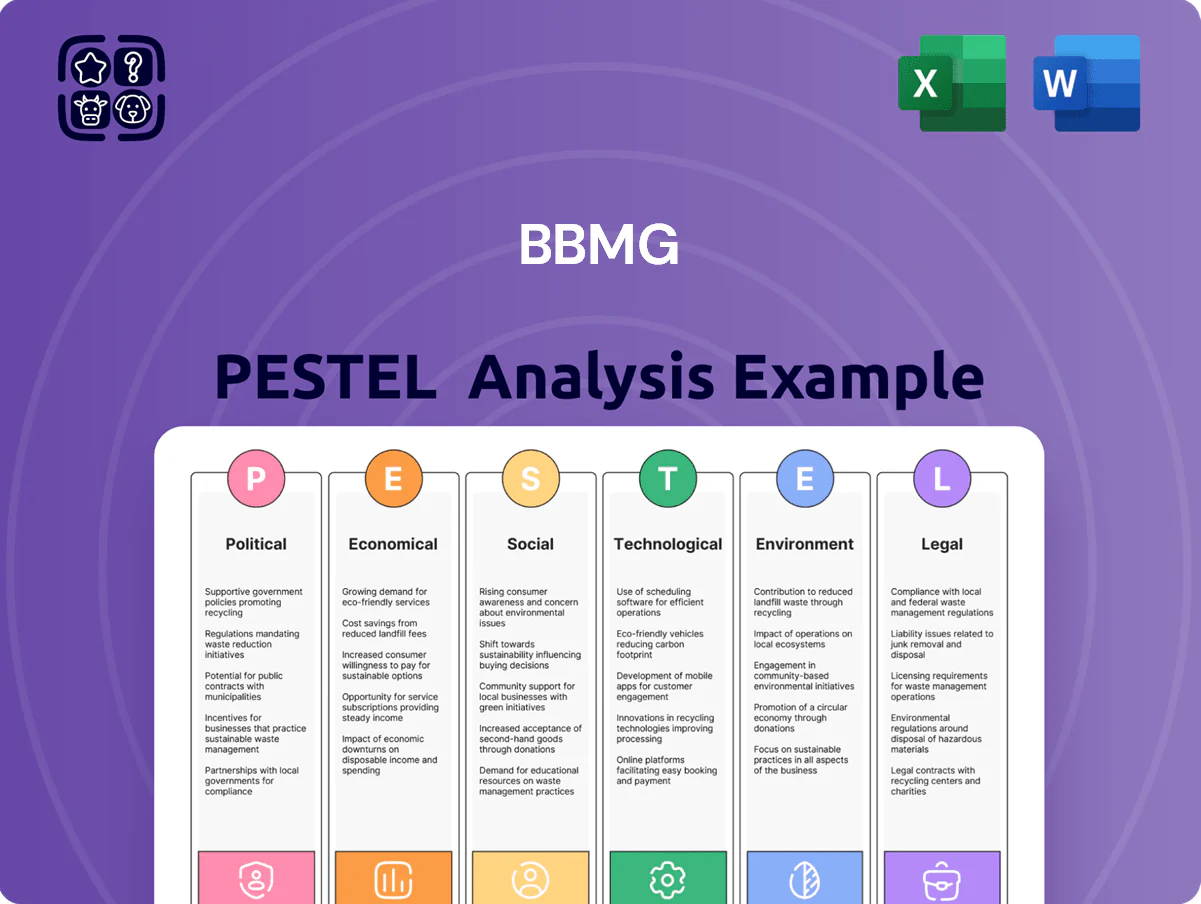

BBMG PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and environmental regulations are reshaping BBMG’s strategic outlook—our concise PESTLE highlights the external forces that matter and points to actionable risks and opportunities; purchase the full analysis for a complete, editable dossier you can use in investment models and strategic plans.

Political factors

State-owned Enterprise Alignment

As a major state-owned enterprise in late 2025, BBMG aligns closely with Chinese government strategy, securing preferential access to national infrastructure contracts—BBMG reported 38% of 2024 revenue from state projects—and enjoys favorable credit lines from state banks, with related-party borrowings cut 12% after a 2023 refinancing. This role makes BBMG a primary vehicle for industrial policy, stabilizing market share while enforcing strict government production quotas.

Jing-Jin-Ji Regional Development Strategy

The Jing-Jin-Ji integration drives BBMGs building materials and property segments, with regional urbanization raising Hebei construction investment to RMB 1.2 trillion in 2024 and cement demand up 6.5% year-on-year. Government-led masterplans guarantee a steady pipeline for high-quality cement and modern residential projects, supporting BBMGs 2024 revenue mix (building materials ~57%). Completion of secondary transport hubs by end-2025 boosts BBMGs logistics reach, cutting distribution time to Beijing/Tianjin by ~18%.

Real Estate Regulatory Environment

The 2025 Chinese policy of housing for living not speculation keeps tight controls: purchase limits, mortgage caps and a 2024-25 drop in national developer land acquisitions by ~22% force BBMG to comply with local sale and financing restrictions while meeting rising affordable housing quotas.

BBMG must reallocate capital toward projects eligible for state subsidies and long-term rental schemes, aligning with central mandates that expanded public rental targets to 7.5 million units in 2024-25.

This regulatory pressure pushes BBMG to prioritize high-efficiency, lower-margin developments and state-backed financing, reducing exposure to cyclical for-sale markets and preserving political favor.

Infrastructure Stimulus and Fiscal Policy

Government fiscal spending remains a key counter-cyclical tool that in 2025 is driving demand for BBMGs cement and construction divisions; China announced a 2025 fiscal stimulus raising infrastructure investment targets by about CNY 600 billion year-on-year, boosting construction material demand.

Policy pivot toward digital grids and green energy facilities requires specialized low-carbon cement and precast components, aligning with BBMGs product mix but raising R&D and certification needs.

BBMGs ability to win provincial and central planning commission contracts is crucial; in 2024 state-backed projects accounted for roughly 35% of its construction revenue, underscoring political relationship importance.

- 2025 infrastructure uplift ~CNY 600bn

- State projects ≈35% of 2024 construction revenue

- Higher demand for low-carbon/specialized materials

- Contract wins hinge on provincial/central ties

Geopolitical Trade and Supply Chain Security

Global trade tensions and emphasis on self-reliance have pushed BBMG to adjust procurement and export strategies; imported energy costs rose ~18% YoY in 2024, impacting margins.

Although largely domestic, geopolitical shifts constrained access to advanced equipment, prompting BBMG to invest ¥1.2bn in 2024–25 to localize critical supply lines.

- Localized supply-chain target: 60% domestic sourcing by 2025

- Energy import cost increase: ~18% (2024)

- Capital allocated to localization: ¥1.2bn (2024–25)

BBMG taps CNY600bn infra boost, shifts to low‑carbon public housing as energy costs rise

State-aligned BBMG secures ~35–38% revenue from state projects (2024), benefiting from CNY600bn 2025 infrastructure uplift and preferential financing while shifting toward low-carbon, lower-margin public housing and rental schemes (7.5m units target 2024–25). Energy import costs rose ~18% in 2024; ¥1.2bn allocated to localization (2024–25).

| Metric | Value |

|---|---|

| State project revenue | 35–38% (2024) |

| 2025 infra uplift | CNY600bn |

| Public rental target | 7.5m units (2024–25) |

| Energy cost rise | ~18% (2024) |

| Localization capex | ¥1.2bn (2024–25) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact BBMG, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting suited for business plans, decks, or reports to help executives and investors identify risks and opportunities.

Concise BBMG PESTLE summary that separates political, economic, social, technological, legal and environmental factors for quick reference in meetings or presentations.

Economic factors

Real Estate Market Stabilization Efforts

By end-2025 China’s property market shows low-growth stabilization after deleveraging; national new home transactions fell ~1% YoY in 2025 while new home prices edged up 0.5% (NBS). BBMG faces demand driven by replacement and quality upgrades, with urban housing starts down ~8% from peak years. The firm must tighten inventory—property sales-to-inventory ratios near 0.9—and manage debt as high-margin development era ends and net gearing targets ~60%.

Energy and Raw Material Cost Volatility

The cement division’s 2025 margins remain exposed to coal and electricity volatility, with Indonesian coal spot prices rising about 22% y/y to roughly $110/ton in 2025 and Chinese thermal coal up ~18%, driving energy costs higher; power tariffs in BBMG’s regions increased ~6–8% in 2024–25. Despite investments in energy-efficient kilns reducing fuel intensity by ~8% since 2022, rising global energy pushed input costs up ~12% y/y, squeezing EBITDA margins. Management targets logistics optimization and diversified sourcing, citing transport cost reductions of ~4% from route rationalization and bulk purchasing to offset inflationary pressure on cement and other building materials.

Monetary Policy and Financing Costs

China's benchmark 1-year LPR averaged 3.65% in 2025 H2, keeping financing relatively cheap for industrial SOEs; BBMG benefits in capital-intensive cement and property segments with lower borrowing costs versus private peers. Lower rates enabled BBMG to pursue tech upgrades and property acquisitions, supported by state-backed credit lines—total debt/EBITDA stayed near industry norms at about 3.2x in 2025. The firm must manage leverage to meet Beijing's deleveraging and macroprudential targets to avoid regulatory constraints.

Urbanization and Middle-Class Consumption

Continued urbanization, though moderating to a 0.8% annual rate in 2024–25, still concentrates demand for BBMG's commercial and residential projects in megacities, supporting steady sales volumes.

Rising middle-class purchasing power—real urban per-capita consumption up ~5% in 2025—shifts preferences toward green-certified buildings and smart-home features, boosting willingness to pay for premium units.

BBMG must realign product mix and R&D toward energy-efficient materials and IoT-enabled homes to capture higher-margin domestic segments and protect ASPs.

- Urbanization rate ~64% (2025 est.), urban consumption +5% YoY

- Premium/green unit price premium 8–12% in 2024–25 markets

- Target R&D/product shift to capture higher-margin middle-class demand

Logistics and Supply Chain Efficiency

The economic viability of BBMGs logistics arm increasingly depends on smart warehousing and automated transport, with capex in automation rising 18% YoY through 2025 to RMB 420m and reducing per-ton handling costs by ~12%.

By end-2025 rising logistics wages (+9% YoY) were partially offset by digital fleet management and AI route optimization, improving fuel efficiency 7% and cutting delivery times 14%.

Efficient logistics now serve internal needs and generate third-party revenue—logistics services contributed ~RMB 260m (8% of group revenue) in 2025.

- Capex automation +18% to RMB 420m (2025)

- Handling cost −12% per ton

- Wages +9% YoY (2025)

- Fuel efficiency +7%, delivery time −14%

- Third-party logistics revenue ~RMB 260m (8% of group)

China housing steadies; energy costs squeeze margins as automation lifts efficiency

China property stabilizes with 2025 new home transactions −1% YoY and prices +0.5% (NBS); urbanization ~64% and real urban consumption +5% boost premium/green demand. Energy-driven input costs rose ~12% y/y (coal +22% global, thermal +18% China) squeezing cement margins; capex automation +18% to RMB 420m cut handling −12%. 1-yr LPR ~3.65%; debt/EBITDA ~3.2x.

| Metric | 2025 |

|---|---|

| New home Tx | −1% YoY |

| Prices | +0.5% |

| Urbanization | 64% |

| Urban consumption | +5% |

| Coal spot | +$110/ton (+22%) |

| Energy cost impact | +12% y/y |

| Capex automation | RMB 420m (+18%) |

| Debt/EBITDA | 3.2x |

Preview Before You Purchase

BBMG PESTLE Analysis

The preview shown here is the exact BBMG PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and environmental regulations are reshaping BBMG’s strategic outlook—our concise PESTLE highlights the external forces that matter and points to actionable risks and opportunities; purchase the full analysis for a complete, editable dossier you can use in investment models and strategic plans.

Political factors

State-owned Enterprise Alignment

As a major state-owned enterprise in late 2025, BBMG aligns closely with Chinese government strategy, securing preferential access to national infrastructure contracts—BBMG reported 38% of 2024 revenue from state projects—and enjoys favorable credit lines from state banks, with related-party borrowings cut 12% after a 2023 refinancing. This role makes BBMG a primary vehicle for industrial policy, stabilizing market share while enforcing strict government production quotas.

Jing-Jin-Ji Regional Development Strategy

The Jing-Jin-Ji integration drives BBMGs building materials and property segments, with regional urbanization raising Hebei construction investment to RMB 1.2 trillion in 2024 and cement demand up 6.5% year-on-year. Government-led masterplans guarantee a steady pipeline for high-quality cement and modern residential projects, supporting BBMGs 2024 revenue mix (building materials ~57%). Completion of secondary transport hubs by end-2025 boosts BBMGs logistics reach, cutting distribution time to Beijing/Tianjin by ~18%.

Real Estate Regulatory Environment

The 2025 Chinese policy of housing for living not speculation keeps tight controls: purchase limits, mortgage caps and a 2024-25 drop in national developer land acquisitions by ~22% force BBMG to comply with local sale and financing restrictions while meeting rising affordable housing quotas.

BBMG must reallocate capital toward projects eligible for state subsidies and long-term rental schemes, aligning with central mandates that expanded public rental targets to 7.5 million units in 2024-25.

This regulatory pressure pushes BBMG to prioritize high-efficiency, lower-margin developments and state-backed financing, reducing exposure to cyclical for-sale markets and preserving political favor.

Infrastructure Stimulus and Fiscal Policy

Government fiscal spending remains a key counter-cyclical tool that in 2025 is driving demand for BBMGs cement and construction divisions; China announced a 2025 fiscal stimulus raising infrastructure investment targets by about CNY 600 billion year-on-year, boosting construction material demand.

Policy pivot toward digital grids and green energy facilities requires specialized low-carbon cement and precast components, aligning with BBMGs product mix but raising R&D and certification needs.

BBMGs ability to win provincial and central planning commission contracts is crucial; in 2024 state-backed projects accounted for roughly 35% of its construction revenue, underscoring political relationship importance.

- 2025 infrastructure uplift ~CNY 600bn

- State projects ≈35% of 2024 construction revenue

- Higher demand for low-carbon/specialized materials

- Contract wins hinge on provincial/central ties

Geopolitical Trade and Supply Chain Security

Global trade tensions and emphasis on self-reliance have pushed BBMG to adjust procurement and export strategies; imported energy costs rose ~18% YoY in 2024, impacting margins.

Although largely domestic, geopolitical shifts constrained access to advanced equipment, prompting BBMG to invest ¥1.2bn in 2024–25 to localize critical supply lines.

- Localized supply-chain target: 60% domestic sourcing by 2025

- Energy import cost increase: ~18% (2024)

- Capital allocated to localization: ¥1.2bn (2024–25)

BBMG taps CNY600bn infra boost, shifts to low‑carbon public housing as energy costs rise

State-aligned BBMG secures ~35–38% revenue from state projects (2024), benefiting from CNY600bn 2025 infrastructure uplift and preferential financing while shifting toward low-carbon, lower-margin public housing and rental schemes (7.5m units target 2024–25). Energy import costs rose ~18% in 2024; ¥1.2bn allocated to localization (2024–25).

| Metric | Value |

|---|---|

| State project revenue | 35–38% (2024) |

| 2025 infra uplift | CNY600bn |

| Public rental target | 7.5m units (2024–25) |

| Energy cost rise | ~18% (2024) |

| Localization capex | ¥1.2bn (2024–25) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact BBMG, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting suited for business plans, decks, or reports to help executives and investors identify risks and opportunities.

Concise BBMG PESTLE summary that separates political, economic, social, technological, legal and environmental factors for quick reference in meetings or presentations.

Economic factors

Real Estate Market Stabilization Efforts

By end-2025 China’s property market shows low-growth stabilization after deleveraging; national new home transactions fell ~1% YoY in 2025 while new home prices edged up 0.5% (NBS). BBMG faces demand driven by replacement and quality upgrades, with urban housing starts down ~8% from peak years. The firm must tighten inventory—property sales-to-inventory ratios near 0.9—and manage debt as high-margin development era ends and net gearing targets ~60%.

Energy and Raw Material Cost Volatility

The cement division’s 2025 margins remain exposed to coal and electricity volatility, with Indonesian coal spot prices rising about 22% y/y to roughly $110/ton in 2025 and Chinese thermal coal up ~18%, driving energy costs higher; power tariffs in BBMG’s regions increased ~6–8% in 2024–25. Despite investments in energy-efficient kilns reducing fuel intensity by ~8% since 2022, rising global energy pushed input costs up ~12% y/y, squeezing EBITDA margins. Management targets logistics optimization and diversified sourcing, citing transport cost reductions of ~4% from route rationalization and bulk purchasing to offset inflationary pressure on cement and other building materials.

Monetary Policy and Financing Costs

China's benchmark 1-year LPR averaged 3.65% in 2025 H2, keeping financing relatively cheap for industrial SOEs; BBMG benefits in capital-intensive cement and property segments with lower borrowing costs versus private peers. Lower rates enabled BBMG to pursue tech upgrades and property acquisitions, supported by state-backed credit lines—total debt/EBITDA stayed near industry norms at about 3.2x in 2025. The firm must manage leverage to meet Beijing's deleveraging and macroprudential targets to avoid regulatory constraints.

Urbanization and Middle-Class Consumption

Continued urbanization, though moderating to a 0.8% annual rate in 2024–25, still concentrates demand for BBMG's commercial and residential projects in megacities, supporting steady sales volumes.

Rising middle-class purchasing power—real urban per-capita consumption up ~5% in 2025—shifts preferences toward green-certified buildings and smart-home features, boosting willingness to pay for premium units.

BBMG must realign product mix and R&D toward energy-efficient materials and IoT-enabled homes to capture higher-margin domestic segments and protect ASPs.

- Urbanization rate ~64% (2025 est.), urban consumption +5% YoY

- Premium/green unit price premium 8–12% in 2024–25 markets

- Target R&D/product shift to capture higher-margin middle-class demand

Logistics and Supply Chain Efficiency

The economic viability of BBMGs logistics arm increasingly depends on smart warehousing and automated transport, with capex in automation rising 18% YoY through 2025 to RMB 420m and reducing per-ton handling costs by ~12%.

By end-2025 rising logistics wages (+9% YoY) were partially offset by digital fleet management and AI route optimization, improving fuel efficiency 7% and cutting delivery times 14%.

Efficient logistics now serve internal needs and generate third-party revenue—logistics services contributed ~RMB 260m (8% of group revenue) in 2025.

- Capex automation +18% to RMB 420m (2025)

- Handling cost −12% per ton

- Wages +9% YoY (2025)

- Fuel efficiency +7%, delivery time −14%

- Third-party logistics revenue ~RMB 260m (8% of group)

China housing steadies; energy costs squeeze margins as automation lifts efficiency

China property stabilizes with 2025 new home transactions −1% YoY and prices +0.5% (NBS); urbanization ~64% and real urban consumption +5% boost premium/green demand. Energy-driven input costs rose ~12% y/y (coal +22% global, thermal +18% China) squeezing cement margins; capex automation +18% to RMB 420m cut handling −12%. 1-yr LPR ~3.65%; debt/EBITDA ~3.2x.

| Metric | 2025 |

|---|---|

| New home Tx | −1% YoY |

| Prices | +0.5% |

| Urbanization | 64% |

| Urban consumption | +5% |

| Coal spot | +$110/ton (+22%) |

| Energy cost impact | +12% y/y |

| Capex automation | RMB 420m (+18%) |

| Debt/EBITDA | 3.2x |

Preview Before You Purchase

BBMG PESTLE Analysis

The preview shown here is the exact BBMG PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.