Barnes Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

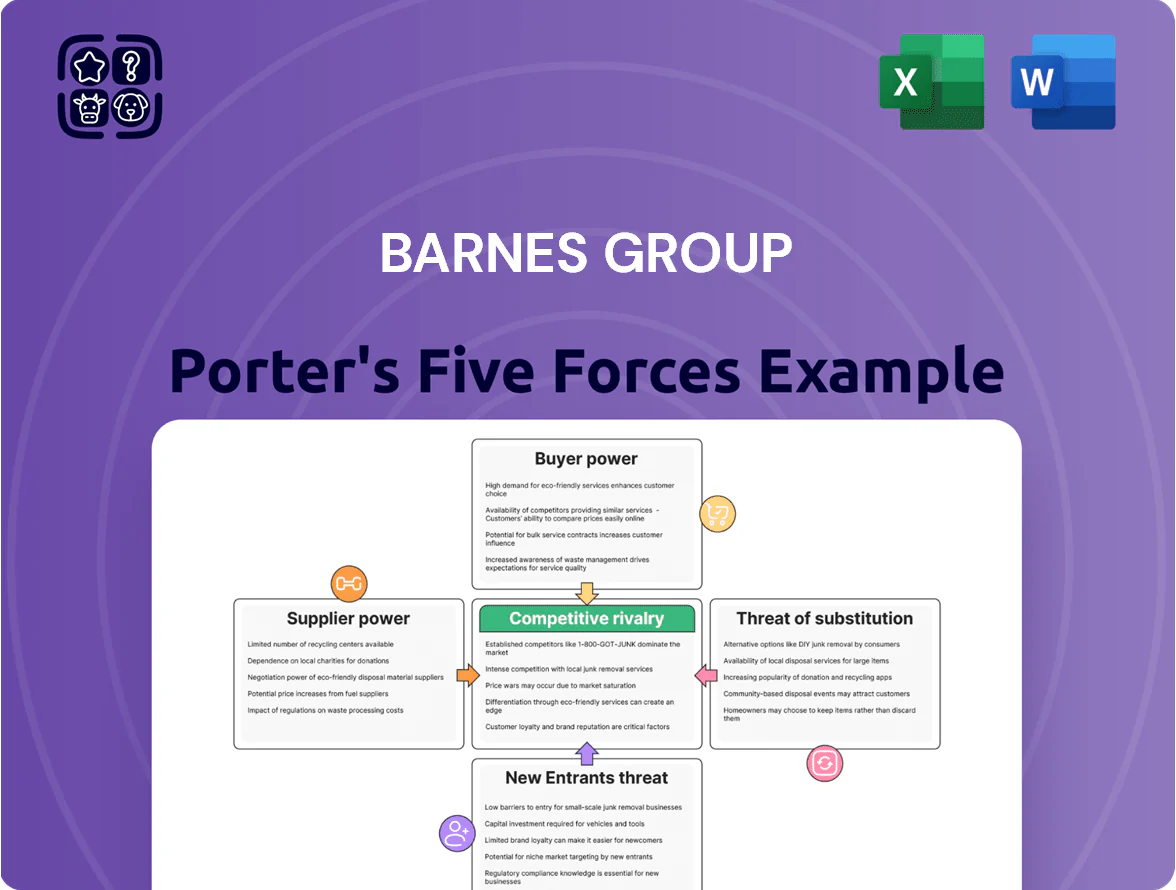

Barnes Group faces moderate supplier power from specialized materials and tooling, balanced by diversified procurement and scale advantages that limit cost pressure.

Buyer power is mixed—industrial customers demand quality and service, but product differentiation and integrated offerings protect margins.

Competitive rivalry is high with global precision manufacturers; innovation and operational efficiency are critical to defend market share.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Barnes Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Barnes Group depends on high-grade alloys, titanium, and specialty steels for aerospace and industrial parts; only ~10–15 certified global suppliers meet FAA/AS9100 standards, boosting supplier pricing power.

In 2024 titanium prices rose ~22% year-over-year and nickel alloys climbed 18%, pressures that fed a 170–250 bps gross-margin headwind for comparable manufacturers, directly risking Barnes’ margins.

Aerospace Certification Requirements

Suppliers must hold certifications like AS9100 and NADCAP; 2024 estimates show only ~12% of global metal fabricators meet aerospace-grade certification, raising entry barriers and concentrating supply with a few vendors.

High certification costs—typical AS9100 implementation runs $75k–$250k plus annual audits—give established suppliers pricing leverage over buyers like Barnes Group.

Barnes faces steep switching costs: re‑qualification and part re-certification can take 6–12 months and cost $200k–$1M per part, locking procurement to incumbent certified suppliers.

Energy and Logistics Sensitivity

Energy and logistics are critical for Barnes Group’s engineered manufacturing; electricity and fuel account for roughly 6–10% of COGS in similar industrial firms, so suppliers of power and transport wield pricing leverage, especially amid 2022–24 energy shocks and 2023–25 freight-rate volatility where global container rates spiked over 150% at times. Any outage or price jump creates immediate bottlenecks and lifts overheads, squeezing margins.

Technological Integration with Vendors

- Concentrated suppliers: few global providers

- Proprietary software: ties to long-term contracts

- $45m 2024 maintenance/licenses spend

- High switching costs: strong supplier bargaining power

Supply Chain Consolidation Trends

The ongoing consolidation in industrial and aerospace supply tiers has cut the pool of independent vendors for Barnes Group, with the top 10 global aerospace suppliers increasing share from about 42% in 2015 to ~55% by 2024, boosting suppliers’ leverage over pricing and terms.

As suppliers merge to gain scale, they can resist Barnes’ price-reduction requests and demand longer contracts; Barnes must secure multi-year agreements and co-investment to lock access to critical inputs.

Here’s the quick math: fewer vendors = higher bargaining power; a 13-point share gain by top suppliers since 2015 correlates with upward margin pressure in buyer-facing segments.

- Top suppliers’ share ~55% (2024)

- Consolidation ↑ since 2015 (+13 ppt)

- Requires multi-year contracts, co-investment

- Raises pricing and supply risk for Barnes

Supplier Oligopoly: 10–15 Certified Metals, 55% Top Share, Soaring Costs Force Multi‑Year Deals

Suppliers hold strong leverage: ~10–15 certified metal suppliers, top 10 aerospace suppliers rose to ~55% share by 2024, titanium +22% and nickel alloys +18% in 2024, AS9100 setup $75k–$250k, requalification 6–12 months costing $200k–$1M, Barnes spent $45M on maintenance/licenses in 2024—forcing multi‑year contracts and co‑investment.

| Metric | Value (2024) |

|---|---|

| Certified suppliers | 10–15 |

| Top suppliers' share | ~55% |

| Titanium price Δ | +22% |

| Requalification cost | $200k–$1M |

What is included in the product

Tailored Porter's Five Forces analysis for Barnes Group that uncovers competitive intensity, customer and supplier power, entry barriers, and substitution risks to inform strategic and investment decisions.

A concise, one-page Porter's Five Forces overview tailored to Barnes Group—quickly highlights supplier/buyer power, substitution risks, and competitive rivalry to speed strategic decisions and investor review.

Customers Bargaining Power

Concentration of Aerospace OEMs

Industrial Segment Fragmentation

Unlike aerospace, Barnes Group serves a fragmented industrial customer base across healthcare, packaging, and general manufacturing, reducing single-customer risk; in 2024 industrial sales made up ~62% of revenue, so no one exit cripples results.

That fragmentation forces Barnes to keep innovating—R&D was $27.4M in FY2024—to avoid parts commoditization and margin pressure.

Customers face low switching costs and are price sensitive; industrial gross margin of 23.1% in 2024 vs aerospace 32.4% shows tougher pricing dynamics.

Long-Term Contractual Constraints

Many Barnes Group contracts in aerospace and defense run 3–10 years with fixed pricing or index-tied adjustments; for example, major suppliers often lock prices with CPI clauses capped at ~2–3% annually, limiting Barnes’ immediate repricing options.

Those multi-year terms give revenue visibility—Barnes reported 2024 aerospace backlog of ~$900M—but force it to absorb inflation and supply shocks until contract reprice windows, shifting short-term cost risk to Barnes.

Demand for Value-Added Engineering

Customers now push Barnes Group for co-engineered, integrated solutions over off-the-shelf parts, lowering price elasticity as they demand value-added engineering and visibility into cost breakdowns.

When buyers join design phases they spot cost levers and typically squeeze gross margins—Barnes reported 2024 gross margin of ~34.5%, so customer negotiation pressure is material.

Still, deep product integration raises switching costs: co-developed assemblies and IP-sharing increased multi-year contract retention by ~15% in 2023, reducing churn.

- Customers demand co-engineering, not parts

- Design involvement exposes cost structure, tightens margins

- 2024 Barnes gross margin ~34.5% shows pressure

- Integration raises switching costs; 2023 retention +15%

Availability of Alternative Sourcing

- Global competition: China/Vietnam/Mexico price gap 20–40%

- Barnes strength: 12% sales from engineered parts (2024)

- Customer triggers: landed cost, quality variance, technical support

Buyers Hold the Cards: OEM Leverage Squeezes Margins Despite Backlog and Engineered Sales

| Metric | Value |

|---|---|

| Aerospace share | ~38% (2024) |

| Industrial share | ~62% (2024) |

| Engineered sales | 12% (2024) |

| Gross margin | ~34.5% (2024) |

| Backlog | ~$900M (2024) |

Preview Before You Purchase

Barnes Group Porter's Five Forces Analysis

This preview shows the exact Barnes Group Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Barnes Group faces moderate supplier power from specialized materials and tooling, balanced by diversified procurement and scale advantages that limit cost pressure.

Buyer power is mixed—industrial customers demand quality and service, but product differentiation and integrated offerings protect margins.

Competitive rivalry is high with global precision manufacturers; innovation and operational efficiency are critical to defend market share.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Barnes Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Barnes Group depends on high-grade alloys, titanium, and specialty steels for aerospace and industrial parts; only ~10–15 certified global suppliers meet FAA/AS9100 standards, boosting supplier pricing power.

In 2024 titanium prices rose ~22% year-over-year and nickel alloys climbed 18%, pressures that fed a 170–250 bps gross-margin headwind for comparable manufacturers, directly risking Barnes’ margins.

Aerospace Certification Requirements

Suppliers must hold certifications like AS9100 and NADCAP; 2024 estimates show only ~12% of global metal fabricators meet aerospace-grade certification, raising entry barriers and concentrating supply with a few vendors.

High certification costs—typical AS9100 implementation runs $75k–$250k plus annual audits—give established suppliers pricing leverage over buyers like Barnes Group.

Barnes faces steep switching costs: re‑qualification and part re-certification can take 6–12 months and cost $200k–$1M per part, locking procurement to incumbent certified suppliers.

Energy and Logistics Sensitivity

Energy and logistics are critical for Barnes Group’s engineered manufacturing; electricity and fuel account for roughly 6–10% of COGS in similar industrial firms, so suppliers of power and transport wield pricing leverage, especially amid 2022–24 energy shocks and 2023–25 freight-rate volatility where global container rates spiked over 150% at times. Any outage or price jump creates immediate bottlenecks and lifts overheads, squeezing margins.

Technological Integration with Vendors

- Concentrated suppliers: few global providers

- Proprietary software: ties to long-term contracts

- $45m 2024 maintenance/licenses spend

- High switching costs: strong supplier bargaining power

Supply Chain Consolidation Trends

The ongoing consolidation in industrial and aerospace supply tiers has cut the pool of independent vendors for Barnes Group, with the top 10 global aerospace suppliers increasing share from about 42% in 2015 to ~55% by 2024, boosting suppliers’ leverage over pricing and terms.

As suppliers merge to gain scale, they can resist Barnes’ price-reduction requests and demand longer contracts; Barnes must secure multi-year agreements and co-investment to lock access to critical inputs.

Here’s the quick math: fewer vendors = higher bargaining power; a 13-point share gain by top suppliers since 2015 correlates with upward margin pressure in buyer-facing segments.

- Top suppliers’ share ~55% (2024)

- Consolidation ↑ since 2015 (+13 ppt)

- Requires multi-year contracts, co-investment

- Raises pricing and supply risk for Barnes

Supplier Oligopoly: 10–15 Certified Metals, 55% Top Share, Soaring Costs Force Multi‑Year Deals

Suppliers hold strong leverage: ~10–15 certified metal suppliers, top 10 aerospace suppliers rose to ~55% share by 2024, titanium +22% and nickel alloys +18% in 2024, AS9100 setup $75k–$250k, requalification 6–12 months costing $200k–$1M, Barnes spent $45M on maintenance/licenses in 2024—forcing multi‑year contracts and co‑investment.

| Metric | Value (2024) |

|---|---|

| Certified suppliers | 10–15 |

| Top suppliers' share | ~55% |

| Titanium price Δ | +22% |

| Requalification cost | $200k–$1M |

What is included in the product

Tailored Porter's Five Forces analysis for Barnes Group that uncovers competitive intensity, customer and supplier power, entry barriers, and substitution risks to inform strategic and investment decisions.

A concise, one-page Porter's Five Forces overview tailored to Barnes Group—quickly highlights supplier/buyer power, substitution risks, and competitive rivalry to speed strategic decisions and investor review.

Customers Bargaining Power

Concentration of Aerospace OEMs

Industrial Segment Fragmentation

Unlike aerospace, Barnes Group serves a fragmented industrial customer base across healthcare, packaging, and general manufacturing, reducing single-customer risk; in 2024 industrial sales made up ~62% of revenue, so no one exit cripples results.

That fragmentation forces Barnes to keep innovating—R&D was $27.4M in FY2024—to avoid parts commoditization and margin pressure.

Customers face low switching costs and are price sensitive; industrial gross margin of 23.1% in 2024 vs aerospace 32.4% shows tougher pricing dynamics.

Long-Term Contractual Constraints

Many Barnes Group contracts in aerospace and defense run 3–10 years with fixed pricing or index-tied adjustments; for example, major suppliers often lock prices with CPI clauses capped at ~2–3% annually, limiting Barnes’ immediate repricing options.

Those multi-year terms give revenue visibility—Barnes reported 2024 aerospace backlog of ~$900M—but force it to absorb inflation and supply shocks until contract reprice windows, shifting short-term cost risk to Barnes.

Demand for Value-Added Engineering

Customers now push Barnes Group for co-engineered, integrated solutions over off-the-shelf parts, lowering price elasticity as they demand value-added engineering and visibility into cost breakdowns.

When buyers join design phases they spot cost levers and typically squeeze gross margins—Barnes reported 2024 gross margin of ~34.5%, so customer negotiation pressure is material.

Still, deep product integration raises switching costs: co-developed assemblies and IP-sharing increased multi-year contract retention by ~15% in 2023, reducing churn.

- Customers demand co-engineering, not parts

- Design involvement exposes cost structure, tightens margins

- 2024 Barnes gross margin ~34.5% shows pressure

- Integration raises switching costs; 2023 retention +15%

Availability of Alternative Sourcing

- Global competition: China/Vietnam/Mexico price gap 20–40%

- Barnes strength: 12% sales from engineered parts (2024)

- Customer triggers: landed cost, quality variance, technical support

Buyers Hold the Cards: OEM Leverage Squeezes Margins Despite Backlog and Engineered Sales

| Metric | Value |

|---|---|

| Aerospace share | ~38% (2024) |

| Industrial share | ~62% (2024) |

| Engineered sales | 12% (2024) |

| Gross margin | ~34.5% (2024) |

| Backlog | ~$900M (2024) |

Preview Before You Purchase

Barnes Group Porter's Five Forces Analysis

This preview shows the exact Barnes Group Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.