Becton Dickinson PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, supply-chain dynamics, and rapid medtech innovation are reshaping Becton Dickinson’s strategic horizon—our concise PESTLE snapshot highlights the risks and opportunities driving performance. Purchase the full PESTLE analysis to access evidence-backed insights, scenario impacts, and ready-to-use recommendations for investors, strategists, and advisors.

Political factors

Post-election healthcare policy shifts

Post-election healthcare policy shifts in 2025—driven by major US and EU elections in late 2024—have prompted projected increases in national healthcare budgets: US federal health outlays up 4.2% YoY and EU health spending rising 3.1% in 2025, affecting subsidies for medtech adoption.

BD must recalibrate product pricing and R&D allocation as changes to reimbursement models could alter hospital capital expenditures—US hospital capex forecast +2.5% in 2025—while public health initiatives expand procurement for diagnostics and vaccination supplies.

Aligning with evolving subsidy frameworks and value-based purchasing pilots, BD’s strategy should prioritize devices eligible for government reimbursement to protect revenue streams tied to public contracts that represent over 30% of certain regional sales.

Geopolitical trade tensions and protectionism

Persistent trade frictions—US-China tariffs and 2023 EU import measures—raised global medical-supply costs; BD reported 2024 supply-chain costs up ~2–3% and invested $1.1bn in manufacturing capacity (2023–2024) to localize production. Protectionist mandates in India and Brazil forced BD to expand regional facilities, diversifying suppliers to sustain margins. Navigating these policies is critical to keep market access across Asia and Latin America.

Global pandemic preparedness funding

Governmental focus on biosecurity and pandemic prevention remained high through late 2025, driving sustained public investment—global health security spending rose to an estimated $85 billion in 2024–25, with diagnostics and surveillance accounting for roughly 28% ($23.8B), areas where BD holds a competitive edge in instruments and assays.

International regulatory harmonization efforts

Political cooperation among regulators — including ICH, IMDRF and WHO prequalification initiatives — is streamlining approvals for medical devices and diagnostics, potentially cutting time-to-market by up to 30% in some markets.

Harmonization reduces multiple filings but forces BD to comply with unified, often stricter standards; BD reported regulatory-related R&D spending of about $1.2 billion in 2024 to support global compliance.

BD actively lobbies and consults with policymakers and regulators to shape frameworks that balance patient safety with innovation, engaging in over 25 regulatory working groups and public consultations in 2024.

- Streamlining may reduce approval timelines by ~30%

- BD regulatory R&D spend ~ $1.2B in 2024

- Participation in 25+ regulatory working groups (2024)

Governmental focus on drug pricing and transparency

Political pressure to lower healthcare costs has intensified scrutiny on the medical supply chain, with U.S. policymakers pursuing drug and device price reforms that could affect BD's margins; CMS rulemaking in 2024 expanded price transparency expectations for suppliers.

Legislation promoting price transparency and value-based care compels BD to prove cost-effectiveness and improved outcomes—key for placement in hospital formularies and GPO contracts where 20–30% of purchasing now ties to value metrics.

Failure to meet transparency and value standards risks exclusion from government-funded procurement; BD reported 2024 revenue of about 18.4 billion USD, a material portion tied to public-sector contracts vulnerable to policy shifts.

- Increased regulatory scrutiny on pricing and transparency

- Value-based procurement links 20–30% of purchasing to outcomes

- 2024 revenue ~18.4 billion USD; public contracts at risk

BD faces revenue pressure as value-based procurement and protectionism reshape 2025

Political shifts in 2024–25 raised public health budgets (US +4.2% YoY; EU +3.1% 2025), boosting procurement for diagnostics/vaccines; BD faces reimbursement and price-transparency pressures as value-based purchasing ties 20–30% of procurement to outcomes, risking public contract revenue within its $18.4B 2024 sales. Trade protectionism raised supply costs ~2–3%; BD spent $1.2B on regulatory R&D (2024).

| Metric | Value |

|---|---|

| 2024 Revenue | $18.4B |

| Public procurement tied to value | 20–30% |

| US health outlays 2025 | +4.2% YoY |

| EU health spend 2025 | +3.1% |

| Supply-chain cost rise | ~2–3% |

| Regulatory R&D (2024) | $1.2B |

What is included in the product

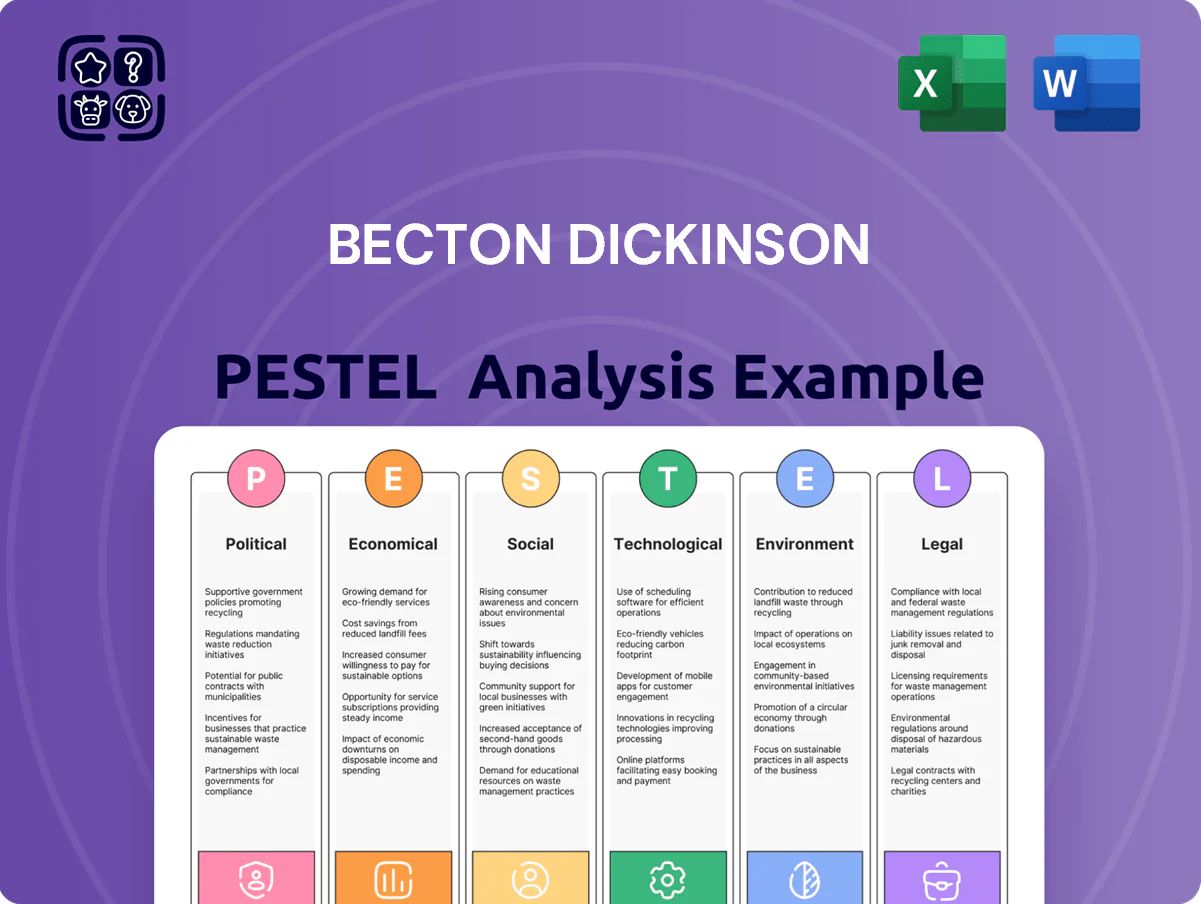

Explores how external macro-environmental factors uniquely affect Becton Dickinson across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise, PESTLE-segmented summary of Becton Dickinson that streamlines external risk assessment and market positioning for meetings, allowing quick drop-in to slides or strategy docs and easy team sharing.

Economic factors

Global inflationary pressures on manufacturing

By end-2025 global inflation stabilized at a higher baseline—core goods inflation near 4.5%—raising energy and medical-grade plastics costs by ~8–12% year-over-year, pressuring BD’s COGS on high-volume consumables.

BD offsets via strategic hedging (currency and commodity contracts covering ~60% of exposures) and operational efficiencies—productivity programs aiming for $500–700M annual run-rate savings—to protect margins.

Healthcare budget constraints in emerging markets

Economic volatility in emerging markets drives swings in public healthcare spending—World Bank data show government health expenditure as % of GDP varies from 1.5% to 6% across low- and middle-income countries—reducing demand for high-end diagnostics and pressuring BD to adapt pricing and payment terms.

BD must tailor product lines and tiered pricing; in 2024, emerging Asia health spending grew ~3.8% y/y while Sub-Saharan Africa contracted, underscoring divergent purchasing power across regions.

Successful expansion requires mapping local economic cycles, offering scalable, modular diagnostic platforms and financing models (leasing, reagent rental) to capture markets where capital budgets are constrained.

Currency exchange rate volatility

As a global healthcare supplier, BD faces material exposure to FX swings; in 2025 a 5% appreciation of the US dollar versus major currencies could reduce reported revenue by an estimated mid-single-digit percentage given ~40% of sales outside the US (2024 sales mix).

BD reported a 2024 FX headwind of about $200m on adjusted EPS; ongoing dollar strength remains a key downside risk into 2025.

Management employs robust hedging and natural offsets—forward contracts and currency options—targeting much of near-term transactional exposure to stabilize earnings.

Interest rate impacts on capital investment

The US federal funds rate rose from near-zero in 2021 to about 5.25–5.50% by late 2023; higher borrowing costs increase BD’s cost of debt and can compress hospitals’ capex—61% of US hospitals reported in 2024 delaying capital projects due to rates—shifting demand toward leasing and service models.

BD counters with flexible financing and leasing programs; in 2024 BD’s capital solutions supported customers as equipment leasing grew ~8% year-over-year.

- Higher rates raise BD’s funding costs and pressure hospital capex.

- 61% of US hospitals delayed projects in 2024.

- Demand shifts to leasing/service models; BD’s financing grew ~8% YoY in 2024.

Shift toward value-based purchasing models

The shift from volume- to value-based reimbursement in mature markets accelerated: US value-based programs covered roughly 40% of Medicare payments by 2024, pushing BD to supply real-world evidence that its devices lower total cost of care by reducing LOS and readmissions.

BD’s economic performance increasingly depends on bundling devices, analytics, and services into integrated value propositions that demonstrably improve outcomes and cut per-patient costs.

- ~40% Medicare under value-based models (2024)

- Focus on reducing LOS and readmissions to prove cost savings

- Need for integrated devices + analytics + services

BG: Rising COGS, $200M FX drag, 61% hospitals delay capex; leasing +8%, Medicare VBR ~40%

Higher baseline inflation and commodity cost inflation (8–12% y/y) raised BD’s COGS; 2024 FX headwind ≈$200m; ~40% sales outside US; 61% of US hospitals delayed capex in 2024; equipment leasing +8% YoY; Medicare value-based ~40% (2024).

| Metric | 2024–25 |

|---|---|

| COGS pressure | +8–12% |

| FX headwind | $200m |

| Sales outside US | ~40% |

| Hospitals delaying capex | 61% |

| Leasing growth | +8% YoY |

| Medicare VBR | ~40% |

What You See Is What You Get

Becton Dickinson PESTLE Analysis

The preview shown here is the exact Becton Dickinson PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, supply-chain dynamics, and rapid medtech innovation are reshaping Becton Dickinson’s strategic horizon—our concise PESTLE snapshot highlights the risks and opportunities driving performance. Purchase the full PESTLE analysis to access evidence-backed insights, scenario impacts, and ready-to-use recommendations for investors, strategists, and advisors.

Political factors

Post-election healthcare policy shifts

Post-election healthcare policy shifts in 2025—driven by major US and EU elections in late 2024—have prompted projected increases in national healthcare budgets: US federal health outlays up 4.2% YoY and EU health spending rising 3.1% in 2025, affecting subsidies for medtech adoption.

BD must recalibrate product pricing and R&D allocation as changes to reimbursement models could alter hospital capital expenditures—US hospital capex forecast +2.5% in 2025—while public health initiatives expand procurement for diagnostics and vaccination supplies.

Aligning with evolving subsidy frameworks and value-based purchasing pilots, BD’s strategy should prioritize devices eligible for government reimbursement to protect revenue streams tied to public contracts that represent over 30% of certain regional sales.

Geopolitical trade tensions and protectionism

Persistent trade frictions—US-China tariffs and 2023 EU import measures—raised global medical-supply costs; BD reported 2024 supply-chain costs up ~2–3% and invested $1.1bn in manufacturing capacity (2023–2024) to localize production. Protectionist mandates in India and Brazil forced BD to expand regional facilities, diversifying suppliers to sustain margins. Navigating these policies is critical to keep market access across Asia and Latin America.

Global pandemic preparedness funding

Governmental focus on biosecurity and pandemic prevention remained high through late 2025, driving sustained public investment—global health security spending rose to an estimated $85 billion in 2024–25, with diagnostics and surveillance accounting for roughly 28% ($23.8B), areas where BD holds a competitive edge in instruments and assays.

International regulatory harmonization efforts

Political cooperation among regulators — including ICH, IMDRF and WHO prequalification initiatives — is streamlining approvals for medical devices and diagnostics, potentially cutting time-to-market by up to 30% in some markets.

Harmonization reduces multiple filings but forces BD to comply with unified, often stricter standards; BD reported regulatory-related R&D spending of about $1.2 billion in 2024 to support global compliance.

BD actively lobbies and consults with policymakers and regulators to shape frameworks that balance patient safety with innovation, engaging in over 25 regulatory working groups and public consultations in 2024.

- Streamlining may reduce approval timelines by ~30%

- BD regulatory R&D spend ~ $1.2B in 2024

- Participation in 25+ regulatory working groups (2024)

Governmental focus on drug pricing and transparency

Political pressure to lower healthcare costs has intensified scrutiny on the medical supply chain, with U.S. policymakers pursuing drug and device price reforms that could affect BD's margins; CMS rulemaking in 2024 expanded price transparency expectations for suppliers.

Legislation promoting price transparency and value-based care compels BD to prove cost-effectiveness and improved outcomes—key for placement in hospital formularies and GPO contracts where 20–30% of purchasing now ties to value metrics.

Failure to meet transparency and value standards risks exclusion from government-funded procurement; BD reported 2024 revenue of about 18.4 billion USD, a material portion tied to public-sector contracts vulnerable to policy shifts.

- Increased regulatory scrutiny on pricing and transparency

- Value-based procurement links 20–30% of purchasing to outcomes

- 2024 revenue ~18.4 billion USD; public contracts at risk

BD faces revenue pressure as value-based procurement and protectionism reshape 2025

Political shifts in 2024–25 raised public health budgets (US +4.2% YoY; EU +3.1% 2025), boosting procurement for diagnostics/vaccines; BD faces reimbursement and price-transparency pressures as value-based purchasing ties 20–30% of procurement to outcomes, risking public contract revenue within its $18.4B 2024 sales. Trade protectionism raised supply costs ~2–3%; BD spent $1.2B on regulatory R&D (2024).

| Metric | Value |

|---|---|

| 2024 Revenue | $18.4B |

| Public procurement tied to value | 20–30% |

| US health outlays 2025 | +4.2% YoY |

| EU health spend 2025 | +3.1% |

| Supply-chain cost rise | ~2–3% |

| Regulatory R&D (2024) | $1.2B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Becton Dickinson across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise, PESTLE-segmented summary of Becton Dickinson that streamlines external risk assessment and market positioning for meetings, allowing quick drop-in to slides or strategy docs and easy team sharing.

Economic factors

Global inflationary pressures on manufacturing

By end-2025 global inflation stabilized at a higher baseline—core goods inflation near 4.5%—raising energy and medical-grade plastics costs by ~8–12% year-over-year, pressuring BD’s COGS on high-volume consumables.

BD offsets via strategic hedging (currency and commodity contracts covering ~60% of exposures) and operational efficiencies—productivity programs aiming for $500–700M annual run-rate savings—to protect margins.

Healthcare budget constraints in emerging markets

Economic volatility in emerging markets drives swings in public healthcare spending—World Bank data show government health expenditure as % of GDP varies from 1.5% to 6% across low- and middle-income countries—reducing demand for high-end diagnostics and pressuring BD to adapt pricing and payment terms.

BD must tailor product lines and tiered pricing; in 2024, emerging Asia health spending grew ~3.8% y/y while Sub-Saharan Africa contracted, underscoring divergent purchasing power across regions.

Successful expansion requires mapping local economic cycles, offering scalable, modular diagnostic platforms and financing models (leasing, reagent rental) to capture markets where capital budgets are constrained.

Currency exchange rate volatility

As a global healthcare supplier, BD faces material exposure to FX swings; in 2025 a 5% appreciation of the US dollar versus major currencies could reduce reported revenue by an estimated mid-single-digit percentage given ~40% of sales outside the US (2024 sales mix).

BD reported a 2024 FX headwind of about $200m on adjusted EPS; ongoing dollar strength remains a key downside risk into 2025.

Management employs robust hedging and natural offsets—forward contracts and currency options—targeting much of near-term transactional exposure to stabilize earnings.

Interest rate impacts on capital investment

The US federal funds rate rose from near-zero in 2021 to about 5.25–5.50% by late 2023; higher borrowing costs increase BD’s cost of debt and can compress hospitals’ capex—61% of US hospitals reported in 2024 delaying capital projects due to rates—shifting demand toward leasing and service models.

BD counters with flexible financing and leasing programs; in 2024 BD’s capital solutions supported customers as equipment leasing grew ~8% year-over-year.

- Higher rates raise BD’s funding costs and pressure hospital capex.

- 61% of US hospitals delayed projects in 2024.

- Demand shifts to leasing/service models; BD’s financing grew ~8% YoY in 2024.

Shift toward value-based purchasing models

The shift from volume- to value-based reimbursement in mature markets accelerated: US value-based programs covered roughly 40% of Medicare payments by 2024, pushing BD to supply real-world evidence that its devices lower total cost of care by reducing LOS and readmissions.

BD’s economic performance increasingly depends on bundling devices, analytics, and services into integrated value propositions that demonstrably improve outcomes and cut per-patient costs.

- ~40% Medicare under value-based models (2024)

- Focus on reducing LOS and readmissions to prove cost savings

- Need for integrated devices + analytics + services

BG: Rising COGS, $200M FX drag, 61% hospitals delay capex; leasing +8%, Medicare VBR ~40%

Higher baseline inflation and commodity cost inflation (8–12% y/y) raised BD’s COGS; 2024 FX headwind ≈$200m; ~40% sales outside US; 61% of US hospitals delayed capex in 2024; equipment leasing +8% YoY; Medicare value-based ~40% (2024).

| Metric | 2024–25 |

|---|---|

| COGS pressure | +8–12% |

| FX headwind | $200m |

| Sales outside US | ~40% |

| Hospitals delaying capex | 61% |

| Leasing growth | +8% YoY |

| Medicare VBR | ~40% |

What You See Is What You Get

Becton Dickinson PESTLE Analysis

The preview shown here is the exact Becton Dickinson PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.