Banner Bank Porter's Five Forces Analysis

From Overview to Strategy Blueprint

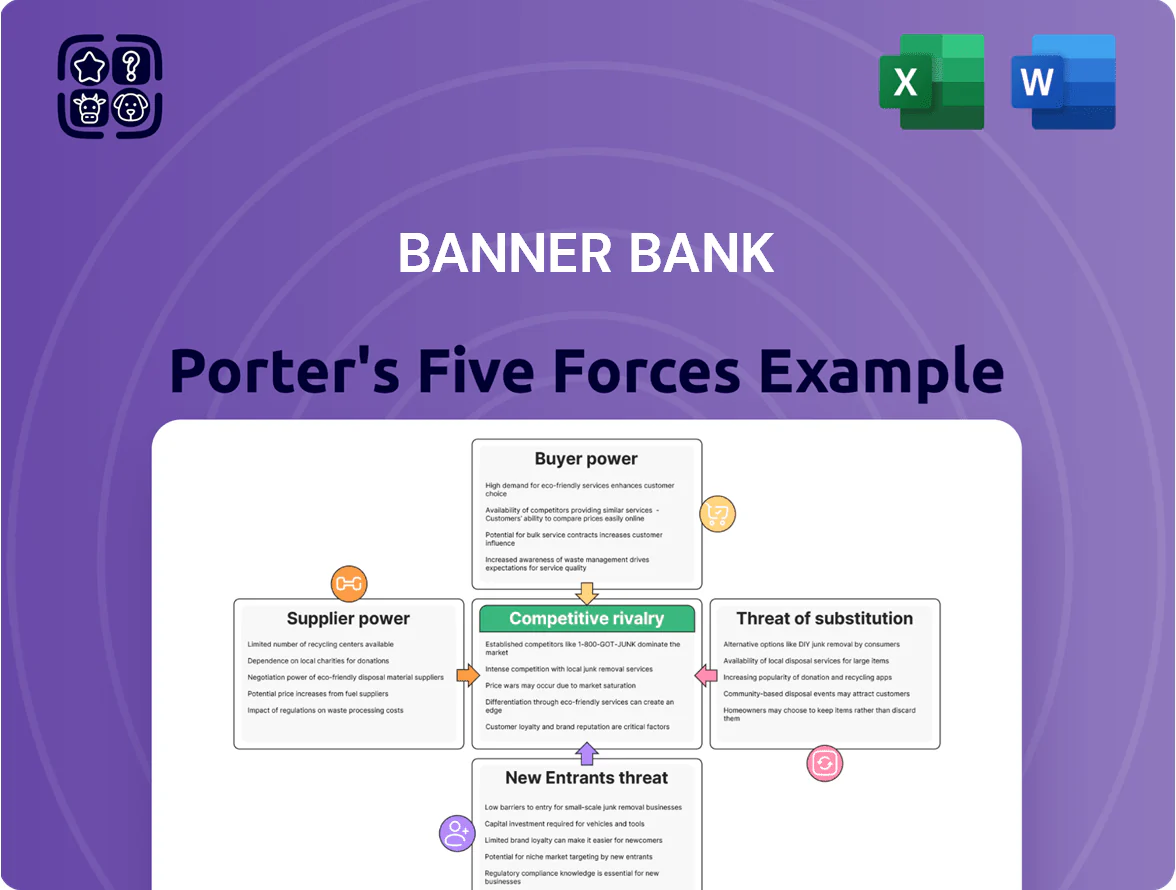

Banner Bank faces moderate competitive rivalry, rising digital disintermediation risks, and concentrated buyer power in commercial banking segments; supplier and entrant threats are manageable but shifting with fintech partnerships. This snapshot highlights key pressure points and strategic levers for growth. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations tailored to Banner Bank.

Suppliers Bargaining Power

Cost of Deposits and Liquidity Sources

Depositors are Banner Bank’s main capital suppliers; by Q4 2025 rising market rates (U.S. 10-year Treasury ~4.5% in Dec 2025) pushed retail and commercial customers to demand higher yields, lifting Banner’s deposit cost—net interest margin pressure rose as average deposit rates climbed toward 1.8–2.2% vs. 1.1% a year earlier.

Technology and Core Banking Infrastructure Providers

Banner Bank depends on third-party vendors for core processing, cybersecurity, and digital platforms, and top providers like Fiserv and Jack Henry hold strong leverage because switching costs often exceed $50M and take 12–24+ months to execute.

Those vendors can set terms on software updates, SLAs, and API access, directly affecting Banner’s product rollout speed and regulatory compliance.

In 2024, bank tech outages averaged 4.2 hours per institution annually, so vendor-imposed limitations can materially harm deposit flows and digital engagement.

Access to Wholesale Funding and Federal Markets

The Federal Home Loan Bank system and the Federal Reserve function as secondary liquidity suppliers that set a floor on borrowing costs; as of Q4 2025 the FHLB advance rates tracked roughly 25–75bps above the fed funds effective rate, constraining Banner Bank’s short-term funding cost. When loan originations exceed deposit growth—Banner’s loan-to-deposit ratio rose to about 83% in 2024—reliance on these sources increases, raising exposure to Fed rate moves. Their non-negotiable terms create concentrated supplier power that compresses Banner’s net interest margin (NIM), which fell to 2.5% in 2024 from 3.1% in 2022.

Specialized Human Capital and Labor Market

The supply of skilled financial professionals, especially in commercial lending and digital transformation, stays tight through 2025; Banner Bank competes with JPMorgan Chase, Bank of America, and Big Tech, so recruiters and top performers hold strong bargaining leverage.

Wage inflation in banking rose ~5.4% in 2024 and specialized compliance hires command premiums of 10–20%, increasing supplier power and pushing Banner to raise pay or offer retention bonuses.

- Skilled labor tight through 2025

- 2024 banking wage inflation ~5.4%

- Compliance hire premium 10–20%

- Competes with national banks + tech firms

Regulatory and Compliance Oversight Bodies

Regulatory agencies supply the non-negotiable legal framework and licenses Banner Bank needs to operate, effectively acting as fixed suppliers of operational constraints.

Capital adequacy rules—like the Basel III‑derived CET1 ratios and FDIC assessment metrics—force Banner to hold capital that limits return on equity; as of Q4 2025 the US average CET1 for large banks was ~12.5%.

Compliance standards (AML, BSA, CRA) create ongoing costs and process constraints; major federal law shifts can require immediate, costly changes to Banner’s business model or capital structure.

- Regulators = nontraditional suppliers

- Capital rules fix minimum equity (CET1 ~12–13%)

- Compliance raises fixed costs

- Law changes cause sudden, costly adjustments

Supplier pressures bite: higher deposit rates, costly vendors, funding spreads, wage inflation

Suppliers wield medium-high power: depositors pushed Banner’s deposit cost up (avg rates ~1.8–2.2% in Dec 2025 vs 1.1% a year earlier), core vendors (Fiserv, Jack Henry) have high switching costs (~$50M, 12–24+ months), FHLB/Fed funding adds non-negotiable spreads (FHLB 25–75bps over fed funds), and skilled labor/wage inflation (~5.4% in 2024) raises hiring costs.

| Supplier | Key metric |

|---|---|

| Depositors | Rates 1.8–2.2% (Dec 2025) |

| Vendors | Switch cost ~$50M; 12–24+ months |

| FHLB/Fed | Spread 25–75bps (Q4 2025) |

| Labor | Wage inflation 5.4% (2024) |

What is included in the product

Tailored exclusively for Banner Bank, this Porter's Five Forces analysis uncovers key competitive drivers, customer and supplier influence, and market entry risks while identifying disruptive threats and substitutes that could erode market share.

A concise Banner Bank Porter's Five Forces one-sheet that highlights competitive pressures and strategic levers—ideal for quick boardroom decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs for Retail Consumers

Retail customers in 2025 face low switching costs thanks to digital account opening and automated switching services; a 2024 UK CMA-style study showed 60% of consumers would switch banks for 50 bps higher rates, and US fintechs report account-to-account moves up 35% year-over-year. This mobility boosts customer bargaining power, pressing Banner Bank to spend more on relationship management and loyalty—expect deposit retention programs and CRM upgrades costing several million annually to avoid rapid deposit flight.

Price Sensitivity in Commercial Lending

Small and medium-sized enterprises (SMEs), Banner Bank’s core clients, show high price sensitivity: 2024 FDIC data show small business loan rate spreads averaged 1.8 percentage points, so SMEs routinely solicit multiple bids for lines and equipment financing.

Because SMEs shop rates among regional banks, credit unions, and national lenders, Banner must compete on interest and fees, squeezing net interest margins (Banner reported a 2.45% NIM in 2024) and compressing loan profitability.

Expectations for Advanced Digital Integration

Modern customers expect digital experiences like top tech apps, making seamless mobile and API services table stakes; 70% of US consumers used mobile banking in 2024, so digital gaps cost deposits.

If Banner Bank lags, customers shift to neobanks or big banks—Chime, Ally, and JPMorgan spent $1.2B+ on digital R&D in 2023—raising churn risk and diluting fee income.

Information Transparency and Rate Comparison Tools

The rise of online aggregators and comparison tools lets customers track rates in real time; 72% of US consumers used comparison sites for financial products in 2024, so Banner Bank faces informed clients who spot rate gaps instantly.

That visibility means Banner must match or beat market yields—between 2023–2025 regional banks raised deposit rates by ~150–300 bps—or risk deposits shifting quickly.

- 72% of consumers used comparison sites in 2024

- Regional banks raised rates ~150–300 bps (2023–25)

- Real-time transparency reduces switching frictions

- Forces faster, dynamic pricing to retain deposits

Concentration of Large Commercial Accounts

Customer power surges: mobile churn, SME rate shopping and big-account liquidity squeeze

Customers have strong bargaining power: retail mobility and 70% mobile use (2024) raise churn; SMEs shop rates—small-business loan spreads averaged 1.8 pp (2024); Banner’s $12.3B deposits (2025) mean large accounts (200–500M) can move liquidity and margins; real-time rate transparency (72% comparison use, 2024) forces dynamic pricing and CRM/digital spend.

| Metric | Value |

|---|---|

| Banner deposits (2025) | $12.3B |

| Mobile banking use (2024) | 70% |

| Comparison sites (2024) | 72% |

| SME loan spread (2024) | 1.8 pp |

Same Document Delivered

Banner Bank Porter's Five Forces Analysis

This preview shows the exact Banner Bank Porter's Five Forces analysis you'll receive—no mockups or samples—fully formatted and ready for instant download after purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Banner Bank faces moderate competitive rivalry, rising digital disintermediation risks, and concentrated buyer power in commercial banking segments; supplier and entrant threats are manageable but shifting with fintech partnerships. This snapshot highlights key pressure points and strategic levers for growth. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations tailored to Banner Bank.

Suppliers Bargaining Power

Cost of Deposits and Liquidity Sources

Depositors are Banner Bank’s main capital suppliers; by Q4 2025 rising market rates (U.S. 10-year Treasury ~4.5% in Dec 2025) pushed retail and commercial customers to demand higher yields, lifting Banner’s deposit cost—net interest margin pressure rose as average deposit rates climbed toward 1.8–2.2% vs. 1.1% a year earlier.

Technology and Core Banking Infrastructure Providers

Banner Bank depends on third-party vendors for core processing, cybersecurity, and digital platforms, and top providers like Fiserv and Jack Henry hold strong leverage because switching costs often exceed $50M and take 12–24+ months to execute.

Those vendors can set terms on software updates, SLAs, and API access, directly affecting Banner’s product rollout speed and regulatory compliance.

In 2024, bank tech outages averaged 4.2 hours per institution annually, so vendor-imposed limitations can materially harm deposit flows and digital engagement.

Access to Wholesale Funding and Federal Markets

The Federal Home Loan Bank system and the Federal Reserve function as secondary liquidity suppliers that set a floor on borrowing costs; as of Q4 2025 the FHLB advance rates tracked roughly 25–75bps above the fed funds effective rate, constraining Banner Bank’s short-term funding cost. When loan originations exceed deposit growth—Banner’s loan-to-deposit ratio rose to about 83% in 2024—reliance on these sources increases, raising exposure to Fed rate moves. Their non-negotiable terms create concentrated supplier power that compresses Banner’s net interest margin (NIM), which fell to 2.5% in 2024 from 3.1% in 2022.

Specialized Human Capital and Labor Market

The supply of skilled financial professionals, especially in commercial lending and digital transformation, stays tight through 2025; Banner Bank competes with JPMorgan Chase, Bank of America, and Big Tech, so recruiters and top performers hold strong bargaining leverage.

Wage inflation in banking rose ~5.4% in 2024 and specialized compliance hires command premiums of 10–20%, increasing supplier power and pushing Banner to raise pay or offer retention bonuses.

- Skilled labor tight through 2025

- 2024 banking wage inflation ~5.4%

- Compliance hire premium 10–20%

- Competes with national banks + tech firms

Regulatory and Compliance Oversight Bodies

Regulatory agencies supply the non-negotiable legal framework and licenses Banner Bank needs to operate, effectively acting as fixed suppliers of operational constraints.

Capital adequacy rules—like the Basel III‑derived CET1 ratios and FDIC assessment metrics—force Banner to hold capital that limits return on equity; as of Q4 2025 the US average CET1 for large banks was ~12.5%.

Compliance standards (AML, BSA, CRA) create ongoing costs and process constraints; major federal law shifts can require immediate, costly changes to Banner’s business model or capital structure.

- Regulators = nontraditional suppliers

- Capital rules fix minimum equity (CET1 ~12–13%)

- Compliance raises fixed costs

- Law changes cause sudden, costly adjustments

Supplier pressures bite: higher deposit rates, costly vendors, funding spreads, wage inflation

Suppliers wield medium-high power: depositors pushed Banner’s deposit cost up (avg rates ~1.8–2.2% in Dec 2025 vs 1.1% a year earlier), core vendors (Fiserv, Jack Henry) have high switching costs (~$50M, 12–24+ months), FHLB/Fed funding adds non-negotiable spreads (FHLB 25–75bps over fed funds), and skilled labor/wage inflation (~5.4% in 2024) raises hiring costs.

| Supplier | Key metric |

|---|---|

| Depositors | Rates 1.8–2.2% (Dec 2025) |

| Vendors | Switch cost ~$50M; 12–24+ months |

| FHLB/Fed | Spread 25–75bps (Q4 2025) |

| Labor | Wage inflation 5.4% (2024) |

What is included in the product

Tailored exclusively for Banner Bank, this Porter's Five Forces analysis uncovers key competitive drivers, customer and supplier influence, and market entry risks while identifying disruptive threats and substitutes that could erode market share.

A concise Banner Bank Porter's Five Forces one-sheet that highlights competitive pressures and strategic levers—ideal for quick boardroom decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs for Retail Consumers

Retail customers in 2025 face low switching costs thanks to digital account opening and automated switching services; a 2024 UK CMA-style study showed 60% of consumers would switch banks for 50 bps higher rates, and US fintechs report account-to-account moves up 35% year-over-year. This mobility boosts customer bargaining power, pressing Banner Bank to spend more on relationship management and loyalty—expect deposit retention programs and CRM upgrades costing several million annually to avoid rapid deposit flight.

Price Sensitivity in Commercial Lending

Small and medium-sized enterprises (SMEs), Banner Bank’s core clients, show high price sensitivity: 2024 FDIC data show small business loan rate spreads averaged 1.8 percentage points, so SMEs routinely solicit multiple bids for lines and equipment financing.

Because SMEs shop rates among regional banks, credit unions, and national lenders, Banner must compete on interest and fees, squeezing net interest margins (Banner reported a 2.45% NIM in 2024) and compressing loan profitability.

Expectations for Advanced Digital Integration

Modern customers expect digital experiences like top tech apps, making seamless mobile and API services table stakes; 70% of US consumers used mobile banking in 2024, so digital gaps cost deposits.

If Banner Bank lags, customers shift to neobanks or big banks—Chime, Ally, and JPMorgan spent $1.2B+ on digital R&D in 2023—raising churn risk and diluting fee income.

Information Transparency and Rate Comparison Tools

The rise of online aggregators and comparison tools lets customers track rates in real time; 72% of US consumers used comparison sites for financial products in 2024, so Banner Bank faces informed clients who spot rate gaps instantly.

That visibility means Banner must match or beat market yields—between 2023–2025 regional banks raised deposit rates by ~150–300 bps—or risk deposits shifting quickly.

- 72% of consumers used comparison sites in 2024

- Regional banks raised rates ~150–300 bps (2023–25)

- Real-time transparency reduces switching frictions

- Forces faster, dynamic pricing to retain deposits

Concentration of Large Commercial Accounts

Customer power surges: mobile churn, SME rate shopping and big-account liquidity squeeze

Customers have strong bargaining power: retail mobility and 70% mobile use (2024) raise churn; SMEs shop rates—small-business loan spreads averaged 1.8 pp (2024); Banner’s $12.3B deposits (2025) mean large accounts (200–500M) can move liquidity and margins; real-time rate transparency (72% comparison use, 2024) forces dynamic pricing and CRM/digital spend.

| Metric | Value |

|---|---|

| Banner deposits (2025) | $12.3B |

| Mobile banking use (2024) | 70% |

| Comparison sites (2024) | 72% |

| SME loan spread (2024) | 1.8 pp |

Same Document Delivered

Banner Bank Porter's Five Forces Analysis

This preview shows the exact Banner Bank Porter's Five Forces analysis you'll receive—no mockups or samples—fully formatted and ready for instant download after purchase.