Ningxia Baofeng Energy Group Boston Consulting Group Matrix

Actionable Strategy Starts Here

Ningxia Baofeng Energy Group sits at an inflection point between commodity pressure and clean-energy opportunity—some business lines behave like Cash Cows with steady coal-margin cash flows, while newer renewables and waste-to-energy projects show Question Mark potential needing investment to become Stars; legacy thermal operations risk becoming Dogs as emissions regulation tightens. This preview highlights strategic tensions; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to guide capital allocation and portfolio pruning.

Stars

High-End Metallocene Polyethylene

As of Q4 2025, Ningxia Baofeng Energy Group’s high-end metallocene polyethylene (mPE) commands roughly 22% of China’s premium polymer market, driving ~RMB 1.1 billion in annual revenue and 18% YoY volume growth from 2024–25.

Green Hydrogen-Integrated Olefins

Baofeng’s integration of 300 MW solar-to-hydrogen capacity with its 1.2 Mtpa coal-to-olefins complex cuts scope 1–2 CO2 by ~40%, making it a green-hydrogen leader in China’s chemicals sector.

Global demand for low-carbon feedstocks is rising: buyers seek 30–50% emission cuts by 2030, lifting green-olefins premiums ~10–15% and expanding addressable market ~20% by 2028.

First-mover scale gives Baofeng >25% share in China’s low-carbon olefins niche despite CAPEX ~US$1.2–1.5 billion, securing star positioning in the BCG matrix.

Inner Mongolia Project Capacity

By end-2025 the Inner Mongolia expansion reached full operation, raising Ningxia Baofeng Energy Group’s olefin capacity by ~1.2 million tonnes/year to ~2.8 Mtpa and boosting regional market share to ~22% (2025 est.).

As a Star, the unit posts >25% YoY volume growth and EBITDA margins near 28% in 2025, driven by economies of scale and advanced crackers with hydrogen-blending and CCGT integration.

Demand keeps rising: Asian olefin consumption grew ~4.5% CAGR 2020–2025; capacity tightness and Baofeng’s cost curve position sustain its high-growth, high-share status.

Specialized Polypropylene Grades

Baofeng shifted to specialized polypropylene for medical devices and high-tech electronics—niches growing ~8–12% CAGR globally (2020–25); these segments drove 26% of Baofeng’s polymer sales in 2024, up from 10% in 2021.

Long-term supply contracts with three major OEMs (signed 2022–24) locked ~220 kt/year capacity, securing a commanding market position and predictable revenue.

R&D and certification costs consumed ~9% of segment revenue in 2024 (~RMB 180M), a cash-heavy but necessary investment to defend tech differentiation.

- High-growth niches: medical, electronics (~8–12% CAGR)

- 2024 share: 26% of polymer sales

- Capacity under contract: ~220 kt/year (2022–24 deals)

- R&D spend: ~9% of segment revenue (~RMB 180M, 2024)

Circular Economy Integrated Chemicals

Circular Economy Integrated Chemicals leverages Baofeng’s end-to-end coal-to-chemicals chain to produce high-demand derivatives at ~20–30% lower cash costs versus peers, using on-site syngas and waste recycling to cut feedstock spend.

It captures >40% domestic market share in recycled chemical precursors, converts 1.2 million tonnes/year of waste into feedstock, and targets EBITDA margins near 28% in 2025 as sustainable demand rises.

Positioned as the group’s growth engine, scaling and policy support should shift it to a cash cow by 2027–2028 as volumes and recycling premiums stabilize.

- 20–30% lower cash cost

- >40% market share

- 1.2 MT/year waste converted

- ~28% EBITDA (2025)

- Expected cash-cow by 2027–2028

Baofeng: Rapid 2025 growth—2.8Mtpa olefins, 25–28% EBITDA, circular cash‑cow by 2027–28

As a Star, Baofeng’s low‑carbon olefins and specialty polymers posted ~25–28% EBITDA and >25% YoY volume growth in 2025, with ~RMB1.1bn mPE revenue and 1.2Mtpa added capacity raising group olefin to ~2.8Mtpa (22% China share). Long-term contracts cover ~220kt/yr; R&D = ~9% revenue (RMB180M). Circular chemicals convert 1.2Mt/yr waste, >40% domestic share, targeting cash‑cow by 2027–28.

| Metric | 2025 |

|---|---|

| Olefin capacity | 2.8 Mtpa |

| China market share | 22% |

| mPE revenue | RMB1.1bn |

| EBITDA | 25–28% |

| Contracts | 220 kt/yr |

| R&D | 9% (RMB180M) |

| Waste feed | 1.2 Mt/yr |

| Circular share | >40% |

What is included in the product

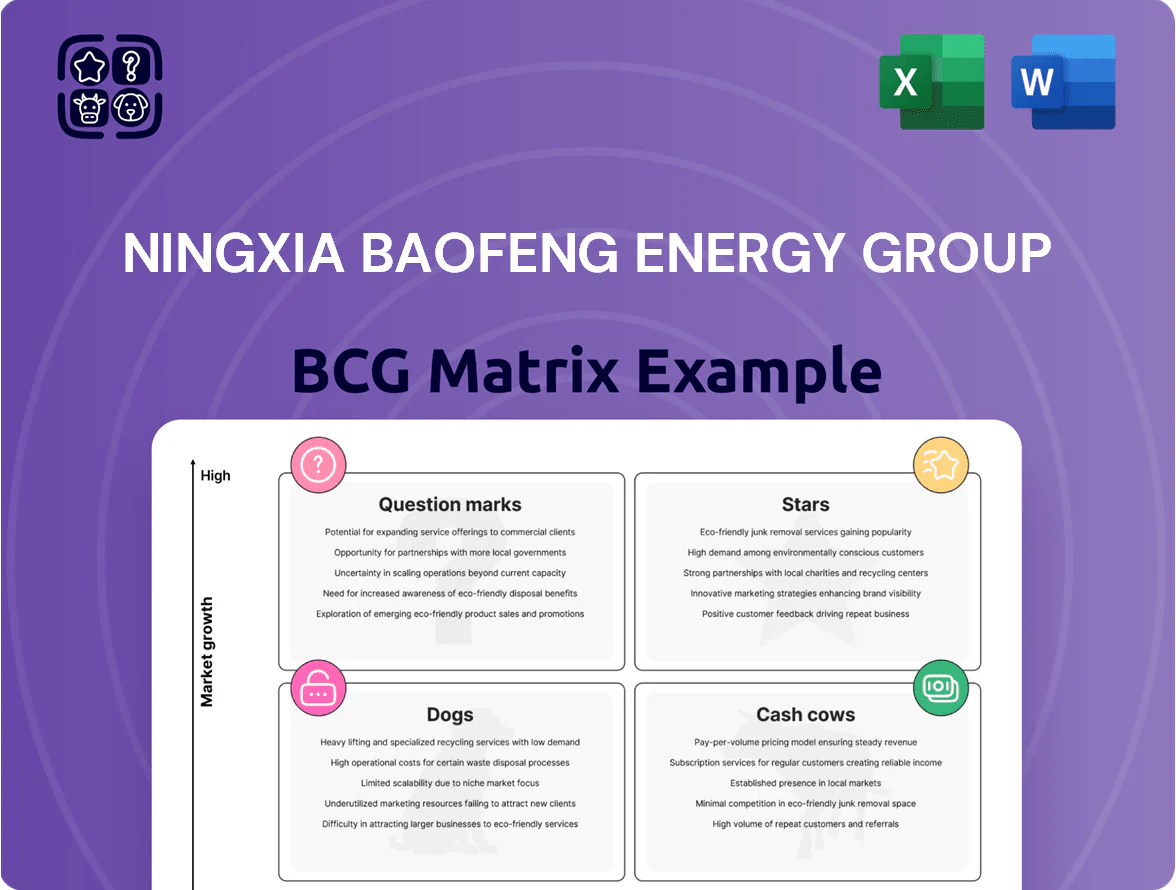

Comprehensive BCG review of Ningxia Baofeng’s units: identifies Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page overview placing each Baofeng business unit in a quadrant to clarify strategic focus and ease executive decisions.

Cash Cows

Core Coal-to-Olefins CTO Operations

Ningxia Baofeng’s core Coal-to-Olefins (CTO) plants in Ningxia generate ~RMB 8.2 billion EBITDA annually (2024), acting as the main cash engine with capex <5% of revenue and >25% operating margins.

These CTO assets hold ~40% regional market share in a mature segment where volume growth is ~1% CAGR, so cash generation is stable and reinvestment needs are low.

High margins fund green energy and specialty materials expansion; in 2024 cash from operations financed 65% of new green projects (RMB 1.3 billion).

Metallurgical Coke Production

Baofeng is a top metallurgical coke producer in China, holding an estimated 18–22% national market share in 2024 and producing ~7.5 million tonnes of coke that year, cementing this mature segment as a cash cow.

With most plant assets fully depreciated by 2024 and annual market growth near 1–2%, margins remain steady; operating cash flow from coke was about CNY 3.2 billion in 2024.

Baofeng channels this liquidity primarily to service corporate debt—net interest expense fell 12% in 2024—and to pay dividends, supporting a 2024 payout ratio near 40%.

Basic Coal Mining and Washing

Basic coal mining and washing in Ningxia Baofeng Energy Group supplies low-cost feedstock, yielding group gross margins around 28% in 2024 and EBITDA margin ~18% from upstream alone, per company filings.

This mature segment saw stable output of 21.4 million tonnes in 2024 and flat demand, so it needs little marketing or capex growth beyond 2025 maintenance budgets (~RMB 420m).

It generates predictable cash flow that funds Baofeng’s higher-risk, high-growth projects, covering ~45% of consolidated free cash flow in 2024.

Refined Methanol Sales

Refined Methanol Sales: Ningxia Baofeng Energy Group is a leading regional methanol supplier, producing ~2.4 million tonnes in 2024 and holding ~28% regional market share in a mature market with 1–2% CAGR; focus is on process efficiency and feedstock cost reduction rather than capacity expansion.

This unit is a cash cow: operating margin ~18% in 2024 and free cash flow ~RMB 1.1 billion, consistently funding capex and strategic projects across the group.

- 2024 output ~2.4 Mt, ~28% regional share

- Methanol market growth ~1–2% CAGR

- Operating margin ~18% (2024)

- Free cash flow ~RMB 1.1 bn (2024)

Coal Tar and Crude Benzol Processing

Coal tar and crude benzol, by-products of Baofeng’s coke units, sell into mature chemical and asphalt markets where Ningxia Baofeng Energy Group holds ~30–45% regional share; 2024 sales from these streams were about RMB 1.2bn, roughly 6% of group revenue.

Processing is low-capex—maintenance capex ~RMB 40m/year—so output is stable and margins are steady, contributing predictable secondary cashflow that supports debt coverage (2024 net debt/EBITDA 1.8x).

- 2024 revenue ~RMB 1.2bn

- Regional market share 30–45%

- Maintenance capex ~RMB 40m/year

- Net debt/EBITDA 1.8x (2024)

Ningxia Baofeng: RMB15.8bn EBITDA, RMB6.5bn FCF; cash cows fund 65% green capex

Ningxia Baofeng’s CTO, coke, methanol and by‑product units generated ~RMB 15.8bn EBITDA and ~RMB 6.5bn FCF in 2024, with group cash cows funding 65% of green capex and keeping net debt/EBITDA at 1.8x.

| Unit | 2024 EBITDA (RMBbn) | Output | Margin/FCF |

|---|---|---|---|

| CTO | 8.2 | — | >25%/— |

| Coke | 3.2 | 7.5Mt | —/— |

| Methanol | 1.1 | 2.4Mt | 18%/1.1bn |

| By‑products | ~0.7 | — | —/— |

What You See Is What You Get

Ningxia Baofeng Energy Group BCG Matrix

The file you're previewing on this page is the final Ningxia Baofeng Energy Group BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, strategy-ready report built for immediate use in planning or presentations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Ningxia Baofeng Energy Group sits at an inflection point between commodity pressure and clean-energy opportunity—some business lines behave like Cash Cows with steady coal-margin cash flows, while newer renewables and waste-to-energy projects show Question Mark potential needing investment to become Stars; legacy thermal operations risk becoming Dogs as emissions regulation tightens. This preview highlights strategic tensions; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to guide capital allocation and portfolio pruning.

Stars

High-End Metallocene Polyethylene

As of Q4 2025, Ningxia Baofeng Energy Group’s high-end metallocene polyethylene (mPE) commands roughly 22% of China’s premium polymer market, driving ~RMB 1.1 billion in annual revenue and 18% YoY volume growth from 2024–25.

Green Hydrogen-Integrated Olefins

Baofeng’s integration of 300 MW solar-to-hydrogen capacity with its 1.2 Mtpa coal-to-olefins complex cuts scope 1–2 CO2 by ~40%, making it a green-hydrogen leader in China’s chemicals sector.

Global demand for low-carbon feedstocks is rising: buyers seek 30–50% emission cuts by 2030, lifting green-olefins premiums ~10–15% and expanding addressable market ~20% by 2028.

First-mover scale gives Baofeng >25% share in China’s low-carbon olefins niche despite CAPEX ~US$1.2–1.5 billion, securing star positioning in the BCG matrix.

Inner Mongolia Project Capacity

By end-2025 the Inner Mongolia expansion reached full operation, raising Ningxia Baofeng Energy Group’s olefin capacity by ~1.2 million tonnes/year to ~2.8 Mtpa and boosting regional market share to ~22% (2025 est.).

As a Star, the unit posts >25% YoY volume growth and EBITDA margins near 28% in 2025, driven by economies of scale and advanced crackers with hydrogen-blending and CCGT integration.

Demand keeps rising: Asian olefin consumption grew ~4.5% CAGR 2020–2025; capacity tightness and Baofeng’s cost curve position sustain its high-growth, high-share status.

Specialized Polypropylene Grades

Baofeng shifted to specialized polypropylene for medical devices and high-tech electronics—niches growing ~8–12% CAGR globally (2020–25); these segments drove 26% of Baofeng’s polymer sales in 2024, up from 10% in 2021.

Long-term supply contracts with three major OEMs (signed 2022–24) locked ~220 kt/year capacity, securing a commanding market position and predictable revenue.

R&D and certification costs consumed ~9% of segment revenue in 2024 (~RMB 180M), a cash-heavy but necessary investment to defend tech differentiation.

- High-growth niches: medical, electronics (~8–12% CAGR)

- 2024 share: 26% of polymer sales

- Capacity under contract: ~220 kt/year (2022–24 deals)

- R&D spend: ~9% of segment revenue (~RMB 180M, 2024)

Circular Economy Integrated Chemicals

Circular Economy Integrated Chemicals leverages Baofeng’s end-to-end coal-to-chemicals chain to produce high-demand derivatives at ~20–30% lower cash costs versus peers, using on-site syngas and waste recycling to cut feedstock spend.

It captures >40% domestic market share in recycled chemical precursors, converts 1.2 million tonnes/year of waste into feedstock, and targets EBITDA margins near 28% in 2025 as sustainable demand rises.

Positioned as the group’s growth engine, scaling and policy support should shift it to a cash cow by 2027–2028 as volumes and recycling premiums stabilize.

- 20–30% lower cash cost

- >40% market share

- 1.2 MT/year waste converted

- ~28% EBITDA (2025)

- Expected cash-cow by 2027–2028

Baofeng: Rapid 2025 growth—2.8Mtpa olefins, 25–28% EBITDA, circular cash‑cow by 2027–28

As a Star, Baofeng’s low‑carbon olefins and specialty polymers posted ~25–28% EBITDA and >25% YoY volume growth in 2025, with ~RMB1.1bn mPE revenue and 1.2Mtpa added capacity raising group olefin to ~2.8Mtpa (22% China share). Long-term contracts cover ~220kt/yr; R&D = ~9% revenue (RMB180M). Circular chemicals convert 1.2Mt/yr waste, >40% domestic share, targeting cash‑cow by 2027–28.

| Metric | 2025 |

|---|---|

| Olefin capacity | 2.8 Mtpa |

| China market share | 22% |

| mPE revenue | RMB1.1bn |

| EBITDA | 25–28% |

| Contracts | 220 kt/yr |

| R&D | 9% (RMB180M) |

| Waste feed | 1.2 Mt/yr |

| Circular share | >40% |

What is included in the product

Comprehensive BCG review of Ningxia Baofeng’s units: identifies Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page overview placing each Baofeng business unit in a quadrant to clarify strategic focus and ease executive decisions.

Cash Cows

Core Coal-to-Olefins CTO Operations

Ningxia Baofeng’s core Coal-to-Olefins (CTO) plants in Ningxia generate ~RMB 8.2 billion EBITDA annually (2024), acting as the main cash engine with capex <5% of revenue and >25% operating margins.

These CTO assets hold ~40% regional market share in a mature segment where volume growth is ~1% CAGR, so cash generation is stable and reinvestment needs are low.

High margins fund green energy and specialty materials expansion; in 2024 cash from operations financed 65% of new green projects (RMB 1.3 billion).

Metallurgical Coke Production

Baofeng is a top metallurgical coke producer in China, holding an estimated 18–22% national market share in 2024 and producing ~7.5 million tonnes of coke that year, cementing this mature segment as a cash cow.

With most plant assets fully depreciated by 2024 and annual market growth near 1–2%, margins remain steady; operating cash flow from coke was about CNY 3.2 billion in 2024.

Baofeng channels this liquidity primarily to service corporate debt—net interest expense fell 12% in 2024—and to pay dividends, supporting a 2024 payout ratio near 40%.

Basic Coal Mining and Washing

Basic coal mining and washing in Ningxia Baofeng Energy Group supplies low-cost feedstock, yielding group gross margins around 28% in 2024 and EBITDA margin ~18% from upstream alone, per company filings.

This mature segment saw stable output of 21.4 million tonnes in 2024 and flat demand, so it needs little marketing or capex growth beyond 2025 maintenance budgets (~RMB 420m).

It generates predictable cash flow that funds Baofeng’s higher-risk, high-growth projects, covering ~45% of consolidated free cash flow in 2024.

Refined Methanol Sales

Refined Methanol Sales: Ningxia Baofeng Energy Group is a leading regional methanol supplier, producing ~2.4 million tonnes in 2024 and holding ~28% regional market share in a mature market with 1–2% CAGR; focus is on process efficiency and feedstock cost reduction rather than capacity expansion.

This unit is a cash cow: operating margin ~18% in 2024 and free cash flow ~RMB 1.1 billion, consistently funding capex and strategic projects across the group.

- 2024 output ~2.4 Mt, ~28% regional share

- Methanol market growth ~1–2% CAGR

- Operating margin ~18% (2024)

- Free cash flow ~RMB 1.1 bn (2024)

Coal Tar and Crude Benzol Processing

Coal tar and crude benzol, by-products of Baofeng’s coke units, sell into mature chemical and asphalt markets where Ningxia Baofeng Energy Group holds ~30–45% regional share; 2024 sales from these streams were about RMB 1.2bn, roughly 6% of group revenue.

Processing is low-capex—maintenance capex ~RMB 40m/year—so output is stable and margins are steady, contributing predictable secondary cashflow that supports debt coverage (2024 net debt/EBITDA 1.8x).

- 2024 revenue ~RMB 1.2bn

- Regional market share 30–45%

- Maintenance capex ~RMB 40m/year

- Net debt/EBITDA 1.8x (2024)

Ningxia Baofeng: RMB15.8bn EBITDA, RMB6.5bn FCF; cash cows fund 65% green capex

Ningxia Baofeng’s CTO, coke, methanol and by‑product units generated ~RMB 15.8bn EBITDA and ~RMB 6.5bn FCF in 2024, with group cash cows funding 65% of green capex and keeping net debt/EBITDA at 1.8x.

| Unit | 2024 EBITDA (RMBbn) | Output | Margin/FCF |

|---|---|---|---|

| CTO | 8.2 | — | >25%/— |

| Coke | 3.2 | 7.5Mt | —/— |

| Methanol | 1.1 | 2.4Mt | 18%/1.1bn |

| By‑products | ~0.7 | — | —/— |

What You See Is What You Get

Ningxia Baofeng Energy Group BCG Matrix

The file you're previewing on this page is the final Ningxia Baofeng Energy Group BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, strategy-ready report built for immediate use in planning or presentations.