Becton Dickinson Boston Consulting Group Matrix

Download Your Competitive Advantage

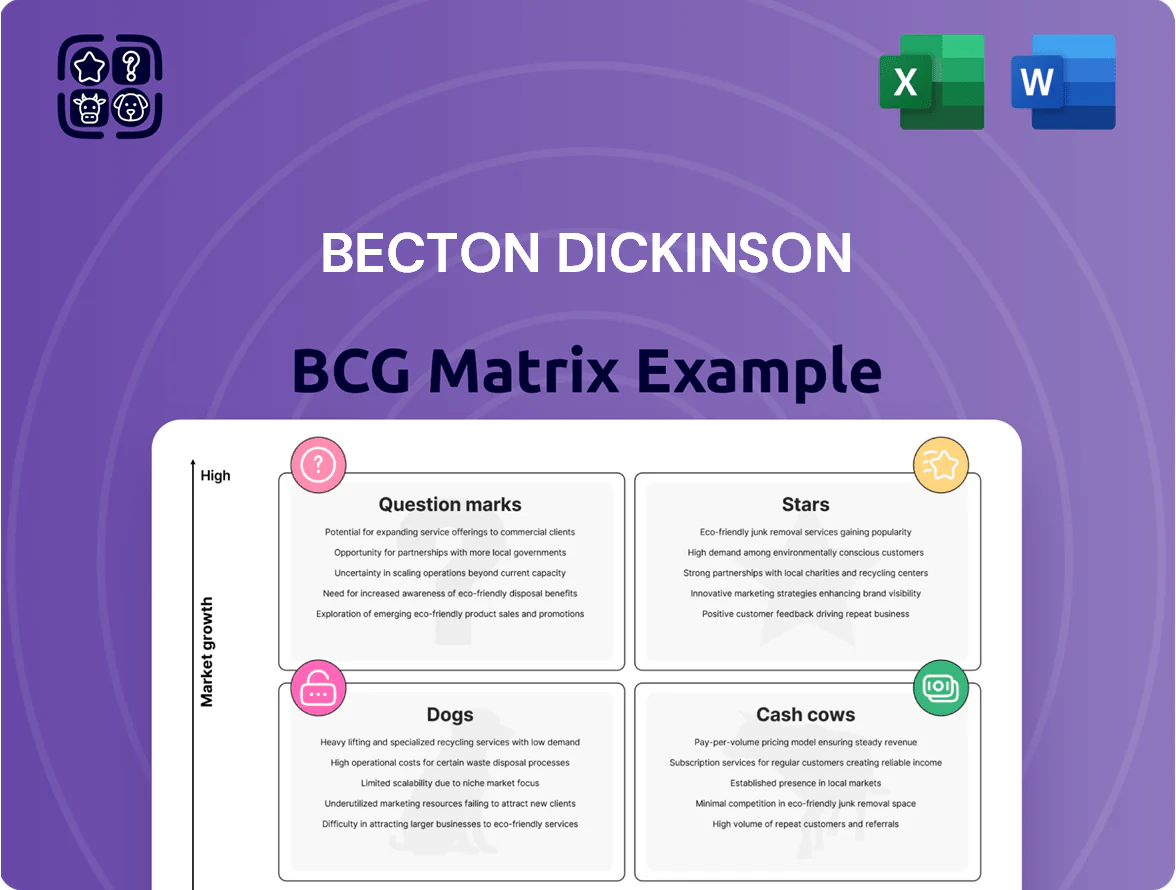

Becton Dickinson’s BCG Matrix snapshot highlights where its core medical-device franchises likely sit amid shifting healthcare demand—identifying potential Stars in high-growth segments, Cash Cows in stable legacy lines, and products that may need reinvestment or divestment. This preview teases quadrant-level positioning and strategic implications but the full BCG Matrix delivers comprehensive placements, data-driven recommendations, and actionable capital-allocation guidance. Purchase the complete report to receive an editable Word analysis plus an Excel summary for immediate use and confident decision-making.

Stars

Connected Medication Management Systems

BDs Alaris infusion pumps and Pyxis automated dispensing cabinets lead hospital medication-safety automation, holding an estimated combined market share ~28% in acute-care infusion and ADCs in 2024, driven by digital workflow adoption and a 7–9% CAGR in connected medication management software through 2023–25.

Hospitals prioritizing error reduction and pharmacy labor optimization drive SaaS growth for BD, with subscription revenue rising ~15% YoY in 2024 and capex and service contracts funding continuous cybersecurity and EHR interoperability upgrades.

Molecular Diagnostics and BD COR System

BD has moved diagnostic leadership into high-growth molecular testing with BD COR and BD MAX; BD reported molecular diagnostics revenue of about $1.6 billion in FY2024, up ~12% year-over-year, driven by high-throughput infectious disease and women’s health panels.

These systems meet growing post-pandemic demand—global molecular diagnostics market grew ~9% in 2024 to $12.5 billion—and BD captures a top-three share in clinical labs, though expanding test menus needs continued R&D investment (~10% of diagnostics revenue).

Single-Cell Multiomics and Flow Cytometry

The BD Biosciences segment leads high-end research tools—BD Horizon RealBlue and RealYellow reagents plus advanced cell sorters—driving roughly 12–15% annual growth in single-cell multiomics and flow cytometry sales (2024 est.), with consumables recurring revenue ~55% of segment revenue.

Personalized medicine and immunology research fuel demand; market for single-cell tools hit ~$4.2B in 2024 and BD holds an estimated 25–30% share, keeping a dominant position but requiring ~USD 400–500M annual R&D and capex to stay ahead of genomic-tech shifts.

GLP-1 Drug Delivery Solutions

BDs pre-fillable syringe unit sits in Stars: rapid GLP-1 demand (obesity/diabetes) has driven >40% CAGR in device volumes since 2022, making BD a primary supplier to top pharma partners and capturing an estimated 50%+ share of injector supply by 2025.

Keeping supply parity needs heavy capex: BD announced a $1.2B capacity expansion plan in 2024 to meet projected demand of ~1.5 billion GLP-1 doses/year by 2030, or risk supply bottlenecks and lost revenue.

- High growth: device volumes +40% CAGR since 2022

- Market share: ~50%+ injector supply by 2025

- Capex: $1.2B expansion announced 2024

- Demand: ~1.5B GLP-1 doses/year projected by 2030

Advanced Peripheral Intervention Devices

Advanced Peripheral Intervention Devices: BD’s interventional unit grew revenue ~6% in 2024, driven by Venovo venous stent and PowerPICC sales, targeting venous disease and oncology in an aging population needing minimally invasive care.

BD keeps leadership via ongoing clinical trials (50+ studies globally by 2025) and iterative product updates to defend a high share vs. smaller challengers.

- 2024 revenue growth ~6%

- 50+ clinical studies by 2025

- Key products: Venovo stent, PowerPICC

- Market: aging population, minimally invasive vascular procedures

BD growth surge: dominant pre-fill syringes & Alaris/Pyxis SaaS fueling rapid expansion

BD Stars: pre-fillable syringes (50%+ injector share by 2025; >40% device CAGR since 2022; $1.2B capex 2024) and Alaris/Pyxis infusion/ADC (~28% acute-care market share 2024; 7–9% connected SaaS CAGR 2023–25; subscription rev +15% YoY 2024).

| Business | 2024 metric | 2025 outlook |

|---|---|---|

| Pre-fillable syringes | 50%+ share; $1.2B capex | meet ~1.5B doses/yr by 2030 |

| Alaris/Pyxis | ~28% share; SaaS +15% YoY | 7–9% SaaS CAGR |

What is included in the product

Comprehensive BCG Matrix review of Becton Dickinson’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG Matrix placing Becton Dickinson units in quadrants for quick strategic decisions and investor briefings.

Cash Cows

BD Vacutainer Blood Collection Systems

BD Vacutainer blood collection systems are the global gold standard, with BD (Becton Dickinson and Company, NYSE: BDX) holding an estimated >50% global market share in tube-based phlebotomy as of 2025 and serving hospitals and labs in 190+ countries.

The market is mature, growing ~2–3% annually; Vacutainer products generate high free cash flow—BD reported medical segment operating margin ~18% in FY2024—while requiring low promotional spend.

Those stable profits fund BD’s higher-growth bets in molecular diagnostics and digital health, where BD targets double-digit CAGR investments and M&A to boost recurring revenue and innovation.

Standard Hypodermic Needles and Syringes

As one of the world’s largest makers of standard hypodermic needles and syringes, Becton Dickinson (BD) captures unmatched economies of scale in a low-growth, high-volume market; global disposable syringe demand was ~20 billion units in 2024.

Unit margins are lower than for specialty devices, but volume yields stable revenue—BD reported $2.8 billion in syringe/needle segment sales in FY2024—providing predictable cash flow.

R&D needs are minimal, so BD can allocate free cash to service ~ $4.5 billion net debt (2024) and sustain a dividend (2024 payout ratio ~25%), making this a classic cash cow.

Peripheral IV Catheters

BD’s Medication Delivery Solutions unit holds roughly 30–35% share of the global peripheral IV catheter market (2024 estimate), making these staples in nearly all acute-care settings; annual catheter revenues are estimated at ~$900M within BD Medical (FY2024 pro forma).

The product is mature with low obsolescence, high gross margins (~45%–55%) from long-term hospital contracts and brand trust, so it acts as a reliable cash cow.

Cash flow from peripheral IVs finances BD Medical’s push into complex, digitally enabled infusion systems and sensors, supporting R&D and M&A—BD reported $1.8B in Medical segment operating cash flow in FY2024.

Infection Prevention and ChloraPrep

ChloraPrep holds a leading share (>40% in US perioperative skin antiseptics as of 2024) in a low-growth surgical site infection (SSI) prevention market, driven by regulation like CMS and Joint Commission standards that keep demand stable.

The line generates steady cash for Becton Dickinson (BD), with disposable margins supported by scale; 2024 BD Surgical Solutions revenue ~USD 3.2bn implies predictable contribution without need for heavy marketing spend.

Focus on incremental packaging and applicator improvements—easier single-dose delivery, reduced waste—maintains margins and extends lifecycle in a mature category.

- Market share >40% (US, 2024)

- SSI market growth <3% CAGR

- BD Surgical Solutions rev ~USD 3.2bn (2024)

- Strategy: small-capex packaging, delivery tweaks

Hernia Repair and Surgical Mesh

BD Interventional leads the mature hernia repair mesh market, with BD holding an estimated mid-20s market share in U.S. surgical mesh and fixation devices as of 2025; the category grows roughly 3–4% annually, so it generates predictable margins and cash flow.

Strong surgeon relationships and hospital contracting lock in repeat sales, funding R&D into bio-resorbable materials and next-gen soft tissue repair technologies; surgical-mesh revenue contributed an estimated several hundred million dollars to BD’s 2024 device sales.

- Leading position; mid-20s % U.S. share (2025)

- Market growth ~3–4% CAGR

- Reliable margins, steady cash flow (hundreds of $M, 2024)

- Funds bio-resorbable and next-gen soft-tissue R&D

BD’s cash cows: dominant disposables, steady cash flow funding growth bets

BD’s Vacutainer, syringes/needles, peripheral IVs, ChloraPrep and hernia mesh are cash cows: >50% global Vacutainer share (2025), ~20B syringes demand (2024), syringe sales $2.8B (FY2024), IV catheter share 30–35% with ~$900M revenue (FY2024), ChloraPrep >40% US (2024), Surgical Solutions ~$3.2B (2024); low growth (~2–4% CAGR), high free cash flow funds BD’s growth bets.

| Product | Share/Size (year) | Revenue/Volume (year) | Growth |

|---|---|---|---|

| Vacutainer | >50% (2025) | Global | 2–3% CAGR |

| Syringes/Needles | — | $2.8B sales; ~20B units (2024) | Low |

| Peripheral IV | 30–35% (2024) | ~$900M (2024) | 3–4% CAGR |

| ChloraPrep | >40% US (2024) | Within Surgical ~$3.2B (2024) | <3% CAGR |

| Hernia Mesh | Mid-20s % US (2025) | Hundreds $M (2024) | 3–4% CAGR |

Full Transparency, Always

Becton Dickinson BCG Matrix

The file you're previewing on this page is the final Becton Dickinson BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready report designed for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Becton Dickinson’s BCG Matrix snapshot highlights where its core medical-device franchises likely sit amid shifting healthcare demand—identifying potential Stars in high-growth segments, Cash Cows in stable legacy lines, and products that may need reinvestment or divestment. This preview teases quadrant-level positioning and strategic implications but the full BCG Matrix delivers comprehensive placements, data-driven recommendations, and actionable capital-allocation guidance. Purchase the complete report to receive an editable Word analysis plus an Excel summary for immediate use and confident decision-making.

Stars

Connected Medication Management Systems

BDs Alaris infusion pumps and Pyxis automated dispensing cabinets lead hospital medication-safety automation, holding an estimated combined market share ~28% in acute-care infusion and ADCs in 2024, driven by digital workflow adoption and a 7–9% CAGR in connected medication management software through 2023–25.

Hospitals prioritizing error reduction and pharmacy labor optimization drive SaaS growth for BD, with subscription revenue rising ~15% YoY in 2024 and capex and service contracts funding continuous cybersecurity and EHR interoperability upgrades.

Molecular Diagnostics and BD COR System

BD has moved diagnostic leadership into high-growth molecular testing with BD COR and BD MAX; BD reported molecular diagnostics revenue of about $1.6 billion in FY2024, up ~12% year-over-year, driven by high-throughput infectious disease and women’s health panels.

These systems meet growing post-pandemic demand—global molecular diagnostics market grew ~9% in 2024 to $12.5 billion—and BD captures a top-three share in clinical labs, though expanding test menus needs continued R&D investment (~10% of diagnostics revenue).

Single-Cell Multiomics and Flow Cytometry

The BD Biosciences segment leads high-end research tools—BD Horizon RealBlue and RealYellow reagents plus advanced cell sorters—driving roughly 12–15% annual growth in single-cell multiomics and flow cytometry sales (2024 est.), with consumables recurring revenue ~55% of segment revenue.

Personalized medicine and immunology research fuel demand; market for single-cell tools hit ~$4.2B in 2024 and BD holds an estimated 25–30% share, keeping a dominant position but requiring ~USD 400–500M annual R&D and capex to stay ahead of genomic-tech shifts.

GLP-1 Drug Delivery Solutions

BDs pre-fillable syringe unit sits in Stars: rapid GLP-1 demand (obesity/diabetes) has driven >40% CAGR in device volumes since 2022, making BD a primary supplier to top pharma partners and capturing an estimated 50%+ share of injector supply by 2025.

Keeping supply parity needs heavy capex: BD announced a $1.2B capacity expansion plan in 2024 to meet projected demand of ~1.5 billion GLP-1 doses/year by 2030, or risk supply bottlenecks and lost revenue.

- High growth: device volumes +40% CAGR since 2022

- Market share: ~50%+ injector supply by 2025

- Capex: $1.2B expansion announced 2024

- Demand: ~1.5B GLP-1 doses/year projected by 2030

Advanced Peripheral Intervention Devices

Advanced Peripheral Intervention Devices: BD’s interventional unit grew revenue ~6% in 2024, driven by Venovo venous stent and PowerPICC sales, targeting venous disease and oncology in an aging population needing minimally invasive care.

BD keeps leadership via ongoing clinical trials (50+ studies globally by 2025) and iterative product updates to defend a high share vs. smaller challengers.

- 2024 revenue growth ~6%

- 50+ clinical studies by 2025

- Key products: Venovo stent, PowerPICC

- Market: aging population, minimally invasive vascular procedures

BD growth surge: dominant pre-fill syringes & Alaris/Pyxis SaaS fueling rapid expansion

BD Stars: pre-fillable syringes (50%+ injector share by 2025; >40% device CAGR since 2022; $1.2B capex 2024) and Alaris/Pyxis infusion/ADC (~28% acute-care market share 2024; 7–9% connected SaaS CAGR 2023–25; subscription rev +15% YoY 2024).

| Business | 2024 metric | 2025 outlook |

|---|---|---|

| Pre-fillable syringes | 50%+ share; $1.2B capex | meet ~1.5B doses/yr by 2030 |

| Alaris/Pyxis | ~28% share; SaaS +15% YoY | 7–9% SaaS CAGR |

What is included in the product

Comprehensive BCG Matrix review of Becton Dickinson’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG Matrix placing Becton Dickinson units in quadrants for quick strategic decisions and investor briefings.

Cash Cows

BD Vacutainer Blood Collection Systems

BD Vacutainer blood collection systems are the global gold standard, with BD (Becton Dickinson and Company, NYSE: BDX) holding an estimated >50% global market share in tube-based phlebotomy as of 2025 and serving hospitals and labs in 190+ countries.

The market is mature, growing ~2–3% annually; Vacutainer products generate high free cash flow—BD reported medical segment operating margin ~18% in FY2024—while requiring low promotional spend.

Those stable profits fund BD’s higher-growth bets in molecular diagnostics and digital health, where BD targets double-digit CAGR investments and M&A to boost recurring revenue and innovation.

Standard Hypodermic Needles and Syringes

As one of the world’s largest makers of standard hypodermic needles and syringes, Becton Dickinson (BD) captures unmatched economies of scale in a low-growth, high-volume market; global disposable syringe demand was ~20 billion units in 2024.

Unit margins are lower than for specialty devices, but volume yields stable revenue—BD reported $2.8 billion in syringe/needle segment sales in FY2024—providing predictable cash flow.

R&D needs are minimal, so BD can allocate free cash to service ~ $4.5 billion net debt (2024) and sustain a dividend (2024 payout ratio ~25%), making this a classic cash cow.

Peripheral IV Catheters

BD’s Medication Delivery Solutions unit holds roughly 30–35% share of the global peripheral IV catheter market (2024 estimate), making these staples in nearly all acute-care settings; annual catheter revenues are estimated at ~$900M within BD Medical (FY2024 pro forma).

The product is mature with low obsolescence, high gross margins (~45%–55%) from long-term hospital contracts and brand trust, so it acts as a reliable cash cow.

Cash flow from peripheral IVs finances BD Medical’s push into complex, digitally enabled infusion systems and sensors, supporting R&D and M&A—BD reported $1.8B in Medical segment operating cash flow in FY2024.

Infection Prevention and ChloraPrep

ChloraPrep holds a leading share (>40% in US perioperative skin antiseptics as of 2024) in a low-growth surgical site infection (SSI) prevention market, driven by regulation like CMS and Joint Commission standards that keep demand stable.

The line generates steady cash for Becton Dickinson (BD), with disposable margins supported by scale; 2024 BD Surgical Solutions revenue ~USD 3.2bn implies predictable contribution without need for heavy marketing spend.

Focus on incremental packaging and applicator improvements—easier single-dose delivery, reduced waste—maintains margins and extends lifecycle in a mature category.

- Market share >40% (US, 2024)

- SSI market growth <3% CAGR

- BD Surgical Solutions rev ~USD 3.2bn (2024)

- Strategy: small-capex packaging, delivery tweaks

Hernia Repair and Surgical Mesh

BD Interventional leads the mature hernia repair mesh market, with BD holding an estimated mid-20s market share in U.S. surgical mesh and fixation devices as of 2025; the category grows roughly 3–4% annually, so it generates predictable margins and cash flow.

Strong surgeon relationships and hospital contracting lock in repeat sales, funding R&D into bio-resorbable materials and next-gen soft tissue repair technologies; surgical-mesh revenue contributed an estimated several hundred million dollars to BD’s 2024 device sales.

- Leading position; mid-20s % U.S. share (2025)

- Market growth ~3–4% CAGR

- Reliable margins, steady cash flow (hundreds of $M, 2024)

- Funds bio-resorbable and next-gen soft-tissue R&D

BD’s cash cows: dominant disposables, steady cash flow funding growth bets

BD’s Vacutainer, syringes/needles, peripheral IVs, ChloraPrep and hernia mesh are cash cows: >50% global Vacutainer share (2025), ~20B syringes demand (2024), syringe sales $2.8B (FY2024), IV catheter share 30–35% with ~$900M revenue (FY2024), ChloraPrep >40% US (2024), Surgical Solutions ~$3.2B (2024); low growth (~2–4% CAGR), high free cash flow funds BD’s growth bets.

| Product | Share/Size (year) | Revenue/Volume (year) | Growth |

|---|---|---|---|

| Vacutainer | >50% (2025) | Global | 2–3% CAGR |

| Syringes/Needles | — | $2.8B sales; ~20B units (2024) | Low |

| Peripheral IV | 30–35% (2024) | ~$900M (2024) | 3–4% CAGR |

| ChloraPrep | >40% US (2024) | Within Surgical ~$3.2B (2024) | <3% CAGR |

| Hernia Mesh | Mid-20s % US (2025) | Hundreds $M (2024) | 3–4% CAGR |

Full Transparency, Always

Becton Dickinson BCG Matrix

The file you're previewing on this page is the final Becton Dickinson BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready report designed for strategic clarity and professional use.