Becton Dickinson SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Becton Dickinson’s robust medical device portfolio and global reach position it strongly amid aging populations and rising healthcare investment, though integration challenges and regulatory scrutiny pose material risks; competitive pressure from medtech innovators and supply-chain volatility temper near-term upside. Discover the full strategic picture with our complete SWOT analysis—purchase the editable, investor-ready report (Word + Excel) for data-driven planning and confident decisions.

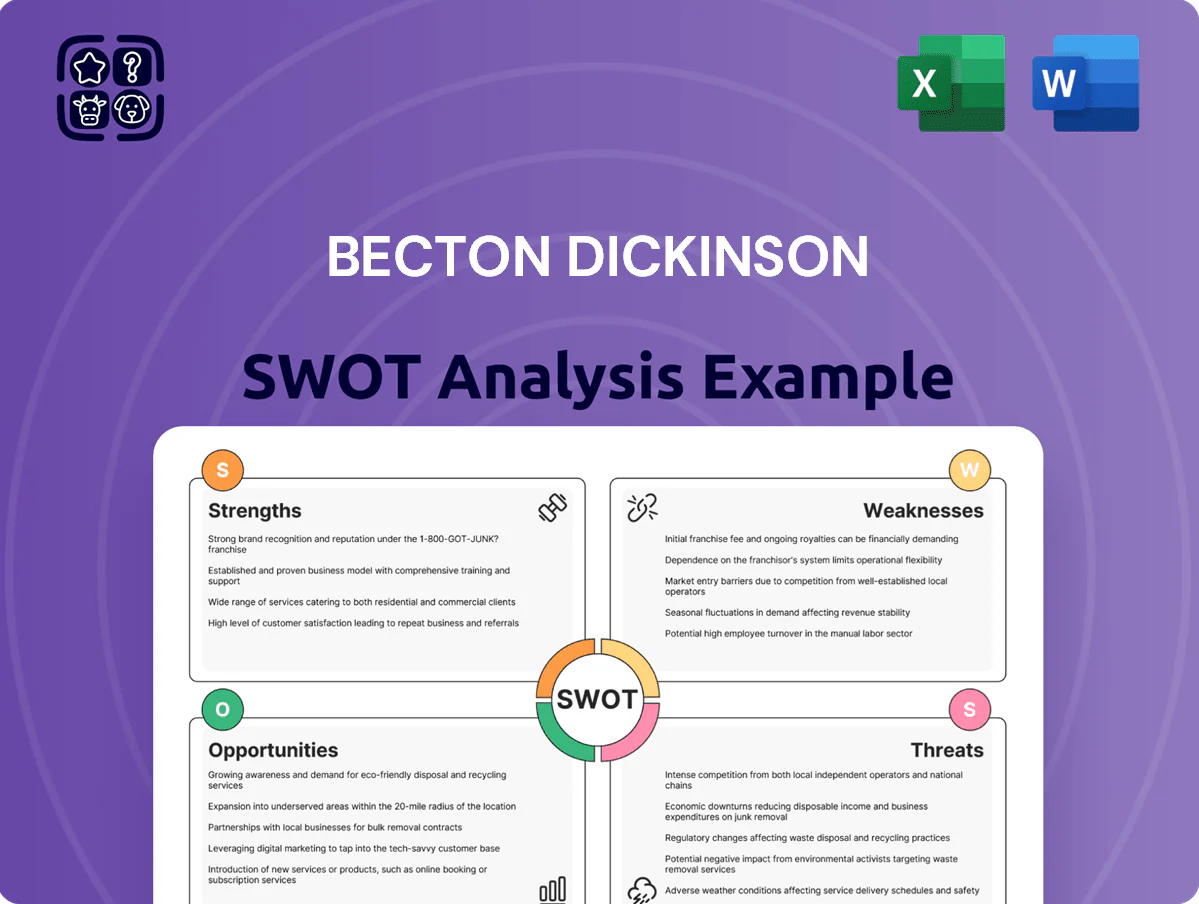

Strengths

Dominant Market Leadership in Medical Consumables

BD holds a leading share in medical consumables—needles, syringes, collection tubes—fueling about 45% of its 2024 product revenue of $10.1B, giving steady recurring sales because these items are used every patient encounter.

High unit volumes yield economies of scale: BD reported manufacturing gross margins of ~38% in FY2024, a cost advantage rivals struggle to match given BD’s global production footprint and procurement scale.

Diversified Revenue Streams Across Three Segments

BD operates through BD Medical, BD Life Sciences, and BD Interventional, reducing reliance on any single product line and lowering concentration risk.

In 2025 BD reported revenue of $20.6 billion; each segment contributed meaningfully (BD Medical ~45%, Life Sciences ~30%, Interventional ~25%), which cushions the company against sector-specific downturns.

This segment mix strengthens cash flow stability and regulatory resilience, helping sustain margins and fund R&D and M&A.

Robust Research and Development Pipeline

Extensive Global Distribution Infrastructure

BD operates in over 190 countries, giving it one of the largest medtech distribution networks; in FY2024 BD reported revenue of $20.5 billion, with international sales ~48%, enabling fast rollouts and scale in markets from the US to India.

Local teams ease regulatory approvals and logistics, reducing time-to-market for new products—BD cited over 30 regional regulatory hubs and a global supply chain footprint of 100+ manufacturing and distribution sites in 2024.

- 190+ countries presence

- FY2024 revenue $20.5B; 48% international

- 100+ manufacturing/distribution sites

- 30+ regional regulatory hubs

Strong Brand Reputation and Clinical Trust

BD’s ~125-year presence in hospitals has built strong clinical trust; FY2024 revenue hit $20.5B, showing durable customer relationships that ease new product adoption.

That brand equity helps secure multi-year procurement deals—repeat orders lowered churn and supported a 2024 gross margin of ~43%, improving marketing ROI.

- 125 years in healthcare

- $20.5B revenue FY2024

- ~43% gross margin FY2024

- Lower churn, stronger contract wins

BD’s global scale fuels $20.6B FY25 revenue, 45% consumables and $1.2B R&D

BD’s global scale drives recurring sales: FY2025 revenue $20.6B with ~45% from medical consumables; FY2024 gross margin ~38–43% and R&D ~$1.2B (2025). Presence in 190+ countries, 100+ sites, 30+ regulatory hubs, 125-year clinical trust, 40+ active R&D projects; 3.5% organic CAGR to 2027 and 0.9 ppt market share gain in 2025.

| Metric | Value |

|---|---|

| FY2025 Revenue | $20.6B |

| Consumables % | ~45% |

| R&D (2025) | $1.2B |

| Global reach | 190+ countries |

What is included in the product

Provides a concise SWOT overview of Becton Dickinson, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess the company’s strategic positioning and growth prospects.

Provides a concise SWOT matrix for Becton Dickinson to quickly align strategy and highlight priority risks and opportunities for executive decision-making.

Weaknesses

Significant Debt Load from Strategic Acquisitions

Historical Regulatory Challenges with Infusion Pumps

Ongoing issues and recalls of the Alaris infusion pump system have dented Becton Dickinson’s reputation and led to >$300m in remediation and legal costs through 2023, pressuring margins and contributing to a 2023 operating margin decline of ~220 basis points versus 2021.

Despite extensive fixes and a 2022–2024 compliance program, FDA and EU scrutiny persists, requiring continued CAPAs (corrective and preventive actions) and tying up senior management time.

These events expose weaknesses in BD’s quality controls for complex electronic devices; product-related recall frequency rose by ~30% in 2021–2023 versus 2018–2020.

Exposure to Fluctuations in Hospital Capital Budgets

A portion of BD's revenue—about 18% of fiscal 2024 sales ($4.1B of $22.7B total revenue)—comes from large capital-equipment and instrument sales that track hospital capex cycles; when hospitals cut budgets, orders are postponed, contributing to quarterly revenue swings (BD reported 6.5% YoY revenue decline in Q3 FY2024 for its life sciences/medical segments) and making 12–24 month forecasting less reliable.

Operational Complexity and Integration Risks

Becton Dickinson (BD) faces operational complexity across 60+ manufacturing sites and 50+ acquisitions since 2015, which strained integration — BD reported $16.2B revenue in FY2024 but saw SG&A rise 5% Y/Y, partly from integration costs.

Integrating diverse cultures and legacy IT systems caused temporary productivity dips; BD noted restructuring charges of $280M in 2024 tied to consolidation.

Size slows decisions versus smaller rivals; BD’s 2024 operating margin was 13.8%, below some mid-cap peers at ~18%.

- 60+ plants, 50+ acquisitions since 2015

- $16.2B revenue FY2024; SG&A +5% Y/Y

- $280M restructuring charges in 2024

- Operating margin 13.8% (2024)

Dependency on Specific Raw Material Pricing

Becton Dickinson (BD) relies heavily on plastics, resins and specialty metals for syringes and catheters, so raw-material price swings—oil-linked resin costs up ~18% in 2024—can hit margins if BD cannot pass costs to buyers.

Inflation in 2023–24 raised COGS pressure; BD’s 2024 gross margin fell to 39.1%, showing vulnerability without cost pass-through.

BD therefore needs active commodity hedging, multi-sourcing, and long-term contracts to protect profitability.

- Plastics/resins exposure

- Oil-linked input volatility ~+18% (2024)

- Gross margin 39.1% (FY2024)

- Requires hedging and multi-sourcing

Heavy debt, recalls dent margins: $16.5B net debt, rising costs squeeze results

| Metric | Value |

|---|---|

| Net debt (FY2024) | $16.5B |

| Edwards deal (2023) | $24B |

| Revenue (FY2024) | $16.2B |

| Operating margin (FY2024) | 13.8% |

| Gross margin (FY2024) | 39.1% |

| Alaris costs through 2023 | >$300M |

| Product recall rise | +30% (2021–2023) |

| Raw-materials change (2024) | +18% |

Same Document Delivered

Becton Dickinson SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; once purchased, the complete, editable version is unlocked. You’re viewing a live preview of the real file, ready for immediate download after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Becton Dickinson’s robust medical device portfolio and global reach position it strongly amid aging populations and rising healthcare investment, though integration challenges and regulatory scrutiny pose material risks; competitive pressure from medtech innovators and supply-chain volatility temper near-term upside. Discover the full strategic picture with our complete SWOT analysis—purchase the editable, investor-ready report (Word + Excel) for data-driven planning and confident decisions.

Strengths

Dominant Market Leadership in Medical Consumables

BD holds a leading share in medical consumables—needles, syringes, collection tubes—fueling about 45% of its 2024 product revenue of $10.1B, giving steady recurring sales because these items are used every patient encounter.

High unit volumes yield economies of scale: BD reported manufacturing gross margins of ~38% in FY2024, a cost advantage rivals struggle to match given BD’s global production footprint and procurement scale.

Diversified Revenue Streams Across Three Segments

BD operates through BD Medical, BD Life Sciences, and BD Interventional, reducing reliance on any single product line and lowering concentration risk.

In 2025 BD reported revenue of $20.6 billion; each segment contributed meaningfully (BD Medical ~45%, Life Sciences ~30%, Interventional ~25%), which cushions the company against sector-specific downturns.

This segment mix strengthens cash flow stability and regulatory resilience, helping sustain margins and fund R&D and M&A.

Robust Research and Development Pipeline

Extensive Global Distribution Infrastructure

BD operates in over 190 countries, giving it one of the largest medtech distribution networks; in FY2024 BD reported revenue of $20.5 billion, with international sales ~48%, enabling fast rollouts and scale in markets from the US to India.

Local teams ease regulatory approvals and logistics, reducing time-to-market for new products—BD cited over 30 regional regulatory hubs and a global supply chain footprint of 100+ manufacturing and distribution sites in 2024.

- 190+ countries presence

- FY2024 revenue $20.5B; 48% international

- 100+ manufacturing/distribution sites

- 30+ regional regulatory hubs

Strong Brand Reputation and Clinical Trust

BD’s ~125-year presence in hospitals has built strong clinical trust; FY2024 revenue hit $20.5B, showing durable customer relationships that ease new product adoption.

That brand equity helps secure multi-year procurement deals—repeat orders lowered churn and supported a 2024 gross margin of ~43%, improving marketing ROI.

- 125 years in healthcare

- $20.5B revenue FY2024

- ~43% gross margin FY2024

- Lower churn, stronger contract wins

BD’s global scale fuels $20.6B FY25 revenue, 45% consumables and $1.2B R&D

BD’s global scale drives recurring sales: FY2025 revenue $20.6B with ~45% from medical consumables; FY2024 gross margin ~38–43% and R&D ~$1.2B (2025). Presence in 190+ countries, 100+ sites, 30+ regulatory hubs, 125-year clinical trust, 40+ active R&D projects; 3.5% organic CAGR to 2027 and 0.9 ppt market share gain in 2025.

| Metric | Value |

|---|---|

| FY2025 Revenue | $20.6B |

| Consumables % | ~45% |

| R&D (2025) | $1.2B |

| Global reach | 190+ countries |

What is included in the product

Provides a concise SWOT overview of Becton Dickinson, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess the company’s strategic positioning and growth prospects.

Provides a concise SWOT matrix for Becton Dickinson to quickly align strategy and highlight priority risks and opportunities for executive decision-making.

Weaknesses

Significant Debt Load from Strategic Acquisitions

Historical Regulatory Challenges with Infusion Pumps

Ongoing issues and recalls of the Alaris infusion pump system have dented Becton Dickinson’s reputation and led to >$300m in remediation and legal costs through 2023, pressuring margins and contributing to a 2023 operating margin decline of ~220 basis points versus 2021.

Despite extensive fixes and a 2022–2024 compliance program, FDA and EU scrutiny persists, requiring continued CAPAs (corrective and preventive actions) and tying up senior management time.

These events expose weaknesses in BD’s quality controls for complex electronic devices; product-related recall frequency rose by ~30% in 2021–2023 versus 2018–2020.

Exposure to Fluctuations in Hospital Capital Budgets

A portion of BD's revenue—about 18% of fiscal 2024 sales ($4.1B of $22.7B total revenue)—comes from large capital-equipment and instrument sales that track hospital capex cycles; when hospitals cut budgets, orders are postponed, contributing to quarterly revenue swings (BD reported 6.5% YoY revenue decline in Q3 FY2024 for its life sciences/medical segments) and making 12–24 month forecasting less reliable.

Operational Complexity and Integration Risks

Becton Dickinson (BD) faces operational complexity across 60+ manufacturing sites and 50+ acquisitions since 2015, which strained integration — BD reported $16.2B revenue in FY2024 but saw SG&A rise 5% Y/Y, partly from integration costs.

Integrating diverse cultures and legacy IT systems caused temporary productivity dips; BD noted restructuring charges of $280M in 2024 tied to consolidation.

Size slows decisions versus smaller rivals; BD’s 2024 operating margin was 13.8%, below some mid-cap peers at ~18%.

- 60+ plants, 50+ acquisitions since 2015

- $16.2B revenue FY2024; SG&A +5% Y/Y

- $280M restructuring charges in 2024

- Operating margin 13.8% (2024)

Dependency on Specific Raw Material Pricing

Becton Dickinson (BD) relies heavily on plastics, resins and specialty metals for syringes and catheters, so raw-material price swings—oil-linked resin costs up ~18% in 2024—can hit margins if BD cannot pass costs to buyers.

Inflation in 2023–24 raised COGS pressure; BD’s 2024 gross margin fell to 39.1%, showing vulnerability without cost pass-through.

BD therefore needs active commodity hedging, multi-sourcing, and long-term contracts to protect profitability.

- Plastics/resins exposure

- Oil-linked input volatility ~+18% (2024)

- Gross margin 39.1% (FY2024)

- Requires hedging and multi-sourcing

Heavy debt, recalls dent margins: $16.5B net debt, rising costs squeeze results

| Metric | Value |

|---|---|

| Net debt (FY2024) | $16.5B |

| Edwards deal (2023) | $24B |

| Revenue (FY2024) | $16.2B |

| Operating margin (FY2024) | 13.8% |

| Gross margin (FY2024) | 39.1% |

| Alaris costs through 2023 | >$300M |

| Product recall rise | +30% (2021–2023) |

| Raw-materials change (2024) | +18% |

Same Document Delivered

Becton Dickinson SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; once purchased, the complete, editable version is unlocked. You’re viewing a live preview of the real file, ready for immediate download after payment.