BCG (Boston Consulting Group) Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

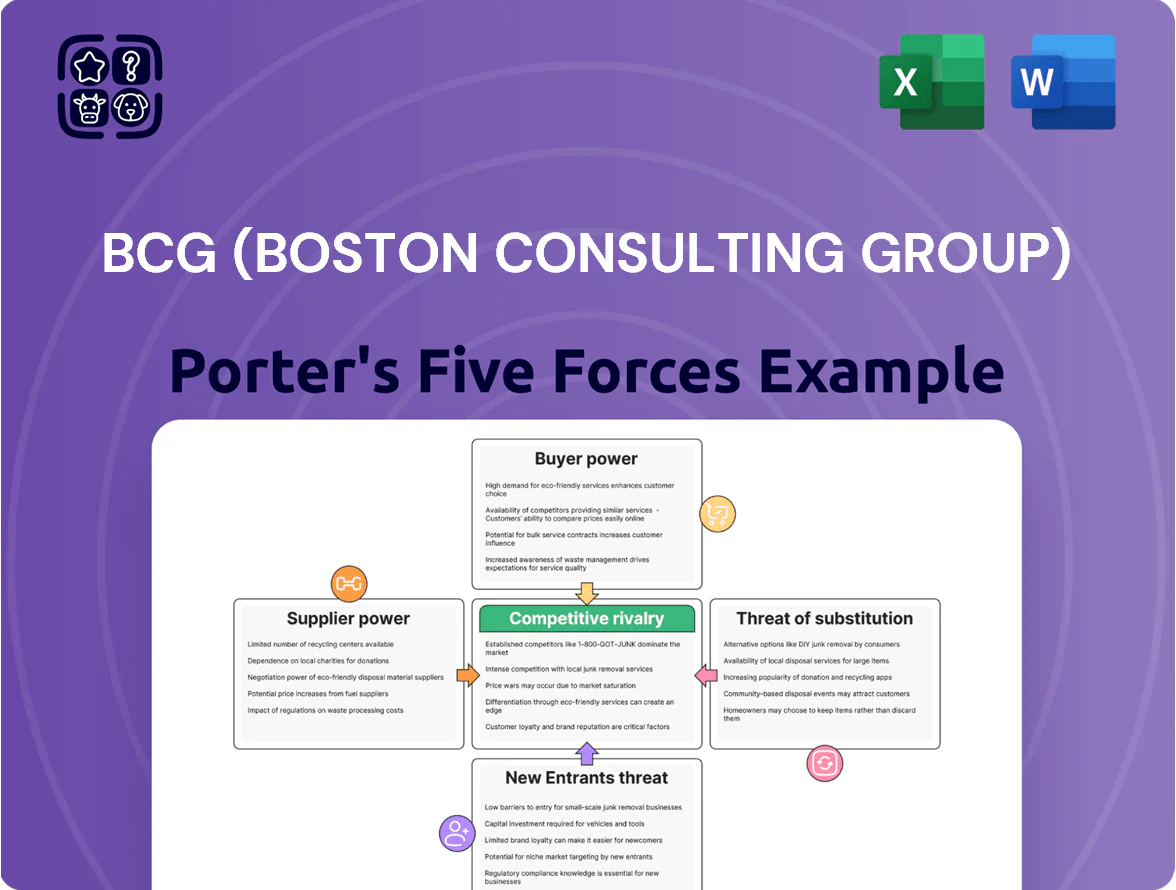

BCG faces intense rivalry from other top consultancies, strong client bargaining power, and moderate threat from new boutique entrants—while supplier power and substitutes remain limited due to specialized expertise and brand strength.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BCG (Boston Consulting Group)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

High-End Talent and Specialized Consultants

The primary suppliers for BCG are highly skilled consultants and graduates from top business schools who supply intellectual capital; they account for about 60–70% of consulting cost structures.

By late 2025, demand for generative AI and sustainability specialists raised salary benchmarks 15–30% in leading markets, boosting supplier leverage.

BCG must match industry-leading pay—partner-track salaries, signing bonuses (often $50k+ for MSc/PhD hires)—and clear career paths to retain talent in a tight labor market.

Advanced AI and Data Infrastructure Providers

As BCG leans on proprietary AI and analytics, suppliers like Microsoft Azure, Google Cloud, and OpenAI hold real leverage; cloud IaaS and PaaS spend for top consultancies can exceed $200M annually, locking customers into provider ecosystems.

These providers supply LLMs and GPU clusters that power BCG’s services; in 2024 NVIDIA GPUs accounted for roughly 80% of datacenter AI deployments, reinforcing supplier dominance.

High integration and migration costs—often tens of millions and 6–18 months—raise switching barriers, keeping supplier bargaining power strong.

Specialized Expert Networks

BCG relies heavily on third-party expert networks that connect consultants to niche specialists; these suppliers control access to real-time, sector-specific intel—about 35–45% of top-tier project briefs in 2024 cited expert-network input, and demand rose ~18% by Q3 2025. That control raises supplier bargaining power because such insights differentiate BCG’s strategy work and are costly to replicate internally.

Academic Institutions and Business Schools

Top-tier universities supply BCG with elite recruits and research prestige; in 2024 roughly 35% of hired consultants at top firms came from the global top 50 universities, so these schools act as a critical talent pipeline.

BCG invests in deep partnerships—funding chairs, co-authored research, campus programs—to secure recruits and access to new management theory, spending millions annually on academic collaborations.

The small pool of elite schools (≈50 globally) creates a bottleneck, giving them indirect leverage over BCG’s long-term human capital strategy and early access to rising talent.

- 35% hires from top-50 universities (2024)

- ≈50 global elite institutions = bottleneck

- Millions invested yearly in research/partnerships

Global Real Estate and Infrastructure Providers

BCG still needs premium offices in hubs like New York, London, Singapore to preserve brand and client access despite hybrid work; in 2024 prime CBD rents rose ~3–6% y/y, keeping occupancy costs high.

Developers in those cities control scarce prestige addresses, giving suppliers leverage over lease terms and fit-out timelines; BCG faces fixed overheads — global office capex and rents often >20% of local operating budgets.

Managing these costs through 2025 is strategic: lease renegotiation, flexible footprints, and co-location in marquee buildings protect elite positioning and client access.

- Prime rent growth 2024: NYC ~4%, London ~3%, Singapore ~3.5%

- Prestige address scarcity raises bargaining power

- Occupancy costs can exceed 20% of local Opex

- Strategies: renegotiate leases, flexible space, co-location

Suppliers Hold the Power: Talent, NVIDIA, Cloud & Elite Universities Dictate Costs

Suppliers (elite consultants, cloud/AI vendors, expert networks, top universities, premium landlords) hold high bargaining power due to scarce talent, dominant cloud/GPU providers, costly niche intel, and prestige real estate; key 2024–25 metrics: 60–70% labor cost share, 15–30% salary inflation for AI/sustainability roles, NVIDIA ~80% datacenter GPU share (2024), cloud spend >$200M, 35% hires from top-50 universities.

| Supplier | Metric | 2024–25 Value |

|---|---|---|

| Labor | Cost share | 60–70% |

| AI/sustainability hires | Salary rise | 15–30% |

| Cloud/GPU vendors | NVIDIA market share | ~80% |

| Cloud spend | Top consultancies | >$200M/yr |

| Elite universities | Share of hires | 35% |

What is included in the product

Comprehensive Porter's Five Forces review of BCG (Boston Consulting Group), highlighting competitive rivalry, client bargaining power, supplier dynamics, threats from new entrants and substitutes, and strategic levers to protect market position.

One-sheet Porter's Five Forces summary tailored by BCG methodology—quickly spot competitive pressures and actionable strategic levers.

Customers Bargaining Power

Concentration of High-Value Corporate Clients

BCG depends on a concentrated base of Fortune 500 and government clients that account for a large share of revenue—top 100 clients often generate 40–60% of firm-level fees—giving buyers strong leverage. These clients negotiate fees and demand tailored, high-impact solutions, pressuring margins and scope. By end-2025, many have procurement teams using ROI and outcomes KPIs, rejecting proposals failing to show >15–20% impact. This raises price sensitivity and increases contract complexity.

Increasing Sophistication of In-House Strategy Teams

Many of BCG’s clients now have sizable in-house strategy teams, often hiring ex-MBB consultants; a 2024 Spencer Stuart survey found 42% of large corporations expanded internal strategy hires since 2020.

These teams handle scoping and initial analysis, cutting demand for routine advisory work and shifting BCG toward high-complexity projects that must justify premium fees.

As a result, BCG faces greater pressure to deliver measurable impact—clients expect ROI metrics and faster time-to-insight for engagements costing $1m+.

Low Switching Costs Between Top-Tier Firms

While deep, multi-month projects create temporary lock-in, long-term switching costs among BCG, McKinsey, and Bain remain low for Fortune 500 clients; Bain, BCG, and McKinsey collectively held about 55% of global top-tier consulting revenue in 2024, so alternatives are close and credible.

Clients can pivot between firms for the next engagement if dissatisfied with outcomes or pricing, and surveys show 27% of large-company C-suite respondents switched primary advisor within three years (2023 data).

This buyer-centric dynamic forces BCG to continuously prove a distinct value proposition—through outcome guarantees, IP, or pricing—to retain accounts where average annual project spend exceeds $5–10 million.

Demand for Tangible ROI and Outcome-Based Pricing

Clients in late 2025 demand outcome-based pricing, with 42% of Fortune 500 companies preferring ROI-tied contracts per a 2025 ALM Research survey, shifting risk to consultants and raising buyer power.

BCG must reprice deals, model downside scenarios, and use performance corridors so partnerships stay profitable while accepting outcome risk.

- 42% Fortune 500 prefer ROI contracts (ALM Research, 2025)

- Outcome pricing shifts ~20–35% project risk to firms (industry avg)

- BCG needs downside buffers and milestone KPIs

Global Transparency and Competitive Bidding

Global digital procurement platforms and standardized consulting benchmarks let buyers compare bids quickly; 2024 sourcing platforms reported a 28% rise in RFP submissions year-over-year, increasing price pressure on consultancies.

Clients now play firms against each other to cut fees or expand scope, forcing BCG to protect margins by selling proprietary tools and IP—BCG reported >$600m revenue from IP-linked offerings in 2023.

Buyers Gain Leverage: ROI Contracts, Rising RFPs & Outcome Pricing Shift Risk

Buyers hold strong leverage: top 100 clients generate ~40–60% fees, 42% prefer ROI-tied contracts (ALM Research, 2025), and 27% switched primary advisor within three years (2023). RFPs rose 28% (2024), pushing price pressure; BCG IP revenue >$600m (2023). Outcome pricing shifts ~20–35% project risk to firms, forcing downside buffers and KPI-linked milestones.

| Metric | Value |

|---|---|

| Top-100 client share | 40–60% |

| ROI-contract preference | 42% (2025) |

| Advisor switching | 27% (2023) |

| RFP growth | +28% (2024) |

| BCG IP revenue | >$600m (2023) |

Preview Before You Purchase

BCG (Boston Consulting Group) Porter's Five Forces Analysis

This preview shows the exact BCG-Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders, no samples. It’s the final, professionally formatted document, ready for immediate download and use. The report combines BCG insights with Porter’s framework to assess competitive rivalry, buyer and supplier power, threats of entry and substitution, and strategic implications. What you see is precisely what you’ll get after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

BCG faces intense rivalry from other top consultancies, strong client bargaining power, and moderate threat from new boutique entrants—while supplier power and substitutes remain limited due to specialized expertise and brand strength.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BCG (Boston Consulting Group)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

High-End Talent and Specialized Consultants

The primary suppliers for BCG are highly skilled consultants and graduates from top business schools who supply intellectual capital; they account for about 60–70% of consulting cost structures.

By late 2025, demand for generative AI and sustainability specialists raised salary benchmarks 15–30% in leading markets, boosting supplier leverage.

BCG must match industry-leading pay—partner-track salaries, signing bonuses (often $50k+ for MSc/PhD hires)—and clear career paths to retain talent in a tight labor market.

Advanced AI and Data Infrastructure Providers

As BCG leans on proprietary AI and analytics, suppliers like Microsoft Azure, Google Cloud, and OpenAI hold real leverage; cloud IaaS and PaaS spend for top consultancies can exceed $200M annually, locking customers into provider ecosystems.

These providers supply LLMs and GPU clusters that power BCG’s services; in 2024 NVIDIA GPUs accounted for roughly 80% of datacenter AI deployments, reinforcing supplier dominance.

High integration and migration costs—often tens of millions and 6–18 months—raise switching barriers, keeping supplier bargaining power strong.

Specialized Expert Networks

BCG relies heavily on third-party expert networks that connect consultants to niche specialists; these suppliers control access to real-time, sector-specific intel—about 35–45% of top-tier project briefs in 2024 cited expert-network input, and demand rose ~18% by Q3 2025. That control raises supplier bargaining power because such insights differentiate BCG’s strategy work and are costly to replicate internally.

Academic Institutions and Business Schools

Top-tier universities supply BCG with elite recruits and research prestige; in 2024 roughly 35% of hired consultants at top firms came from the global top 50 universities, so these schools act as a critical talent pipeline.

BCG invests in deep partnerships—funding chairs, co-authored research, campus programs—to secure recruits and access to new management theory, spending millions annually on academic collaborations.

The small pool of elite schools (≈50 globally) creates a bottleneck, giving them indirect leverage over BCG’s long-term human capital strategy and early access to rising talent.

- 35% hires from top-50 universities (2024)

- ≈50 global elite institutions = bottleneck

- Millions invested yearly in research/partnerships

Global Real Estate and Infrastructure Providers

BCG still needs premium offices in hubs like New York, London, Singapore to preserve brand and client access despite hybrid work; in 2024 prime CBD rents rose ~3–6% y/y, keeping occupancy costs high.

Developers in those cities control scarce prestige addresses, giving suppliers leverage over lease terms and fit-out timelines; BCG faces fixed overheads — global office capex and rents often >20% of local operating budgets.

Managing these costs through 2025 is strategic: lease renegotiation, flexible footprints, and co-location in marquee buildings protect elite positioning and client access.

- Prime rent growth 2024: NYC ~4%, London ~3%, Singapore ~3.5%

- Prestige address scarcity raises bargaining power

- Occupancy costs can exceed 20% of local Opex

- Strategies: renegotiate leases, flexible space, co-location

Suppliers Hold the Power: Talent, NVIDIA, Cloud & Elite Universities Dictate Costs

Suppliers (elite consultants, cloud/AI vendors, expert networks, top universities, premium landlords) hold high bargaining power due to scarce talent, dominant cloud/GPU providers, costly niche intel, and prestige real estate; key 2024–25 metrics: 60–70% labor cost share, 15–30% salary inflation for AI/sustainability roles, NVIDIA ~80% datacenter GPU share (2024), cloud spend >$200M, 35% hires from top-50 universities.

| Supplier | Metric | 2024–25 Value |

|---|---|---|

| Labor | Cost share | 60–70% |

| AI/sustainability hires | Salary rise | 15–30% |

| Cloud/GPU vendors | NVIDIA market share | ~80% |

| Cloud spend | Top consultancies | >$200M/yr |

| Elite universities | Share of hires | 35% |

What is included in the product

Comprehensive Porter's Five Forces review of BCG (Boston Consulting Group), highlighting competitive rivalry, client bargaining power, supplier dynamics, threats from new entrants and substitutes, and strategic levers to protect market position.

One-sheet Porter's Five Forces summary tailored by BCG methodology—quickly spot competitive pressures and actionable strategic levers.

Customers Bargaining Power

Concentration of High-Value Corporate Clients

BCG depends on a concentrated base of Fortune 500 and government clients that account for a large share of revenue—top 100 clients often generate 40–60% of firm-level fees—giving buyers strong leverage. These clients negotiate fees and demand tailored, high-impact solutions, pressuring margins and scope. By end-2025, many have procurement teams using ROI and outcomes KPIs, rejecting proposals failing to show >15–20% impact. This raises price sensitivity and increases contract complexity.

Increasing Sophistication of In-House Strategy Teams

Many of BCG’s clients now have sizable in-house strategy teams, often hiring ex-MBB consultants; a 2024 Spencer Stuart survey found 42% of large corporations expanded internal strategy hires since 2020.

These teams handle scoping and initial analysis, cutting demand for routine advisory work and shifting BCG toward high-complexity projects that must justify premium fees.

As a result, BCG faces greater pressure to deliver measurable impact—clients expect ROI metrics and faster time-to-insight for engagements costing $1m+.

Low Switching Costs Between Top-Tier Firms

While deep, multi-month projects create temporary lock-in, long-term switching costs among BCG, McKinsey, and Bain remain low for Fortune 500 clients; Bain, BCG, and McKinsey collectively held about 55% of global top-tier consulting revenue in 2024, so alternatives are close and credible.

Clients can pivot between firms for the next engagement if dissatisfied with outcomes or pricing, and surveys show 27% of large-company C-suite respondents switched primary advisor within three years (2023 data).

This buyer-centric dynamic forces BCG to continuously prove a distinct value proposition—through outcome guarantees, IP, or pricing—to retain accounts where average annual project spend exceeds $5–10 million.

Demand for Tangible ROI and Outcome-Based Pricing

Clients in late 2025 demand outcome-based pricing, with 42% of Fortune 500 companies preferring ROI-tied contracts per a 2025 ALM Research survey, shifting risk to consultants and raising buyer power.

BCG must reprice deals, model downside scenarios, and use performance corridors so partnerships stay profitable while accepting outcome risk.

- 42% Fortune 500 prefer ROI contracts (ALM Research, 2025)

- Outcome pricing shifts ~20–35% project risk to firms (industry avg)

- BCG needs downside buffers and milestone KPIs

Global Transparency and Competitive Bidding

Global digital procurement platforms and standardized consulting benchmarks let buyers compare bids quickly; 2024 sourcing platforms reported a 28% rise in RFP submissions year-over-year, increasing price pressure on consultancies.

Clients now play firms against each other to cut fees or expand scope, forcing BCG to protect margins by selling proprietary tools and IP—BCG reported >$600m revenue from IP-linked offerings in 2023.

Buyers Gain Leverage: ROI Contracts, Rising RFPs & Outcome Pricing Shift Risk

Buyers hold strong leverage: top 100 clients generate ~40–60% fees, 42% prefer ROI-tied contracts (ALM Research, 2025), and 27% switched primary advisor within three years (2023). RFPs rose 28% (2024), pushing price pressure; BCG IP revenue >$600m (2023). Outcome pricing shifts ~20–35% project risk to firms, forcing downside buffers and KPI-linked milestones.

| Metric | Value |

|---|---|

| Top-100 client share | 40–60% |

| ROI-contract preference | 42% (2025) |

| Advisor switching | 27% (2023) |

| RFP growth | +28% (2024) |

| BCG IP revenue | >$600m (2023) |

Preview Before You Purchase

BCG (Boston Consulting Group) Porter's Five Forces Analysis

This preview shows the exact BCG-Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders, no samples. It’s the final, professionally formatted document, ready for immediate download and use. The report combines BCG insights with Porter’s framework to assess competitive rivalry, buyer and supplier power, threats of entry and substitution, and strategic implications. What you see is precisely what you’ll get after payment.