Banque Cantonale Vaudoise PESTLE Analysis

Your Competitive Advantage Starts with This Report

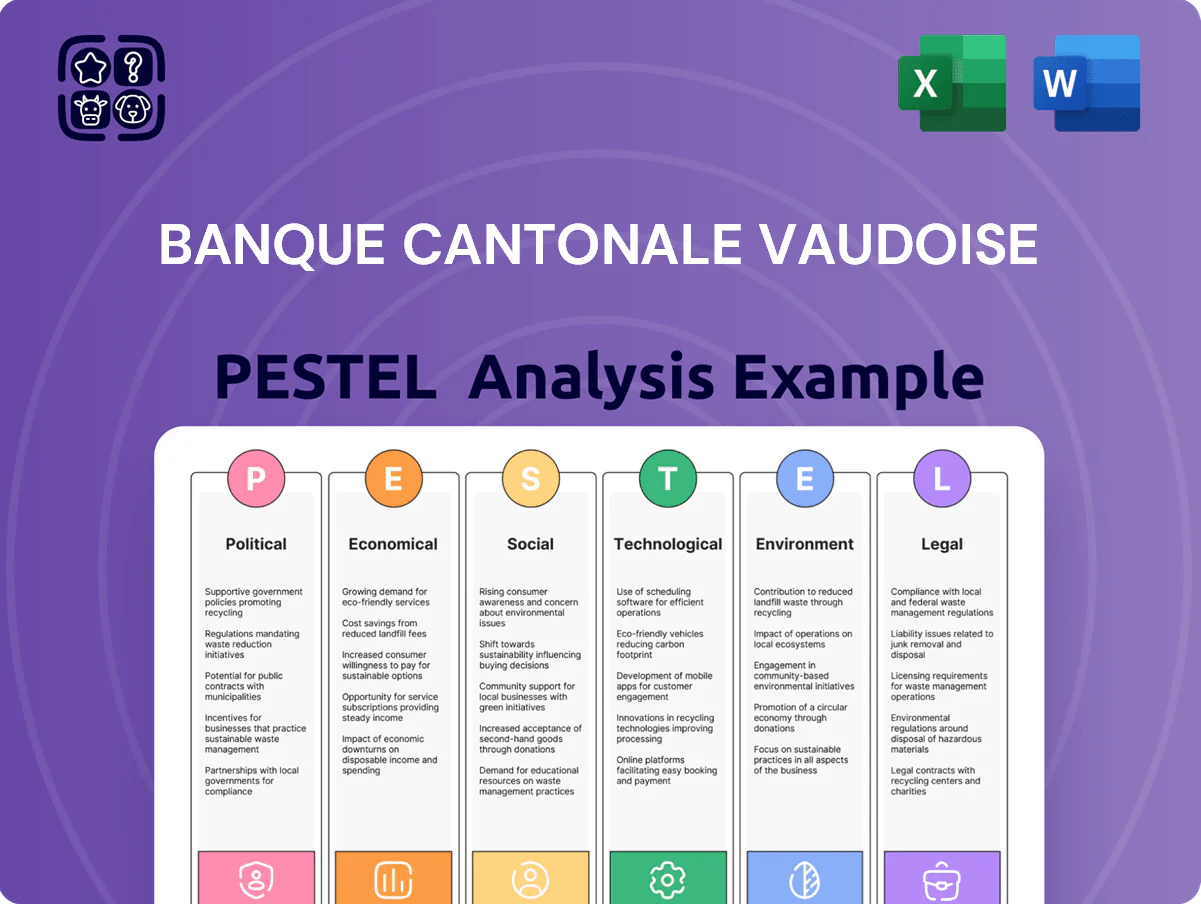

Gain a strategic advantage with our concise PESTLE Analysis of Banque Cantonale Vaudoise—highlighting political, economic, social, technological, legal, and environmental drivers that will shape its outlook; this ready-to-use brief points to risks and opportunities you can act on immediately. Purchase the full report to access detailed, sourced insights and editable charts for investment memos, strategy decks, or boardroom decisions.

Political factors

Cantonal Ownership and Governance

The Canton of Vaud holds about 67% of Banque Cantonale Vaudoise as of late 2025, providing political stability and aligning BCV’s strategy with regional economic development; BCV reported CHF 3.8bn in total equity and CHF 54bn in total assets in 2024, reinforcing its role as a regional pillar.

Majority ownership attracts political scrutiny over dividend policy and public-policy support, with canton expectations influencing capital allocation—BCV paid CHF 120m in dividends in 2024, highlighting tension between shareholder returns and public mandates.

Swiss-EU Bilateral Relations

Ongoing Switzerland-EU negotiations over the third bilateral package, unresolved since 2021, materially affect cross-border finance: about 25% of Swiss bank assets relate to EU clients, so outcome alters BCV’s market access and potential revenue exposure. For BCV, limits on passporting could raise compliance costs; freer access could support growth in its ~CHF 52bn balance sheet (2024). Labor mobility constraints risk reducing access to EU talent for BCV’s specialized teams.

International Tax Transparency Standards

Switzerland’s commitment to automatic exchange of information (AEOI) and OECD-led tax cooperation—96 jurisdictions participating in AEOI as of 2025—forces BCV to align reporting and due-diligence processes to avoid sanctions and reputational risk. BCV must adapt KYC/AML systems and cross-border reporting for over CHF 50bn in client assets under management to meet evolving Common Reporting Standard requirements. Ongoing regulatory updates require continuous investment in compliance technology and staff training to preserve Swiss banking confidentiality strengths while ensuring full transparency.

Federal Financial Stability Regulations

Federal moves after recent domestic failures have tightened too-big-to-fail rules; BCV, though cantonal, is treated as systemically important for Vaud and must maintain CET1 ratios above Swiss average—BCV reported CET1 13.2% in 2024 versus Swiss system ~12.5%—reflecting federal pressure for higher buffers.

Political debates in Bern drive changes to liquidity and recovery planning; SNB and FINMA expectations have increased stress-test frequency and NSFR-like liquidity monitoring, influencing BCV's risk frameworks and capital planning.

- BCV CET1 13.2% (2024)

- Swiss avg CET1 ~12.5% (2024)

- Increased stress tests and stricter liquidity oversight

Geopolitical Safe Haven Status

Switzerland’s neutral stance amid 2024–2025 geopolitical tensions reinforced its safe-haven status, boosting cross-border asset inflows; Swiss banks saw CHF deposits rise 3.8% y/y in 2024, supporting BCV’s mandate as a cantonal custodian.

BCV benefits from investor flight-to-safety toward state-backed institutions; cantonal guarantees and Switzerland’s fiscal strength (general government debt ~40% of GDP in 2024) underpin its positioning.

- Neutrality maintained capital inflows; Swiss financial reserves ~CHF 870bn (2024)

- Cantonal guarantee enhances depositor confidence for BCV

- Geopolitical fragmentation increases demand for Swiss asset management

BCV: Cantonal Control, Solid CET1, CHF120m Dividends Spur Oversight

Cantonal majority (67% Vaud) ensures political support but draws scrutiny on dividends (CHF 120m in 2024) and public mandates; BCV CET1 13.2% vs Swiss avg ~12.5% (2024). Switzerland’s neutrality and AEOI/tax cooperation increase inflows and compliance costs; SNB/FINMA tighter liquidity and stress tests raise capital and operational requirements.

| Metric | Value |

|---|---|

| Cantonal stake | 67% |

| Dividends (2024) | CHF 120m |

| CET1 (BCV) | 13.2% |

| Swiss avg CET1 | ~12.5% |

| Swiss deposits change (2024) | +3.8% y/y |

What is included in the product

Explores how macro-environmental factors uniquely affect Banque Cantonale Vaudoise across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities.

Condensed PESTLE insights tailored to Banque Cantonale Vaudoise, enabling swift reference in meetings and presentations to pinpoint external risks and strategic opportunities.

Economic factors

Interest Rate Environment and SNB Policy

The Swiss National Bank's policy remains the key driver of BCV's net interest income; SNB sight deposit rate was 1.75% at end-2025 after cuts from 1.90% in mid-2024, forcing BCV to manage deposit-mortgage spreads tightly.

As Swiss mortgage rates averaged ~2.1% in 2025 versus typical retail deposit yields ~0.4%, margin compression and repricing lags affected BCV's retail and corporate lending profitability within Vaud canton.

Vaud Regional Economic Health

BCV’s performance is closely tied to Canton Vaud’s GDP growth; Vaud grew ~2.1% in 2023 and the Lemanic arc accounts for ~30% of cantonal GDP, driven by life sciences and tech clusters around Lausanne and EPFL.

The regional economy’s diversification and low unemployment—4.0% in Vaud as of Q4 2024 versus 4.8% national—supports stable commercial lending and lower credit defaults for BCV.

Business investment in the region rose ~5% YoY in 2023, making local capex and R&D spending key inputs in BCV’s loan growth and credit provisioning models.

Mortgage Market Stability

The Lake Geneva real estate market shows sustained demand and tight supply, underpinning BCV’s CHF 34.2 billion mortgage book (2024), but rising construction costs—up ~7% year-on-year in 2023—and shifting cantonal housing policies could pressure valuations and new lending volumes.

Currency Volatility and the Swiss Franc

The Swiss franc's 2024 average trade-weighted index rose ~3.5% year-on-year versus major peers, strengthening AUM valuation in CHF while compressing euro- and dollar-denominated returns for BCV clients.

Exporters in Vaud face margin pressure as CHF appreciated ~5% vs EUR and ~4% vs USD in 2023–24, increasing demand for BCV trade finance and FX risk solutions.

BCV offsets exposure via layered hedging, forwards and options and expanded FX services; in 2024 FX-related revenues represented an estimated mid-single-digit percent of fee income.

- CHF appreciation: +5% vs EUR (2023–24)

- Trade-weighted index: +3.5% (2024 avg)

- FX revenues: mid-single-digit % of fees (2024 est.)

Inflationary Trends and Operational Costs

Switzerland's inflation averaged about 1.3% in 2024 versus eurozone 2.4%, but BCV faces rising wage costs (banking sector salaries up ~3% in 2024) and higher IT spending—Swiss banks increased tech capex ~8% y/y; this squeezes the bank's cost-income ratio.

BCV prioritizes efficiency—2026 forecasts emphasize digital automation and branch optimization to offset persistent inflationary pressure on operating budgets.

- Switzerland inflation 2024: ~1.3%

- Banking wages growth 2024: ~3%

- IT capex increase: ~8% y/y

- 2026 focus: efficiency gains, automation, branch optimization

SNB 1.75% lifts mortgage spreads, NII squeezed as CHF strength and costs bite

SNB rate 1.75% end-2025 drove tight deposit-mortgage spreads; Swiss mortgage avg ~2.1% vs deposit yield ~0.4% in 2025, pressuring NII. Vaud GDP supportive (2.1% in 2023) with unemployment 4.0% Q4 2024, backing loan quality; mortgage book CHF 34.2bn (2024) faces higher construction costs +7% (2023). CHF appreciated ~5% vs EUR (2023–24); inflation 1.3% (2024), banking wages +3%, IT capex +8% y/y.

| Metric | Value |

|---|---|

| SNB rate | 1.75% (end-2025) |

| Mortgage avg | ~2.1% (2025) |

| Deposit yield | ~0.4% (2025) |

| Vaud GDP | 2.1% (2023) |

| Unemployment Vaud | 4.0% Q4 2024 |

| BCV mortgage book | CHF 34.2bn (2024) |

| CHF vs EUR | +5% (2023–24) |

| Inflation Switzerland | 1.3% (2024) |

| Bank wages | +3% (2024) |

| IT capex | +8% y/y (2024) |

Preview Before You Purchase

Banque Cantonale Vaudoise PESTLE Analysis

The preview shown here is the exact Banque Cantonale Vaudoise PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our concise PESTLE Analysis of Banque Cantonale Vaudoise—highlighting political, economic, social, technological, legal, and environmental drivers that will shape its outlook; this ready-to-use brief points to risks and opportunities you can act on immediately. Purchase the full report to access detailed, sourced insights and editable charts for investment memos, strategy decks, or boardroom decisions.

Political factors

Cantonal Ownership and Governance

The Canton of Vaud holds about 67% of Banque Cantonale Vaudoise as of late 2025, providing political stability and aligning BCV’s strategy with regional economic development; BCV reported CHF 3.8bn in total equity and CHF 54bn in total assets in 2024, reinforcing its role as a regional pillar.

Majority ownership attracts political scrutiny over dividend policy and public-policy support, with canton expectations influencing capital allocation—BCV paid CHF 120m in dividends in 2024, highlighting tension between shareholder returns and public mandates.

Swiss-EU Bilateral Relations

Ongoing Switzerland-EU negotiations over the third bilateral package, unresolved since 2021, materially affect cross-border finance: about 25% of Swiss bank assets relate to EU clients, so outcome alters BCV’s market access and potential revenue exposure. For BCV, limits on passporting could raise compliance costs; freer access could support growth in its ~CHF 52bn balance sheet (2024). Labor mobility constraints risk reducing access to EU talent for BCV’s specialized teams.

International Tax Transparency Standards

Switzerland’s commitment to automatic exchange of information (AEOI) and OECD-led tax cooperation—96 jurisdictions participating in AEOI as of 2025—forces BCV to align reporting and due-diligence processes to avoid sanctions and reputational risk. BCV must adapt KYC/AML systems and cross-border reporting for over CHF 50bn in client assets under management to meet evolving Common Reporting Standard requirements. Ongoing regulatory updates require continuous investment in compliance technology and staff training to preserve Swiss banking confidentiality strengths while ensuring full transparency.

Federal Financial Stability Regulations

Federal moves after recent domestic failures have tightened too-big-to-fail rules; BCV, though cantonal, is treated as systemically important for Vaud and must maintain CET1 ratios above Swiss average—BCV reported CET1 13.2% in 2024 versus Swiss system ~12.5%—reflecting federal pressure for higher buffers.

Political debates in Bern drive changes to liquidity and recovery planning; SNB and FINMA expectations have increased stress-test frequency and NSFR-like liquidity monitoring, influencing BCV's risk frameworks and capital planning.

- BCV CET1 13.2% (2024)

- Swiss avg CET1 ~12.5% (2024)

- Increased stress tests and stricter liquidity oversight

Geopolitical Safe Haven Status

Switzerland’s neutral stance amid 2024–2025 geopolitical tensions reinforced its safe-haven status, boosting cross-border asset inflows; Swiss banks saw CHF deposits rise 3.8% y/y in 2024, supporting BCV’s mandate as a cantonal custodian.

BCV benefits from investor flight-to-safety toward state-backed institutions; cantonal guarantees and Switzerland’s fiscal strength (general government debt ~40% of GDP in 2024) underpin its positioning.

- Neutrality maintained capital inflows; Swiss financial reserves ~CHF 870bn (2024)

- Cantonal guarantee enhances depositor confidence for BCV

- Geopolitical fragmentation increases demand for Swiss asset management

BCV: Cantonal Control, Solid CET1, CHF120m Dividends Spur Oversight

Cantonal majority (67% Vaud) ensures political support but draws scrutiny on dividends (CHF 120m in 2024) and public mandates; BCV CET1 13.2% vs Swiss avg ~12.5% (2024). Switzerland’s neutrality and AEOI/tax cooperation increase inflows and compliance costs; SNB/FINMA tighter liquidity and stress tests raise capital and operational requirements.

| Metric | Value |

|---|---|

| Cantonal stake | 67% |

| Dividends (2024) | CHF 120m |

| CET1 (BCV) | 13.2% |

| Swiss avg CET1 | ~12.5% |

| Swiss deposits change (2024) | +3.8% y/y |

What is included in the product

Explores how macro-environmental factors uniquely affect Banque Cantonale Vaudoise across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities.

Condensed PESTLE insights tailored to Banque Cantonale Vaudoise, enabling swift reference in meetings and presentations to pinpoint external risks and strategic opportunities.

Economic factors

Interest Rate Environment and SNB Policy

The Swiss National Bank's policy remains the key driver of BCV's net interest income; SNB sight deposit rate was 1.75% at end-2025 after cuts from 1.90% in mid-2024, forcing BCV to manage deposit-mortgage spreads tightly.

As Swiss mortgage rates averaged ~2.1% in 2025 versus typical retail deposit yields ~0.4%, margin compression and repricing lags affected BCV's retail and corporate lending profitability within Vaud canton.

Vaud Regional Economic Health

BCV’s performance is closely tied to Canton Vaud’s GDP growth; Vaud grew ~2.1% in 2023 and the Lemanic arc accounts for ~30% of cantonal GDP, driven by life sciences and tech clusters around Lausanne and EPFL.

The regional economy’s diversification and low unemployment—4.0% in Vaud as of Q4 2024 versus 4.8% national—supports stable commercial lending and lower credit defaults for BCV.

Business investment in the region rose ~5% YoY in 2023, making local capex and R&D spending key inputs in BCV’s loan growth and credit provisioning models.

Mortgage Market Stability

The Lake Geneva real estate market shows sustained demand and tight supply, underpinning BCV’s CHF 34.2 billion mortgage book (2024), but rising construction costs—up ~7% year-on-year in 2023—and shifting cantonal housing policies could pressure valuations and new lending volumes.

Currency Volatility and the Swiss Franc

The Swiss franc's 2024 average trade-weighted index rose ~3.5% year-on-year versus major peers, strengthening AUM valuation in CHF while compressing euro- and dollar-denominated returns for BCV clients.

Exporters in Vaud face margin pressure as CHF appreciated ~5% vs EUR and ~4% vs USD in 2023–24, increasing demand for BCV trade finance and FX risk solutions.

BCV offsets exposure via layered hedging, forwards and options and expanded FX services; in 2024 FX-related revenues represented an estimated mid-single-digit percent of fee income.

- CHF appreciation: +5% vs EUR (2023–24)

- Trade-weighted index: +3.5% (2024 avg)

- FX revenues: mid-single-digit % of fees (2024 est.)

Inflationary Trends and Operational Costs

Switzerland's inflation averaged about 1.3% in 2024 versus eurozone 2.4%, but BCV faces rising wage costs (banking sector salaries up ~3% in 2024) and higher IT spending—Swiss banks increased tech capex ~8% y/y; this squeezes the bank's cost-income ratio.

BCV prioritizes efficiency—2026 forecasts emphasize digital automation and branch optimization to offset persistent inflationary pressure on operating budgets.

- Switzerland inflation 2024: ~1.3%

- Banking wages growth 2024: ~3%

- IT capex increase: ~8% y/y

- 2026 focus: efficiency gains, automation, branch optimization

SNB 1.75% lifts mortgage spreads, NII squeezed as CHF strength and costs bite

SNB rate 1.75% end-2025 drove tight deposit-mortgage spreads; Swiss mortgage avg ~2.1% vs deposit yield ~0.4% in 2025, pressuring NII. Vaud GDP supportive (2.1% in 2023) with unemployment 4.0% Q4 2024, backing loan quality; mortgage book CHF 34.2bn (2024) faces higher construction costs +7% (2023). CHF appreciated ~5% vs EUR (2023–24); inflation 1.3% (2024), banking wages +3%, IT capex +8% y/y.

| Metric | Value |

|---|---|

| SNB rate | 1.75% (end-2025) |

| Mortgage avg | ~2.1% (2025) |

| Deposit yield | ~0.4% (2025) |

| Vaud GDP | 2.1% (2023) |

| Unemployment Vaud | 4.0% Q4 2024 |

| BCV mortgage book | CHF 34.2bn (2024) |

| CHF vs EUR | +5% (2023–24) |

| Inflation Switzerland | 1.3% (2024) |

| Bank wages | +3% (2024) |

| IT capex | +8% y/y (2024) |

Preview Before You Purchase

Banque Cantonale Vaudoise PESTLE Analysis

The preview shown here is the exact Banque Cantonale Vaudoise PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.