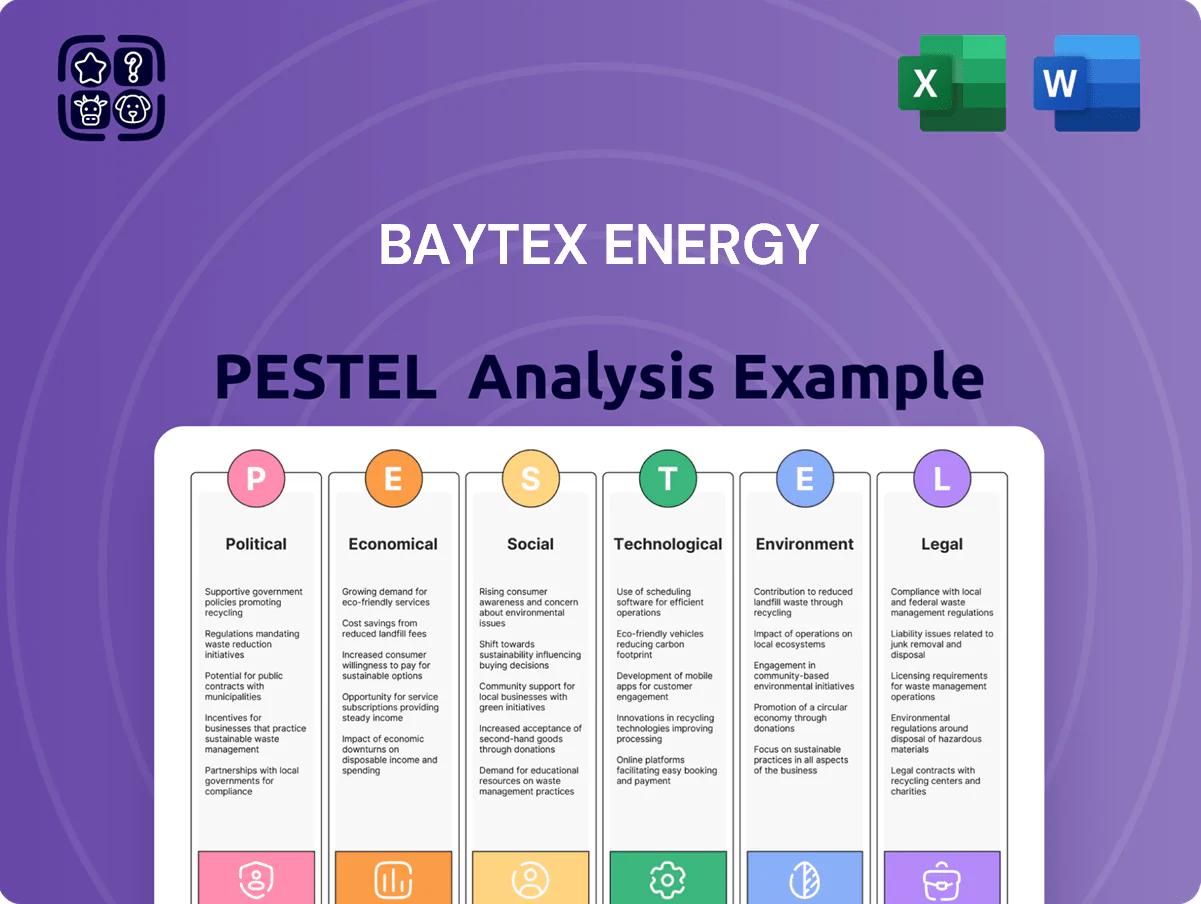

Baytex Energy PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, commodity cycles, and environmental regulations are reshaping Baytex Energy’s outlook—our concise PESTLE preview highlights key external risks and opportunities that matter to investors and strategists. Purchase the full PESTLE Analysis to access detailed, actionable insights, editable charts, and scenario-driven recommendations you can deploy immediately.

Political factors

Geopolitical Trade Relations

Stable Canada-US energy exports are critical for Baytex; in 2025 bilateral crude flows averaged about 4.0 million bpd, with heavy crude to Gulf Coast refineries accounting for a meaningful share of market access for Western Canadian Select (WCS) priced around US$55–65/bbl in 2024–2025, influencing Baytex revenue forecasts.

Cross-border trade policies and pipeline approvals—notably Trans Mountain and Line 3 debates—remain key risk factors; political shifts can alter tariff regimes or delay permits, tightening takeaway capacity and pressuring differentials that drive Baytex capital allocation and long-term planning.

Canadian Energy Policy

Federal and provincial policies in Alberta and Saskatchewan shape Baytex Energy’s capital allocation, with Alberta’s 2024 royalty review and Saskatchewan’s incentives for in-situ projects affecting investment returns across the Western Canadian Sedimentary Basin.

Changes to royalty frameworks or federal subsidies—Canada committed CA$1.3 billion in 2024 for CCS scaling—directly influence project IRRs and NPV for Baytex’s heavy oil and bitumen assets.

Evolving national energy security mandates, including 2025 guidance prioritizing domestic supply reliability, force Baytex to balance domestic production commitments against export opportunities and pricing dynamics.

U.S. Federal Land Regulations

Baytex’s Eagle Ford exposure makes it sensitive to U.S. Department of the Interior actions: in 2024 DOI processing times for federal drilling permits averaged about 145 days, up 18% year-over-year, constraining development schedules and capex deployment.

Shifts in leasing rules or federal restrictions on hydraulic fracturing could reduce recoverable volumes and compress projected 2025 U.S. production (Baytex reported ~20% of 2023 boe/d from U.S. assets), impacting revenue visibility.

Political emphasis on energy independence, reflected in 2024 federal oil production targets and tax incentives, often conflicts with conservation-driven moratoria, creating regulatory uncertainty that can raise cost of capital and delay project approvals.

Indigenous Relations and Sovereignty

Baytex must engage First Nations to secure land access and approvals; in Canada the Duty to Consult framework and UNDRIP (implemented federally 2021) increasingly shape outcomes, with Indigenous agreements influencing project timelines and capital allocation.

In Alberta and Saskatchewan, where Baytex operates, negotiated benefit-sharing can reduce legal risk—Indigenous economic participation rose 18% in 2023 in energy sector partnerships—supporting social license and access to permits and capital.

- Duty to Consult and UNDRIP drive approvals and timelines

- Indigenous partnerships cut legal/political risk

- Energy sector Indigenous participation +18% in 2023

Global Energy Security Trends

The realignment of global energy alliances and supply chains increases price volatility for Baytex; Brent crude swung 40% in 2022–2024, driving realized prices and hedging costs. Political instability in regions like the Middle East and Libya pressured global flows, boosting North American crude demand and narrowing WTI-Brent differentials to under US$5/bbl at times in 2024. Baytex monitors tensions to hedge and target export windows.

- Brent volatility ~40% (2022–2024)

- WTI-Brent spread < US$5/bbl in 2024

- Increased export demand from North America during MENA disruptions

Political risks reshape Baytex: pipelines, permits, royalties, Indigenous stakes

Political risks—pipeline approvals, Alberta/Saskatchewan royalty reviews, U.S. permitting and fracking rules, Indigenous consultation (UNDRIP/Duty to Consult), and global supply shocks—materially affect Baytex’s access, pricing, capex and timelines; 2024–25 data: Canada–US crude ~4.0M bpd, WCS US$55–65/bbl, DOI permit avg 145 days, Indigenous energy partnerships +18% (2023).

| Metric | 2024–25 |

|---|---|

| Canada–US crude flows | ~4.0M bpd |

| WCS price | US$55–65/bbl |

| DOI permit time | 145 days |

| Indigenous participation | +18% (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Baytex Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE snapshot for Baytex Energy that clarifies external risks and market drivers for fast inclusion in presentations or strategy sessions.

Economic factors

Crude Oil Price Volatility

The primary driver of Baytex Energy revenue remains WTI and WCS prices; in 2024–2025 average WTI traded near $80–85/bbl while WCS averaged about $55–60/bbl, directly shaping realized pricing and revenue. By late 2025 global supply-demand shifts and OPEC+ output cuts kept Brent volatility elevated, causing free cash flow variance of ±25–35% year-over-year. Management employs hedges covering a portion of production—hedge book reduced downside, supporting planned 2025 capex of CAD ~300–350m.

Inflationary Pressure on Input Costs

Currency Exchange Rate Fluctuations

As a Canadian producer selling much of its oil in US dollars, Baytex’s results are sensitive to CAD/USD moves; in 2024 the average CAD/USD was ~0.74, so a weaker Loonie boosted CAD revenues versus predominantly CAD-denominated operating costs. A 10% Loonie appreciation would compress margins materially and reduce reported CAD value of US assets; Baytex reported net US assets and dollar exposure in 2023–2024 financials, amplifying translation risk.

Capital Market Access

Capital market access for oil and gas firms is cyclical and tied to investor sentiment on fossil fuels; in 2024 global energy sectors saw a 12% drop in equity issuance toward hydrocarbons as ESG pressures rose.

Baytex targets an investment-grade profile, reducing net debt by 35% from 2021–2024 to secure lower-cost financing and a 2025 credit facility covenant headroom of ~US$400m.

Shift to value investing has driven Baytex to prioritize shareholder returns and further debt reduction, with buybacks/dividends funded only after maintaining >1.5x net debt/EBITDA.

- Equity/debt issuance down ~12% (2024) for hydrocarbon firms

- Baytex net debt cut ~35% (2021–2024)

- ~US$400m covenant headroom on 2025 facility

- Target net debt/EBITDA >1.5x before buybacks/dividends

Market Access and Midstream Costs

Baytex's profitability depends on pipeline and rail capacity; in 2025 Alberta heavy differentials averaged about US$18–22/bbl vs WTI, widening to over US$30/bbl during 2022–23 bottlenecks when takeaway capacity tightened.

Midstream tolls and rail rates (rail ~US$10–15/bbl inland in 2024) materially affect netbacks; delayed projects like Keystone XL historically pushed discounts deeper.

Efficient midstream economics are needed to keep heavy oil profitable when global demand softens and WTI weakens.

- 2025 Alberta heavy differential ~US$18–22/bbl vs WTI

- Rail transport cost ~US$10–15/bbl (2024 estimates)

- Takeaway constraints historically widened discounts >US$30/bbl

Oil price swings, rising costs compress netbacks but debt cut leaves $400M covenant cushion

WTI/WCS prices (2024–25 avg WTI $80–85/bbl; WCS $55–60/bbl) drive revenue; Brent volatility caused ±25–35% FCF swings in 2025. Wage growth ~4.5% (2025) and US rig rates +18% raised LOE; rail ~$10–15/bbl and Alberta heavy differential $18–22/bbl compressed netbacks. CAD/USD ~0.74 (2024) amplified translation; net debt cut ~35% (2021–24) leaving ~US$400m covenant headroom.

| Metric | Value |

|---|---|

| WTI (2024–25 avg) | $80–85/bbl |

| WCS (2024–25 avg) | $55–60/bbl |

| Alberta heavy diff (2025) | $18–22/bbl |

| Rail cost (2024) | $10–15/bbl |

| CAD/USD (2024) | ~0.74 |

| Net debt reduction (2021–24) | ~35% |

| Covenant headroom (2025) | ~US$400m |

Full Version Awaits

Baytex Energy PESTLE Analysis

The preview shown here is the exact Baytex Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, commodity cycles, and environmental regulations are reshaping Baytex Energy’s outlook—our concise PESTLE preview highlights key external risks and opportunities that matter to investors and strategists. Purchase the full PESTLE Analysis to access detailed, actionable insights, editable charts, and scenario-driven recommendations you can deploy immediately.

Political factors

Geopolitical Trade Relations

Stable Canada-US energy exports are critical for Baytex; in 2025 bilateral crude flows averaged about 4.0 million bpd, with heavy crude to Gulf Coast refineries accounting for a meaningful share of market access for Western Canadian Select (WCS) priced around US$55–65/bbl in 2024–2025, influencing Baytex revenue forecasts.

Cross-border trade policies and pipeline approvals—notably Trans Mountain and Line 3 debates—remain key risk factors; political shifts can alter tariff regimes or delay permits, tightening takeaway capacity and pressuring differentials that drive Baytex capital allocation and long-term planning.

Canadian Energy Policy

Federal and provincial policies in Alberta and Saskatchewan shape Baytex Energy’s capital allocation, with Alberta’s 2024 royalty review and Saskatchewan’s incentives for in-situ projects affecting investment returns across the Western Canadian Sedimentary Basin.

Changes to royalty frameworks or federal subsidies—Canada committed CA$1.3 billion in 2024 for CCS scaling—directly influence project IRRs and NPV for Baytex’s heavy oil and bitumen assets.

Evolving national energy security mandates, including 2025 guidance prioritizing domestic supply reliability, force Baytex to balance domestic production commitments against export opportunities and pricing dynamics.

U.S. Federal Land Regulations

Baytex’s Eagle Ford exposure makes it sensitive to U.S. Department of the Interior actions: in 2024 DOI processing times for federal drilling permits averaged about 145 days, up 18% year-over-year, constraining development schedules and capex deployment.

Shifts in leasing rules or federal restrictions on hydraulic fracturing could reduce recoverable volumes and compress projected 2025 U.S. production (Baytex reported ~20% of 2023 boe/d from U.S. assets), impacting revenue visibility.

Political emphasis on energy independence, reflected in 2024 federal oil production targets and tax incentives, often conflicts with conservation-driven moratoria, creating regulatory uncertainty that can raise cost of capital and delay project approvals.

Indigenous Relations and Sovereignty

Baytex must engage First Nations to secure land access and approvals; in Canada the Duty to Consult framework and UNDRIP (implemented federally 2021) increasingly shape outcomes, with Indigenous agreements influencing project timelines and capital allocation.

In Alberta and Saskatchewan, where Baytex operates, negotiated benefit-sharing can reduce legal risk—Indigenous economic participation rose 18% in 2023 in energy sector partnerships—supporting social license and access to permits and capital.

- Duty to Consult and UNDRIP drive approvals and timelines

- Indigenous partnerships cut legal/political risk

- Energy sector Indigenous participation +18% in 2023

Global Energy Security Trends

The realignment of global energy alliances and supply chains increases price volatility for Baytex; Brent crude swung 40% in 2022–2024, driving realized prices and hedging costs. Political instability in regions like the Middle East and Libya pressured global flows, boosting North American crude demand and narrowing WTI-Brent differentials to under US$5/bbl at times in 2024. Baytex monitors tensions to hedge and target export windows.

- Brent volatility ~40% (2022–2024)

- WTI-Brent spread < US$5/bbl in 2024

- Increased export demand from North America during MENA disruptions

Political risks reshape Baytex: pipelines, permits, royalties, Indigenous stakes

Political risks—pipeline approvals, Alberta/Saskatchewan royalty reviews, U.S. permitting and fracking rules, Indigenous consultation (UNDRIP/Duty to Consult), and global supply shocks—materially affect Baytex’s access, pricing, capex and timelines; 2024–25 data: Canada–US crude ~4.0M bpd, WCS US$55–65/bbl, DOI permit avg 145 days, Indigenous energy partnerships +18% (2023).

| Metric | 2024–25 |

|---|---|

| Canada–US crude flows | ~4.0M bpd |

| WCS price | US$55–65/bbl |

| DOI permit time | 145 days |

| Indigenous participation | +18% (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Baytex Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE snapshot for Baytex Energy that clarifies external risks and market drivers for fast inclusion in presentations or strategy sessions.

Economic factors

Crude Oil Price Volatility

The primary driver of Baytex Energy revenue remains WTI and WCS prices; in 2024–2025 average WTI traded near $80–85/bbl while WCS averaged about $55–60/bbl, directly shaping realized pricing and revenue. By late 2025 global supply-demand shifts and OPEC+ output cuts kept Brent volatility elevated, causing free cash flow variance of ±25–35% year-over-year. Management employs hedges covering a portion of production—hedge book reduced downside, supporting planned 2025 capex of CAD ~300–350m.

Inflationary Pressure on Input Costs

Currency Exchange Rate Fluctuations

As a Canadian producer selling much of its oil in US dollars, Baytex’s results are sensitive to CAD/USD moves; in 2024 the average CAD/USD was ~0.74, so a weaker Loonie boosted CAD revenues versus predominantly CAD-denominated operating costs. A 10% Loonie appreciation would compress margins materially and reduce reported CAD value of US assets; Baytex reported net US assets and dollar exposure in 2023–2024 financials, amplifying translation risk.

Capital Market Access

Capital market access for oil and gas firms is cyclical and tied to investor sentiment on fossil fuels; in 2024 global energy sectors saw a 12% drop in equity issuance toward hydrocarbons as ESG pressures rose.

Baytex targets an investment-grade profile, reducing net debt by 35% from 2021–2024 to secure lower-cost financing and a 2025 credit facility covenant headroom of ~US$400m.

Shift to value investing has driven Baytex to prioritize shareholder returns and further debt reduction, with buybacks/dividends funded only after maintaining >1.5x net debt/EBITDA.

- Equity/debt issuance down ~12% (2024) for hydrocarbon firms

- Baytex net debt cut ~35% (2021–2024)

- ~US$400m covenant headroom on 2025 facility

- Target net debt/EBITDA >1.5x before buybacks/dividends

Market Access and Midstream Costs

Baytex's profitability depends on pipeline and rail capacity; in 2025 Alberta heavy differentials averaged about US$18–22/bbl vs WTI, widening to over US$30/bbl during 2022–23 bottlenecks when takeaway capacity tightened.

Midstream tolls and rail rates (rail ~US$10–15/bbl inland in 2024) materially affect netbacks; delayed projects like Keystone XL historically pushed discounts deeper.

Efficient midstream economics are needed to keep heavy oil profitable when global demand softens and WTI weakens.

- 2025 Alberta heavy differential ~US$18–22/bbl vs WTI

- Rail transport cost ~US$10–15/bbl (2024 estimates)

- Takeaway constraints historically widened discounts >US$30/bbl

Oil price swings, rising costs compress netbacks but debt cut leaves $400M covenant cushion

WTI/WCS prices (2024–25 avg WTI $80–85/bbl; WCS $55–60/bbl) drive revenue; Brent volatility caused ±25–35% FCF swings in 2025. Wage growth ~4.5% (2025) and US rig rates +18% raised LOE; rail ~$10–15/bbl and Alberta heavy differential $18–22/bbl compressed netbacks. CAD/USD ~0.74 (2024) amplified translation; net debt cut ~35% (2021–24) leaving ~US$400m covenant headroom.

| Metric | Value |

|---|---|

| WTI (2024–25 avg) | $80–85/bbl |

| WCS (2024–25 avg) | $55–60/bbl |

| Alberta heavy diff (2025) | $18–22/bbl |

| Rail cost (2024) | $10–15/bbl |

| CAD/USD (2024) | ~0.74 |

| Net debt reduction (2021–24) | ~35% |

| Covenant headroom (2025) | ~US$400m |

Full Version Awaits

Baytex Energy PESTLE Analysis

The preview shown here is the exact Baytex Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.