BBTV Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

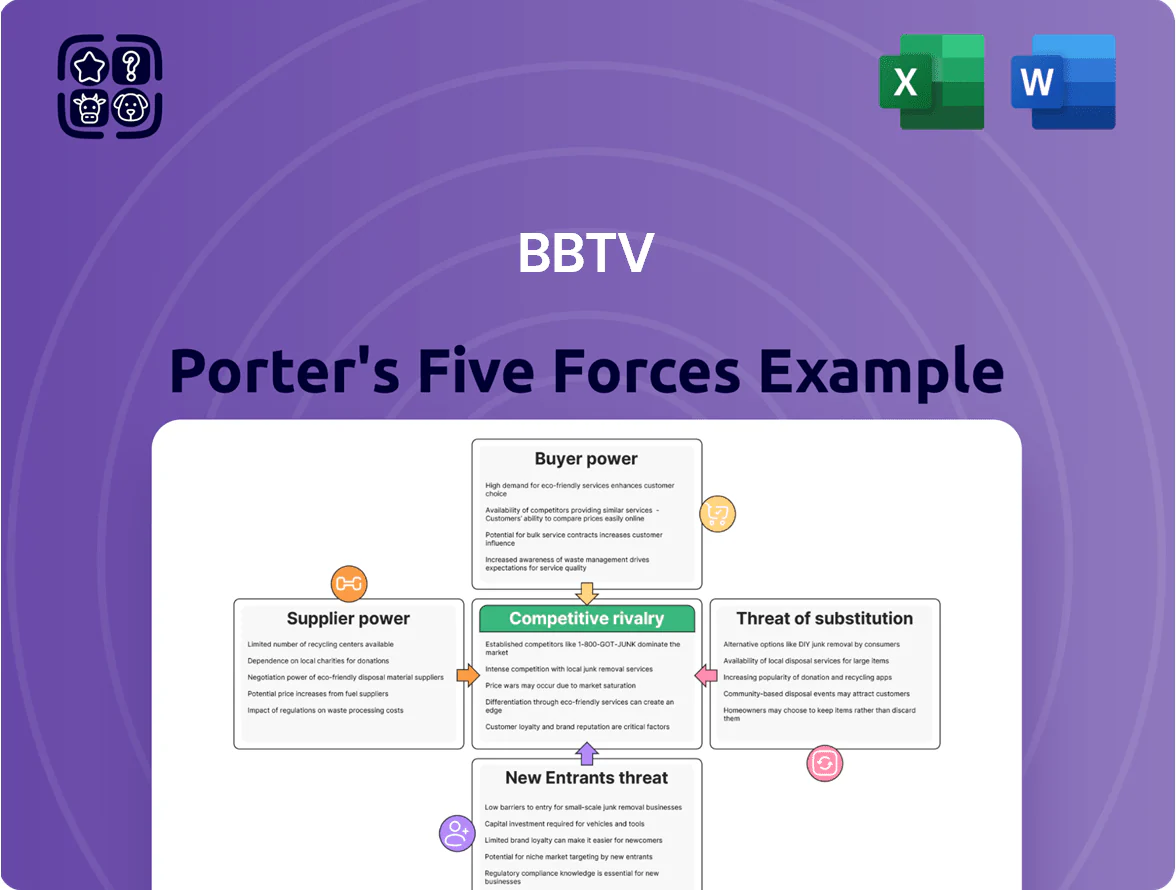

BBTV faces a dynamic mix of platform bargaining power, moderate supplier influence, rising threat from niche creators, and substitution risk from alternative monetization models—this snapshot highlights key pressure points but skips the granular ratings and data behind each force.

This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable implications tailored to BBTV for investment or strategy use.

Suppliers Bargaining Power

Concentration of High-Value Content Creators

Top-tier creators with massive global followings command strong leverage over BBTV, negotiating revenue-share splits well above platform averages; in 2025 marquee talent secured deals paying 40–60% of net ad revenue versus typical creator rates of 20–35%.

These creators have multiple management options—MCNs, talent agencies, direct brand deals—and can switch platforms, raising churn risk and pushing BBTV to offer advance guarantees or CPA bonuses.

As of late 2025, premium brand-safe talent remains scarce: the top 1% of channels capture roughly 35% of viewer hours, concentrating bargaining power and keeping supplier-side terms tilted in creators’ favor.

Platform Dependency and Policy Control

Major platforms like YouTube (Alphabet) and Meta supply the infrastructure and audience BBTV needs; YouTube accounted for over 70% of global long-form creator ad revenue in 2024, so BBTV is highly dependent. These platforms control monetization rules, algorithm updates, and API access—changes there can cut BBTV’s revenue streams quickly. A single policy shift can force BBTV to rework its business model with little notice and limited legal recourse.

Availability of Sophisticated Creator Tools

By 2025 the indie creator tools market reached scale: 72% of mid-sized creators use platforms like LumaFusion, DistroKid, and Amper for rights and distribution, cutting reliance on BBTV’s services. This tech democratization lowers suppliers’ bargaining power, as many can self-manage monetization and licensing. BBTV must therefore keep innovating—investing in exclusive analytics and monetization features—to stop a DIY shift and protect revenue per creator.

Supplier Integration Trends

- 12 major studios reclaimed digital rights in 2024

- 15–20% contraction in addressable creator inventory

- Downward pressure on CPMs and licensing revenue

- Persistent threat to BBTV’s scale and monetization

Switching Costs for Talent

Technical integration raises some friction for creators, but financial switching costs between multi-channel networks (MCNs) stay low—creator revenue splits typically range 55–70% to creators, so a 5–10% better split or faster pay can prompt moves.

BBTV must deliver measurably higher CPMs and exclusive ad products to secure long contracts; a competitor offering clearer dashboards or 15–30 day payout cycles can win creators when terms end.

Top creators seize leverage: deals, platform risk, and indie tools reshape creator economics

Top creators hold strong leverage—2025 deals often pay 40–60% of net ad revenue vs typical 20–35%, and the top 1% capture ~35% of viewer hours, concentrating bargaining power. BBTV depends on platforms: YouTube drove >70% of long-form creator ad revenue in 2024, so policy/API changes can rapidly cut revenue. Indie tools now reach 72% of mid-sized creators, lowering dependence on MCNs and pressuring BBTV to offer better CPMs, faster payouts, and exclusive analytics.

| Metric | 2024–2025 Value |

|---|---|

| Top creator share of viewer hours | 35% |

| Top creator deal splits | 40–60% net ad rev |

| Typical creator split (MCN) | 55–70% to creator |

| YouTube share of long-form ad rev | >70% |

| Mid-sized creators using indie tools | 72% |

| Studios reclaiming digital rights (2024) | 12 studios; 15–20% inventory |

What is included in the product

Tailored Porter's Five Forces analysis for BBTV that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats to assess pricing leverage and strategic positioning.

A concise, one-sheet BBTV Porter's Five Forces summary that clarifies competitive pressure and strategic levers for rapid decision-making.

Customers Bargaining Power

Advertiser Demand for Granular Data

By end-2025 brands and agencies demand granular targeting and transparent ROI for video; 78% of global ad buyers cite audience precision as a top buying criterion, forcing BBTV to spend more on analytics—management disclosed a 42% increase in data-platform capex in 2024–25 to meet this need. If BBTV cannot deliver exact segments and third-party verification, buyers reallocate budgets to rivals within weeks, raising churn and revenue-at-risk.

Fragmentation of Advertising Budgets

Advertisers now choose among hundreds of channels—retail media networks, TikTok, Instagram Reels, and programmatic platforms—splitting the $520B global digital ad market (2024, IAB) and shrinking BBTV’s addressable slice; this fragmentation raises customer bargaining power as brands shift spend to specialists with higher measured ROI, and BBTV risks churn if its managed-content CPMs and engagement rates lag competitors by even 10–20%.

Direct Brand-to-Creator Partnerships

Large advertisers are increasingly cutting out media intermediaries to sign direct influencer deals—global influencer marketing spend hit about $24.1B in 2024, up 15% YoY—reducing BBTV’s middleman value on high-impact campaigns. This weakens BBTV’s bargaining power as clients favor bespoke creator endorsements with higher engagement rates. BBTV must show its bundled inventory delivers superior combined reach and CPM efficiency versus direct deals; otherwise revenue per campaign will erode.

Price Sensitivity in a Saturated Market

Abundant digital video inventory has driven CPMs down; global programmatic video CPMs fell ~12% in 2024, letting buyers bid down rates and squeezing BBTV’s ad-margin (BBTV reported 2024 gross margin of ~28%).

Advertising buyers use tools to chase lowest-cost impressions, so BBTV must mark inventory as premium—higher viewability, brand safety, or exclusive creator deals—to avoid commoditization.

- 2024 programmatic video CPMs down ~12%

- BBTV 2024 gross margin ~28%

- Premium signals: viewability, brand safety, exclusives

Low Switching Costs for Ad Buyers

Digital ad buys are usually short-term or campaign-based, so customers can pause or move spend with little penalty; in 2024 programmatic ad spend saw 66% of global digital budgets bought flexibly, boosting buyer leverage.

BBTV must constantly re-earn spend through measurable performance; churn risk rises if CPMs or view-through rates drop by even 10% versus TikTok or Amazon benchmarks.

- Short contracts = high buyer leverage

- 2024: ~66% programmatic flexibility

- Competitors (TikTok, Amazon) absorb reallocations fast

- Performance-driven retention required

Ad buyers demand precision: 78% seek granular targeting as CPMs fall and churn rises

Customers hold high bargaining power: 78% of ad buyers demand granular targeting (2025), global digital ad market $520B (2024), influencer spend $24.1B (2024), programmatic video CPMs down ~12% (2024), BBTV gross margin ~28% (2024); short-term buys (66% flexible) raise churn risk if BBTV lags rivals by 10–20% on CPM/engagement.

| Metric | Value |

|---|---|

| Ad market (2024) | $520B |

| Influencer spend (2024) | $24.1B |

| Buyers demand (2025) | 78% |

| Prog. CPM change (2024) | -12% |

| BBTV gross margin (2024) | ~28% |

| Flexible buys (2024) | 66% |

What You See Is What You Get

BBTV Porter's Five Forces Analysis

This preview shows the exact BBTV Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

The document displayed here is the same professionally written file included with your order; once you buy, you’ll have instant access to this complete analysis for download.

You're viewing the final deliverable: a ready-to-use report that requires no setup or customization and is available to you the moment payment is completed.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

BBTV faces a dynamic mix of platform bargaining power, moderate supplier influence, rising threat from niche creators, and substitution risk from alternative monetization models—this snapshot highlights key pressure points but skips the granular ratings and data behind each force.

This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable implications tailored to BBTV for investment or strategy use.

Suppliers Bargaining Power

Concentration of High-Value Content Creators

Top-tier creators with massive global followings command strong leverage over BBTV, negotiating revenue-share splits well above platform averages; in 2025 marquee talent secured deals paying 40–60% of net ad revenue versus typical creator rates of 20–35%.

These creators have multiple management options—MCNs, talent agencies, direct brand deals—and can switch platforms, raising churn risk and pushing BBTV to offer advance guarantees or CPA bonuses.

As of late 2025, premium brand-safe talent remains scarce: the top 1% of channels capture roughly 35% of viewer hours, concentrating bargaining power and keeping supplier-side terms tilted in creators’ favor.

Platform Dependency and Policy Control

Major platforms like YouTube (Alphabet) and Meta supply the infrastructure and audience BBTV needs; YouTube accounted for over 70% of global long-form creator ad revenue in 2024, so BBTV is highly dependent. These platforms control monetization rules, algorithm updates, and API access—changes there can cut BBTV’s revenue streams quickly. A single policy shift can force BBTV to rework its business model with little notice and limited legal recourse.

Availability of Sophisticated Creator Tools

By 2025 the indie creator tools market reached scale: 72% of mid-sized creators use platforms like LumaFusion, DistroKid, and Amper for rights and distribution, cutting reliance on BBTV’s services. This tech democratization lowers suppliers’ bargaining power, as many can self-manage monetization and licensing. BBTV must therefore keep innovating—investing in exclusive analytics and monetization features—to stop a DIY shift and protect revenue per creator.

Supplier Integration Trends

- 12 major studios reclaimed digital rights in 2024

- 15–20% contraction in addressable creator inventory

- Downward pressure on CPMs and licensing revenue

- Persistent threat to BBTV’s scale and monetization

Switching Costs for Talent

Technical integration raises some friction for creators, but financial switching costs between multi-channel networks (MCNs) stay low—creator revenue splits typically range 55–70% to creators, so a 5–10% better split or faster pay can prompt moves.

BBTV must deliver measurably higher CPMs and exclusive ad products to secure long contracts; a competitor offering clearer dashboards or 15–30 day payout cycles can win creators when terms end.

Top creators seize leverage: deals, platform risk, and indie tools reshape creator economics

Top creators hold strong leverage—2025 deals often pay 40–60% of net ad revenue vs typical 20–35%, and the top 1% capture ~35% of viewer hours, concentrating bargaining power. BBTV depends on platforms: YouTube drove >70% of long-form creator ad revenue in 2024, so policy/API changes can rapidly cut revenue. Indie tools now reach 72% of mid-sized creators, lowering dependence on MCNs and pressuring BBTV to offer better CPMs, faster payouts, and exclusive analytics.

| Metric | 2024–2025 Value |

|---|---|

| Top creator share of viewer hours | 35% |

| Top creator deal splits | 40–60% net ad rev |

| Typical creator split (MCN) | 55–70% to creator |

| YouTube share of long-form ad rev | >70% |

| Mid-sized creators using indie tools | 72% |

| Studios reclaiming digital rights (2024) | 12 studios; 15–20% inventory |

What is included in the product

Tailored Porter's Five Forces analysis for BBTV that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats to assess pricing leverage and strategic positioning.

A concise, one-sheet BBTV Porter's Five Forces summary that clarifies competitive pressure and strategic levers for rapid decision-making.

Customers Bargaining Power

Advertiser Demand for Granular Data

By end-2025 brands and agencies demand granular targeting and transparent ROI for video; 78% of global ad buyers cite audience precision as a top buying criterion, forcing BBTV to spend more on analytics—management disclosed a 42% increase in data-platform capex in 2024–25 to meet this need. If BBTV cannot deliver exact segments and third-party verification, buyers reallocate budgets to rivals within weeks, raising churn and revenue-at-risk.

Fragmentation of Advertising Budgets

Advertisers now choose among hundreds of channels—retail media networks, TikTok, Instagram Reels, and programmatic platforms—splitting the $520B global digital ad market (2024, IAB) and shrinking BBTV’s addressable slice; this fragmentation raises customer bargaining power as brands shift spend to specialists with higher measured ROI, and BBTV risks churn if its managed-content CPMs and engagement rates lag competitors by even 10–20%.

Direct Brand-to-Creator Partnerships

Large advertisers are increasingly cutting out media intermediaries to sign direct influencer deals—global influencer marketing spend hit about $24.1B in 2024, up 15% YoY—reducing BBTV’s middleman value on high-impact campaigns. This weakens BBTV’s bargaining power as clients favor bespoke creator endorsements with higher engagement rates. BBTV must show its bundled inventory delivers superior combined reach and CPM efficiency versus direct deals; otherwise revenue per campaign will erode.

Price Sensitivity in a Saturated Market

Abundant digital video inventory has driven CPMs down; global programmatic video CPMs fell ~12% in 2024, letting buyers bid down rates and squeezing BBTV’s ad-margin (BBTV reported 2024 gross margin of ~28%).

Advertising buyers use tools to chase lowest-cost impressions, so BBTV must mark inventory as premium—higher viewability, brand safety, or exclusive creator deals—to avoid commoditization.

- 2024 programmatic video CPMs down ~12%

- BBTV 2024 gross margin ~28%

- Premium signals: viewability, brand safety, exclusives

Low Switching Costs for Ad Buyers

Digital ad buys are usually short-term or campaign-based, so customers can pause or move spend with little penalty; in 2024 programmatic ad spend saw 66% of global digital budgets bought flexibly, boosting buyer leverage.

BBTV must constantly re-earn spend through measurable performance; churn risk rises if CPMs or view-through rates drop by even 10% versus TikTok or Amazon benchmarks.

- Short contracts = high buyer leverage

- 2024: ~66% programmatic flexibility

- Competitors (TikTok, Amazon) absorb reallocations fast

- Performance-driven retention required

Ad buyers demand precision: 78% seek granular targeting as CPMs fall and churn rises

Customers hold high bargaining power: 78% of ad buyers demand granular targeting (2025), global digital ad market $520B (2024), influencer spend $24.1B (2024), programmatic video CPMs down ~12% (2024), BBTV gross margin ~28% (2024); short-term buys (66% flexible) raise churn risk if BBTV lags rivals by 10–20% on CPM/engagement.

| Metric | Value |

|---|---|

| Ad market (2024) | $520B |

| Influencer spend (2024) | $24.1B |

| Buyers demand (2025) | 78% |

| Prog. CPM change (2024) | -12% |

| BBTV gross margin (2024) | ~28% |

| Flexible buys (2024) | 66% |

What You See Is What You Get

BBTV Porter's Five Forces Analysis

This preview shows the exact BBTV Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

The document displayed here is the same professionally written file included with your order; once you buy, you’ll have instant access to this complete analysis for download.

You're viewing the final deliverable: a ready-to-use report that requires no setup or customization and is available to you the moment payment is completed.