Banner Bank Business Model Canvas

Banner Bank Business Model Canvas: Value, Revenue & Competitive Edge

Unlock Banner Bank's strategic playbook with our concise Business Model Canvas—discover how it creates customer value, optimizes revenue streams, and sustains competitive advantage across retail and commercial banking.

Partnerships

Fintech and Technology Providers

Banner Bank partners with fintechs to upgrade digital banking and its mobile app, using third-party APIs to add real-time payments and MFA security while avoiding $5–10M+ in in-house development costs typical for mid-sized banks (2024 industry averages). These integrations helped Banner improve digital transaction volume by ~18% year-over-year in 2024 and kept tech spend focused on core lending and treasury operations.

Mortgage Secondary Market Investors

Banner Bank sells many residential loans to Fannie Mae and Freddie Mac, preserving servicing rights while cutting long-term rate exposure; in 2024 roughly 30–40% of its originated mortgages were dispatched to the secondary market, helping free capital for new loans. These GSE ties give Banner steady wholesale funding and liquidity—supporting its Pacific Northwest lending amid a $50–60bn regional mortgage market.

Payment and Card Networks

Banner Bank partners with Visa and Mastercard to issue branded credit and debit cards, tapping networks that process billions of transactions yearly—Visa handled $14.6 trillion in global payments in 2024—while providing real-time transaction routing, fraud monitoring, and merchant acquiring services.

Regulatory and Compliance Agencies

Banner Bank engages continuously with the FDIC and state banking departments—undergoing annual and risk-based audits, submitting quarterly Call Reports (FFIEC 041/031) and meeting capital adequacy rules; as of 2025 Banner Financial Corp reported a CET1 ratio around 11.8%, supporting regulatory compliance and market confidence.

These agencies require transparent reporting, prompt remediation of findings, and alignment with evolving financial-stability guidance; maintaining the charter and depositor trust depends on meeting exam timelines and corrective action plans.

- Regular audits: annual plus risk-based exams

- Reporting: quarterly Call Reports, FR Y-9C equivalents

- Capital: CET1 ~11.8% (2025)

- Purpose: preserve charter and public trust

Local Community Organizations

Banner Bank partners with regional non-profits and community development groups to meet Community Reinvestment Act goals and spur local growth, channeling roughly $120–150 million annually (2024 figure) into affordable housing loans and small-business grants.

These ties build brand loyalty, surface niche lending deals—about 18% of new CRE/small-business originations in 2024—and reduce acquisition costs by strengthening local referral pipelines.

- $120–150M annual community financing (2024)

- ~18% of new originations from community partnerships (2024)

- Focus: affordable housing loans, small-business grants

Banner Bank scales digital mortgage & community finance—$120–150M deployed, 18% digital growth

Banner Bank leverages fintechs, Visa/Mastercard, GSEs (Fannie/Freddie), regulators, and community groups to scale digital services, manage mortgage pipeline risk, ensure compliance (CET1 ~11.8% in 2025), and fund affordable housing—saving $5–10M in dev costs, driving ~18% YoY digital transaction growth, selling 30–40% of mortgages, and deploying $120–150M community finance in 2024.

| Partner | Key metric (2024/25) |

|---|---|

| Fintechs | $5–10M saved; +18% digital tx |

| GSEs | 30–40% mortgages sold |

| Card networks | Visa $14.6T global (2024) |

| Regulators | CET1 ~11.8% (2025) |

| Community | $120–150M financed (2024) |

What is included in the product

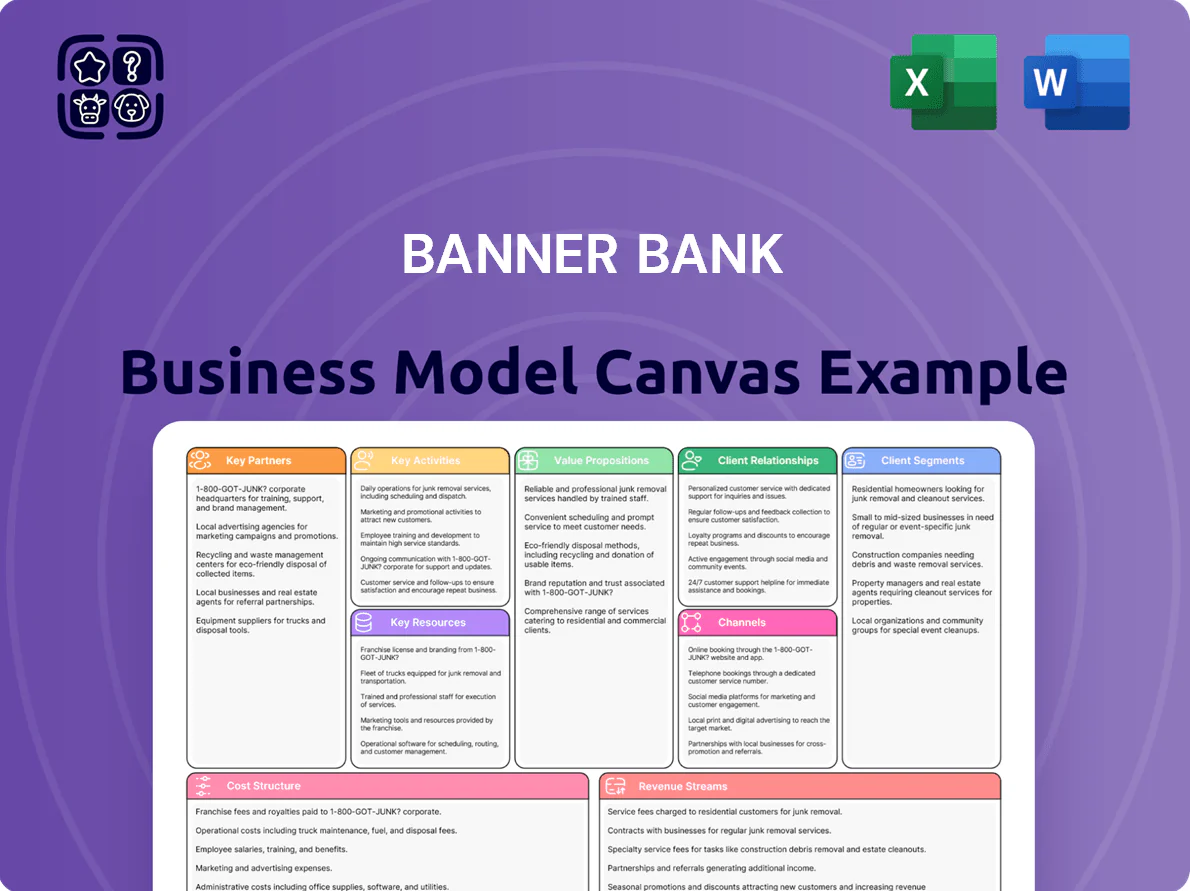

A concise, ready-made Business Model Canvas for Banner Bank outlining customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure, and customer relationships aligned with the bank’s regional commercial and consumer strategy.

High-level view of Banner Bank’s business model with editable cells to quickly pinpoint customer segments, revenue streams, and cost drivers—ideal for teams needing a concise, shareable snapshot to streamline strategy and decision-making.

Activities

Commercial and Retail Lending

Banner Bank underwrites and manages a diversified loan portfolio—commercial real estate, construction, and consumer loans—driving interest income (net interest margin 2.78% in 2025 Q3) while targeting asset quality (nonperforming assets 0.45% at 2025 Q3). Credit analysts and loan officers assess risk to balance yield and credit losses, supporting regional lending where total loans held for investment reached $14.2 billion as of Sep 30, 2025.

Deposit and Liquidity Management

Banner Bank prioritizes attracting core deposits—non-interest checking, business accounts, and high-yield savings—to fund lending; as of 2024 it held about $12.3 billion in deposits, with core deposits making up roughly 78% of total funding. Effective liquidity management keeps cash and liquid securities aligned with expected outflows and regulatory buffers, maintaining a loan-to-deposit ratio near 85% and CET1 capital above regulatory minimums.

Risk Management and Compliance

A significant portion of Banner Bank’s operations focuses on monitoring credit risk, market volatility, and operational hazards, with the bank running monthly stress tests that showed a 6.2% projected loan-loss under a severe recession scenario in FY2024. The bank uses advanced credit and scenario models and maintained 2024 AML/KYC compliance spending near $28 million to limit legal exposure and protect capital in a tighter regulatory landscape.

Digital Banking Transformation

Banner Bank treats digital banking transformation as a core activity, investing over $75 million since 2020 to upgrade online and mobile platforms, add biometric logins, improve UX, and automate back-office workflows to cut transaction clearing times by ~30%.

- Biometric login rollout across mobile apps (2024)

- ~30% faster clearing via automation

- $75M+ digital investment since 2020

- Higher NPS and lower servicing cost per account

Community Relationship Banking

Banner Bank’s Community Relationship Banking delivers high-touch service via 140+ branches and 1,800+ employees, offering personalized advice and dedicated relationship managers to small businesses and professional firms.

Staff perform proactive outreach—over 25,000 client touchpoints in 2024—to craft tailored lending, cash management, and treasury solutions, driving higher retention versus national peers.

- 140+ branches; 1,800+ staff (2024)

- 25,000+ client touchpoints (2024)

- Focus: SMB lending, cash mgmt, treasury

Banner Bank: $14.2B Loan Engine, Core-Funded, Digitally Upgraded & Stress-Tested

Banner Bank originates and services diversified loans ($14.2B loans, 2025-09-30), funds lending via core deposits ($12.3B, 2024) with L/D ~85%, runs monthly stress tests (severe-loss 6.2% FY2024), invests $75M+ in digital since 2020, and operates 140+ branches with 1,800+ staff and 25k+ client touchpoints (2024).

| Metric | Value |

|---|---|

| Total loans | $14.2B (2025-09-30) |

| Deposits | $12.3B (2024) |

| Net interest margin | 2.78% (2025 Q3) |

| Nonperforming assets | 0.45% (2025 Q3) |

| Stress loss (severe) | 6.2% FY2024 |

| Digital spend since 2020 | $75M+ |

| Branches / staff | 140+ / 1,800+ (2024) |

| Client touchpoints | 25,000+ (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Banner Bank Business Model Canvas you’ll receive after purchase—not a mockup or sample—and when you complete your order you’ll get this same professional, fully editable file ready for use in Word and Excel.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Banner Bank Business Model Canvas: Value, Revenue & Competitive Edge

Unlock Banner Bank's strategic playbook with our concise Business Model Canvas—discover how it creates customer value, optimizes revenue streams, and sustains competitive advantage across retail and commercial banking.

Partnerships

Fintech and Technology Providers

Banner Bank partners with fintechs to upgrade digital banking and its mobile app, using third-party APIs to add real-time payments and MFA security while avoiding $5–10M+ in in-house development costs typical for mid-sized banks (2024 industry averages). These integrations helped Banner improve digital transaction volume by ~18% year-over-year in 2024 and kept tech spend focused on core lending and treasury operations.

Mortgage Secondary Market Investors

Banner Bank sells many residential loans to Fannie Mae and Freddie Mac, preserving servicing rights while cutting long-term rate exposure; in 2024 roughly 30–40% of its originated mortgages were dispatched to the secondary market, helping free capital for new loans. These GSE ties give Banner steady wholesale funding and liquidity—supporting its Pacific Northwest lending amid a $50–60bn regional mortgage market.

Payment and Card Networks

Banner Bank partners with Visa and Mastercard to issue branded credit and debit cards, tapping networks that process billions of transactions yearly—Visa handled $14.6 trillion in global payments in 2024—while providing real-time transaction routing, fraud monitoring, and merchant acquiring services.

Regulatory and Compliance Agencies

Banner Bank engages continuously with the FDIC and state banking departments—undergoing annual and risk-based audits, submitting quarterly Call Reports (FFIEC 041/031) and meeting capital adequacy rules; as of 2025 Banner Financial Corp reported a CET1 ratio around 11.8%, supporting regulatory compliance and market confidence.

These agencies require transparent reporting, prompt remediation of findings, and alignment with evolving financial-stability guidance; maintaining the charter and depositor trust depends on meeting exam timelines and corrective action plans.

- Regular audits: annual plus risk-based exams

- Reporting: quarterly Call Reports, FR Y-9C equivalents

- Capital: CET1 ~11.8% (2025)

- Purpose: preserve charter and public trust

Local Community Organizations

Banner Bank partners with regional non-profits and community development groups to meet Community Reinvestment Act goals and spur local growth, channeling roughly $120–150 million annually (2024 figure) into affordable housing loans and small-business grants.

These ties build brand loyalty, surface niche lending deals—about 18% of new CRE/small-business originations in 2024—and reduce acquisition costs by strengthening local referral pipelines.

- $120–150M annual community financing (2024)

- ~18% of new originations from community partnerships (2024)

- Focus: affordable housing loans, small-business grants

Banner Bank scales digital mortgage & community finance—$120–150M deployed, 18% digital growth

Banner Bank leverages fintechs, Visa/Mastercard, GSEs (Fannie/Freddie), regulators, and community groups to scale digital services, manage mortgage pipeline risk, ensure compliance (CET1 ~11.8% in 2025), and fund affordable housing—saving $5–10M in dev costs, driving ~18% YoY digital transaction growth, selling 30–40% of mortgages, and deploying $120–150M community finance in 2024.

| Partner | Key metric (2024/25) |

|---|---|

| Fintechs | $5–10M saved; +18% digital tx |

| GSEs | 30–40% mortgages sold |

| Card networks | Visa $14.6T global (2024) |

| Regulators | CET1 ~11.8% (2025) |

| Community | $120–150M financed (2024) |

What is included in the product

A concise, ready-made Business Model Canvas for Banner Bank outlining customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure, and customer relationships aligned with the bank’s regional commercial and consumer strategy.

High-level view of Banner Bank’s business model with editable cells to quickly pinpoint customer segments, revenue streams, and cost drivers—ideal for teams needing a concise, shareable snapshot to streamline strategy and decision-making.

Activities

Commercial and Retail Lending

Banner Bank underwrites and manages a diversified loan portfolio—commercial real estate, construction, and consumer loans—driving interest income (net interest margin 2.78% in 2025 Q3) while targeting asset quality (nonperforming assets 0.45% at 2025 Q3). Credit analysts and loan officers assess risk to balance yield and credit losses, supporting regional lending where total loans held for investment reached $14.2 billion as of Sep 30, 2025.

Deposit and Liquidity Management

Banner Bank prioritizes attracting core deposits—non-interest checking, business accounts, and high-yield savings—to fund lending; as of 2024 it held about $12.3 billion in deposits, with core deposits making up roughly 78% of total funding. Effective liquidity management keeps cash and liquid securities aligned with expected outflows and regulatory buffers, maintaining a loan-to-deposit ratio near 85% and CET1 capital above regulatory minimums.

Risk Management and Compliance

A significant portion of Banner Bank’s operations focuses on monitoring credit risk, market volatility, and operational hazards, with the bank running monthly stress tests that showed a 6.2% projected loan-loss under a severe recession scenario in FY2024. The bank uses advanced credit and scenario models and maintained 2024 AML/KYC compliance spending near $28 million to limit legal exposure and protect capital in a tighter regulatory landscape.

Digital Banking Transformation

Banner Bank treats digital banking transformation as a core activity, investing over $75 million since 2020 to upgrade online and mobile platforms, add biometric logins, improve UX, and automate back-office workflows to cut transaction clearing times by ~30%.

- Biometric login rollout across mobile apps (2024)

- ~30% faster clearing via automation

- $75M+ digital investment since 2020

- Higher NPS and lower servicing cost per account

Community Relationship Banking

Banner Bank’s Community Relationship Banking delivers high-touch service via 140+ branches and 1,800+ employees, offering personalized advice and dedicated relationship managers to small businesses and professional firms.

Staff perform proactive outreach—over 25,000 client touchpoints in 2024—to craft tailored lending, cash management, and treasury solutions, driving higher retention versus national peers.

- 140+ branches; 1,800+ staff (2024)

- 25,000+ client touchpoints (2024)

- Focus: SMB lending, cash mgmt, treasury

Banner Bank: $14.2B Loan Engine, Core-Funded, Digitally Upgraded & Stress-Tested

Banner Bank originates and services diversified loans ($14.2B loans, 2025-09-30), funds lending via core deposits ($12.3B, 2024) with L/D ~85%, runs monthly stress tests (severe-loss 6.2% FY2024), invests $75M+ in digital since 2020, and operates 140+ branches with 1,800+ staff and 25k+ client touchpoints (2024).

| Metric | Value |

|---|---|

| Total loans | $14.2B (2025-09-30) |

| Deposits | $12.3B (2024) |

| Net interest margin | 2.78% (2025 Q3) |

| Nonperforming assets | 0.45% (2025 Q3) |

| Stress loss (severe) | 6.2% FY2024 |

| Digital spend since 2020 | $75M+ |

| Branches / staff | 140+ / 1,800+ (2024) |

| Client touchpoints | 25,000+ (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Banner Bank Business Model Canvas you’ll receive after purchase—not a mockup or sample—and when you complete your order you’ll get this same professional, fully editable file ready for use in Word and Excel.