Baoshan Iron & Steel Porter's Five Forces Analysis

From Overview to Strategy Blueprint

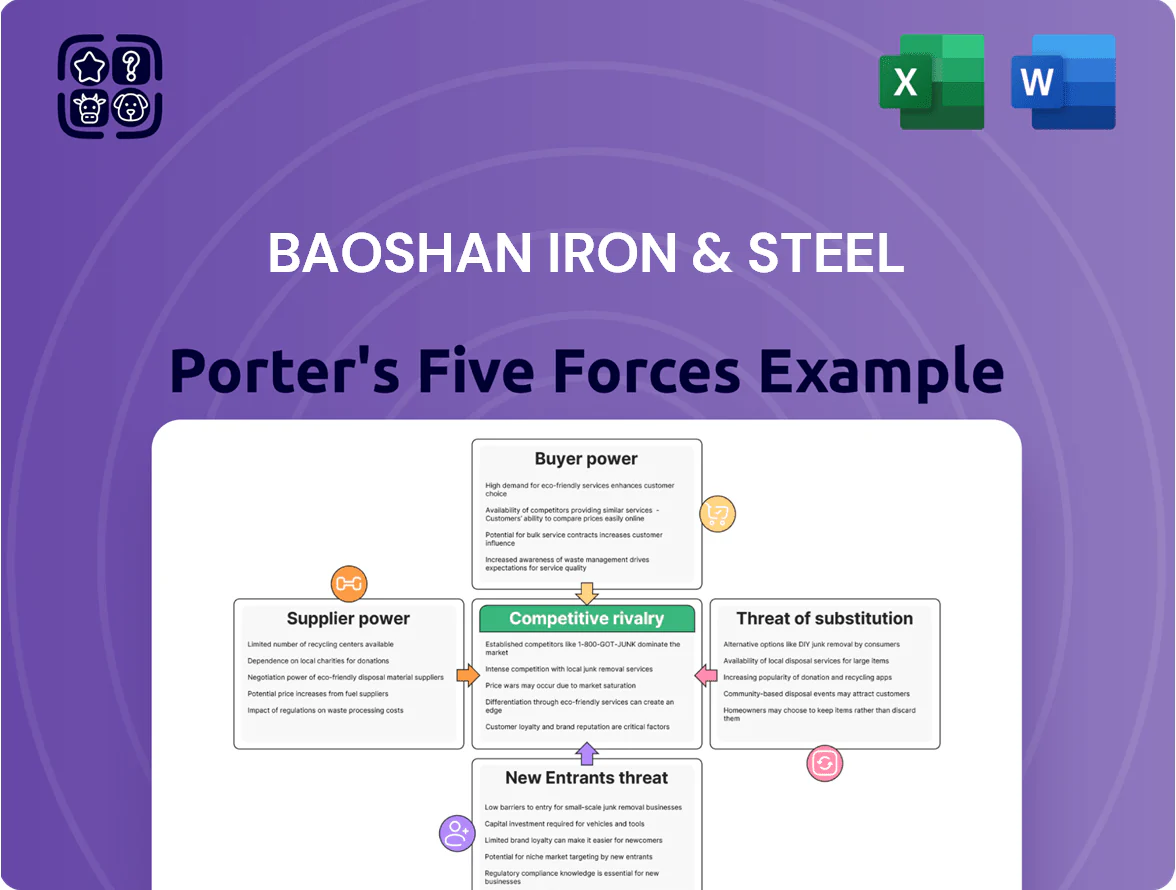

Baoshan Iron & Steel faces intense rivalry from domestic and global steelmakers, moderate supplier leverage from raw material providers, and steady buyer pressure amid commoditized product lines and price sensitivity.

Suppliers Bargaining Power

Concentration of Global Iron Ore Miners

The global iron ore market is highly concentrated: Rio Tinto, Vale, and BHP supplied about 56% of seaborne iron ore in 2024, giving them strong pricing power over raw material costs.

That oligopoly lets suppliers influence long-term contract terms and spot prices; benchmark 62% Fe fines averaged roughly $100–120/tonne in 2024, raising input cost risk for Baosteel.

Baosteel, needing ~100+ million tonnes yearly of high‑grade ore, must balance long‑term contracts, port logistics, and blending to mitigate supplier leverage and price volatility.

Volatility in Coking Coal Procurement

Coking coal is a vital input for Baoshan Iron & Steel’s blast furnaces, and in 2024 global coking coal prices averaged about $240/ton, up 18% year-on-year due to geopolitics and supply shocks; sudden export curbs or Australian port disruptions can trigger sharp spikes that compress Baosteel’s margins. Domestic mining regulations in China, tightened in 2023–24, constrained domestic output by roughly 5–7%, pushing Baosteel to secure long-term contracts covering ~60% of needs and increase strategic domestic sourcing to stabilize input costs.

Transition to Renewable Energy Sources

As Baoshan Iron & Steel shifts to carbon neutrality, reliance moves from coal and gas to renewables and hydrogen suppliers, many of which in China are state-controlled, limiting bargaining power; in 2024 China’s renewable electricity market saw 60% of large-scale projects tied to state firms.

Logistics and Maritime Freight Costs

- 2024 BDI range: 700–2,300

- Freight ≈4–6% of 2024 COGS

- Disruption adds 5–10% cost spike

- Mitigation: long-term charters, slot agreements

Strategic Vertical Integration Efforts

Baosteel and parent China Baowu have ramped up upstream mining investments: by 2024 Baowu held stakes in at least 6 overseas iron‑ore projects and increased coking‑coal self‑supply to ~28% of needs, cutting spot purchases and exposure to miner pricing swings.

The vertical integration lowers supplier bargaining power by securing ~15–25% of feedstock volume through owned or JV mines, giving Baoshan better cost predictability and negotiating leverage versus global miners.

- 6+ overseas iron‑ore projects (2024)

- ~28% coking‑coal self‑supply (2024)

- 15–25% feedstock from owned/JV mines

Major miners dominate ore; Baosteel's coal self‑supply trims supplier leverage

Suppliers hold moderate-to-high power: Rio Tinto, Vale, BHP ~56% seaborne ore (2024), 62% Fe ~ $100–120/t; coking coal ~$240/t (2024). Baosteel secures ~60% long‑term coal contracts and ~28% self‑supply, plus 6+ overseas mines, cutting supplier leverage to net moderate bargaining power.

| Metric | 2024 |

|---|---|

| Top 3 ore share | 56% |

| 62% Fe price | $100–120/t |

| Coking coal | $240/t |

| Self‑supply | ~28% |

What is included in the product

Tailored Porter's Five Forces for Baoshan Iron & Steel, uncovering competitive intensity, supplier and buyer power, substitution threats, and entry barriers to assess pricing pressure, profitability risks, and strategic defenses.

A concise Porter's Five Forces summary for Baoshan Iron & Steel—ideal for quick strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of Automotive Sector Clients

Baosteel supplies major global and Chinese automakers with galvanized sheets and ultra-high-strength steel, and top 10 OEMs account for roughly 45% of its automotive sales, giving buyers large leverage.

These OEMs buy millions of tons annually, so volume purchasing and tight specs force Baosteel into slimmer margins and bespoke R&D costs.

The EV shift raised demand for lightweight advanced steels; by 2024 EV content doubled in contracts, pushing buyers to demand lower prices and tailored grades.

Demand for Green and Low-Carbon Steel

Availability of Domestic and International Alternatives

Despite Baosteel's leadership, buyers can turn to Tier-1 rivals—Shougang (China) or POSCO (Korea)—and global mills; in 2024 China’s top 5 producers held ~40% of domestic crude steel, so alternatives are plentiful.

Commodity steel has low switching costs, and spot coil prices swung ~18% in 2024, enabling buyers to pivot quickly on price.

This ready supply keeps persistent downward pressure on Baosteel’s pricing for standard products, squeezing margins on commodity lines.

Price Sensitivity in Infrastructure Projects

A significant share of steel demand for Baoshan Iron & Steel (Baosteel) comes from state-led infrastructure and construction projects, where budget caps drive buyers to the lowest-cost bids; China’s infrastructure investment fell to 5.5% annual growth in 2024, tightening public tender margins.

Government-linked contractors use strict competitive bidding that favors price over brand; Baosteel must reconcile its high-end product mix with discounting pressure in large-volume tenders, where a 1–3% price gap can shift contracts.

High Switching Costs for Specialized Alloys

For high-end electrical steel used in transformers, switching suppliers involves complex qualifying tests and retooling; Baoshan Iron & Steel (Baosteel) held about 22% of China’s grain-oriented electrical steel capacity in 2024, creating customer lock-in.

Baosteel’s proprietary coating and tight thickness tolerance raise technical barriers, so buyers needing <0.5% core loss performance have limited alternatives and weaker bargaining power.

- 22% China capacity share (2024)

- <0.5% core loss spec common

- Proprietary coating, tight tolerances

- High qualification time and cost

OEM buying power, spot swings & green costs squeeze steel margins amid infra and e-steel locks

Buyers hold strong leverage: top 10 OEMs = ~45% auto sales, large-volume purchasing and tight specs cut margins; 2024 spot coil swings ~18% enable quick switching. ESG demands rose—62% of OEMs seek CO2 intensity data, Baosteel spent ¥12.4bn on green capex in 2024—raising costs. State tenders (5.5% infra growth 2024) favor lowest bids; electrical steel is a pocket of lock-in (22% capacity share).

| Metric | 2024 |

|---|---|

| Top-10 OEM share | ~45% |

| Spot price swing | ~18% |

| OEMs needing CO2 data | 62% |

| Green capex | ¥12.4bn |

| Infra growth | 5.5% |

| Electrical steel share | 22% |

What You See Is What You Get

Baoshan Iron & Steel Porter's Five Forces Analysis

This preview shows the exact Baoshan Iron & Steel Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

You're viewing the full professional document, fully formatted and ready for download and use the moment you buy.

The analysis is the same file delivered after payment, complete and ready for immediate application in research, strategy, or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Baoshan Iron & Steel faces intense rivalry from domestic and global steelmakers, moderate supplier leverage from raw material providers, and steady buyer pressure amid commoditized product lines and price sensitivity.

Suppliers Bargaining Power

Concentration of Global Iron Ore Miners

The global iron ore market is highly concentrated: Rio Tinto, Vale, and BHP supplied about 56% of seaborne iron ore in 2024, giving them strong pricing power over raw material costs.

That oligopoly lets suppliers influence long-term contract terms and spot prices; benchmark 62% Fe fines averaged roughly $100–120/tonne in 2024, raising input cost risk for Baosteel.

Baosteel, needing ~100+ million tonnes yearly of high‑grade ore, must balance long‑term contracts, port logistics, and blending to mitigate supplier leverage and price volatility.

Volatility in Coking Coal Procurement

Coking coal is a vital input for Baoshan Iron & Steel’s blast furnaces, and in 2024 global coking coal prices averaged about $240/ton, up 18% year-on-year due to geopolitics and supply shocks; sudden export curbs or Australian port disruptions can trigger sharp spikes that compress Baosteel’s margins. Domestic mining regulations in China, tightened in 2023–24, constrained domestic output by roughly 5–7%, pushing Baosteel to secure long-term contracts covering ~60% of needs and increase strategic domestic sourcing to stabilize input costs.

Transition to Renewable Energy Sources

As Baoshan Iron & Steel shifts to carbon neutrality, reliance moves from coal and gas to renewables and hydrogen suppliers, many of which in China are state-controlled, limiting bargaining power; in 2024 China’s renewable electricity market saw 60% of large-scale projects tied to state firms.

Logistics and Maritime Freight Costs

- 2024 BDI range: 700–2,300

- Freight ≈4–6% of 2024 COGS

- Disruption adds 5–10% cost spike

- Mitigation: long-term charters, slot agreements

Strategic Vertical Integration Efforts

Baosteel and parent China Baowu have ramped up upstream mining investments: by 2024 Baowu held stakes in at least 6 overseas iron‑ore projects and increased coking‑coal self‑supply to ~28% of needs, cutting spot purchases and exposure to miner pricing swings.

The vertical integration lowers supplier bargaining power by securing ~15–25% of feedstock volume through owned or JV mines, giving Baoshan better cost predictability and negotiating leverage versus global miners.

- 6+ overseas iron‑ore projects (2024)

- ~28% coking‑coal self‑supply (2024)

- 15–25% feedstock from owned/JV mines

Major miners dominate ore; Baosteel's coal self‑supply trims supplier leverage

Suppliers hold moderate-to-high power: Rio Tinto, Vale, BHP ~56% seaborne ore (2024), 62% Fe ~ $100–120/t; coking coal ~$240/t (2024). Baosteel secures ~60% long‑term coal contracts and ~28% self‑supply, plus 6+ overseas mines, cutting supplier leverage to net moderate bargaining power.

| Metric | 2024 |

|---|---|

| Top 3 ore share | 56% |

| 62% Fe price | $100–120/t |

| Coking coal | $240/t |

| Self‑supply | ~28% |

What is included in the product

Tailored Porter's Five Forces for Baoshan Iron & Steel, uncovering competitive intensity, supplier and buyer power, substitution threats, and entry barriers to assess pricing pressure, profitability risks, and strategic defenses.

A concise Porter's Five Forces summary for Baoshan Iron & Steel—ideal for quick strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of Automotive Sector Clients

Baosteel supplies major global and Chinese automakers with galvanized sheets and ultra-high-strength steel, and top 10 OEMs account for roughly 45% of its automotive sales, giving buyers large leverage.

These OEMs buy millions of tons annually, so volume purchasing and tight specs force Baosteel into slimmer margins and bespoke R&D costs.

The EV shift raised demand for lightweight advanced steels; by 2024 EV content doubled in contracts, pushing buyers to demand lower prices and tailored grades.

Demand for Green and Low-Carbon Steel

Availability of Domestic and International Alternatives

Despite Baosteel's leadership, buyers can turn to Tier-1 rivals—Shougang (China) or POSCO (Korea)—and global mills; in 2024 China’s top 5 producers held ~40% of domestic crude steel, so alternatives are plentiful.

Commodity steel has low switching costs, and spot coil prices swung ~18% in 2024, enabling buyers to pivot quickly on price.

This ready supply keeps persistent downward pressure on Baosteel’s pricing for standard products, squeezing margins on commodity lines.

Price Sensitivity in Infrastructure Projects

A significant share of steel demand for Baoshan Iron & Steel (Baosteel) comes from state-led infrastructure and construction projects, where budget caps drive buyers to the lowest-cost bids; China’s infrastructure investment fell to 5.5% annual growth in 2024, tightening public tender margins.

Government-linked contractors use strict competitive bidding that favors price over brand; Baosteel must reconcile its high-end product mix with discounting pressure in large-volume tenders, where a 1–3% price gap can shift contracts.

High Switching Costs for Specialized Alloys

For high-end electrical steel used in transformers, switching suppliers involves complex qualifying tests and retooling; Baoshan Iron & Steel (Baosteel) held about 22% of China’s grain-oriented electrical steel capacity in 2024, creating customer lock-in.

Baosteel’s proprietary coating and tight thickness tolerance raise technical barriers, so buyers needing <0.5% core loss performance have limited alternatives and weaker bargaining power.

- 22% China capacity share (2024)

- <0.5% core loss spec common

- Proprietary coating, tight tolerances

- High qualification time and cost

OEM buying power, spot swings & green costs squeeze steel margins amid infra and e-steel locks

Buyers hold strong leverage: top 10 OEMs = ~45% auto sales, large-volume purchasing and tight specs cut margins; 2024 spot coil swings ~18% enable quick switching. ESG demands rose—62% of OEMs seek CO2 intensity data, Baosteel spent ¥12.4bn on green capex in 2024—raising costs. State tenders (5.5% infra growth 2024) favor lowest bids; electrical steel is a pocket of lock-in (22% capacity share).

| Metric | 2024 |

|---|---|

| Top-10 OEM share | ~45% |

| Spot price swing | ~18% |

| OEMs needing CO2 data | 62% |

| Green capex | ¥12.4bn |

| Infra growth | 5.5% |

| Electrical steel share | 22% |

What You See Is What You Get

Baoshan Iron & Steel Porter's Five Forces Analysis

This preview shows the exact Baoshan Iron & Steel Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

You're viewing the full professional document, fully formatted and ready for download and use the moment you buy.

The analysis is the same file delivered after payment, complete and ready for immediate application in research, strategy, or investment decisions.