Banorte Porter's Five Forces Analysis

From Overview to Strategy Blueprint

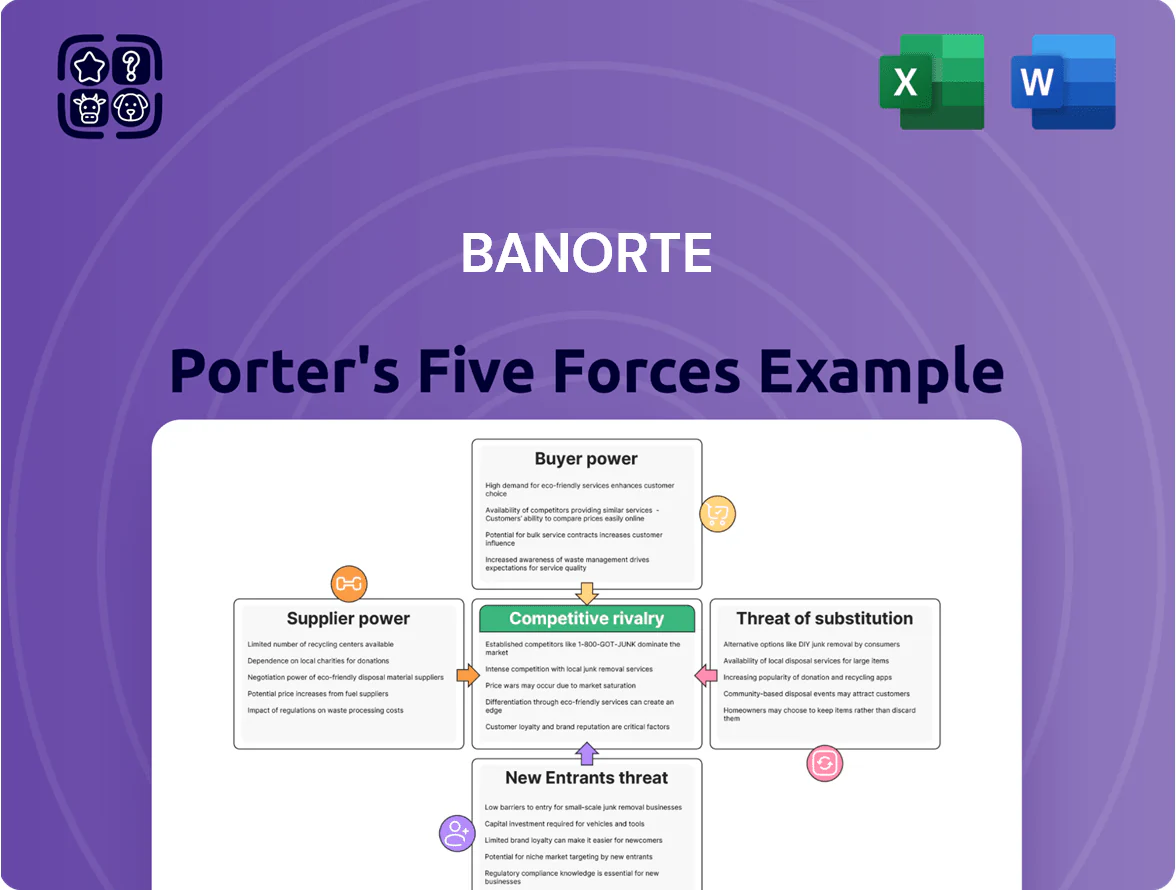

Banorte operates in a highly regulated, capital-intensive banking sector where intense rivalry, strong buyer bargaining from corporates and retail clients, and moderate supplier power shape margins and growth prospects.

Threats from fintech disruptors and substitutes are rising, while barriers to entry remain significant—favoring incumbents but forcing innovation and efficiency plays.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Banorte’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Highly Skilled Financial and Tech Talent

Competition for specialized labor in Mexico is intense as traditional banks shift to digital-first models, and Banorte must vie with global fintechs and multinational banks for software engineers, data scientists, and risk experts.

High-quality talent commands strong bargaining power over wages and benefits; median tech salaries in Mexico rose about 18% from 2022–2024, and top data scientists saw offers north of MXN 1.8m annually by end-2025.

This talent squeeze increases Banorte’s labor cost pressure and retention spending, raising operating expenses and strategic risk if hiring keeps pace with digital transformation.

Dependence on Global Technology and Cloud Infrastructure

Banorte depends on a few global vendors for cloud, cybersecurity, and core banking software, giving suppliers strong leverage; top cloud providers account for over 70% of market share worldwide (AWS, Microsoft, Google) as of 2024.

These services are mission-critical for uptime and digital transformation, so vendors can push higher fees and stricter terms; operational outages risk revenue hits—Mexican banks lost an estimated MXN 2.1bn in 2023 to IT incidents.

Switching vendors entails high migration costs and technical risk: a conservative estimate for replatforming core systems runs USD 50–150m and 18–36 months, which locks Banorte into existing supplier terms.

Influence of Regulatory Bodies and Central Bank Policies

The Banco de México and CNBV act as institutional suppliers of Banorte’s operating rules and liquidity; Banco de México raised the policy rate to 11.25% in Dec 2023 and reserve requirements stood at ~1.5% for MXN deposits in 2025, directly lifting Banorte’s funding costs and net interest margin pressures.

Cost of Wholesale Funding and Capital Markets

Banorte's strong retail deposit base covers much funding, but in 2025 it still tapped local and international capital markets—issuing MXN and USD bonds—to diversify funding; the bank reported roughly 18% of liabilities as wholesale funding in FY2024.

Large institutional holders can push yields higher if Mexican sovereign spreads widen: Mexico 10y CDS moved from ~60bps in Jan 2024 to ~95bps in mid‑2025, so market sentiment acts as a liquidity supplier with moderate bargaining power.

- Wholesale funding ≈18% of liabilities (FY2024)

- Mexico 10y CDS: ~60bps (Jan 2024) → ~95bps (mid‑2025)

- Reliance on bond markets = moderate supplier power

Physical Security and Logistics Infrastructure

Maintaining Banorte’s ~1,400 branches and ~7,500 ATMs (2024) needs specialized armored transport and security; in Mexico three to five major firms dominate high‑security logistics, giving them localized bargaining power.

Any service disruption or price rise—say a 10% jump in armored-transport fees—would raise Banorte’s nationwide OPEX materially given cash-handling scale; contract concentration increases switching costs and operational risk.

- ~1,400 branches, ~7,500 ATMs (2024)

- 3–5 dominant armored carriers nationwide

- 10% cost rise → notable OPEX impact

Suppliers squeeze margins: rising tech pay, cloud dominance, funding & replatform costs

Suppliers hold moderate-to-high bargaining power: tech talent shortages (median tech pay +18% 2022–24; top data scientists >MXN1.8m/yr by end-2025), cloud vendors >70% global share (AWS/MSFT/Google), wholesale funding ~18% liabilities (FY2024) and Mexico 10y CDS ~95bps mid-2025 raise costs; switching core systems ≈USD50–150m and 18–36 months, armored transport concentrated (3–5 firms) so cost shocks hit OPEX.

| Metric | Value |

|---|---|

| Tech pay rise | +18% (2022–24) |

| Top data scientist pay | >MXN1.8m (end-2025) |

| Cloud market share (top3) | >70% (2024) |

| Wholesale funding | ≈18% liabilities (FY2024) |

| Mexico 10y CDS | ~95bps (mid-2025) |

| Replatform cost/time | USD50–150m; 18–36 months |

| Branches/ATMs | ~1,400 / ~7,500 (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Banorte, uncovering competitive pressures, customer and supplier influence, entry barriers, substitutes, and emerging threats that shape its market position and profitability.

Concise Porter's Five Forces for Banorte—one-sheet clarity to speed strategic decisions and flag key competitive pressures.

Customers Bargaining Power

Lower Switching Costs for Retail Customers

The rise of digital banking and mobile portability in Mexico has cut switching friction: 78% of Mexican adults used mobile banking in 2024 and fintech onboarding times average under 10 minutes, so customers can open or close accounts within minutes via apps. This reduces branch-driven loyalty and pressures Banorte to match market-leading deposit rates (eg. top savings promos of ~6% in 2024) and invest in UX to retain retail clients.

High Negotiating Leverage of Government and Corporate Clients

Banorte is a primary lender to the Mexican federal and state governments and to large domestic firms, with public-sector and corporate loans representing about 28% of gross loans as of Q4 2025, giving those clients strong price leverage.

These counterparties can demand bespoke rates and service terms because large deposits and syndicated-credit lines are material to Banorte’s NII (net interest income); losing one major government contract could cut interest income by several percentage points.

Increased Transparency and Price Comparison Tools

Demand for Integrated Digital Ecosystems

Modern customers expect banks to offer integrated services—insurance, brokerage, rewards—so Banorte must bundle beyond savings to retain clients; 2024 BBVA/Statista data show 62% of Mexican adults prefer one platform for banking plus adjacent services.

If Banorte lags, customers switch to fintechs: Mexican fintechs grew 18% in users in 2023, and niche platforms report 25–40% higher NPS in insurance or investing segments.

This raises pressure to innovate: Banorte needs continuous product bundling and API partnerships to defend share and keep cross-sell rates above its 2024 industry peers' ~1.8 products per customer.

Impact of Financial Inclusion and Literacy Programs

Banorte must boost service and education spend; for example, shifting 0.5–1.0% of revenue to CX and financial literacy programs could cut annual churn by an estimated 10–15% among new entrants.

Failure to act risks migration to agile competitors offering lower fees and faster onboarding, especially as 42% of new account holders cite digital ease as their top choice in 2024 surveys.

- 68% account ownership (2023)

- 42% prioritize digital ease (2024)

- Target: 0.5–1.0% revenue to CX/education

- Potential churn cut: 10–15%

Banorte under pressure: digital-first customers, fintechs squeeze spreads—invest in CX now

Customers have rising power: 78% used mobile banking in 2024, 42% cite digital ease as top choice, and 60% compare 3+ providers; price transparency and fintechs (18% user growth 2023) pressure Banorte’s spreads (~3.1% retail loan spread in 2024). Banorte must match rates, bundle services, and invest ~0.5–1.0% revenue in CX to cut churn 10–15%.

| Metric | Value |

|---|---|

| Mobile banking (2024) | 78% |

| Prioritize digital (2024) | 42% |

| Fintech user growth (2023) | 18% |

| Retail loan spread (2024) | 3.1% |

Same Document Delivered

Banorte Porter's Five Forces Analysis

This preview shows the exact Banorte Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; it's the full, professionally formatted document ready for download and use.

The analysis covers rivalry, supplier and buyer power, threats of new entrants and substitutes, with concise findings and actionable implications tailored to Banorte's competitive landscape; what you see is the final file you'll get instantly after buying.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Banorte operates in a highly regulated, capital-intensive banking sector where intense rivalry, strong buyer bargaining from corporates and retail clients, and moderate supplier power shape margins and growth prospects.

Threats from fintech disruptors and substitutes are rising, while barriers to entry remain significant—favoring incumbents but forcing innovation and efficiency plays.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Banorte’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Highly Skilled Financial and Tech Talent

Competition for specialized labor in Mexico is intense as traditional banks shift to digital-first models, and Banorte must vie with global fintechs and multinational banks for software engineers, data scientists, and risk experts.

High-quality talent commands strong bargaining power over wages and benefits; median tech salaries in Mexico rose about 18% from 2022–2024, and top data scientists saw offers north of MXN 1.8m annually by end-2025.

This talent squeeze increases Banorte’s labor cost pressure and retention spending, raising operating expenses and strategic risk if hiring keeps pace with digital transformation.

Dependence on Global Technology and Cloud Infrastructure

Banorte depends on a few global vendors for cloud, cybersecurity, and core banking software, giving suppliers strong leverage; top cloud providers account for over 70% of market share worldwide (AWS, Microsoft, Google) as of 2024.

These services are mission-critical for uptime and digital transformation, so vendors can push higher fees and stricter terms; operational outages risk revenue hits—Mexican banks lost an estimated MXN 2.1bn in 2023 to IT incidents.

Switching vendors entails high migration costs and technical risk: a conservative estimate for replatforming core systems runs USD 50–150m and 18–36 months, which locks Banorte into existing supplier terms.

Influence of Regulatory Bodies and Central Bank Policies

The Banco de México and CNBV act as institutional suppliers of Banorte’s operating rules and liquidity; Banco de México raised the policy rate to 11.25% in Dec 2023 and reserve requirements stood at ~1.5% for MXN deposits in 2025, directly lifting Banorte’s funding costs and net interest margin pressures.

Cost of Wholesale Funding and Capital Markets

Banorte's strong retail deposit base covers much funding, but in 2025 it still tapped local and international capital markets—issuing MXN and USD bonds—to diversify funding; the bank reported roughly 18% of liabilities as wholesale funding in FY2024.

Large institutional holders can push yields higher if Mexican sovereign spreads widen: Mexico 10y CDS moved from ~60bps in Jan 2024 to ~95bps in mid‑2025, so market sentiment acts as a liquidity supplier with moderate bargaining power.

- Wholesale funding ≈18% of liabilities (FY2024)

- Mexico 10y CDS: ~60bps (Jan 2024) → ~95bps (mid‑2025)

- Reliance on bond markets = moderate supplier power

Physical Security and Logistics Infrastructure

Maintaining Banorte’s ~1,400 branches and ~7,500 ATMs (2024) needs specialized armored transport and security; in Mexico three to five major firms dominate high‑security logistics, giving them localized bargaining power.

Any service disruption or price rise—say a 10% jump in armored-transport fees—would raise Banorte’s nationwide OPEX materially given cash-handling scale; contract concentration increases switching costs and operational risk.

- ~1,400 branches, ~7,500 ATMs (2024)

- 3–5 dominant armored carriers nationwide

- 10% cost rise → notable OPEX impact

Suppliers squeeze margins: rising tech pay, cloud dominance, funding & replatform costs

Suppliers hold moderate-to-high bargaining power: tech talent shortages (median tech pay +18% 2022–24; top data scientists >MXN1.8m/yr by end-2025), cloud vendors >70% global share (AWS/MSFT/Google), wholesale funding ~18% liabilities (FY2024) and Mexico 10y CDS ~95bps mid-2025 raise costs; switching core systems ≈USD50–150m and 18–36 months, armored transport concentrated (3–5 firms) so cost shocks hit OPEX.

| Metric | Value |

|---|---|

| Tech pay rise | +18% (2022–24) |

| Top data scientist pay | >MXN1.8m (end-2025) |

| Cloud market share (top3) | >70% (2024) |

| Wholesale funding | ≈18% liabilities (FY2024) |

| Mexico 10y CDS | ~95bps (mid-2025) |

| Replatform cost/time | USD50–150m; 18–36 months |

| Branches/ATMs | ~1,400 / ~7,500 (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Banorte, uncovering competitive pressures, customer and supplier influence, entry barriers, substitutes, and emerging threats that shape its market position and profitability.

Concise Porter's Five Forces for Banorte—one-sheet clarity to speed strategic decisions and flag key competitive pressures.

Customers Bargaining Power

Lower Switching Costs for Retail Customers

The rise of digital banking and mobile portability in Mexico has cut switching friction: 78% of Mexican adults used mobile banking in 2024 and fintech onboarding times average under 10 minutes, so customers can open or close accounts within minutes via apps. This reduces branch-driven loyalty and pressures Banorte to match market-leading deposit rates (eg. top savings promos of ~6% in 2024) and invest in UX to retain retail clients.

High Negotiating Leverage of Government and Corporate Clients

Banorte is a primary lender to the Mexican federal and state governments and to large domestic firms, with public-sector and corporate loans representing about 28% of gross loans as of Q4 2025, giving those clients strong price leverage.

These counterparties can demand bespoke rates and service terms because large deposits and syndicated-credit lines are material to Banorte’s NII (net interest income); losing one major government contract could cut interest income by several percentage points.

Increased Transparency and Price Comparison Tools

Demand for Integrated Digital Ecosystems

Modern customers expect banks to offer integrated services—insurance, brokerage, rewards—so Banorte must bundle beyond savings to retain clients; 2024 BBVA/Statista data show 62% of Mexican adults prefer one platform for banking plus adjacent services.

If Banorte lags, customers switch to fintechs: Mexican fintechs grew 18% in users in 2023, and niche platforms report 25–40% higher NPS in insurance or investing segments.

This raises pressure to innovate: Banorte needs continuous product bundling and API partnerships to defend share and keep cross-sell rates above its 2024 industry peers' ~1.8 products per customer.

Impact of Financial Inclusion and Literacy Programs

Banorte must boost service and education spend; for example, shifting 0.5–1.0% of revenue to CX and financial literacy programs could cut annual churn by an estimated 10–15% among new entrants.

Failure to act risks migration to agile competitors offering lower fees and faster onboarding, especially as 42% of new account holders cite digital ease as their top choice in 2024 surveys.

- 68% account ownership (2023)

- 42% prioritize digital ease (2024)

- Target: 0.5–1.0% revenue to CX/education

- Potential churn cut: 10–15%

Banorte under pressure: digital-first customers, fintechs squeeze spreads—invest in CX now

Customers have rising power: 78% used mobile banking in 2024, 42% cite digital ease as top choice, and 60% compare 3+ providers; price transparency and fintechs (18% user growth 2023) pressure Banorte’s spreads (~3.1% retail loan spread in 2024). Banorte must match rates, bundle services, and invest ~0.5–1.0% revenue in CX to cut churn 10–15%.

| Metric | Value |

|---|---|

| Mobile banking (2024) | 78% |

| Prioritize digital (2024) | 42% |

| Fintech user growth (2023) | 18% |

| Retail loan spread (2024) | 3.1% |

Same Document Delivered

Banorte Porter's Five Forces Analysis

This preview shows the exact Banorte Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; it's the full, professionally formatted document ready for download and use.

The analysis covers rivalry, supplier and buyer power, threats of new entrants and substitutes, with concise findings and actionable implications tailored to Banorte's competitive landscape; what you see is the final file you'll get instantly after buying.