BankUnited PESTLE Analysis

Your Competitive Advantage Starts with This Report

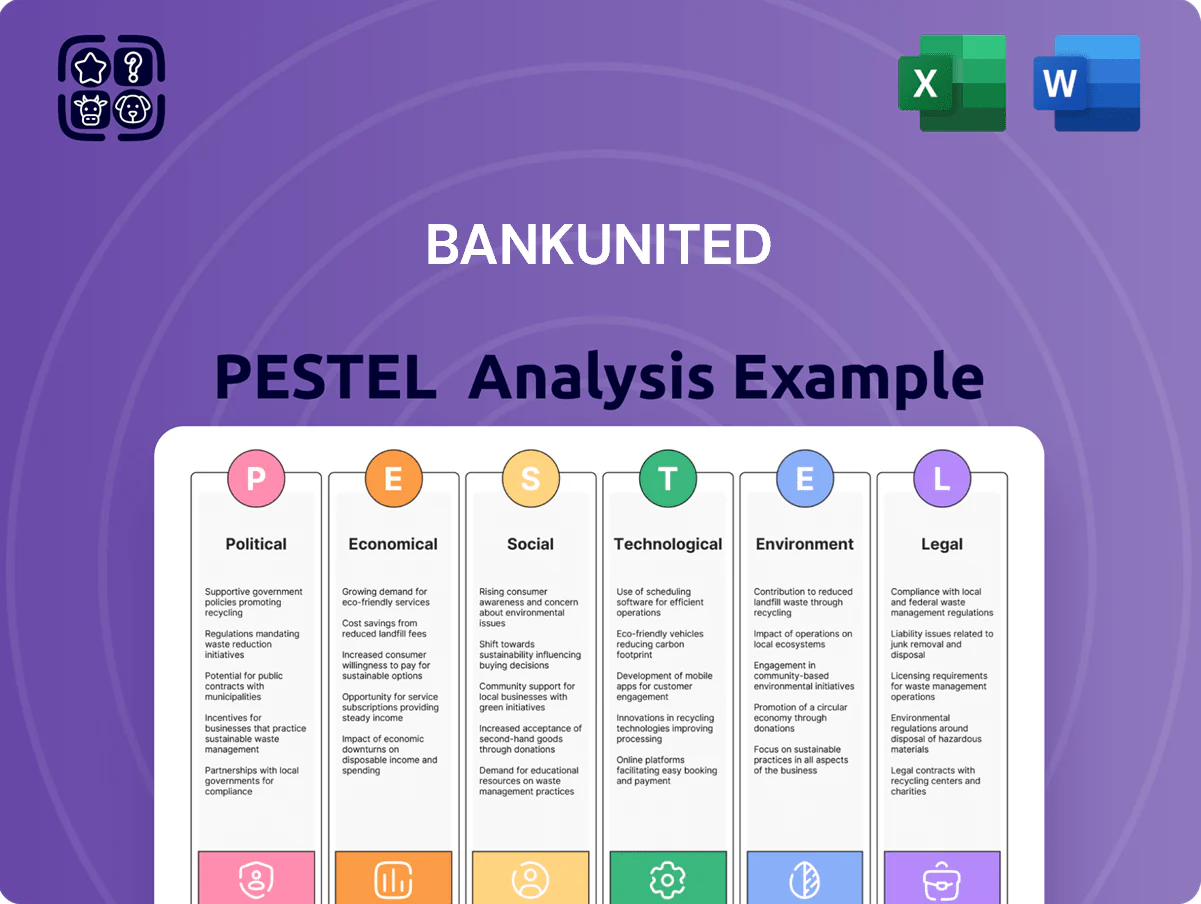

Gain a competitive edge with our tailored PESTLE Analysis for BankUnited—uncover how political shifts, economic cycles, and tech trends will shape its strategy and risk profile; buy the full report to access detailed, actionable insights and ready-to-use slides for investment decisions and strategic planning.

Political factors

Regulatory shifts under new administration

The 2024 election outcomes prompted regulatory shifts by late 2025, with federal proposals raising minimum Tier 1 capital ratios from 8% to a proposed 9.5% for regional banks, directly affecting BankUnited’s $45.6bn assets under management and capital planning.

New community reinvestment standards increase low-to-moderate lending quotas by ~20%, pressuring BankUnited’s lending mix and expected return on equity, which was 10.2% in 2024.

Compliance costs are projected to rise by an estimated $18–25m annually for banks of similar size, constraining free cash flow and capital deployment flexibility.

Geopolitical influence on regional trade

Geopolitical shifts between the US and Latin America materially affect BankUnited’s Florida operations; in 2025 Miami-Dade held about 23% of the bank’s deposits, making foreign deposit flows sensitive to regional instability and tariff or remittance policy changes. Political unrest in 2024–25 in several Latin American countries coincided with a 4–6% quarterly variance in cross-border deposits into Miami-linked accounts, prompting enhanced liquidity monitoring and adjusted customer-acquisition spending.

State-level policy divergence

Operating mainly in Florida and New York forces BankUnited to manage divergent state politics: Florida's low-tax, pro-growth stance helped Florida GDP grow 3.7% in 2024, supporting higher loan demand and lower tax burden, while New York's tighter regulations and higher effective tax rates—New York state tax revenue rose 4.1% in 2024—raise compliance costs and constrain margin management.

Federal Reserve independence and pressure

Political debate over Federal Reserve independence directly affects BankUnited's interest rate risk; markets reacted sharply in Q4 2025 when 10-year Treasury yields swung 65 bps over two weeks after high-profile hearings.

Perceived political pressure increases volatility risk to net interest margin (NIM); BankUnited reported NIM of 3.21% in 2024 and must hedge against multi-quarter rate moves.

Robust hedging—swaps, caps, and duration management—remains essential to protect loan deposit spreads and forecasted earnings at risk.

- 10-year UST volatility: +65 bps (Q4 2025 shock)

Government-backed lending initiatives

Participation in federal and state small business lending programs shifts with political priorities; BankUnited increased SBA loan originations to $1.1bn in 2024, reflecting responsiveness to policy-driven demand.

New mandates or subsidies for tech, clean energy, and healthcare created commercial lending opportunities; BankUnited directed 18% of CRE and C&I growth in 2024 toward these sectors.

BankUnited aligns product development with government initiatives—launching targeted loan products and local partnership programs—to support economic development and expand market share in Florida and Sunbelt markets.

- 2024 SBA originations: $1.1bn

- 18% of 2024 CRE/C&I growth into policy-favored sectors

- Focus markets: Florida and Sunbelt

BankUnited faces 9.5% Tier 1 hurdle: $45.6B AUM, Miami concentration and rate risk

Political shifts since 2024 raised proposed Tier 1 minimums to 9.5%, risking capital strain on BankUnited's $45.6bn AUM; compliance costs up $18–25m/year; Miami-Dade holds ~23% of deposits, with 4–6% cross-border deposit volatility in 2024–25; NIM 3.21% (2024) exposed to 65 bp UST swing (Q4 2025); SBA originations $1.1bn (2024); 18% CRE/C&I growth into policy-favored sectors.

| Metric | Value |

|---|---|

| Assets under management | $45.6bn |

| Tier 1 proposed min | 9.5% |

| Compliance cost increase | $18–25m/yr |

| Miami-Dade deposit share | 23% |

| Cross-border deposit volatility | 4–6% |

| NIM (2024) | 3.21% |

| 10y UST shock (Q4 2025) | +65 bps |

| SBA originations (2024) | $1.1bn |

| CRE/C&I into favored sectors (2024) | 18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect BankUnited, with each section grounded in current data and trends to highlight region- and industry-specific risks and opportunities.

A concise, visually segmented PESTLE summary for BankUnited that can be dropped into presentations or shared across teams to streamline external risk discussions and support quick, aligned decision-making.

Economic factors

Interest rate environment stabilization

By end-2025 interest rates settled around a fed funds effective rate near 5.25% after prior volatility, creating a more predictable funding backdrop for BankUnited; net interest margin remained a focal metric as the bank reported NIM of 3.45% in 3Q/2025, with loan yields approximately 6.2% versus deposit costs near 1.8%. Management is rebalancing the balance sheet—shifting toward higher-yield commercial loans and optimizing deposit mix—to protect spreads in this stabilized rate environment.

Real estate market health in core regions

Florida and the New York metro real estate markets underpin roughly 70% of BankUnited’s commercial and residential loan book; Q4 2025 Florida home price growth slowed to 1.8% YoY while NYC metro prices rose 3.2% YoY, affecting collateral values and stress testing.

Rising Florida office vacancy at 19% and NYC office vacancy near 17% elevate credit risk for CRE exposures; loan nonperforming assets ratio must be watched alongside local vacancy trends.

Maintaining loan-to-value requires active monitoring of county-level valuations: Miami-Dade median home price ~$470,000 and Nassau-Suffolk median ~$590,000 to guard loss severity assumptions.

Inflationary impact on operational costs

By late 2025 headline CPI had cooled to about 3.2% YoY, yet BankUnited still faces wage inflation with average employee costs up ~4–5% in 2024–25, squeezing the efficiency ratio that was 61.4% in FY2024. Rising vendor and service fees lifted non-interest expenses 6% YoY in 2024, forcing a trade-off between competitive pay to retain talent and cost control. Continued investment in automation—capex rising ~8% in 2024—aims to offset these pressures.

Consumer and business confidence levels

Consumer and business confidence directly affects demand for new credit and utilization of lines among BankUnited clients; US consumer confidence rose to 111.5 in Jan 2025 (Conference Board), supporting higher card and personal loan usage and a 6% YoY rise in mortgage applications in 2024.

High confidence drives commercial expansion and residential mortgage demand, while uncertainty prompts deleveraging—BankUnited saw loan growth slow to 2.1% YoY in Q3 2025 amid risk-off sentiment, compressing fee income.

- Confidence up → more credit demand, mortgage applications +6% (2024)

- Confidence down → deleveraging, loan growth as low as 2.1% YoY (Q3 2025)

- Impact: direct effect on interest and fee income, commercial loan origination

Employment trends in service-oriented sectors

BankUnited’s core markets, concentrated in Florida, hinge on tourism, finance, and professional services where leisure employment recovered to 92% of pre-pandemic levels by Q4 2025 and finance employment rose 3.1% YoY in 2025; swings here directly affect deposit growth and borrower repayment capacity.

The bank monitors regional unemployment (Florida 4.0% Jan 2026) and sectoral payrolls to forecast credit deterioration and liquidity stress, adjusting reserves and lending standards accordingly.

- Tourism employment at 92% of 2019 levels (Q4 2025)

- Finance jobs +3.1% YoY (2025)

- Florida unemployment 4.0% (Jan 2026)

- Impacts: deposit volatility, credit risk, reserve adjustments

Stable rates bolster NIM; CRE risks rise as loan growth slows and expenses climb

Interest-rate stability (fed funds ~5.25% end-2025) supported NIM ~3.45% and loan yields ~6.2% vs deposit cost ~1.8%; management shifted toward higher-yield commercial loans. Florida/NYC real estate (70% book) saw modest price gains (Miami-Dade ~$470k, Nassau-Suffolk ~$590k) amid high CRE vacancy (FL 19%, NYC 17%), raising collateral risk. Wage inflation (+4–5% 2024–25) and 61.4% efficiency ratio pressure expenses; consumer confidence (111.5 Jan 2025) lifted loan demand but loan growth slowed to 2.1% YoY Q3 2025.

| Metric | Value |

|---|---|

| Fed funds (end-2025) | ≈5.25% |

| NIM (3Q/2025) | 3.45% |

| Loan yield / deposit cost | 6.2% / 1.8% |

| Loan growth (Q3 2025) | 2.1% YoY |

| Miami-Dade median | ~$470,000 |

| Nassau-Suffolk median | ~$590,000 |

| Florida unemployment (Jan 2026) | 4.0% |

Preview Before You Purchase

BankUnited PESTLE Analysis

The preview shown here is the exact BankUnited PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our tailored PESTLE Analysis for BankUnited—uncover how political shifts, economic cycles, and tech trends will shape its strategy and risk profile; buy the full report to access detailed, actionable insights and ready-to-use slides for investment decisions and strategic planning.

Political factors

Regulatory shifts under new administration

The 2024 election outcomes prompted regulatory shifts by late 2025, with federal proposals raising minimum Tier 1 capital ratios from 8% to a proposed 9.5% for regional banks, directly affecting BankUnited’s $45.6bn assets under management and capital planning.

New community reinvestment standards increase low-to-moderate lending quotas by ~20%, pressuring BankUnited’s lending mix and expected return on equity, which was 10.2% in 2024.

Compliance costs are projected to rise by an estimated $18–25m annually for banks of similar size, constraining free cash flow and capital deployment flexibility.

Geopolitical influence on regional trade

Geopolitical shifts between the US and Latin America materially affect BankUnited’s Florida operations; in 2025 Miami-Dade held about 23% of the bank’s deposits, making foreign deposit flows sensitive to regional instability and tariff or remittance policy changes. Political unrest in 2024–25 in several Latin American countries coincided with a 4–6% quarterly variance in cross-border deposits into Miami-linked accounts, prompting enhanced liquidity monitoring and adjusted customer-acquisition spending.

State-level policy divergence

Operating mainly in Florida and New York forces BankUnited to manage divergent state politics: Florida's low-tax, pro-growth stance helped Florida GDP grow 3.7% in 2024, supporting higher loan demand and lower tax burden, while New York's tighter regulations and higher effective tax rates—New York state tax revenue rose 4.1% in 2024—raise compliance costs and constrain margin management.

Federal Reserve independence and pressure

Political debate over Federal Reserve independence directly affects BankUnited's interest rate risk; markets reacted sharply in Q4 2025 when 10-year Treasury yields swung 65 bps over two weeks after high-profile hearings.

Perceived political pressure increases volatility risk to net interest margin (NIM); BankUnited reported NIM of 3.21% in 2024 and must hedge against multi-quarter rate moves.

Robust hedging—swaps, caps, and duration management—remains essential to protect loan deposit spreads and forecasted earnings at risk.

- 10-year UST volatility: +65 bps (Q4 2025 shock)

Government-backed lending initiatives

Participation in federal and state small business lending programs shifts with political priorities; BankUnited increased SBA loan originations to $1.1bn in 2024, reflecting responsiveness to policy-driven demand.

New mandates or subsidies for tech, clean energy, and healthcare created commercial lending opportunities; BankUnited directed 18% of CRE and C&I growth in 2024 toward these sectors.

BankUnited aligns product development with government initiatives—launching targeted loan products and local partnership programs—to support economic development and expand market share in Florida and Sunbelt markets.

- 2024 SBA originations: $1.1bn

- 18% of 2024 CRE/C&I growth into policy-favored sectors

- Focus markets: Florida and Sunbelt

BankUnited faces 9.5% Tier 1 hurdle: $45.6B AUM, Miami concentration and rate risk

Political shifts since 2024 raised proposed Tier 1 minimums to 9.5%, risking capital strain on BankUnited's $45.6bn AUM; compliance costs up $18–25m/year; Miami-Dade holds ~23% of deposits, with 4–6% cross-border deposit volatility in 2024–25; NIM 3.21% (2024) exposed to 65 bp UST swing (Q4 2025); SBA originations $1.1bn (2024); 18% CRE/C&I growth into policy-favored sectors.

| Metric | Value |

|---|---|

| Assets under management | $45.6bn |

| Tier 1 proposed min | 9.5% |

| Compliance cost increase | $18–25m/yr |

| Miami-Dade deposit share | 23% |

| Cross-border deposit volatility | 4–6% |

| NIM (2024) | 3.21% |

| 10y UST shock (Q4 2025) | +65 bps |

| SBA originations (2024) | $1.1bn |

| CRE/C&I into favored sectors (2024) | 18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect BankUnited, with each section grounded in current data and trends to highlight region- and industry-specific risks and opportunities.

A concise, visually segmented PESTLE summary for BankUnited that can be dropped into presentations or shared across teams to streamline external risk discussions and support quick, aligned decision-making.

Economic factors

Interest rate environment stabilization

By end-2025 interest rates settled around a fed funds effective rate near 5.25% after prior volatility, creating a more predictable funding backdrop for BankUnited; net interest margin remained a focal metric as the bank reported NIM of 3.45% in 3Q/2025, with loan yields approximately 6.2% versus deposit costs near 1.8%. Management is rebalancing the balance sheet—shifting toward higher-yield commercial loans and optimizing deposit mix—to protect spreads in this stabilized rate environment.

Real estate market health in core regions

Florida and the New York metro real estate markets underpin roughly 70% of BankUnited’s commercial and residential loan book; Q4 2025 Florida home price growth slowed to 1.8% YoY while NYC metro prices rose 3.2% YoY, affecting collateral values and stress testing.

Rising Florida office vacancy at 19% and NYC office vacancy near 17% elevate credit risk for CRE exposures; loan nonperforming assets ratio must be watched alongside local vacancy trends.

Maintaining loan-to-value requires active monitoring of county-level valuations: Miami-Dade median home price ~$470,000 and Nassau-Suffolk median ~$590,000 to guard loss severity assumptions.

Inflationary impact on operational costs

By late 2025 headline CPI had cooled to about 3.2% YoY, yet BankUnited still faces wage inflation with average employee costs up ~4–5% in 2024–25, squeezing the efficiency ratio that was 61.4% in FY2024. Rising vendor and service fees lifted non-interest expenses 6% YoY in 2024, forcing a trade-off between competitive pay to retain talent and cost control. Continued investment in automation—capex rising ~8% in 2024—aims to offset these pressures.

Consumer and business confidence levels

Consumer and business confidence directly affects demand for new credit and utilization of lines among BankUnited clients; US consumer confidence rose to 111.5 in Jan 2025 (Conference Board), supporting higher card and personal loan usage and a 6% YoY rise in mortgage applications in 2024.

High confidence drives commercial expansion and residential mortgage demand, while uncertainty prompts deleveraging—BankUnited saw loan growth slow to 2.1% YoY in Q3 2025 amid risk-off sentiment, compressing fee income.

- Confidence up → more credit demand, mortgage applications +6% (2024)

- Confidence down → deleveraging, loan growth as low as 2.1% YoY (Q3 2025)

- Impact: direct effect on interest and fee income, commercial loan origination

Employment trends in service-oriented sectors

BankUnited’s core markets, concentrated in Florida, hinge on tourism, finance, and professional services where leisure employment recovered to 92% of pre-pandemic levels by Q4 2025 and finance employment rose 3.1% YoY in 2025; swings here directly affect deposit growth and borrower repayment capacity.

The bank monitors regional unemployment (Florida 4.0% Jan 2026) and sectoral payrolls to forecast credit deterioration and liquidity stress, adjusting reserves and lending standards accordingly.

- Tourism employment at 92% of 2019 levels (Q4 2025)

- Finance jobs +3.1% YoY (2025)

- Florida unemployment 4.0% (Jan 2026)

- Impacts: deposit volatility, credit risk, reserve adjustments

Stable rates bolster NIM; CRE risks rise as loan growth slows and expenses climb

Interest-rate stability (fed funds ~5.25% end-2025) supported NIM ~3.45% and loan yields ~6.2% vs deposit cost ~1.8%; management shifted toward higher-yield commercial loans. Florida/NYC real estate (70% book) saw modest price gains (Miami-Dade ~$470k, Nassau-Suffolk ~$590k) amid high CRE vacancy (FL 19%, NYC 17%), raising collateral risk. Wage inflation (+4–5% 2024–25) and 61.4% efficiency ratio pressure expenses; consumer confidence (111.5 Jan 2025) lifted loan demand but loan growth slowed to 2.1% YoY Q3 2025.

| Metric | Value |

|---|---|

| Fed funds (end-2025) | ≈5.25% |

| NIM (3Q/2025) | 3.45% |

| Loan yield / deposit cost | 6.2% / 1.8% |

| Loan growth (Q3 2025) | 2.1% YoY |

| Miami-Dade median | ~$470,000 |

| Nassau-Suffolk median | ~$590,000 |

| Florida unemployment (Jan 2026) | 4.0% |

Preview Before You Purchase

BankUnited PESTLE Analysis

The preview shown here is the exact BankUnited PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.