BayWa Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

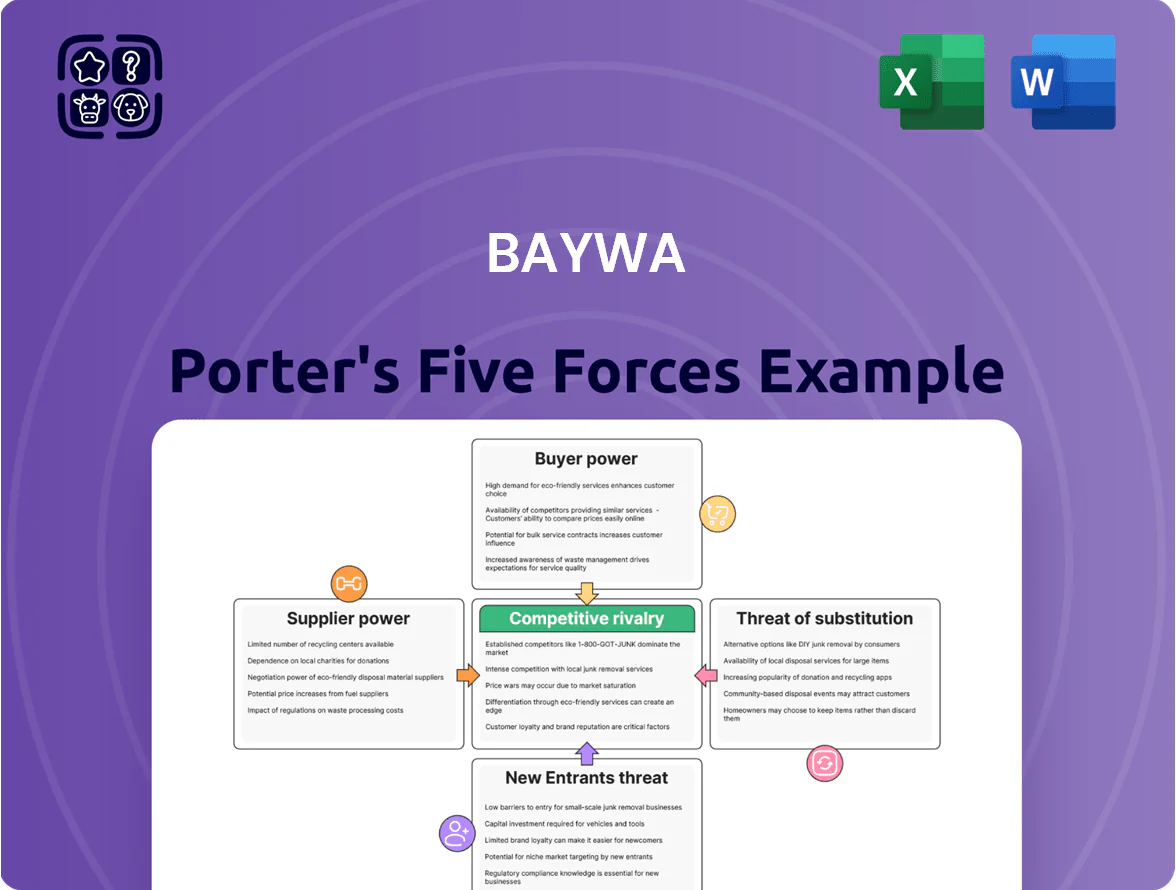

BayWa faces moderate supplier power and strong buyer sensitivity in its diversified agribusiness and energy segments, while competitive rivalry is intensified by global players and margin pressure from commodity cycles.

Barriers to entry are moderate—scale and distribution matter—while substitutes and regulatory shifts pose material strategic risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BayWa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of global agricultural input providers

BayWa depends on a handful of global seed, fertilizer and crop-protection firms—Bayer CropScience, Corteva, BASF and Nutrien—who together control over 60% of key seed and agrochemical market share (2023–24 estimates), giving them clear pricing power over inputs.

Industry consolidation—M&A that cut global competitors by ~30% since 2010—reduces BayWa’s alternative suppliers, raising switching costs and procurement risk.

During 2022–24 supply shocks and Russia-Ukraine disruptions, input availability trumped price; import delays and export curbs pushed spot fertilizer premiums up 40–70%, exposing BayWa’s supply-security vulnerability.

Dependence on renewable energy component manufacturers

BayWa r.e.'s expansion raises dependence on a few global makers of PV panels and turbine parts, notably Chinese firms that supplied ~70% of modules globally in 2023; this concentrates risk and gives suppliers pricing power.

Chinese supplier exposure subjects BayWa to tariffs, higher logistics costs—container rates spiked 180% in 2021–22—and to policy shifts like export curbs, raising procurement volatility.

Even as a major buyer, BayWa faces tight markets: global solar+wind component demand outstripped supply by an estimated 15–20% in 2024, keeping supplier leverage high.

Volatility in energy and raw material costs

Suppliers of fossil fuels and construction inputs trade on global indices (Brent, LME) so BayWa cannot negotiate prices; energy accounted for ~6% of BayWa Group COGS in 2024, forcing margin pressure when Brent rose 40% in 2022–23.

BayWa often absorbs hikes or cuts volumes; every €10/tonne rise in steel adds ~€15m pa to procurement for a €3bn materials spend (quick math).

By late 2025, demand for certified low‑carbon materials grew ~35% y/y, boosting pricing power of sustainable suppliers and raising BayWa’s sourcing costs and switch complexity.

Influence of financial capital providers

Following BayWa’s 2024–2025 financial restructurings, banks and institutional lenders now hold substantial leverage, setting interest rates and covenant terms that constrain capital allocation and M&A moves.

In 2025 BayWa had net debt ~EUR 1.1bn and interest coverage below 4x at times, so tight covenants can force asset sales or capex cuts to stay compliant.

Maintaining a strong credit profile (lower net debt/EBITDA, higher EBITDA interest cover) is essential to limit lender control over strategic decisions.

- Net debt ~EUR 1.1bn (2025)

- Interest coverage near 3.5–4.0x in 2025

- Covenants affect capex, dividends, M&A

- Lower leverage reduces lender bargaining power

Fragmentation of local agricultural producers

Individual farmers supplying grain and produce to BayWa have low bargaining power because there are tens of thousands of smallholders in Germany and Europe, few coordinated channels, and high dependence on BayWa’s aggregation and logistics network that handled roughly €12.6 billion in agricultural trading in 2024.

BayWa’s scale, storage footprint, and transport links make bypass costly for small farms, though rising producer cooperatives—about 1,200 registered in Germany as of 2024—can sometimes pool volume to push for better prices.

When cooperatives control a significant share of regional output, BayWa faces short-term price pressure, but overall supplier fragmentation keeps BayWa’s supplier bargaining power high.

- Many small suppliers → low individual leverage

- BayWa handled €12.6bn agri trading in 2024 → aggregator advantage

- ~1,200 German cooperatives (2024) → occasional consolidated pressure

- Cooperatives can demand better purchase prices

Supplier Concentration Spurs Price Power as BayWa Debt, Renewables Tightness Bite

Suppliers hold high leverage: top agrochemical/seed firms >60% share (2023–24), PV modules ~70% Chinese supply (2023), global solar+wind demand >supply by ~15–20% (2024), spot fertilizer premiums +40–70% (2022–24). BayWa net debt ~€1.1bn, interest cover ~3.5–4x (2025) limits negotiation. Small farmers weak; BayWa handled €12.6bn agri trading (2024).

| Metric | Value |

|---|---|

| Agro supplier share | >60% |

| PV module supply | ~70% |

| Demand vs supply (renew) | +15–20% |

| Net debt (2025) | €1.1bn |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitute threats, and entry barriers tailored to BayWa’s diversified agriculture, energy, and building materials operations, with strategic insights into pricing influence, market protection, and emerging disruptors.

A concise Porter's Five Forces summary for BayWa that highlights competitive pressures and relief points—ideal for swift strategic decisions and slide-ready reporting.

Customers Bargaining Power

Price sensitivity of agricultural producers

Sophistication of institutional energy buyers

Institutional buyers—utilities, multinationals, and pension funds—wield strong bargaining power, running strict tenders: 2024 IEA data shows corporate PPAs covered 28 GW globally, driving competitive pricing.

They demand full yield transparency and ESG proofs; 2025 surveys find 72% require third-party verification, pushing developers to disclose LCOE and carbon metrics.

With a deep pool of global developers, BayWa often concedes slimmer margins—winning large bids may cut EBITDA margins by 200–400 basis points on flagship deals.

Retail customer mobility in building materials

Individual consumers and small contractors in building materials face low switching costs and can compare prices quickly; a 2024 GfK survey showed 62% of hobbyists check multiple retailers before buying.

Large DIY chains and marketplaces like Obi, Hornbach, and Amazon push BayWa to improve logistics and offer expert consulting; BayWa reported €4.3bn materials revenue in FY2024, so margin pressure matters.

Brand loyalty is weak, tied to local stock and financing—34% of contractors cited credit terms as a top purchase driver in a 2023 trade poll.

Consolidation of food retail chains

BayWa sells into a concentrated food retail market where the top 5 supermarket chains hold ~60–70% market share in key European markets (2024), letting buyers set strict quality, delivery and price terms that compress supplier margins.

This buyer power forces BayWa to cut logistics costs, shorten lead times and invest in traceability; BayWa reported a 2024 gross margin of 9.8% in agricultural trade, underlining margin pressure.

- Top 5 retailers 60–70% share (2024)

- Buyers enforce quality, delivery, price

- BayWa 2024 agricultural trade gross margin 9.8%

- Requires supply-chain efficiency, traceability, faster lead times

Adoption of direct-to-consumer digital platforms

The rise of digital marketplaces lets some customers bypass intermediaries like BayWa and buy directly from manufacturers, cutting distributor margins and forcing BayWa to defend volume.

BayWa has invested in digital platforms—its 2024 online agri-trading volumes grew ~18% year-on-year—but internet transparency still gives buyers stronger price and spec info during negotiations.

To stay relevant BayWa must shift from simple product sales to bundled service models (logistics, financing, analytics); service revenues reduce churn and protect margins.

BayWa fights margin pressure—competitive pricing, RTPRO scale and traceability defend volumes

Buyers across BayWa’s segments hold strong price and quality leverage: EU farm incomes fell 3.5% in 2024, top‑5 food retailers hold 60–70% share (2024), and BayWa’s agri trade gross margin was 9.8% in 2024, forcing competitive pricing, service bundles (RTPRO 85,000 users in 2024) and traceability investments to defend volumes.

| Metric | 2024 |

|---|---|

| EU farm income change | -3.5% |

| Top‑5 retailer share | 60–70% |

| BayWa agri gross margin | 9.8% |

| RTPRO users | 85,000 |

Preview Before You Purchase

BayWa Porter's Five Forces Analysis

This preview shows the exact BayWa Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or samples.

You're viewing the final deliverable: the same comprehensive document will be available for instant download once your payment is complete.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

BayWa faces moderate supplier power and strong buyer sensitivity in its diversified agribusiness and energy segments, while competitive rivalry is intensified by global players and margin pressure from commodity cycles.

Barriers to entry are moderate—scale and distribution matter—while substitutes and regulatory shifts pose material strategic risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BayWa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of global agricultural input providers

BayWa depends on a handful of global seed, fertilizer and crop-protection firms—Bayer CropScience, Corteva, BASF and Nutrien—who together control over 60% of key seed and agrochemical market share (2023–24 estimates), giving them clear pricing power over inputs.

Industry consolidation—M&A that cut global competitors by ~30% since 2010—reduces BayWa’s alternative suppliers, raising switching costs and procurement risk.

During 2022–24 supply shocks and Russia-Ukraine disruptions, input availability trumped price; import delays and export curbs pushed spot fertilizer premiums up 40–70%, exposing BayWa’s supply-security vulnerability.

Dependence on renewable energy component manufacturers

BayWa r.e.'s expansion raises dependence on a few global makers of PV panels and turbine parts, notably Chinese firms that supplied ~70% of modules globally in 2023; this concentrates risk and gives suppliers pricing power.

Chinese supplier exposure subjects BayWa to tariffs, higher logistics costs—container rates spiked 180% in 2021–22—and to policy shifts like export curbs, raising procurement volatility.

Even as a major buyer, BayWa faces tight markets: global solar+wind component demand outstripped supply by an estimated 15–20% in 2024, keeping supplier leverage high.

Volatility in energy and raw material costs

Suppliers of fossil fuels and construction inputs trade on global indices (Brent, LME) so BayWa cannot negotiate prices; energy accounted for ~6% of BayWa Group COGS in 2024, forcing margin pressure when Brent rose 40% in 2022–23.

BayWa often absorbs hikes or cuts volumes; every €10/tonne rise in steel adds ~€15m pa to procurement for a €3bn materials spend (quick math).

By late 2025, demand for certified low‑carbon materials grew ~35% y/y, boosting pricing power of sustainable suppliers and raising BayWa’s sourcing costs and switch complexity.

Influence of financial capital providers

Following BayWa’s 2024–2025 financial restructurings, banks and institutional lenders now hold substantial leverage, setting interest rates and covenant terms that constrain capital allocation and M&A moves.

In 2025 BayWa had net debt ~EUR 1.1bn and interest coverage below 4x at times, so tight covenants can force asset sales or capex cuts to stay compliant.

Maintaining a strong credit profile (lower net debt/EBITDA, higher EBITDA interest cover) is essential to limit lender control over strategic decisions.

- Net debt ~EUR 1.1bn (2025)

- Interest coverage near 3.5–4.0x in 2025

- Covenants affect capex, dividends, M&A

- Lower leverage reduces lender bargaining power

Fragmentation of local agricultural producers

Individual farmers supplying grain and produce to BayWa have low bargaining power because there are tens of thousands of smallholders in Germany and Europe, few coordinated channels, and high dependence on BayWa’s aggregation and logistics network that handled roughly €12.6 billion in agricultural trading in 2024.

BayWa’s scale, storage footprint, and transport links make bypass costly for small farms, though rising producer cooperatives—about 1,200 registered in Germany as of 2024—can sometimes pool volume to push for better prices.

When cooperatives control a significant share of regional output, BayWa faces short-term price pressure, but overall supplier fragmentation keeps BayWa’s supplier bargaining power high.

- Many small suppliers → low individual leverage

- BayWa handled €12.6bn agri trading in 2024 → aggregator advantage

- ~1,200 German cooperatives (2024) → occasional consolidated pressure

- Cooperatives can demand better purchase prices

Supplier Concentration Spurs Price Power as BayWa Debt, Renewables Tightness Bite

Suppliers hold high leverage: top agrochemical/seed firms >60% share (2023–24), PV modules ~70% Chinese supply (2023), global solar+wind demand >supply by ~15–20% (2024), spot fertilizer premiums +40–70% (2022–24). BayWa net debt ~€1.1bn, interest cover ~3.5–4x (2025) limits negotiation. Small farmers weak; BayWa handled €12.6bn agri trading (2024).

| Metric | Value |

|---|---|

| Agro supplier share | >60% |

| PV module supply | ~70% |

| Demand vs supply (renew) | +15–20% |

| Net debt (2025) | €1.1bn |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitute threats, and entry barriers tailored to BayWa’s diversified agriculture, energy, and building materials operations, with strategic insights into pricing influence, market protection, and emerging disruptors.

A concise Porter's Five Forces summary for BayWa that highlights competitive pressures and relief points—ideal for swift strategic decisions and slide-ready reporting.

Customers Bargaining Power

Price sensitivity of agricultural producers

Sophistication of institutional energy buyers

Institutional buyers—utilities, multinationals, and pension funds—wield strong bargaining power, running strict tenders: 2024 IEA data shows corporate PPAs covered 28 GW globally, driving competitive pricing.

They demand full yield transparency and ESG proofs; 2025 surveys find 72% require third-party verification, pushing developers to disclose LCOE and carbon metrics.

With a deep pool of global developers, BayWa often concedes slimmer margins—winning large bids may cut EBITDA margins by 200–400 basis points on flagship deals.

Retail customer mobility in building materials

Individual consumers and small contractors in building materials face low switching costs and can compare prices quickly; a 2024 GfK survey showed 62% of hobbyists check multiple retailers before buying.

Large DIY chains and marketplaces like Obi, Hornbach, and Amazon push BayWa to improve logistics and offer expert consulting; BayWa reported €4.3bn materials revenue in FY2024, so margin pressure matters.

Brand loyalty is weak, tied to local stock and financing—34% of contractors cited credit terms as a top purchase driver in a 2023 trade poll.

Consolidation of food retail chains

BayWa sells into a concentrated food retail market where the top 5 supermarket chains hold ~60–70% market share in key European markets (2024), letting buyers set strict quality, delivery and price terms that compress supplier margins.

This buyer power forces BayWa to cut logistics costs, shorten lead times and invest in traceability; BayWa reported a 2024 gross margin of 9.8% in agricultural trade, underlining margin pressure.

- Top 5 retailers 60–70% share (2024)

- Buyers enforce quality, delivery, price

- BayWa 2024 agricultural trade gross margin 9.8%

- Requires supply-chain efficiency, traceability, faster lead times

Adoption of direct-to-consumer digital platforms

The rise of digital marketplaces lets some customers bypass intermediaries like BayWa and buy directly from manufacturers, cutting distributor margins and forcing BayWa to defend volume.

BayWa has invested in digital platforms—its 2024 online agri-trading volumes grew ~18% year-on-year—but internet transparency still gives buyers stronger price and spec info during negotiations.

To stay relevant BayWa must shift from simple product sales to bundled service models (logistics, financing, analytics); service revenues reduce churn and protect margins.

BayWa fights margin pressure—competitive pricing, RTPRO scale and traceability defend volumes

Buyers across BayWa’s segments hold strong price and quality leverage: EU farm incomes fell 3.5% in 2024, top‑5 food retailers hold 60–70% share (2024), and BayWa’s agri trade gross margin was 9.8% in 2024, forcing competitive pricing, service bundles (RTPRO 85,000 users in 2024) and traceability investments to defend volumes.

| Metric | 2024 |

|---|---|

| EU farm income change | -3.5% |

| Top‑5 retailer share | 60–70% |

| BayWa agri gross margin | 9.8% |

| RTPRO users | 85,000 |

Preview Before You Purchase

BayWa Porter's Five Forces Analysis

This preview shows the exact BayWa Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or samples.

You're viewing the final deliverable: the same comprehensive document will be available for instant download once your payment is complete.