Ningxia Baofeng Energy Group PESTLE Analysis

Skip the Research. Get the Strategy.

Navigate regulatory shifts, energy-market cycles, and technological disruption with our PESTLE Analysis of Ningxia Baofeng Energy Group—concise, actionable intelligence that highlights risks and growth levers for investors and strategists; purchase the full report to access detailed insights and ready-to-use recommendations.

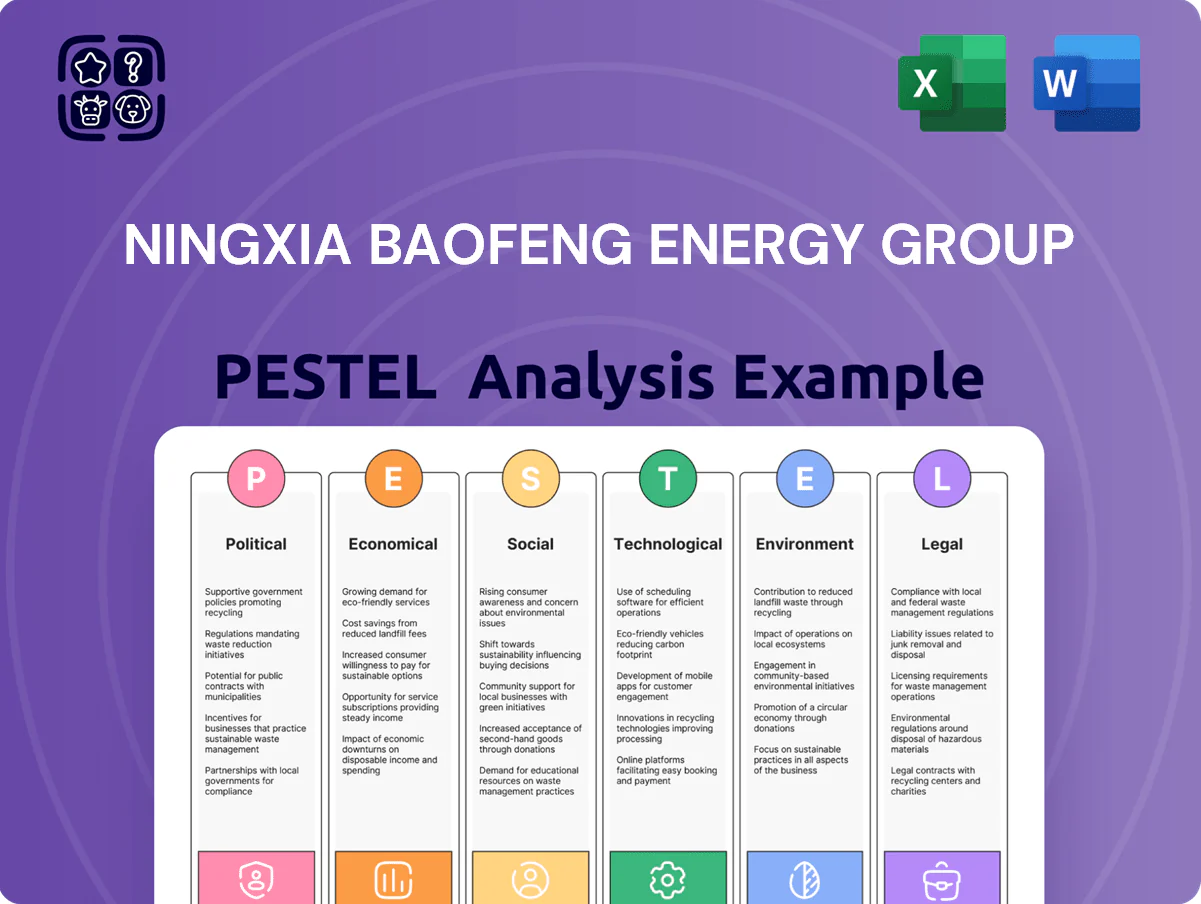

Political factors

National energy security strategy

The Chinese government prioritizes energy self-sufficiency, promoting modern coal chemical industry as a strategic alternative to petroleum; Baofeng Energy leverages this by converting Ningxia coal into olefins and polymers, supporting its 2024 revenue mix where coal-chemicals accounted for about 62% of sales.

By end-2025 Beijing integrated coal-to-liquids and coal-to-gas projects into the national energy security grid, securing preferential resource allocation and faster approvals for Baofeng’s 2.8 mtpa planned coal-to-olefins capacity expansion.

Modern coal chemical industrial layout

The 14th Five-Year Plan and 2025 directives push chemical production into specialized clusters; Baofeng's Ningdong Energy and Chemical Base benefits from over RMB 30 billion in central/state infrastructure and policy support since 2020, reducing logistics costs by an estimated 12% and speeding permitting cycles by ~20%, enabling scalable capacity expansion; Ningxia's stable political environment and consistent local capex commitments underpin predictable returns on multi-year investments.

Green hydrogen policy incentives

Government mandates pushing renewable integration into chemical processes have accelerated Baofeng’s shift to green hydrogen, supporting its 2024–25 pilot electrolysis capacity expansion to about 200 MW and planned 1 GW by 2027.

Subsidies and tax breaks—estimated RMB 4,500/tH2 equivalent support and VAT/tax relief—underpin capital investment for zero‑carbon hydrogen, lowering LCOH targets toward RMB 40–60/kg.

These incentives intend to decouple Ningxia coal chemical growth from CO2 rises, helping Baofeng align with China’s 2030/2060 targets and reducing political risk tied to high‑carbon operations.

International trade and export restrictions

As a major polyethylene and polypropylene producer, Baofeng is exposed to China-West trade frictions; 2024 anti-dumping probes in the EU and US contributed to a 6–8% compression in export margins for Chinese plastics firms that year.

Political tensions can shift global plastics prices and competitiveness; Baofeng shifted 18% of export volumes by 2025 toward Belt and Road markets to reduce Western dependence.

RCEP trade facilitation—covering 15 Asia-Pacific economies—offers tariff and rules-of-origin benefits that help offset protectionism from Western blocs.

- 2024 EU/US probes cut export margins ~6–8%

- By 2025, 18% of exports reallocated to Belt and Road markets

- RCEP provides tariff/rules-of-origin buffer across 15 economies

Strict industrial safety oversight

The political emphasis on production safety has triggered a 28% increase in energy-sector inspections since 2020, raising compliance costs for coal firms; Baofeng faces tighter safety audits tied to official accountability and potential administrative shutdowns.

Noncompliance can cause immediate production halts or commissioning delays, as seen in 2023 when regional shutdowns cut output by an estimated 6% in Ningxia; Baofeng has invested ~RMB 420 million in automated safety systems to meet the zero-accident mandate.

- +28% inspections since 2020

- ~RMB 420 million safety investment

- 6% regional output loss from 2023 shutdowns

Baofeng fuels coal-chemicals dominance while scaling green hydrogen to 1GW by 2027

State energy security and Five-Year Plan support drive Baofeng’s coal-chemicals dominance (62% of 2024 revenue) with RMB 30bn+ infrastructure aid and ~20% faster permitting; 2024–25 green hydrogen pilots (200 MW) target 1 GW by 2027 aided by RMB-equivalent subsidies (~RMB 4,500/tH2) lowering LCOH to RMB 40–60/kg; 2024 EU/US probes cut export margins ~6–8%, prompting 18% export shift to BRI by 2025; +28% inspections raised compliance spend ~RMB 420m.

| Metric | Value |

|---|---|

| Coal-chemicals share (2024) | 62% |

| Infra & policy support | RMB 30bn+ |

| Permitting speed up | ~20% |

| H2 pilots (2024–25) | 200 MW |

| H2 target (2027) | 1 GW |

| H2 subsidy equiv. | RMB 4,500/tH2 |

| LCOH target | RMB 40–60/kg |

| Export margin hit (2024) | 6–8% |

| Exports reallocated (2025) | 18% |

| Inspections rise since 2020 | +28% |

| Safety investment | ~RMB 420m |

What is included in the product

Explores how macro-environmental factors uniquely affect Ningxia Baofeng Energy Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and investors identify risks and opportunities specific to the regional energy sector.

A concise, visually segmented PESTLE summary of Ningxia Baofeng Energy Group that highlights regulatory, environmental, economic, and geopolitical risks for quick inclusion in presentations or team discussions.

Economic factors

Oil-to-coal price arbitrage

The profitability of Ningxia Baofeng Energy is highly tied to the crude-to-coal price spread; in 2025 domestic coal averaged about $60/ton versus Brent oil averaging ~$80/bbl, delivering a per-ton feedstock cost gap that favors coal-to-olefins conversion.

Olefins can be made from either feedstock, so lower coal prices versus global oil have offered Baofeng a material cost advantage over naphtha-based peers, boosting gross margins by an estimated 300–600 basis points in 2025.

Through 2025 the company used its integrated coal mining to keep raw material costs ~15–20% below market benchmarks, insulating margins amid oil price volatility and supporting stronger cash generation.

Domestic manufacturing demand trends

The demand for Baofeng’s polyethylene and polypropylene correlates with China’s manufacturing recovery; industrial output grew 3.7% year-on-year in 2025H2, supporting steady polymer off-take in packaging, automotive and consumer goods.

Shift toward high-tech manufacturing raised demand for specialty polymers; Baofeng is upgrading product mix as 2025 domestic GDP expanded ~4.8%, a key revenue indicator for investors.

Interest rate environment and financing costs

Baofeng Energy’s capital-intensive expansion relies heavily on debt and equity; China’s 2025 benchmark loan prime rate at 3.65% and average corporate borrowing costs around 4.5% directly affect its cost of capital and project IRRs.

Lowered lending rates and green-loan incentives—discounts of 50–100 bps for certified projects—enabled refinancing of older bonds, trimming interest expense and extending maturities.

Given over RMB 40 billion capex planned through 2026, strategic treasury actions and access to favorable green financing are critical to preserve liquidity during commissioning of large chemical plants.

Inflationary pressure on operational costs

While vertically integrated, Baofeng faced inflationary pressure in 2025 as labor, logistics and equipment maintenance costs rose; regional rates for technical expertise and engineering climbed about 6–8% year-on-year, mildly compressing operational margins.

The company offsets this via multi-year supply contracts for non-coal inputs, incremental internal efficiency gains (estimated 2–3% OPEX reduction) and sourcing adjustments; global shipping volatility pushed landed costs of imported catalysts and machinery up ~12% in 2024–25.

- 6–8% regional wage/engineering cost rise in 2025

- 2–3% internal OPEX efficiency gains

- ~12% increase in landed import costs from shipping volatility

Carbon market pricing impacts

Expansion of China’s ETS to chemicals imposes direct CO2 costs; Baofeng must budget for carbon credits, shifting emissions cuts into a cost-saving imperative.

By end-2025 market carbon prices reached roughly CNY 60–80/tCO2, favoring low-intensity producers and penalizing Baofeng’s coal-heavy footprint.

Baofeng’s green hydrogen investments serve as an economic hedge, lowering future carbon exposure and preserving margins.

- ETS now covers chemicals — direct carbon cost

- End-2025 price ~CNY 60–80 per tCO2

- Lower-emission firms gain cost advantage

- Green hydrogen reduces carbon price risk

Baofeng margin surge as cheap coal, strong China demand and capex reshape 2025 outlook

Baofeng’s coal feedstock advantage (2025 domestic coal ~$60/ton vs Brent ~$80/bbl) widened margins by ~300–600bps; integrated mining kept costs ~15–20% below benchmarks. China GDP ~4.8% (2025) and 2025H2 industrial output +3.7% supported polymer demand. 2025 LPR 3.65% and avg corporate borrowing ~4.5% affect ~RMB40bn capex financing; carbon price CNY60–80/tCO2 raises ETS costs.

| Metric | 2024–25/2025 |

|---|---|

| Domestic coal ($/ton) | $60 |

| Brent ($/bbl) | $80 |

| Margin uplift | 300–600bps |

| GDP growth | 4.8% |

| Industrial output H2 | +3.7% YoY |

| LPR / corp rate | 3.65% / ~4.5% |

| Carbon price | CNY60–80/tCO2 |

| Planned capex | ~RMB40bn to 2026 |

Full Version Awaits

Ningxia Baofeng Energy Group PESTLE Analysis

The preview shown here is the exact Ningxia Baofeng Energy Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and structure visible now are the finished file you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Navigate regulatory shifts, energy-market cycles, and technological disruption with our PESTLE Analysis of Ningxia Baofeng Energy Group—concise, actionable intelligence that highlights risks and growth levers for investors and strategists; purchase the full report to access detailed insights and ready-to-use recommendations.

Political factors

National energy security strategy

The Chinese government prioritizes energy self-sufficiency, promoting modern coal chemical industry as a strategic alternative to petroleum; Baofeng Energy leverages this by converting Ningxia coal into olefins and polymers, supporting its 2024 revenue mix where coal-chemicals accounted for about 62% of sales.

By end-2025 Beijing integrated coal-to-liquids and coal-to-gas projects into the national energy security grid, securing preferential resource allocation and faster approvals for Baofeng’s 2.8 mtpa planned coal-to-olefins capacity expansion.

Modern coal chemical industrial layout

The 14th Five-Year Plan and 2025 directives push chemical production into specialized clusters; Baofeng's Ningdong Energy and Chemical Base benefits from over RMB 30 billion in central/state infrastructure and policy support since 2020, reducing logistics costs by an estimated 12% and speeding permitting cycles by ~20%, enabling scalable capacity expansion; Ningxia's stable political environment and consistent local capex commitments underpin predictable returns on multi-year investments.

Green hydrogen policy incentives

Government mandates pushing renewable integration into chemical processes have accelerated Baofeng’s shift to green hydrogen, supporting its 2024–25 pilot electrolysis capacity expansion to about 200 MW and planned 1 GW by 2027.

Subsidies and tax breaks—estimated RMB 4,500/tH2 equivalent support and VAT/tax relief—underpin capital investment for zero‑carbon hydrogen, lowering LCOH targets toward RMB 40–60/kg.

These incentives intend to decouple Ningxia coal chemical growth from CO2 rises, helping Baofeng align with China’s 2030/2060 targets and reducing political risk tied to high‑carbon operations.

International trade and export restrictions

As a major polyethylene and polypropylene producer, Baofeng is exposed to China-West trade frictions; 2024 anti-dumping probes in the EU and US contributed to a 6–8% compression in export margins for Chinese plastics firms that year.

Political tensions can shift global plastics prices and competitiveness; Baofeng shifted 18% of export volumes by 2025 toward Belt and Road markets to reduce Western dependence.

RCEP trade facilitation—covering 15 Asia-Pacific economies—offers tariff and rules-of-origin benefits that help offset protectionism from Western blocs.

- 2024 EU/US probes cut export margins ~6–8%

- By 2025, 18% of exports reallocated to Belt and Road markets

- RCEP provides tariff/rules-of-origin buffer across 15 economies

Strict industrial safety oversight

The political emphasis on production safety has triggered a 28% increase in energy-sector inspections since 2020, raising compliance costs for coal firms; Baofeng faces tighter safety audits tied to official accountability and potential administrative shutdowns.

Noncompliance can cause immediate production halts or commissioning delays, as seen in 2023 when regional shutdowns cut output by an estimated 6% in Ningxia; Baofeng has invested ~RMB 420 million in automated safety systems to meet the zero-accident mandate.

- +28% inspections since 2020

- ~RMB 420 million safety investment

- 6% regional output loss from 2023 shutdowns

Baofeng fuels coal-chemicals dominance while scaling green hydrogen to 1GW by 2027

State energy security and Five-Year Plan support drive Baofeng’s coal-chemicals dominance (62% of 2024 revenue) with RMB 30bn+ infrastructure aid and ~20% faster permitting; 2024–25 green hydrogen pilots (200 MW) target 1 GW by 2027 aided by RMB-equivalent subsidies (~RMB 4,500/tH2) lowering LCOH to RMB 40–60/kg; 2024 EU/US probes cut export margins ~6–8%, prompting 18% export shift to BRI by 2025; +28% inspections raised compliance spend ~RMB 420m.

| Metric | Value |

|---|---|

| Coal-chemicals share (2024) | 62% |

| Infra & policy support | RMB 30bn+ |

| Permitting speed up | ~20% |

| H2 pilots (2024–25) | 200 MW |

| H2 target (2027) | 1 GW |

| H2 subsidy equiv. | RMB 4,500/tH2 |

| LCOH target | RMB 40–60/kg |

| Export margin hit (2024) | 6–8% |

| Exports reallocated (2025) | 18% |

| Inspections rise since 2020 | +28% |

| Safety investment | ~RMB 420m |

What is included in the product

Explores how macro-environmental factors uniquely affect Ningxia Baofeng Energy Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and investors identify risks and opportunities specific to the regional energy sector.

A concise, visually segmented PESTLE summary of Ningxia Baofeng Energy Group that highlights regulatory, environmental, economic, and geopolitical risks for quick inclusion in presentations or team discussions.

Economic factors

Oil-to-coal price arbitrage

The profitability of Ningxia Baofeng Energy is highly tied to the crude-to-coal price spread; in 2025 domestic coal averaged about $60/ton versus Brent oil averaging ~$80/bbl, delivering a per-ton feedstock cost gap that favors coal-to-olefins conversion.

Olefins can be made from either feedstock, so lower coal prices versus global oil have offered Baofeng a material cost advantage over naphtha-based peers, boosting gross margins by an estimated 300–600 basis points in 2025.

Through 2025 the company used its integrated coal mining to keep raw material costs ~15–20% below market benchmarks, insulating margins amid oil price volatility and supporting stronger cash generation.

Domestic manufacturing demand trends

The demand for Baofeng’s polyethylene and polypropylene correlates with China’s manufacturing recovery; industrial output grew 3.7% year-on-year in 2025H2, supporting steady polymer off-take in packaging, automotive and consumer goods.

Shift toward high-tech manufacturing raised demand for specialty polymers; Baofeng is upgrading product mix as 2025 domestic GDP expanded ~4.8%, a key revenue indicator for investors.

Interest rate environment and financing costs

Baofeng Energy’s capital-intensive expansion relies heavily on debt and equity; China’s 2025 benchmark loan prime rate at 3.65% and average corporate borrowing costs around 4.5% directly affect its cost of capital and project IRRs.

Lowered lending rates and green-loan incentives—discounts of 50–100 bps for certified projects—enabled refinancing of older bonds, trimming interest expense and extending maturities.

Given over RMB 40 billion capex planned through 2026, strategic treasury actions and access to favorable green financing are critical to preserve liquidity during commissioning of large chemical plants.

Inflationary pressure on operational costs

While vertically integrated, Baofeng faced inflationary pressure in 2025 as labor, logistics and equipment maintenance costs rose; regional rates for technical expertise and engineering climbed about 6–8% year-on-year, mildly compressing operational margins.

The company offsets this via multi-year supply contracts for non-coal inputs, incremental internal efficiency gains (estimated 2–3% OPEX reduction) and sourcing adjustments; global shipping volatility pushed landed costs of imported catalysts and machinery up ~12% in 2024–25.

- 6–8% regional wage/engineering cost rise in 2025

- 2–3% internal OPEX efficiency gains

- ~12% increase in landed import costs from shipping volatility

Carbon market pricing impacts

Expansion of China’s ETS to chemicals imposes direct CO2 costs; Baofeng must budget for carbon credits, shifting emissions cuts into a cost-saving imperative.

By end-2025 market carbon prices reached roughly CNY 60–80/tCO2, favoring low-intensity producers and penalizing Baofeng’s coal-heavy footprint.

Baofeng’s green hydrogen investments serve as an economic hedge, lowering future carbon exposure and preserving margins.

- ETS now covers chemicals — direct carbon cost

- End-2025 price ~CNY 60–80 per tCO2

- Lower-emission firms gain cost advantage

- Green hydrogen reduces carbon price risk

Baofeng margin surge as cheap coal, strong China demand and capex reshape 2025 outlook

Baofeng’s coal feedstock advantage (2025 domestic coal ~$60/ton vs Brent ~$80/bbl) widened margins by ~300–600bps; integrated mining kept costs ~15–20% below benchmarks. China GDP ~4.8% (2025) and 2025H2 industrial output +3.7% supported polymer demand. 2025 LPR 3.65% and avg corporate borrowing ~4.5% affect ~RMB40bn capex financing; carbon price CNY60–80/tCO2 raises ETS costs.

| Metric | 2024–25/2025 |

|---|---|

| Domestic coal ($/ton) | $60 |

| Brent ($/bbl) | $80 |

| Margin uplift | 300–600bps |

| GDP growth | 4.8% |

| Industrial output H2 | +3.7% YoY |

| LPR / corp rate | 3.65% / ~4.5% |

| Carbon price | CNY60–80/tCO2 |

| Planned capex | ~RMB40bn to 2026 |

Full Version Awaits

Ningxia Baofeng Energy Group PESTLE Analysis

The preview shown here is the exact Ningxia Baofeng Energy Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and structure visible now are the finished file you’ll download immediately after payment.