Bank Central Asia Porter's Five Forces Analysis

From Overview to Strategy Blueprint

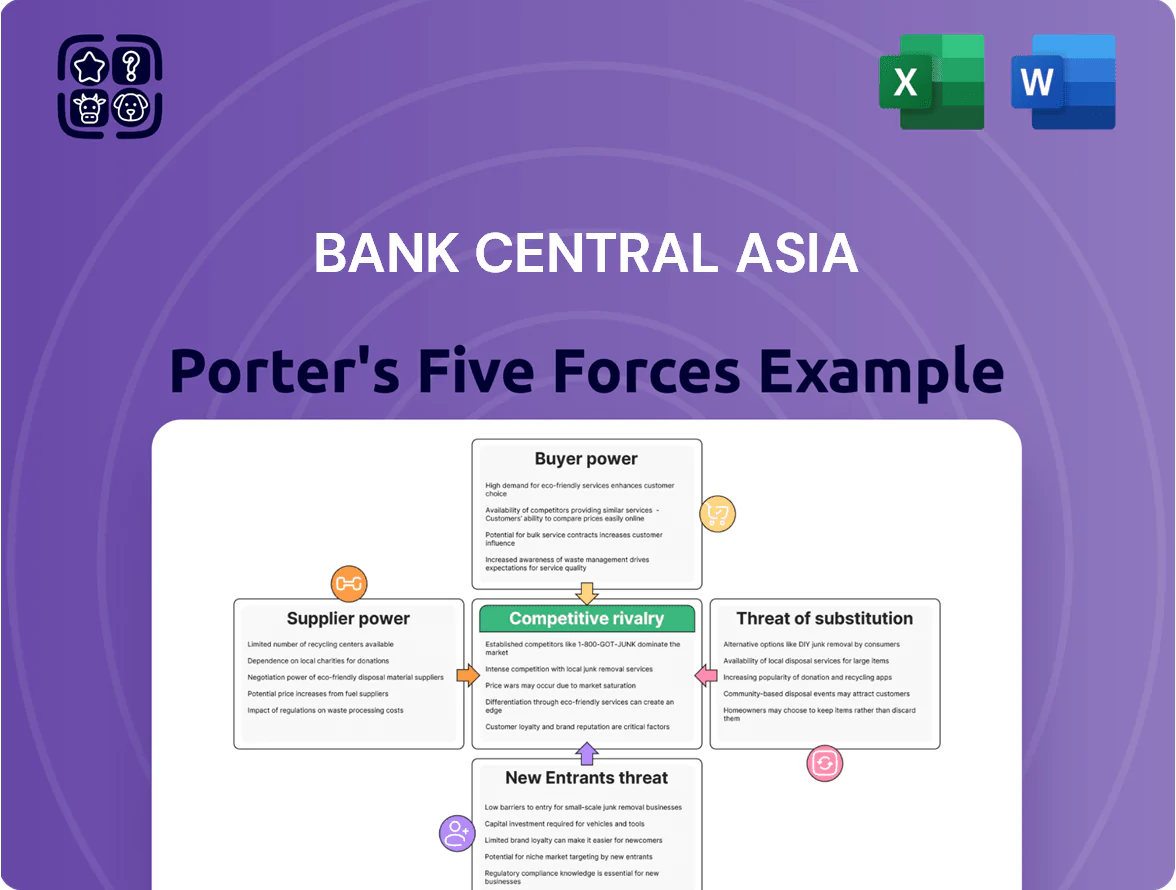

Bank Central Asia faces intense competitive rivalry, moderate buyer power, regulatory-driven supplier constraints, manageable threat of new entrants, and evolving substitute pressures from fintech—this snapshot highlights key pressures shaping margins and growth potential. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy to inform investment or strategic decisions.

Suppliers Bargaining Power

Retail Depositors and Low Cost of Funds

BCA’s massive CASA (current account and savings account) base—about 67% of total deposits at end-2024 and still above 65% by end-2025—remains its primary funding source, keeping funding stable and liquid. Retail depositors, focused on transactional convenience and perceived security, wield low bargaining power and rarely push for higher rates. As a result, BCA sustains a lower cost of funds—net interest margin benefits versus peers—supporting margin resilience through 2025.

Global Technology and Infrastructure Providers

As BCA speeds digital transformation, it depends on global cloud, cybersecurity and core-banking vendors whose specialized services give them moderate bargaining power due to high switching costs; IDC reports 2024 cloud spend in APAC banks rose 18% to $14.2B, raising vendor leverage.

BCA limits this risk by diversifying its tech stack and building proprietary digital platforms—investing roughly IDR 2.3 trillion in IT capex in 2024—cutting external dependency over time.

Human Capital and Specialized Financial Talent

The demand for fintech, data analytics, and risk-management talent in Indonesia grew ~18% in 2024, boosting bargaining power of specialized employees who now attract offers from banks and startups alike.

BCA treats these workers as key suppliers of labor, facing higher retention pressure as industry salary premiums rose ~12% vs 2022.

To secure talent BCA provides top-tier pay, bonuses, and reported IDR 450 billion in 2024 training and upskilling spending to keep a steady internal pipeline.

Central Bank and Regulatory Compliance

Bank Indonesia and OJK act as ultimate suppliers of liquidity and rules, holding absolute bargaining power by setting reserve requirements, capital ratios, and the interest rate corridor that BCA must follow.

As of Dec 2025 targets, BI’s 3.50% policy rate and OJK’s risk-weighted capital minimum (CAR) at 12.5% force BCA to keep liquid assets and CET1 buffers, or risk license and market disruption.

Compliance costs and liquidity impact are material: a 25bp BI hike typically raises BCA’s funding cost by ~5–8bp and can cut NIM by 2–6bps in the following quarter.

- BI policy rate 3.50% (Dec 2025)

- OJK CAR minimum 12.5%

- Reserve ratio changes immediately affect liquidity

- 25bp BI move → funding +5–8bp; NIM -2–6bps

Interbank Market and Institutional Lenders

BCA taps the interbank market and institutional lenders only for short-term liquidity, but these suppliers hold low-to-moderate bargaining power because BCA kept a high liquidity coverage ratio of ~280% and a loan-to-deposit ratio near 74% at end-2024, reducing wholesale funding dependence.

The bank’s AA- local credit rating and access to central bank facilities let it secure funds at favorable spreads when needed, further weakening supplier leverage.

Here’s the quick math: high liquid assets and lower wholesale reliance cut supplier influence and cost pressure.

- Liquidity Coverage Ratio ~280% (2024)

- Loan-to-Deposit Ratio ~74% (2024)

- Local rating AA- (2024)

BCA: Strong CASA & LDR, rising tech/talent costs, regulated by BI/OJK

BCA faces low supplier power from retail depositors thanks to CASA ~66% (end-2025) and LDR ~74% (2024), moderate power from cloud/cyber vendors as APAC bank cloud spend hit $14.2B in 2024, rising tech capex IDR 2.3T (2024) lowers this over time, higher talent power after 18% hiring demand rise (2024) and 12% salary premium, and absolute regulator power with BI policy rate 3.50% and OJK CAR 12.5% (Dec 2025).

| Metric | Value |

|---|---|

| CASA | ~66% (end-2025) |

| LDR | ~74% (2024) |

| IT capex | IDR 2.3T (2024) |

| APAC cloud spend | $14.2B (2024) |

| Hiring demand | +18% (2024) |

| BI policy rate | 3.50% (Dec 2025) |

| OJK CAR min | 12.5% (Dec 2025) |

What is included in the product

Tailored Porter's Five Forces analysis of Bank Central Asia that uncovers competitive intensity, customer and supplier bargaining power, threats from new entrants and substitutes, and strategic barriers that protect its market position.

Concise Porter's Five Forces for Bank Central Asia—one-sheet clarity to assess competitive pressures and guide strategic responses.

Customers Bargaining Power

Corporate and Institutional Borrowers

Large corporate and institutional borrowers hold strong bargaining power with Bank Central Asia (BCA) because top 50 corporates accounted for about 28% of BCA’s corporate loan book in 2024, letting them push for lower loan spreads and preferential cash-management fees.

BCA counters this by bundling treasury, trade finance, and digital cash solutions; its 2024 corporate fee income rose 11% YoY, showing retention via integrated offerings and a reliability premium smaller banks struggle to match.

Retail Banking and Transactional Users

Individual customers have moderate bargaining power since switching basic savings accounts is cheap; Indonesia’s retail churn for banks was ~12% annually in 2024, so price sensitivity matters.

BCA offsets this with 18,000+ ATMs and 20 million active monthly users on the BCA mobile app (Dec 2024), making access and UX a clear retention lever.

By end-2025, BCA’s deep integration—salary disbursements, e-wallet links, and merchant QR adoption—creates soft lock-in, lowering churn vs peers by an estimated 2–3 percentage points.

MSME and Small Business Segment

Micro, Small, and Medium Enterprises (MSMEs) hold low individual bargaining power but face more options as digital lenders and banks target the segment; in Indonesia MSMEs represent 60% of GDP and 97% of firms, so their aggregate pull matters. They demand fast credit and flexible repayments—70% of SME borrowers in 2024 cited speed as top priority—pushing them toward efficient digital platforms. BCA responded by speeding approvals via its Digital Lending Suite, cutting average SME loan approval time to under 48 hours in 2025, so it competes on convenience and turnaround.

High Net Worth Individuals and Wealth Management

Affluent clients wield high bargaining power, accessing global products and private banking; they demand top returns and tailored advice, raising switching risk. BCA counters by expanding wealth-management AUM—BCA Prioritas served clients with Rp 130 trillion+ in 2024—and offering exclusive privileges and dedicated advisors to retain fee income. Higher service quality directly cuts churn and boosts fee margins.

- High bargaining power: global access, private banks

- Sensitivity: returns and advisory quality

- BCA response: BCA Prioritas, Rp 130T+ AUM (2024)

- Impact: lower churn, higher fee income

Digital Savvy Youth and Gen Z

- 70% Gen Z prefer app-first banking (Bank Indonesia, 2024)

- Higher-interest neobanks siphon youth deposits with 0 fees

- BCA updates Blu to match lifestyle needs and promos

Customers split: corporate clout vs app-savvy Gen Z and affluent power — MSMEs matter en masse

Bargaining power of customers is mixed: top 50 corporates drove ~28% of BCA’s corporate loans in 2024, giving them strong price leverage, while retail churn was ~12% (2024) so individual switching matters; affluent clients (BCA Prioritas Rp130T+ AUM, 2024) and Gen Z (70% app-first, Bank Indonesia 2024) exert high power, MSMEs lower individually but large in aggregate (97% firms, 60% GDP).

| Segment | Key metric (2024) |

|---|---|

| Top corporates | 28% corporate loan book |

| Retail churn | ~12% annual |

| BCA Prioritas AUM | Rp130T+ |

| Gen Z | 70% app-first |

| MSMEs | 97% firms, 60% GDP |

Same Document Delivered

Bank Central Asia Porter's Five Forces Analysis

This preview shows the exact Bank Central Asia Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; it's fully formatted, professionally written, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Bank Central Asia faces intense competitive rivalry, moderate buyer power, regulatory-driven supplier constraints, manageable threat of new entrants, and evolving substitute pressures from fintech—this snapshot highlights key pressures shaping margins and growth potential. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy to inform investment or strategic decisions.

Suppliers Bargaining Power

Retail Depositors and Low Cost of Funds

BCA’s massive CASA (current account and savings account) base—about 67% of total deposits at end-2024 and still above 65% by end-2025—remains its primary funding source, keeping funding stable and liquid. Retail depositors, focused on transactional convenience and perceived security, wield low bargaining power and rarely push for higher rates. As a result, BCA sustains a lower cost of funds—net interest margin benefits versus peers—supporting margin resilience through 2025.

Global Technology and Infrastructure Providers

As BCA speeds digital transformation, it depends on global cloud, cybersecurity and core-banking vendors whose specialized services give them moderate bargaining power due to high switching costs; IDC reports 2024 cloud spend in APAC banks rose 18% to $14.2B, raising vendor leverage.

BCA limits this risk by diversifying its tech stack and building proprietary digital platforms—investing roughly IDR 2.3 trillion in IT capex in 2024—cutting external dependency over time.

Human Capital and Specialized Financial Talent

The demand for fintech, data analytics, and risk-management talent in Indonesia grew ~18% in 2024, boosting bargaining power of specialized employees who now attract offers from banks and startups alike.

BCA treats these workers as key suppliers of labor, facing higher retention pressure as industry salary premiums rose ~12% vs 2022.

To secure talent BCA provides top-tier pay, bonuses, and reported IDR 450 billion in 2024 training and upskilling spending to keep a steady internal pipeline.

Central Bank and Regulatory Compliance

Bank Indonesia and OJK act as ultimate suppliers of liquidity and rules, holding absolute bargaining power by setting reserve requirements, capital ratios, and the interest rate corridor that BCA must follow.

As of Dec 2025 targets, BI’s 3.50% policy rate and OJK’s risk-weighted capital minimum (CAR) at 12.5% force BCA to keep liquid assets and CET1 buffers, or risk license and market disruption.

Compliance costs and liquidity impact are material: a 25bp BI hike typically raises BCA’s funding cost by ~5–8bp and can cut NIM by 2–6bps in the following quarter.

- BI policy rate 3.50% (Dec 2025)

- OJK CAR minimum 12.5%

- Reserve ratio changes immediately affect liquidity

- 25bp BI move → funding +5–8bp; NIM -2–6bps

Interbank Market and Institutional Lenders

BCA taps the interbank market and institutional lenders only for short-term liquidity, but these suppliers hold low-to-moderate bargaining power because BCA kept a high liquidity coverage ratio of ~280% and a loan-to-deposit ratio near 74% at end-2024, reducing wholesale funding dependence.

The bank’s AA- local credit rating and access to central bank facilities let it secure funds at favorable spreads when needed, further weakening supplier leverage.

Here’s the quick math: high liquid assets and lower wholesale reliance cut supplier influence and cost pressure.

- Liquidity Coverage Ratio ~280% (2024)

- Loan-to-Deposit Ratio ~74% (2024)

- Local rating AA- (2024)

BCA: Strong CASA & LDR, rising tech/talent costs, regulated by BI/OJK

BCA faces low supplier power from retail depositors thanks to CASA ~66% (end-2025) and LDR ~74% (2024), moderate power from cloud/cyber vendors as APAC bank cloud spend hit $14.2B in 2024, rising tech capex IDR 2.3T (2024) lowers this over time, higher talent power after 18% hiring demand rise (2024) and 12% salary premium, and absolute regulator power with BI policy rate 3.50% and OJK CAR 12.5% (Dec 2025).

| Metric | Value |

|---|---|

| CASA | ~66% (end-2025) |

| LDR | ~74% (2024) |

| IT capex | IDR 2.3T (2024) |

| APAC cloud spend | $14.2B (2024) |

| Hiring demand | +18% (2024) |

| BI policy rate | 3.50% (Dec 2025) |

| OJK CAR min | 12.5% (Dec 2025) |

What is included in the product

Tailored Porter's Five Forces analysis of Bank Central Asia that uncovers competitive intensity, customer and supplier bargaining power, threats from new entrants and substitutes, and strategic barriers that protect its market position.

Concise Porter's Five Forces for Bank Central Asia—one-sheet clarity to assess competitive pressures and guide strategic responses.

Customers Bargaining Power

Corporate and Institutional Borrowers

Large corporate and institutional borrowers hold strong bargaining power with Bank Central Asia (BCA) because top 50 corporates accounted for about 28% of BCA’s corporate loan book in 2024, letting them push for lower loan spreads and preferential cash-management fees.

BCA counters this by bundling treasury, trade finance, and digital cash solutions; its 2024 corporate fee income rose 11% YoY, showing retention via integrated offerings and a reliability premium smaller banks struggle to match.

Retail Banking and Transactional Users

Individual customers have moderate bargaining power since switching basic savings accounts is cheap; Indonesia’s retail churn for banks was ~12% annually in 2024, so price sensitivity matters.

BCA offsets this with 18,000+ ATMs and 20 million active monthly users on the BCA mobile app (Dec 2024), making access and UX a clear retention lever.

By end-2025, BCA’s deep integration—salary disbursements, e-wallet links, and merchant QR adoption—creates soft lock-in, lowering churn vs peers by an estimated 2–3 percentage points.

MSME and Small Business Segment

Micro, Small, and Medium Enterprises (MSMEs) hold low individual bargaining power but face more options as digital lenders and banks target the segment; in Indonesia MSMEs represent 60% of GDP and 97% of firms, so their aggregate pull matters. They demand fast credit and flexible repayments—70% of SME borrowers in 2024 cited speed as top priority—pushing them toward efficient digital platforms. BCA responded by speeding approvals via its Digital Lending Suite, cutting average SME loan approval time to under 48 hours in 2025, so it competes on convenience and turnaround.

High Net Worth Individuals and Wealth Management

Affluent clients wield high bargaining power, accessing global products and private banking; they demand top returns and tailored advice, raising switching risk. BCA counters by expanding wealth-management AUM—BCA Prioritas served clients with Rp 130 trillion+ in 2024—and offering exclusive privileges and dedicated advisors to retain fee income. Higher service quality directly cuts churn and boosts fee margins.

- High bargaining power: global access, private banks

- Sensitivity: returns and advisory quality

- BCA response: BCA Prioritas, Rp 130T+ AUM (2024)

- Impact: lower churn, higher fee income

Digital Savvy Youth and Gen Z

- 70% Gen Z prefer app-first banking (Bank Indonesia, 2024)

- Higher-interest neobanks siphon youth deposits with 0 fees

- BCA updates Blu to match lifestyle needs and promos

Customers split: corporate clout vs app-savvy Gen Z and affluent power — MSMEs matter en masse

Bargaining power of customers is mixed: top 50 corporates drove ~28% of BCA’s corporate loans in 2024, giving them strong price leverage, while retail churn was ~12% (2024) so individual switching matters; affluent clients (BCA Prioritas Rp130T+ AUM, 2024) and Gen Z (70% app-first, Bank Indonesia 2024) exert high power, MSMEs lower individually but large in aggregate (97% firms, 60% GDP).

| Segment | Key metric (2024) |

|---|---|

| Top corporates | 28% corporate loan book |

| Retail churn | ~12% annual |

| BCA Prioritas AUM | Rp130T+ |

| Gen Z | 70% app-first |

| MSMEs | 97% firms, 60% GDP |

Same Document Delivered

Bank Central Asia Porter's Five Forces Analysis

This preview shows the exact Bank Central Asia Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; it's fully formatted, professionally written, and ready for download and use the moment you buy.