Beat PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and technological advances are shaping Beat’s strategic path—our concise PESTLE highlights the external forces that matter and points to actionable risks and opportunities; purchase the full analysis for the complete, editable report and make data-driven decisions with confidence.

Political factors

Geopolitical stability in the Asia-Pacific region

The diplomatic and trade dynamics among China, Japan, and the US directly shape Beat Holdings’ investment landscape; US-China tariffs and export controls since 2020 have cut bilateral high-tech exports by over 25% in key segments, raising project risk and due diligence costs.

As a TMT and fintech investor, Beat faces potential capital flow restrictions and limits on technology transfer—Asia-Pacific foreign direct investment inflows fell 12% in 2023, highlighting vulnerability to escalations.

Maintaining entities in neutral hubs like Singapore or Hong Kong—Singapore attracted SGD 116.9 billion (about USD 86.3 billion) in FDI in 2023—preserves operational flexibility and access to regional markets and capital.

Government support for digital transformation

Regulatory stance on decentralized finance

By end-2025, regulatory stances on decentralized finance vary: 28 countries have enacted positive Web3 frameworks while 15 impose strict controls or bans, forcing Beat Holdings to adapt jurisdictionally to protect its $120m blockchain revenue stream. Navigating these political agendas is essential to maintain compliance across markets representing 42% of Beat’s user base. The company’s capacity to influence policy via industry coalitions and allocate ~4% of annual spend to compliance/legal is critical to secure long-term licenses and permits.

Trade policies and cross-border investment laws

Changes in trade agreements and FDI rules can speed or block TMT expansion; e.g., ASEAN GDP-weighted trade openness rose 3.1% in 2024 while several markets tightened FDI screening—FDI inflows to Southeast Asia fell 7% YoY in 2024, affecting deal pipelines for regional platforms.

Protectionist measures to shield domestic tech firms—India raised FDI scrutiny in 2023 and the EU adopted targeted investment screening—can compress multiples and complicate exits for international holding companies.

Monitoring legislative shifts in priority markets lets Beat Holdings hedge political risk; scenario planning and local joint ventures helped foreign investors preserve ~60–80% of deal value in recent cross-border tech transactions.

- Track FDI screening uptick: several markets tightened rules since 2023

- ASEAN trade openness +3.1% (2024) vs FDI inflows −7% YoY (2024)

- Protectionism risks compress valuation multiples and exit options

- Use scenario hedging and JV structures to retain 60–80% deal value

Data sovereignty and localization requirements

Governments are tightening data sovereignty rules: by 2024 over 60 countries had enacted localization laws, pushing firms to keep personal and financial data onshore. This trend compels fintech and TMT players to spend on local data centers—average capex rises 10–25%—and to manage layered compliance across jurisdictions.

For Beat Holdings, investments must ensure portfolio companies have both cloud/on-prem infrastructure and legal teams to meet local requirements, avoiding fines that in 2023 averaged 2–4% of annual revenue in major enforcement cases.

- 60+ countries with localization laws by 2024

- 10–25% higher capex for local infrastructure

- 2023 enforcement fines ~2–4% of revenue

- Requires tech + legal capacity in portfolio companies

Geopolitics, data rules and Web3 risk shave FDI, boost infra spend — Beat faces $120M blockchain squeeze

Geopolitical tensions (US-China, Japan) and rising protectionism since 2020 have cut high‑tech flows >25% and tightened FDI screening, reducing SEA FDI −7% (2024); 60+ countries adopted data localization by 2024 raising infra capex 10–25%; 28 countries support Web3 vs 15 bans (2025), threatening Beat’s $120m blockchain revenue and necessitating ~4% spend on compliance.

| Metric | Value |

|---|---|

| High‑tech export drop | >25% |

| SEA FDI change (2024) | −7% |

| Data localization (by 2024) | 60+ countries |

| Web3 legal stance (2025) | 28 supportive/15 bans |

| Beat blockchain revenue | $120m |

| Compliance spend | ~4% annual |

What is included in the product

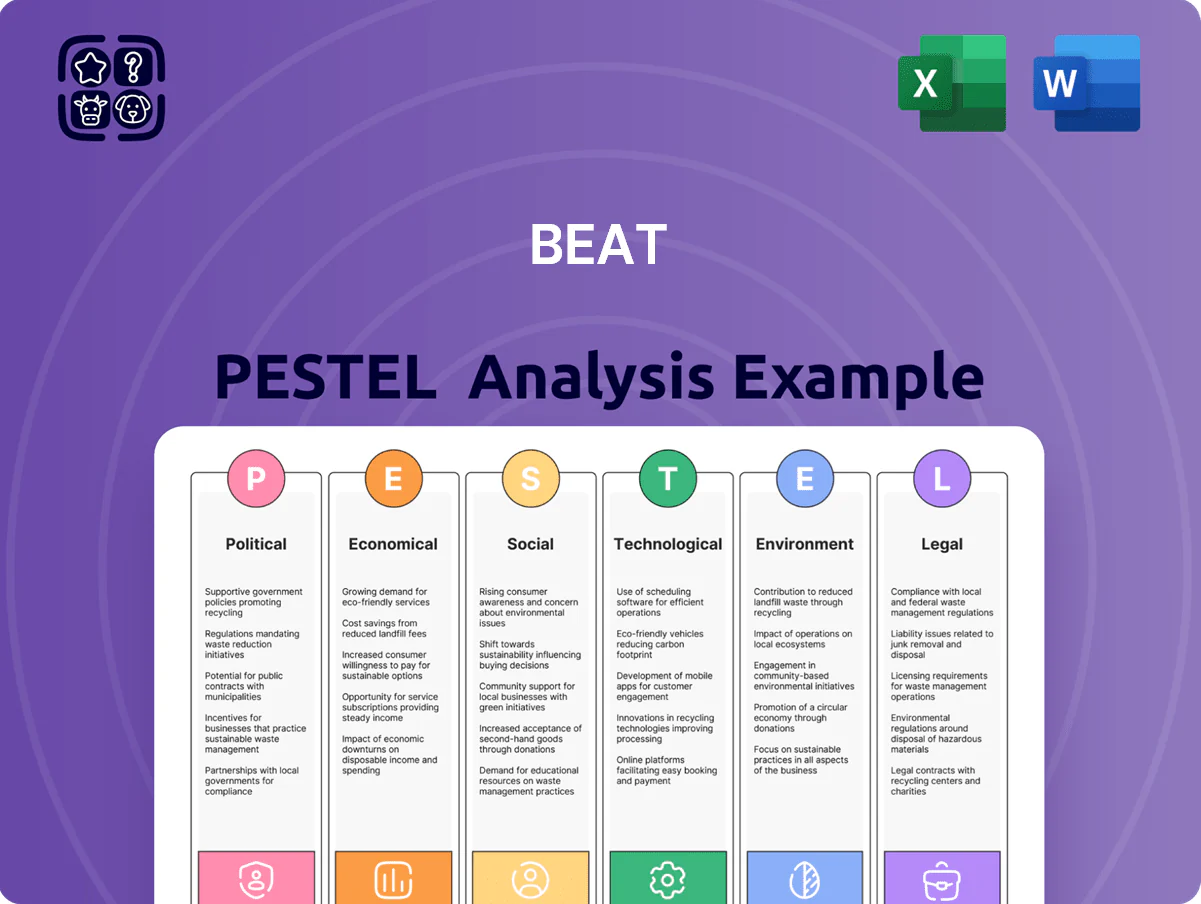

Explores how external macro-environmental factors uniquely affect the Beat across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to reveal risks and opportunities relevant to its region and industry.

Beat PESTLE delivers a concise, visually segmented summary of external risks and opportunities, ideal for dropping into presentations or sharing across teams to streamline strategy discussions and align stakeholders quickly.

Economic factors

Volatility in digital asset valuations

Valuations of blockchain services and digital assets remain highly sensitive to global cycles and sentiment; crypto market cap swung from about $1.6 trillion in Jan 2024 to roughly $1.1 trillion by Dec 2025, amplifying NAV volatility for Beat Holdings' crypto exposure.

Diversifying into traditional TMT and fintech reduced portfolio drawdowns in 2024–25; blended allocations limited peak-to-trough losses to ~28% versus ~54% for pure crypto baskets during major selloffs.

Regional interest rate environments

Interest rate decisions by Asia-Pacific central banks directly affect cost of capital and funding availability for investment holding companies; as of Dec 2025, key rates: RBA 4.35%, BoJ −0.10% (yield curve control relaxed), PBoC 3.45%, and RBI 6.50%, raising borrowing costs for cross-border deals.

Higher rates through 2023–24 compressed valuations for high-growth tech firms—global tech multiples fell ~28% from 2021 peaks—making acquisitions more expensive to finance.

Conversely, markets signaled stabilization in H2 2025 with easing inflation (APAC CPI averaging 3.1%), which may lower funding costs and support scaling fintech operations and M&A activity.

Economic growth rates in emerging Asian markets

Rapid expansion in Southeast Asia—GDP growth averaging 4.5–5.5% in 2023–2024 across ASEAN (Philippines 6.0% in 2024, Vietnam 5.5%) boosts consumer purchasing power, expanding fintech and TMT markets. Beat Holdings targets these markets to capture rising digital payments, lending and telecom demand, where 2024 e-wallet transactions grew ~25% YoY in SEA. Macroeconomic stability and growth trajectories directly shape exit valuations and portfolio revenue potential.

Currency exchange rate fluctuations

Operating across Japan, Hong Kong and the US exposes Beat Holdings to FX risk: JPY weakened ~9% vs USD in 2022–2024 while HKD remained pegged to USD with limited volatility, so translation effects depressed consolidated EBITDA by up to mid-single digits in 2023.

Robust hedging—forward contracts, FX options, and natural hedges—can stabilize cash flows; in 2024 corporate treasuries reported 60–80% hedge ratios for major exposures to limit P&L volatility.

- Primary exposures: JPY, HKD, USD

- 2022–24 JPY vs USD change: ~-9%

- HKD peg reduces local volatility

- Recommended hedges: forwards, options, natural hedging; target 60–80% cover

Availability of venture capital and private equity

The liquidity in private markets determines Beat Holdings ability to co-invest and time exits; global private equity dry powder reached about $2.5 trillion in mid-2025, easing co-investment capacity.

Institutional appetite for fintech and blockchain will shape deal competition by end-2025—allocations to fintech-focused funds rose ~12% in 2024, raising bid intensity for high-potential rounds.

Strong macro liquidity correlates with higher multiples and smoother raises; median late-stage fintech valuation multiples expanded ~18% from 2023 to 2025 amid accommodative conditions.

- Private equity dry powder ~ $2.5T (mid-2025)

- Fintech fund allocations +12% in 2024

- Late-stage fintech multiples +18% (2023–2025)

Macro Shifts: Crypto Slides, ASEAN Growth, PE Dry Powder & 60–80% FX Hedge

Economic swings drove crypto market cap from ~$1.6T (Jan 2024) to ~$1.1T (Dec 2025), while ASEAN GDP averaged 4.5–5.5% (2023–24) and SEA e-wallets +25% YoY (2024); APAC key rates (Dec 2025): RBA 4.35%, BoJ −0.10%, PBoC 3.45%, RBI 6.50%; private equity dry powder ~$2.5T (mid-2025); hedge target 60–80% FX cover to limit translation shocks.

| Metric | Value |

|---|---|

| Crypto mkt cap | $1.1–1.6T (2024–25) |

| ASEAN GDP | 4.5–5.5% |

| e-wallets SEA | +25% YoY (2024) |

| Key rates | RBA 4.35% BoJ −0.10% PBoC 3.45% RBI 6.50% |

| PE dry powder | $2.5T (mid-2025) |

| FX hedge | 60–80% |

Preview the Actual Deliverable

Beat PESTLE Analysis

The preview shown here is the exact Beat PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The layout, content, and structure visible in this preview match the final downloadable file, so what you see is exactly what you’ll own and can apply immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and technological advances are shaping Beat’s strategic path—our concise PESTLE highlights the external forces that matter and points to actionable risks and opportunities; purchase the full analysis for the complete, editable report and make data-driven decisions with confidence.

Political factors

Geopolitical stability in the Asia-Pacific region

The diplomatic and trade dynamics among China, Japan, and the US directly shape Beat Holdings’ investment landscape; US-China tariffs and export controls since 2020 have cut bilateral high-tech exports by over 25% in key segments, raising project risk and due diligence costs.

As a TMT and fintech investor, Beat faces potential capital flow restrictions and limits on technology transfer—Asia-Pacific foreign direct investment inflows fell 12% in 2023, highlighting vulnerability to escalations.

Maintaining entities in neutral hubs like Singapore or Hong Kong—Singapore attracted SGD 116.9 billion (about USD 86.3 billion) in FDI in 2023—preserves operational flexibility and access to regional markets and capital.

Government support for digital transformation

Regulatory stance on decentralized finance

By end-2025, regulatory stances on decentralized finance vary: 28 countries have enacted positive Web3 frameworks while 15 impose strict controls or bans, forcing Beat Holdings to adapt jurisdictionally to protect its $120m blockchain revenue stream. Navigating these political agendas is essential to maintain compliance across markets representing 42% of Beat’s user base. The company’s capacity to influence policy via industry coalitions and allocate ~4% of annual spend to compliance/legal is critical to secure long-term licenses and permits.

Trade policies and cross-border investment laws

Changes in trade agreements and FDI rules can speed or block TMT expansion; e.g., ASEAN GDP-weighted trade openness rose 3.1% in 2024 while several markets tightened FDI screening—FDI inflows to Southeast Asia fell 7% YoY in 2024, affecting deal pipelines for regional platforms.

Protectionist measures to shield domestic tech firms—India raised FDI scrutiny in 2023 and the EU adopted targeted investment screening—can compress multiples and complicate exits for international holding companies.

Monitoring legislative shifts in priority markets lets Beat Holdings hedge political risk; scenario planning and local joint ventures helped foreign investors preserve ~60–80% of deal value in recent cross-border tech transactions.

- Track FDI screening uptick: several markets tightened rules since 2023

- ASEAN trade openness +3.1% (2024) vs FDI inflows −7% YoY (2024)

- Protectionism risks compress valuation multiples and exit options

- Use scenario hedging and JV structures to retain 60–80% deal value

Data sovereignty and localization requirements

Governments are tightening data sovereignty rules: by 2024 over 60 countries had enacted localization laws, pushing firms to keep personal and financial data onshore. This trend compels fintech and TMT players to spend on local data centers—average capex rises 10–25%—and to manage layered compliance across jurisdictions.

For Beat Holdings, investments must ensure portfolio companies have both cloud/on-prem infrastructure and legal teams to meet local requirements, avoiding fines that in 2023 averaged 2–4% of annual revenue in major enforcement cases.

- 60+ countries with localization laws by 2024

- 10–25% higher capex for local infrastructure

- 2023 enforcement fines ~2–4% of revenue

- Requires tech + legal capacity in portfolio companies

Geopolitics, data rules and Web3 risk shave FDI, boost infra spend — Beat faces $120M blockchain squeeze

Geopolitical tensions (US-China, Japan) and rising protectionism since 2020 have cut high‑tech flows >25% and tightened FDI screening, reducing SEA FDI −7% (2024); 60+ countries adopted data localization by 2024 raising infra capex 10–25%; 28 countries support Web3 vs 15 bans (2025), threatening Beat’s $120m blockchain revenue and necessitating ~4% spend on compliance.

| Metric | Value |

|---|---|

| High‑tech export drop | >25% |

| SEA FDI change (2024) | −7% |

| Data localization (by 2024) | 60+ countries |

| Web3 legal stance (2025) | 28 supportive/15 bans |

| Beat blockchain revenue | $120m |

| Compliance spend | ~4% annual |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Beat across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to reveal risks and opportunities relevant to its region and industry.

Beat PESTLE delivers a concise, visually segmented summary of external risks and opportunities, ideal for dropping into presentations or sharing across teams to streamline strategy discussions and align stakeholders quickly.

Economic factors

Volatility in digital asset valuations

Valuations of blockchain services and digital assets remain highly sensitive to global cycles and sentiment; crypto market cap swung from about $1.6 trillion in Jan 2024 to roughly $1.1 trillion by Dec 2025, amplifying NAV volatility for Beat Holdings' crypto exposure.

Diversifying into traditional TMT and fintech reduced portfolio drawdowns in 2024–25; blended allocations limited peak-to-trough losses to ~28% versus ~54% for pure crypto baskets during major selloffs.

Regional interest rate environments

Interest rate decisions by Asia-Pacific central banks directly affect cost of capital and funding availability for investment holding companies; as of Dec 2025, key rates: RBA 4.35%, BoJ −0.10% (yield curve control relaxed), PBoC 3.45%, and RBI 6.50%, raising borrowing costs for cross-border deals.

Higher rates through 2023–24 compressed valuations for high-growth tech firms—global tech multiples fell ~28% from 2021 peaks—making acquisitions more expensive to finance.

Conversely, markets signaled stabilization in H2 2025 with easing inflation (APAC CPI averaging 3.1%), which may lower funding costs and support scaling fintech operations and M&A activity.

Economic growth rates in emerging Asian markets

Rapid expansion in Southeast Asia—GDP growth averaging 4.5–5.5% in 2023–2024 across ASEAN (Philippines 6.0% in 2024, Vietnam 5.5%) boosts consumer purchasing power, expanding fintech and TMT markets. Beat Holdings targets these markets to capture rising digital payments, lending and telecom demand, where 2024 e-wallet transactions grew ~25% YoY in SEA. Macroeconomic stability and growth trajectories directly shape exit valuations and portfolio revenue potential.

Currency exchange rate fluctuations

Operating across Japan, Hong Kong and the US exposes Beat Holdings to FX risk: JPY weakened ~9% vs USD in 2022–2024 while HKD remained pegged to USD with limited volatility, so translation effects depressed consolidated EBITDA by up to mid-single digits in 2023.

Robust hedging—forward contracts, FX options, and natural hedges—can stabilize cash flows; in 2024 corporate treasuries reported 60–80% hedge ratios for major exposures to limit P&L volatility.

- Primary exposures: JPY, HKD, USD

- 2022–24 JPY vs USD change: ~-9%

- HKD peg reduces local volatility

- Recommended hedges: forwards, options, natural hedging; target 60–80% cover

Availability of venture capital and private equity

The liquidity in private markets determines Beat Holdings ability to co-invest and time exits; global private equity dry powder reached about $2.5 trillion in mid-2025, easing co-investment capacity.

Institutional appetite for fintech and blockchain will shape deal competition by end-2025—allocations to fintech-focused funds rose ~12% in 2024, raising bid intensity for high-potential rounds.

Strong macro liquidity correlates with higher multiples and smoother raises; median late-stage fintech valuation multiples expanded ~18% from 2023 to 2025 amid accommodative conditions.

- Private equity dry powder ~ $2.5T (mid-2025)

- Fintech fund allocations +12% in 2024

- Late-stage fintech multiples +18% (2023–2025)

Macro Shifts: Crypto Slides, ASEAN Growth, PE Dry Powder & 60–80% FX Hedge

Economic swings drove crypto market cap from ~$1.6T (Jan 2024) to ~$1.1T (Dec 2025), while ASEAN GDP averaged 4.5–5.5% (2023–24) and SEA e-wallets +25% YoY (2024); APAC key rates (Dec 2025): RBA 4.35%, BoJ −0.10%, PBoC 3.45%, RBI 6.50%; private equity dry powder ~$2.5T (mid-2025); hedge target 60–80% FX cover to limit translation shocks.

| Metric | Value |

|---|---|

| Crypto mkt cap | $1.1–1.6T (2024–25) |

| ASEAN GDP | 4.5–5.5% |

| e-wallets SEA | +25% YoY (2024) |

| Key rates | RBA 4.35% BoJ −0.10% PBoC 3.45% RBI 6.50% |

| PE dry powder | $2.5T (mid-2025) |

| FX hedge | 60–80% |

Preview the Actual Deliverable

Beat PESTLE Analysis

The preview shown here is the exact Beat PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The layout, content, and structure visible in this preview match the final downloadable file, so what you see is exactly what you’ll own and can apply immediately after checkout.