BBMG Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

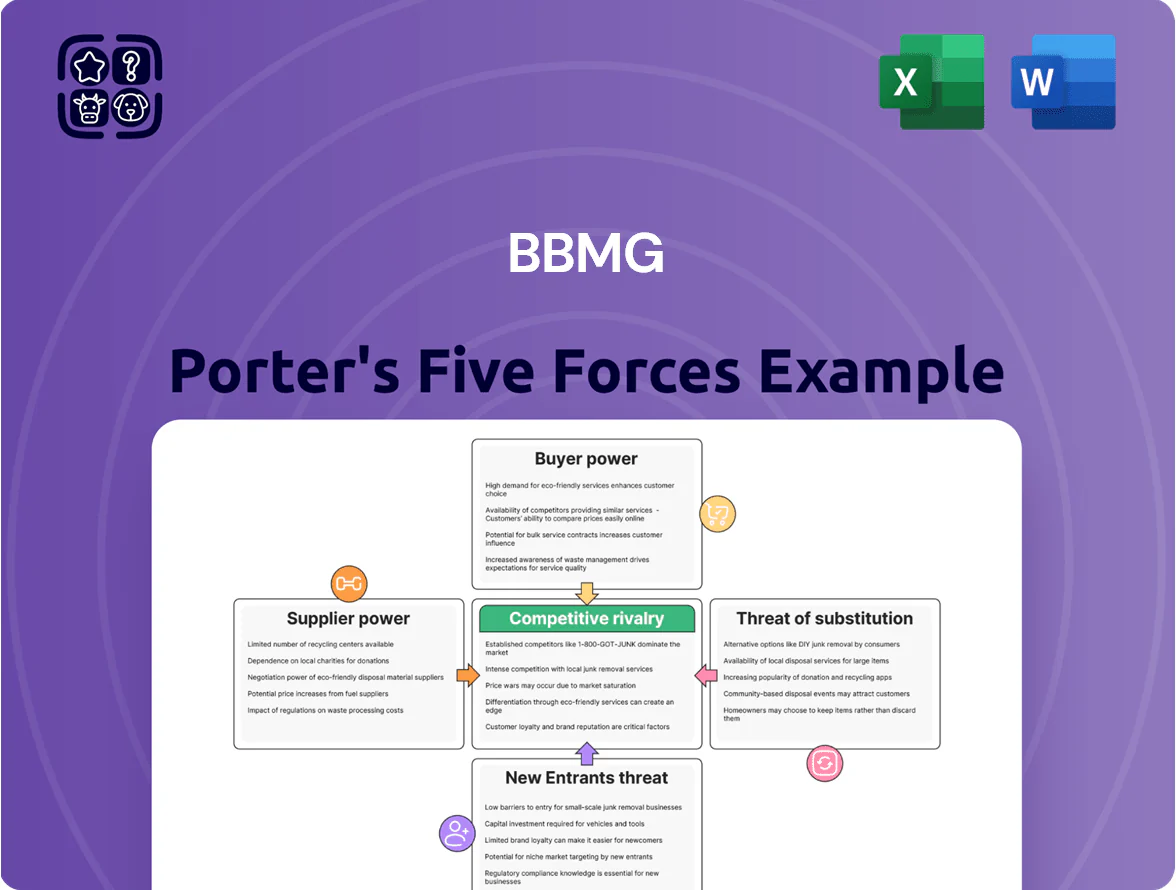

BBMG faces moderate supplier leverage and cyclical demand pressures, while established scale limits immediate new-entrant threats—yet substitute materials and regulatory shifts could intensify competition; this snapshot highlights key tensions shaping margins and strategic choices.

Suppliers Bargaining Power

Volatility of Energy and Coal Costs

BBMG’s cement plants consume ~60–70% of operating energy in coal and electricity, so a 20% rise in coal prices in 2025 raised input costs materially; supplier leverage tightened as global carbon policies pushed coal premiums up ~15% vs 2023.

Access to Raw Limestone Resources

Access to limestone and aggregates is vital for BBMG’s cement and building-materials output; owning mines and long-term concessions covers ~60–70% of its clinker needs, lowering input cost volatility versus smaller rivals.

Still, China’s tightened quarry permits since 2020 and a 2024 permit backlog estimate of ~15% raise bargaining power for existing resource holders, forcing BBMG to manage regulatory risk to keep feedstock supply and margins stable.

Logistics and Transportation Constraints

BBMG relies on rail, road and water to move cement and steel; in 2024 China rail freight volume hit 3.9 trillion tonne‑km, so logistics providers have moderate leverage in congested regions and upgrade zones.

BBMG’s in‑house logistics cuts supplier power—own fleet handled ~28% of shipments in 2023—but external carriers still set prices for international and specialized cargo.

Fuel volatility matters: diesel averaged 1.02 CNY/liter in 2024, driving 6–9% swings in transport costs and tightening negotiations with service providers.

Technological Equipment Providers

Technological equipment providers hold strong bargaining power as smart manufacturing and green cement tech require specialized machinery and software from a handful of global leaders; global smart factory kit revenue hit about USD 215 billion in 2024, concentrating supplier leverage.

BBMG faces high switching costs once a vendor ecosystem is embedded—estimated integration and downtime can exceed CNY 100–200 million per plant—so strategic partnerships are critical to maintain tech edge and cost control.

- Few qualified vendors: raises supplier leverage

- Smart factory market: ~USD 215B (2024)

- Integration cost per plant: ~CNY 100–200M

- Long-term partnerships reduce upgrade risk

Labor Market Dynamics in Construction

Availability of skilled labor for manufacturing and property development is a key supplier risk for BBMG; China’s urban construction skilled-labor shortages pushed average construction wages up ~6.8% in 2024 and heavy-industry workforce fell 2.1% YoY, empowering unions and specialist firms.

BBMG must pay competitive wages and benefits to keep technical staff for modern production lines; upward labor cost pressure reduced Chinese cement makers’ EBITDA margins by ~150–250bps in 2024, squeezing BBMG’s margins too.

- Skilled-labor shortages: +6.8% construction wages 2024

- Workforce shrink: −2.1% heavy industry YoY

- Margin impact: ~150–250bps EBITDA hit in 2024

- Action: competitive pay/benefits to retain tech staff

Suppliers squeeze margins as coal, diesel, wages surge—BBMG offsets with 65% clinker self‑supply

Suppliers exert moderate‑to‑high power: energy and specialized equipment costs drove input pressure (coal +20% in 2025; smart factory market ~USD 215B in 2024), BBMG’s mine ownership covers ~65% clinker needs, in‑house logistics 28% shipments, diesel 1.02 CNY/L (2024) shifted transport costs 6–9%, and labor wage rises (+6.8% 2024) cut peers’ EBITDA by ~150–250bps.

| Metric | Value |

|---|---|

| Clinker self-supply | ~65% |

| In-house logistics | 28% |

| Coal price change (2025) | +20% |

| Diesel (2024) | 1.02 CNY/L |

| Smart factory market (2024) | USD 215B |

| Wage rise (2024) | +6.8% |

| EBITDA impact | −150–250bps |

What is included in the product

Uncovers BBMG’s competitive pressure by analyzing supplier and buyer power, threat of new entrants, substitutes, and rivalry—highlighting disruptive threats and strategic levers to protect market share.

A one-sheet Porter’s Five Forces snapshot that quantifies competitive pressure and highlights relief strategies—ideal for rapid strategy sessions and investor decks.

Customers Bargaining Power

Consolidation of Infrastructure Buyers

Real Estate Market Sensitivity

Individual homebuyers and private developers are BBMG’s main customers for property development and residential materials; in 2024 China mortgage approvals fell ~18% year-over-year, raising buyer price sensitivity and shifting bargaining power to customers during downturns.

When the market cools, buyers routinely push for higher-quality finishes and more amenities at lower prices—transactions in weaker cities saw average discounting rise to ~7–10% in 2024.

BBMG must protect its pricing floor by strengthening brand reputation and obtaining sustainable building certifications (eg, China Green Building Evaluation Standard) that supported 3–5% price premiums in recent studies.

Low Switching Costs in Commodity Cement

In commodity cement and aggregate markets customers face low switching costs, so large construction firms can shift suppliers quickly if BBMG’s price or delivery lags; China’s top 100 builders account for ~35% of volume, raising price sensitivity. This weak brand loyalty forces BBMG to chase operational efficiency—lowering unit cost and logistics spend—to defend margin (cement avg. EBITDA margin ~18% in 2024). BBMG is shifting into specialized, high-performance materials with higher switching costs, such as blended cements and admixtures, which grew 12% y/y in 2024 to reduce churn.

Impact of Digital Procurement Platforms

The rise of B2B digital marketplaces has increased price transparency for building materials, empowering buyers to compare BBMG against regional peers in real time and pressuring margins—online listings cut price dispersion by ~15% in construction materials in 2024 (McKinsey).

Platforms let small buyers aggregate demand, creating collective bargaining power; BBMG’s 2024 e-sales grew to 12% of revenue as it launched its own digital channels and value-added services to retain direct relationships.

- Price transparency up ~15% (2024)

- BBMG e-sales 12% of revenue (2024)

- Buyers aggregate demand → stronger bargaining

- BBMG digital channels to protect margins

Demand for Green and Certified Materials

As China tightens emissions rules, corporate buyers demand low-carbon cement and green certifications to hit ESG targets, giving customers leverage to switch suppliers; by 2025, documented product carbon footprints (EPDs) are expected as a standard requirement.

BBMG risks share loss to nimble green rivals unless it shifts its portfolio, invests in low-clinker mixes and CCUS (carbon capture) and prices transparently—buyers can effectively boycott traditional materials.

- By 2025: EPDs standard;

- Green premium: buyers pay 5–15% more;

- BBMG must cut clinker ratio ~20% to match peers;

- Failure risks regional market share loss ≥5%.

BBMG faces institutional pricing pressure; pivots to higher‑margin blends amid weak retail

Large institutional buyers (62% revenue, 2024) and top 100 builders (~35% volume) exert strong price/term leverage, forcing ~7% average contract discounts (2023) and sensitivity to a 1% infrastructure spend cut → ~0.8% revenue hit. Retail/homebuyer weakness (mortgage approvals -18% y/y, 2024) raises price sensitivity; low switching costs in commodities push BBMG toward higher-margin blended products (+12% y/y, 2024).

| Metric | Value |

|---|---|

| Share from gov/projects | 62% (2024) |

| Top builders volume | ~35% |

| Avg contract discount | ~7% (2023) |

| Mortgage approvals | -18% y/y (2024) |

| Blended products growth | +12% y/y (2024) |

Same Document Delivered

BBMG Porter's Five Forces Analysis

This preview shows the exact BBMG Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and professionally written.

The document displayed here is the same ready-to-download file included with your purchase, containing complete assessment of competitive rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry.

You're viewing the final deliverable; once payment is complete you’ll get instant access to this identical, ready-to-use analysis for your decision-making and reporting needs.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

BBMG faces moderate supplier leverage and cyclical demand pressures, while established scale limits immediate new-entrant threats—yet substitute materials and regulatory shifts could intensify competition; this snapshot highlights key tensions shaping margins and strategic choices.

Suppliers Bargaining Power

Volatility of Energy and Coal Costs

BBMG’s cement plants consume ~60–70% of operating energy in coal and electricity, so a 20% rise in coal prices in 2025 raised input costs materially; supplier leverage tightened as global carbon policies pushed coal premiums up ~15% vs 2023.

Access to Raw Limestone Resources

Access to limestone and aggregates is vital for BBMG’s cement and building-materials output; owning mines and long-term concessions covers ~60–70% of its clinker needs, lowering input cost volatility versus smaller rivals.

Still, China’s tightened quarry permits since 2020 and a 2024 permit backlog estimate of ~15% raise bargaining power for existing resource holders, forcing BBMG to manage regulatory risk to keep feedstock supply and margins stable.

Logistics and Transportation Constraints

BBMG relies on rail, road and water to move cement and steel; in 2024 China rail freight volume hit 3.9 trillion tonne‑km, so logistics providers have moderate leverage in congested regions and upgrade zones.

BBMG’s in‑house logistics cuts supplier power—own fleet handled ~28% of shipments in 2023—but external carriers still set prices for international and specialized cargo.

Fuel volatility matters: diesel averaged 1.02 CNY/liter in 2024, driving 6–9% swings in transport costs and tightening negotiations with service providers.

Technological Equipment Providers

Technological equipment providers hold strong bargaining power as smart manufacturing and green cement tech require specialized machinery and software from a handful of global leaders; global smart factory kit revenue hit about USD 215 billion in 2024, concentrating supplier leverage.

BBMG faces high switching costs once a vendor ecosystem is embedded—estimated integration and downtime can exceed CNY 100–200 million per plant—so strategic partnerships are critical to maintain tech edge and cost control.

- Few qualified vendors: raises supplier leverage

- Smart factory market: ~USD 215B (2024)

- Integration cost per plant: ~CNY 100–200M

- Long-term partnerships reduce upgrade risk

Labor Market Dynamics in Construction

Availability of skilled labor for manufacturing and property development is a key supplier risk for BBMG; China’s urban construction skilled-labor shortages pushed average construction wages up ~6.8% in 2024 and heavy-industry workforce fell 2.1% YoY, empowering unions and specialist firms.

BBMG must pay competitive wages and benefits to keep technical staff for modern production lines; upward labor cost pressure reduced Chinese cement makers’ EBITDA margins by ~150–250bps in 2024, squeezing BBMG’s margins too.

- Skilled-labor shortages: +6.8% construction wages 2024

- Workforce shrink: −2.1% heavy industry YoY

- Margin impact: ~150–250bps EBITDA hit in 2024

- Action: competitive pay/benefits to retain tech staff

Suppliers squeeze margins as coal, diesel, wages surge—BBMG offsets with 65% clinker self‑supply

Suppliers exert moderate‑to‑high power: energy and specialized equipment costs drove input pressure (coal +20% in 2025; smart factory market ~USD 215B in 2024), BBMG’s mine ownership covers ~65% clinker needs, in‑house logistics 28% shipments, diesel 1.02 CNY/L (2024) shifted transport costs 6–9%, and labor wage rises (+6.8% 2024) cut peers’ EBITDA by ~150–250bps.

| Metric | Value |

|---|---|

| Clinker self-supply | ~65% |

| In-house logistics | 28% |

| Coal price change (2025) | +20% |

| Diesel (2024) | 1.02 CNY/L |

| Smart factory market (2024) | USD 215B |

| Wage rise (2024) | +6.8% |

| EBITDA impact | −150–250bps |

What is included in the product

Uncovers BBMG’s competitive pressure by analyzing supplier and buyer power, threat of new entrants, substitutes, and rivalry—highlighting disruptive threats and strategic levers to protect market share.

A one-sheet Porter’s Five Forces snapshot that quantifies competitive pressure and highlights relief strategies—ideal for rapid strategy sessions and investor decks.

Customers Bargaining Power

Consolidation of Infrastructure Buyers

Real Estate Market Sensitivity

Individual homebuyers and private developers are BBMG’s main customers for property development and residential materials; in 2024 China mortgage approvals fell ~18% year-over-year, raising buyer price sensitivity and shifting bargaining power to customers during downturns.

When the market cools, buyers routinely push for higher-quality finishes and more amenities at lower prices—transactions in weaker cities saw average discounting rise to ~7–10% in 2024.

BBMG must protect its pricing floor by strengthening brand reputation and obtaining sustainable building certifications (eg, China Green Building Evaluation Standard) that supported 3–5% price premiums in recent studies.

Low Switching Costs in Commodity Cement

In commodity cement and aggregate markets customers face low switching costs, so large construction firms can shift suppliers quickly if BBMG’s price or delivery lags; China’s top 100 builders account for ~35% of volume, raising price sensitivity. This weak brand loyalty forces BBMG to chase operational efficiency—lowering unit cost and logistics spend—to defend margin (cement avg. EBITDA margin ~18% in 2024). BBMG is shifting into specialized, high-performance materials with higher switching costs, such as blended cements and admixtures, which grew 12% y/y in 2024 to reduce churn.

Impact of Digital Procurement Platforms

The rise of B2B digital marketplaces has increased price transparency for building materials, empowering buyers to compare BBMG against regional peers in real time and pressuring margins—online listings cut price dispersion by ~15% in construction materials in 2024 (McKinsey).

Platforms let small buyers aggregate demand, creating collective bargaining power; BBMG’s 2024 e-sales grew to 12% of revenue as it launched its own digital channels and value-added services to retain direct relationships.

- Price transparency up ~15% (2024)

- BBMG e-sales 12% of revenue (2024)

- Buyers aggregate demand → stronger bargaining

- BBMG digital channels to protect margins

Demand for Green and Certified Materials

As China tightens emissions rules, corporate buyers demand low-carbon cement and green certifications to hit ESG targets, giving customers leverage to switch suppliers; by 2025, documented product carbon footprints (EPDs) are expected as a standard requirement.

BBMG risks share loss to nimble green rivals unless it shifts its portfolio, invests in low-clinker mixes and CCUS (carbon capture) and prices transparently—buyers can effectively boycott traditional materials.

- By 2025: EPDs standard;

- Green premium: buyers pay 5–15% more;

- BBMG must cut clinker ratio ~20% to match peers;

- Failure risks regional market share loss ≥5%.

BBMG faces institutional pricing pressure; pivots to higher‑margin blends amid weak retail

Large institutional buyers (62% revenue, 2024) and top 100 builders (~35% volume) exert strong price/term leverage, forcing ~7% average contract discounts (2023) and sensitivity to a 1% infrastructure spend cut → ~0.8% revenue hit. Retail/homebuyer weakness (mortgage approvals -18% y/y, 2024) raises price sensitivity; low switching costs in commodities push BBMG toward higher-margin blended products (+12% y/y, 2024).

| Metric | Value |

|---|---|

| Share from gov/projects | 62% (2024) |

| Top builders volume | ~35% |

| Avg contract discount | ~7% (2023) |

| Mortgage approvals | -18% y/y (2024) |

| Blended products growth | +12% y/y (2024) |

Same Document Delivered

BBMG Porter's Five Forces Analysis

This preview shows the exact BBMG Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and professionally written.

The document displayed here is the same ready-to-download file included with your purchase, containing complete assessment of competitive rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry.

You're viewing the final deliverable; once payment is complete you’ll get instant access to this identical, ready-to-use analysis for your decision-making and reporting needs.