of Q4 2025, a one-notch downgrade typically raises senior unsecured spreads by ~60–120 bps, raising funding costs materially.

The oligopolistic market for ratings means their opinions strongly constrain BankUnited’s capital-market access; a downgrade would shrink strategic flexibility by increasing cost of funds and limiting repo and bond issuance capacity.

- Moody’s/S&P concentration: 70–80% market share

- One-notch downgrade ≈ +60–120 bps funding spread

- Higher spreads reduce ROE and limit bond issuance

High supplier power squeezes margins: deposits, FHLB, vendors & regulator costs

Suppliers exert moderate-to-high power: depositors funded ~78% of assets (Q4 2025) and FHLB borrowings were $6.2B, forcing deposit betas to ~55–65% and NIM to ~2.45% (Q4 2025); core-banking vendors (FIS, Fiserv, Jack Henry ~70% market share) raise switching costs; regulators (FDIC/OCC) drove $218M compliance spend in 2024; ratings moves add ~60–120 bps to funding on a one-notch downgrade.

What is included in the product

Tailored Porter's Five Forces analysis for BankUnited that uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and emerging threats to its market position—ready for integration into investor decks or strategy reports.

Concise Porter's Five Forces snapshot for BankUnited—quickly assess competitive pressures and regulatory risk to inform strategic moves.

Customers Bargaining Power

Low Switching Costs for Retail Depositors

Retail depositors now shift funds quickly via apps and ACH; 2024 data shows 46% of US consumers switched primary banks or considered switching in the prior 12 months, raising customer leverage over BankUnited.

Low switching costs force BankUnited to compete on rates and UX; online banks like Ally and Marcus offered savings yields up to 4.5% in 2025, pressuring margins and retention.

Price Sensitivity in Commercial Lending

BankUnited’s commercial clients—midmarket firms and CRE borrowers—are sophisticated and often have multiple bids; 2024 LPC data shows 68% of middle-market loans saw price compression from competing offers, pressuring margins.

Borrowers use competing regional and national bank offers to push rates and covenants down; BankUnited’s 2025 Q1 commercial loan yield of ~4.2% vs. peers’ 4.0% reflects tightened spreads to stay competitive.

Demand for Integrated Digital Experiences

Modern customers expect seamless integration across mobile, web, and branches, and 81% of US bank customers (2024 Deloitte survey) say they would switch after a single poor digital experience; if BankUnited lags, customers can migrate to competitors—JPMorgan and Chase reported 6% digital-driven deposit growth in 2024—making digital capability a mandatory retention factor tied directly to deposit flows and fee income.

Concentration of Large Commercial Accounts

A significant share of BankUnited’s loan portfolio—about 28% of total loans as of FY 2024-end ($19.2bn of $68.6bn total loans)—comes from large commercial and industrial borrowers, concentrating credit risk and revenue exposure. Losing a handful of high-value corporate clients could cut net interest income materially and pressure capital ratios given those accounts’ outsized balances. This concentration lets large borrowers demand customized structures and lower yields, squeezing margins and raising negotiation leverage. Banks often offer bespoke pricing to retain >$100m obligors.

- 28% of loans from large commercial accounts (FY 2024)

- $19.2bn in large C&I loans vs $68.6bn total loans

- High-value client loss can materially hit NII and capital

- Large borrowers secure bespoke products and preferential pricing

Availability of Information and Comparison Tools

The rise of financial comparison sites and apps lets retail and commercial clients track deposit, loan, and fee rates in real time; in 2024, 62% of US consumers used at least one comparison tool for banking choices, narrowing information asymmetry versus BankUnited.

That transparency limits BankUnited’s relationship pricing power, compressing net interest margins (US regional banks’ median NIM fell to 2.6% in 2024) and enabling customers to dispute fees and demand added value.

- 62% of consumers used comparison tools in 2024

- Median regional bank NIM 2.6% in 2024

- Real-time rate feeds reduce pricing leverage

- Higher fee pressure from informed clients

BankUnited under margin pressure as digital churn and concentrated C&I loans raise risk

Customers hold high bargaining power: 46% considered switching banks in 2024, 62% used comparison tools, and digital expectations (81% switch after one bad experience) force BankUnited to match rates and UX; 28% of loans ( $19.2bn of $68.6bn in FY2024) concentrate commercial leverage, while regional median NIM fell to 2.6% in 2024, squeezing pricing power.

| Metric | Value |

|---|---|

| Consumers considering switch (2024) | 46% |

| Comparison-tool users (2024) | 62% |

| Digital churn trigger (Deloitte 2024) | 81% |

| BankUnited large C&I loans (FY2024) | $19.2bn (28%) |

| Regional bank median NIM (2024) | 2.6% |

Preview Before You Purchase

BankUnited Porter's Five Forces Analysis

This preview shows the exact BankUnited Porter’s Five Forces analysis you'll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or mockups.