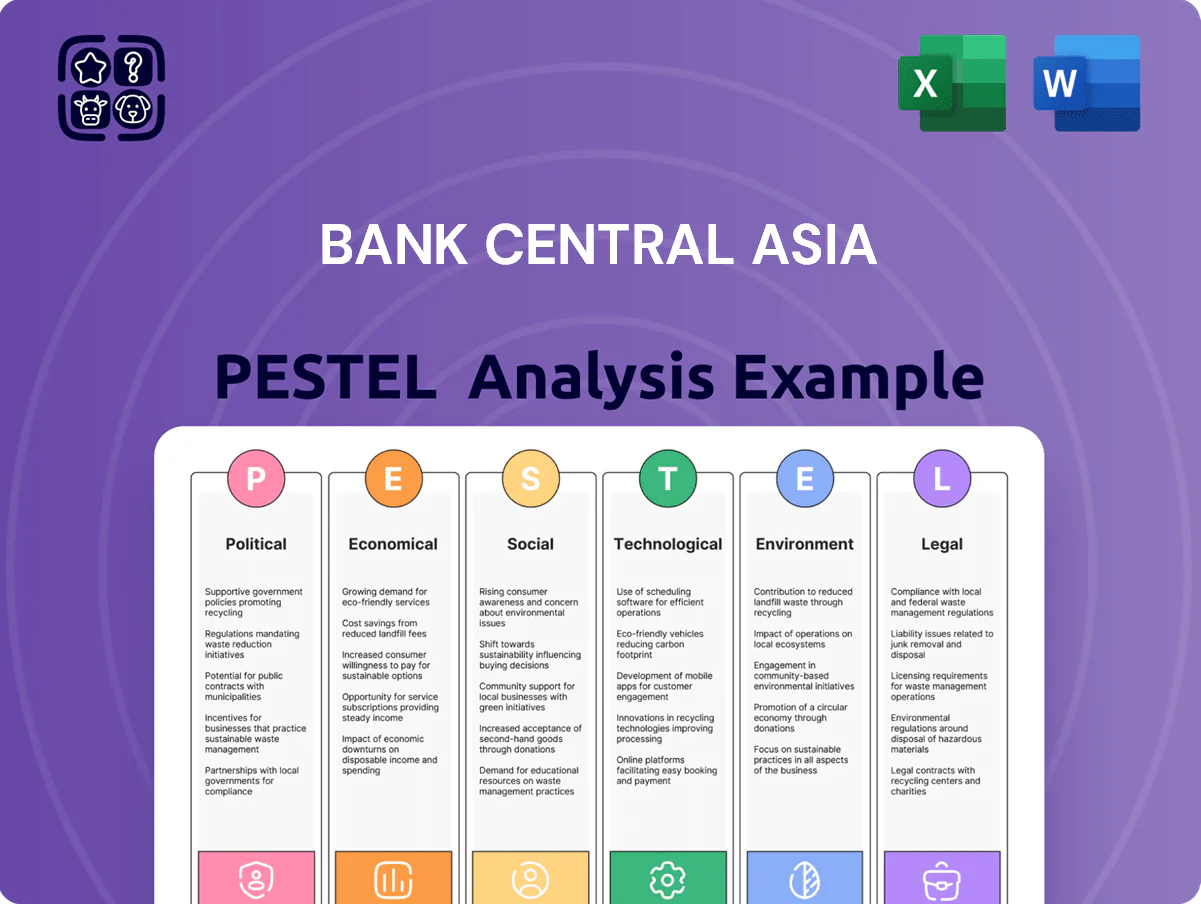

Bank Central Asia PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Bank Central Asia—spot regulatory shifts, economic trends, and tech disruptions shaping its growth, and translate them into actionable moves for investments or strategy. This concise, expert-prepared report saves research time and boosts decision confidence. Purchase the full analysis for the complete, editable breakdown and immediate download.

Political factors

Post-election administrative stability

The transition to the Prabowo-Gibran administration has maintained political stability through 2025, supporting predictable regulatory oversight for banks; Indonesia GDP growth is forecast at 4.8% in 2025, underpinning demand for corporate credit. Continued priority on infrastructure and new economic zones—IDR 600 trillion in planned capital projects for 2024–25—offers BCA steady corporate lending pipelines. BCA uses this continuity to plan multi-year capital allocations with low risk of abrupt policy shifts.

Government focus on downstreaming and industrialization

As of late 2025 the Indonesian government is accelerating downstreaming and industrialization, targeting a 30% increase in domestic mineral processing capacity by 2027; BCA finances supply chains and local firms tied to these projects, with corporate loans to mining and processing sectors rising ~18% YoY in 2024-25. These national priorities generate a steady pipeline for BCA’s corporate and commercial loan book, supporting projected credit growth of 10–12% in industrial lending segments.

Financial sector deepening initiatives

Political efforts to deepen Indonesia’s financial sector—part of OJK and Ministry of Finance programs—offer incentives like subsidized funding and tax breaks to expand credit to underserved regions; in 2024 government targets aimed to raise financial inclusion to 92% from 81% in 2017. BCA aligns branch and digital expansion with these goals to preserve regulator goodwill, aiding faster branch licensing and digital approvals across 34 provinces.

Geopolitical alignment and trade relations

Indonesia's non-aligned, trade-forward stance allows BCA to expand correspondent banking and cross-border payment services across ASEAN and beyond; Indonesia's trade with ASEAN reached US$162.6bn in 2024, aiding transaction volumes for BCA.

The government's push for local currency settlement (LCS) cuts BCA's USD exposure—Indonesia signed LCS deals covering ~25% of ASEAN trade flows by 2024—reducing FX hedging costs.

This political strategy lowers currency-volatility risk for BCA and corporate clients, improving risk-adjusted margins on trade finance and reducing USD funding dependency.

- Reduced USD reliance: ~25% ASEAN trade via LCS (2024)

- Increased cross-border volume: ASEAN trade US$162.6bn (2024)

- Lower FX hedging costs and improved margins for BCA

Digital economy sovereignty policies

The Indonesian government's push for data sovereignty and local infrastructure forces BCA to prioritize onshore data centers and secure cloud investments, aligning with 2024 regulations that mandate local storage for financial data.

Mandates favoring domestic payment rails such as QRIS (over 140 million merchant QRIS transactions monthly in 2024) and BI-FAST (interbank settlement growth >60% YoY in 2024) bolster BCA's transaction volumes and fee income.

By complying with nationalist digital policies, BCA cements its role in national payments, supporting its 2024 market-leading digital customer base of over 30 million users.

- Local data storage mandated for financial institutions

- QRIS: ~140M merchant transactions/month (2024)

- BI-FAST interbank growth >60% YoY (2024)

- BCA digital customers >30M (2024)

Stability to Growth: Prabowo Era Spurs 4.8% GDP, IDR600T Capex and BCA Digital Surge

Political stability under Prabowo-Gibran through 2025 supports predictable banking regulation and 4.8% GDP growth (2025), IDR 600T capex (2024–25) fuels corporate lending; LCS covers ~25% ASEAN trade (2024) lowering USD exposure; data sovereignty mandates local storage and QRIS/BI-FAST growth (140M tx/month; BI-FAST >60% YoY) boost BCA’s digital volumes (30M users, 2024).

| Metric | Value (Year) |

|---|---|

| GDP growth | 4.8% (2025) |

| IDR capex | 600T (2024–25) |

| LCS share ASEAN trade | ~25% (2024) |

| QRIS tx/month | 140M (2024) |

| BI-FAST growth | >60% YoY (2024) |

| BCA digital users | 30M (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Bank Central Asia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary of Bank Central Asia that highlights external risks and regulatory impacts for quick use in presentations or strategy sessions.

Economic factors

Interest rate environment and net interest margin

By end-2025 Bank Indonesia policy rates at 5.75% continue to guide BCA's deposit and loan pricing; BCA leverages a CASA ratio of about 73% (2025 YTD) to keep cost of funds near 1.8% versus peer averages ~3.0%, enabling NIM stability—reported NIM ~5.4% in 2025 despite market rate volatility.

Resilient domestic consumption levels

Strong domestic consumption, contributing about 55% of Indonesia GDP in 2024, directly fuels BCA’s consumer banking; the bank reported a 12% YoY rise in retail loans and double-digit growth in card transaction volume in 2024.

Rising middle-class purchasing power—household consumption up 5.1% in 2024—drives demand for personal loans and credit cards, with BCA’s retail deposits and fee income reflecting this trend.

BCA leverages its transaction dataset from over 22 million CASA customers to tailor retail products, improving cross-sell rates and capturing a larger share of household spending.

Inflationary pressure and operational costs

Management of operational expenses is critical as global supply chain disruptions pushed Indonesia’s CPI to 4.5% in 2024 and forecasts near 3.8–4.2% through 2025, pressuring input costs; BCA counters this by accelerating digital automation—reducing branch transactions and cutting IT-enabled processing costs—supporting a reported efficiency ratio of 44.7% in 2024 versus peers at ~50%. By optimizing efficiency, BCA limits inflation’s drag on net profit margins and ROE preservation.

Small and medium enterprise recovery and growth

The SME sector has rebounded, with Indonesia SMEs contributing about 60% of employment and GDP; BCA views this resilience as central to its credit expansion, noting SME loans grew ~8% YoY in 2024 within the banking sector.

Government SME subsidies and Kredit Usaha Rakyat (KUR) guarantee expansions—KUR disbursements reached IDR 210 trillion in 2024—lower perceived risk, enabling BCA to raise SME exposure while managing provisioning.

These conditions support portfolio diversification: shifting share from large corporates to SMEs reduces concentration risk and aligns with BCA’s targeted SME growth, keeping nonperforming loan ratios stable near industry 2.5%–3.0%.

- SME contribution: ~60% of employment/GDP

- Banking SME loan growth: ~8% YoY (2024)

- KUR disbursements: IDR 210 trillion (2024)

- Industry NPL: ~2.5%–3.0%

Currency stability and foreign exchange revenue

By late 2025 the Rupiah's relative stability—USD/IDR trading around 15,200–15,800—supported BCA's FX fee income, with treasury and FX fees rising an estimated 8% YoY in 2024–25.

Corporate exporters/importers increasingly used BCA hedging products; trade-related FX volumes at BCA grew roughly 6–10% annually, underpinning steady demand for risk-management services.

This demand diversified BCA revenue, with non‑interest income (including treasury) contributing about 30–35% of total operating income in 2024–25.

- USD/IDR ~15,200–15,800 by late 2025

- BCA FX/treasury fee income +~8% YoY (2024–25)

- Trade-related FX volumes +6–10% annually

- Non‑interest income ~30–35% of operating income (2024–25)

BCA: Strong CASA, low funding costs, ~5.4% NIM and solid retail/SME loan growth

BCA benefits from BI rates at 5.75% (end-2025), CASA ~73% (2025 YTD) keeping cost of funds ~1.8% and NIM ~5.4%; retail loans +12% YoY (2024) amid domestic consumption ~55% of GDP; SME loans +8% YoY (2024) with KUR disbursements IDR 210trn; USD/IDR ~15,200–15,800 (late-2025) supporting FX fees, non‑interest income ~30–35%.

| Metric | Value (2024–25) |

|---|---|

| BI policy rate | 5.75% |

| CASA | ~73% |

| Cost of funds | ~1.8% |

| NIM | ~5.4% |

| Retail loan growth | +12% YoY |

| SME loan growth | +8% YoY |

| KUR disbursements | IDR 210 trillion |

| USD/IDR | ~15,200–15,800 |

| Non‑interest income | 30–35% |

Preview the Actual Deliverable

Bank Central Asia PESTLE Analysis

The preview shown here is the exact Bank Central Asia PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The content, layout, and structure visible in this preview are identical to the file you’ll download immediately after payment.

No placeholders or teasers—this is the final, professionally structured report prepared for immediate application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Bank Central Asia—spot regulatory shifts, economic trends, and tech disruptions shaping its growth, and translate them into actionable moves for investments or strategy. This concise, expert-prepared report saves research time and boosts decision confidence. Purchase the full analysis for the complete, editable breakdown and immediate download.

Political factors

Post-election administrative stability

The transition to the Prabowo-Gibran administration has maintained political stability through 2025, supporting predictable regulatory oversight for banks; Indonesia GDP growth is forecast at 4.8% in 2025, underpinning demand for corporate credit. Continued priority on infrastructure and new economic zones—IDR 600 trillion in planned capital projects for 2024–25—offers BCA steady corporate lending pipelines. BCA uses this continuity to plan multi-year capital allocations with low risk of abrupt policy shifts.

Government focus on downstreaming and industrialization

As of late 2025 the Indonesian government is accelerating downstreaming and industrialization, targeting a 30% increase in domestic mineral processing capacity by 2027; BCA finances supply chains and local firms tied to these projects, with corporate loans to mining and processing sectors rising ~18% YoY in 2024-25. These national priorities generate a steady pipeline for BCA’s corporate and commercial loan book, supporting projected credit growth of 10–12% in industrial lending segments.

Financial sector deepening initiatives

Political efforts to deepen Indonesia’s financial sector—part of OJK and Ministry of Finance programs—offer incentives like subsidized funding and tax breaks to expand credit to underserved regions; in 2024 government targets aimed to raise financial inclusion to 92% from 81% in 2017. BCA aligns branch and digital expansion with these goals to preserve regulator goodwill, aiding faster branch licensing and digital approvals across 34 provinces.

Geopolitical alignment and trade relations

Indonesia's non-aligned, trade-forward stance allows BCA to expand correspondent banking and cross-border payment services across ASEAN and beyond; Indonesia's trade with ASEAN reached US$162.6bn in 2024, aiding transaction volumes for BCA.

The government's push for local currency settlement (LCS) cuts BCA's USD exposure—Indonesia signed LCS deals covering ~25% of ASEAN trade flows by 2024—reducing FX hedging costs.

This political strategy lowers currency-volatility risk for BCA and corporate clients, improving risk-adjusted margins on trade finance and reducing USD funding dependency.

- Reduced USD reliance: ~25% ASEAN trade via LCS (2024)

- Increased cross-border volume: ASEAN trade US$162.6bn (2024)

- Lower FX hedging costs and improved margins for BCA

Digital economy sovereignty policies

The Indonesian government's push for data sovereignty and local infrastructure forces BCA to prioritize onshore data centers and secure cloud investments, aligning with 2024 regulations that mandate local storage for financial data.

Mandates favoring domestic payment rails such as QRIS (over 140 million merchant QRIS transactions monthly in 2024) and BI-FAST (interbank settlement growth >60% YoY in 2024) bolster BCA's transaction volumes and fee income.

By complying with nationalist digital policies, BCA cements its role in national payments, supporting its 2024 market-leading digital customer base of over 30 million users.

- Local data storage mandated for financial institutions

- QRIS: ~140M merchant transactions/month (2024)

- BI-FAST interbank growth >60% YoY (2024)

- BCA digital customers >30M (2024)

Stability to Growth: Prabowo Era Spurs 4.8% GDP, IDR600T Capex and BCA Digital Surge

Political stability under Prabowo-Gibran through 2025 supports predictable banking regulation and 4.8% GDP growth (2025), IDR 600T capex (2024–25) fuels corporate lending; LCS covers ~25% ASEAN trade (2024) lowering USD exposure; data sovereignty mandates local storage and QRIS/BI-FAST growth (140M tx/month; BI-FAST >60% YoY) boost BCA’s digital volumes (30M users, 2024).

| Metric | Value (Year) |

|---|---|

| GDP growth | 4.8% (2025) |

| IDR capex | 600T (2024–25) |

| LCS share ASEAN trade | ~25% (2024) |

| QRIS tx/month | 140M (2024) |

| BI-FAST growth | >60% YoY (2024) |

| BCA digital users | 30M (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Bank Central Asia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary of Bank Central Asia that highlights external risks and regulatory impacts for quick use in presentations or strategy sessions.

Economic factors

Interest rate environment and net interest margin

By end-2025 Bank Indonesia policy rates at 5.75% continue to guide BCA's deposit and loan pricing; BCA leverages a CASA ratio of about 73% (2025 YTD) to keep cost of funds near 1.8% versus peer averages ~3.0%, enabling NIM stability—reported NIM ~5.4% in 2025 despite market rate volatility.

Resilient domestic consumption levels

Strong domestic consumption, contributing about 55% of Indonesia GDP in 2024, directly fuels BCA’s consumer banking; the bank reported a 12% YoY rise in retail loans and double-digit growth in card transaction volume in 2024.

Rising middle-class purchasing power—household consumption up 5.1% in 2024—drives demand for personal loans and credit cards, with BCA’s retail deposits and fee income reflecting this trend.

BCA leverages its transaction dataset from over 22 million CASA customers to tailor retail products, improving cross-sell rates and capturing a larger share of household spending.

Inflationary pressure and operational costs

Management of operational expenses is critical as global supply chain disruptions pushed Indonesia’s CPI to 4.5% in 2024 and forecasts near 3.8–4.2% through 2025, pressuring input costs; BCA counters this by accelerating digital automation—reducing branch transactions and cutting IT-enabled processing costs—supporting a reported efficiency ratio of 44.7% in 2024 versus peers at ~50%. By optimizing efficiency, BCA limits inflation’s drag on net profit margins and ROE preservation.

Small and medium enterprise recovery and growth

The SME sector has rebounded, with Indonesia SMEs contributing about 60% of employment and GDP; BCA views this resilience as central to its credit expansion, noting SME loans grew ~8% YoY in 2024 within the banking sector.

Government SME subsidies and Kredit Usaha Rakyat (KUR) guarantee expansions—KUR disbursements reached IDR 210 trillion in 2024—lower perceived risk, enabling BCA to raise SME exposure while managing provisioning.

These conditions support portfolio diversification: shifting share from large corporates to SMEs reduces concentration risk and aligns with BCA’s targeted SME growth, keeping nonperforming loan ratios stable near industry 2.5%–3.0%.

- SME contribution: ~60% of employment/GDP

- Banking SME loan growth: ~8% YoY (2024)

- KUR disbursements: IDR 210 trillion (2024)

- Industry NPL: ~2.5%–3.0%

Currency stability and foreign exchange revenue

By late 2025 the Rupiah's relative stability—USD/IDR trading around 15,200–15,800—supported BCA's FX fee income, with treasury and FX fees rising an estimated 8% YoY in 2024–25.

Corporate exporters/importers increasingly used BCA hedging products; trade-related FX volumes at BCA grew roughly 6–10% annually, underpinning steady demand for risk-management services.

This demand diversified BCA revenue, with non‑interest income (including treasury) contributing about 30–35% of total operating income in 2024–25.

- USD/IDR ~15,200–15,800 by late 2025

- BCA FX/treasury fee income +~8% YoY (2024–25)

- Trade-related FX volumes +6–10% annually

- Non‑interest income ~30–35% of operating income (2024–25)

BCA: Strong CASA, low funding costs, ~5.4% NIM and solid retail/SME loan growth

BCA benefits from BI rates at 5.75% (end-2025), CASA ~73% (2025 YTD) keeping cost of funds ~1.8% and NIM ~5.4%; retail loans +12% YoY (2024) amid domestic consumption ~55% of GDP; SME loans +8% YoY (2024) with KUR disbursements IDR 210trn; USD/IDR ~15,200–15,800 (late-2025) supporting FX fees, non‑interest income ~30–35%.

| Metric | Value (2024–25) |

|---|---|

| BI policy rate | 5.75% |

| CASA | ~73% |

| Cost of funds | ~1.8% |

| NIM | ~5.4% |

| Retail loan growth | +12% YoY |

| SME loan growth | +8% YoY |

| KUR disbursements | IDR 210 trillion |

| USD/IDR | ~15,200–15,800 |

| Non‑interest income | 30–35% |

Preview the Actual Deliverable

Bank Central Asia PESTLE Analysis

The preview shown here is the exact Bank Central Asia PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The content, layout, and structure visible in this preview are identical to the file you’ll download immediately after payment.

No placeholders or teasers—this is the final, professionally structured report prepared for immediate application.