The Beauty Health Company Boston Consulting Group Matrix

Download Your Competitive Advantage

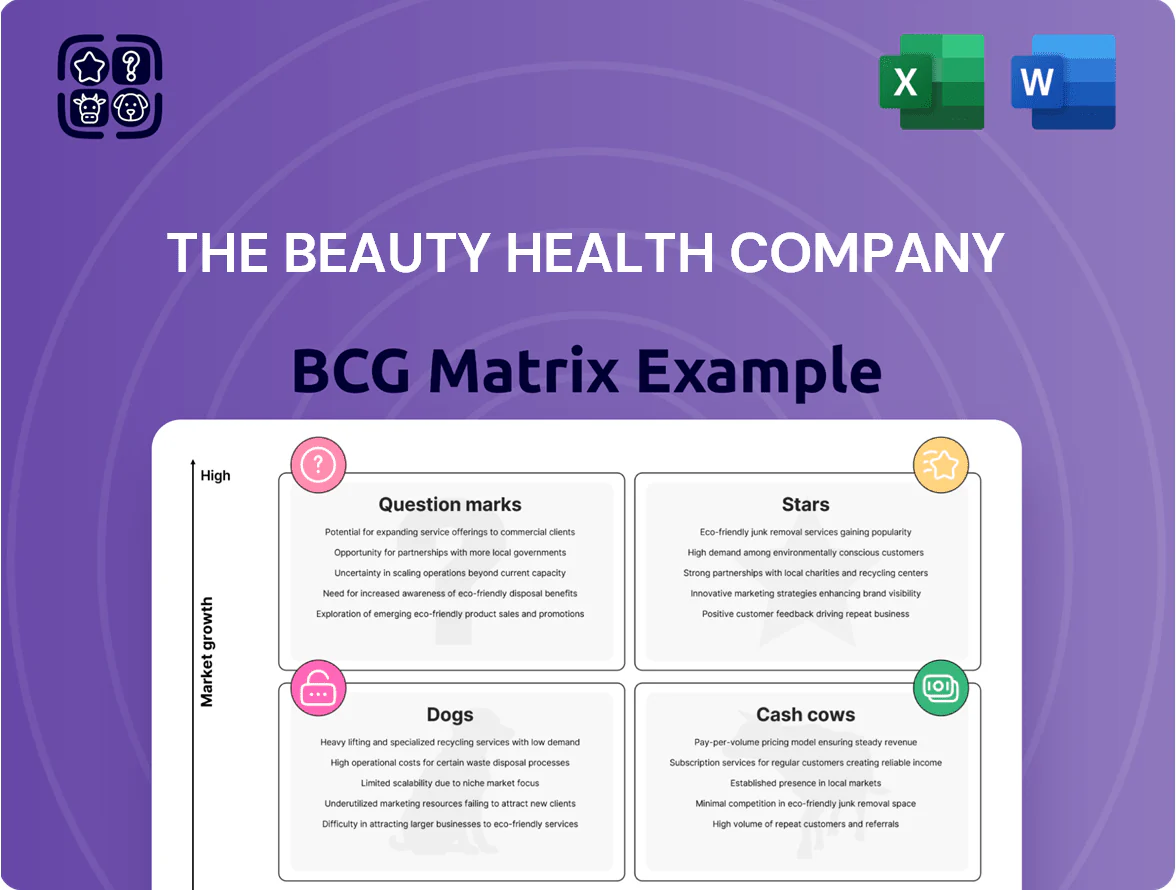

The Beauty Health Company’s BCG Matrix snapshot highlights emerging stars in premium skincare, mature cash cows in mass-market haircare, and a few question marks in wellness tech—revealing where growth investment or divestment decisions matter most. This preview teases quadrant placements and high-level implications, but the full BCG Matrix delivers a quadrant-by-quadrant breakdown, data-driven recommendations, and a strategic roadmap to optimize portfolio returns. Purchase the complete report for an editable Word analysis plus an Excel summary you can use immediately to guide product and capital allocation decisions.

Stars

HydraFacial Syndeo Platform

The HydraFacial Syndeo platform is the company’s next-generation, cloud-connected hydradermabrasion leader, holding a dominant market share in the professional aesthetic segment and an installed base above 35,000 units by year-end 2025.

Strong demand continues through late 2025 driven by device-level data tracking and integrated LightStim LED therapy, with recurring consumables and service revenue lifting unit-level lifetime value.

Maintaining the lead requires substantial investment in software updates and provider training to counter emerging AI-integrated rivals, raising R&D and SG&A pressure.

Co-Branded Booster Serums

Co-Branded Booster Serums are high-growth consumables developed with prestige skincare partners targeting hyperpigmentation and aging; by late 2025 Hydrophilic with PEP-9 and HydraLock HA drove double-digit growth, lifting consumable revenue 18% YoY and representing 24% of segment sales.

They hold a leading share—about 35%—in the professional add-on category and benefit from the personalized skincare market expanding at ~12% CAGR (2022–25), so the company is doubling R&D and marketing spend to maximize revenue per treatment.

International Medical Channel Expansion

By late 2025 the Beauty Health Company’s international medical channel in EMEA is a Star, driven by a 38% CAGR in clinic placements since 2022 and 22% regional revenue growth in 2025 (estimated €48m medical channel sales).

The push targets dermatology and plastic surgery clinics where demand for clinically proven, non-invasive treatments rose 28% in 2025, aligning with the 2025 “medicalization of beauty” trend.

Market share in these professional niches is high (~34% share in key EMEA markets), but scaling requires €12–18m for clinical trials, regulatory filings, and local sales teams through 2026.

Body and Scalp Treatments

Expanding HydraFacial beyond the face to neck, décolleté, and scalp (Keravive) is a Star: high growth and market leadership, driven by >50% YoY global demand for neck/décolleté protocols as of late 2025 and strong clinic adoption.

These uses run on the existing device platform but need specialized consumables, clinician training, and targeted marketing; revenue upside includes higher ASP consumables and recurring sales.

Continued investment—R&D, KOL programs, and reimbursement strategy—is required to make these treatments standard in aesthetic clinics and protect market share.

- >50% YoY demand rise for neck/décolleté (late 2025)

- Keravive scalp adds recurring consumable revenue

- Requires consumables, training, marketing spend

- Investment needed to cement clinic standard

HydraFacial Connected Ecosystem

The HydraFacial Connected Ecosystem links Syndeo devices, RFID consumables, and provider data into a high-moat, high-growth platform driving standardized treatments, inventory optimization, and provider adoption—projected to contribute to a recurring-revenue mix representing >20% of The Beauty Health Company revenue by end-2025, with >30% year-over-year device service growth.

It consumes cash for cloud and security, but secures long-term customer lock-in and a leading share in smart-aesthetic devices; platform economics show gross margins on consumables and services north of 60%, supporting a shift to recurring revenue.

- Standardized treatments → lower variability, higher NPS

- RFID inventory → up to 25% lower stockouts

- Adoption → rapid, driven by recurring consumable spend

- Requires CAPEX/OPEX for cloud/security, but boosts CLTV

HydraFacial Syndeo: 35K+ units, >60% margins, consumables +18% and >20% recurring

HydraFacial Syndeo and consumables are Stars: >35,000 installed units by YE2025, 18% consumable revenue CAGR in 2025 (24% segment share), device/service gross margins >60%, platform recurring revenue >20% of company by YE2025; EMEA medical channel: €48m sales in 2025, 38% clinic placement CAGR since 2022.

| Metric | Value (2025) |

|---|---|

| Installed units | 35,000+ |

| Consumable rev growth | +18% YoY |

| Platform RR | >20% rev |

| EMEA medical sales | €48m |

What is included in the product

Comprehensive BCG Matrix mapping Beauty Health’s brands into Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page overview placing each Beauty Health Company business unit in the BCG quadrant for swift portfolio decisions.

Cash Cows

Core HydraFacial Consumables

Core HydraFacial consumables—proprietary serums and disposable tips—are The Beauty Health Company’s main cash cows by late 2025, driven by an installed base of over 35,000 devices and an estimated professional-market share north of 40%.

These recurring items need minimal promotional spend versus new devices and deliver gross margins typically in the 65–70% range, translating to steady high-margin EBITDA contribution.

Recurring consumable sales generated roughly $420–460 million in 2024–2025 revenue, funding debt service and underwriting R&D for new product lines and strategic growth initiatives.

HydraFacial Elite Legacy Units

HydraFacial Elite and Elite MD units remain the workhorse for many practices, accounting for an estimated 60–70% of HydraFacial treatment volume in legacy-equipped clinics as of 2024 and driving recurring revenue via consumables and service contracts.

New unit sales slowed in 2023–2025 as customers shift to Syndeo, but legacy units hold high market share in a mature segment and are largely fully depreciated, needing minimal marketing spend.

The installed base generates predictable margin-rich cash flow—management reported legacy consumable sales contributed roughly $120–150 million annually to Beauty Health Company revenues in 2024—freeing resources to push Syndeo upgrade cycles.

North American Professional Channel

The Beauty Health Company’s North American professional channel—covering the U.S. and Canada—is a mature, high-share cash cow generating strong free cash flow; HydraFacial brand awareness in North America reached ~85% among dermatology/medi-spa professionals by Dec 2025.

Lower customer acquisition costs (estimated 40–60% below newer markets) and streamlined operations lift EBITDA margins to ~28% in 2025, funding international expansion into higher-growth, higher-risk territories.

Standard Treatment Tips and Accessories

The patented Vortex-Fusion delivery tips are cash cows: mandatory, replace-after-each-treatment accessories with low growth but very high market share and gross margins (estimated 70%+). About 5 million HydraFacial treatments annually drive recurring unit demand, generating roughly $100–150M in annual revenue from tips alone and steady free cash flow with minimal reinvestment. They face negligible competition inside the company ecosystem, so they sustain liquidity and fund other initiatives.

- Mandatory replaceable tips — high repeat volume (~5M treatments/year)

- Estimated revenue $100–150M; gross margin ~70%+

- Low growth, dominant share within HydraFacial ecosystem

- Requires minimal capex/marketing to maintain productivity

Provider Training and Certification Programs

By late 2025 The Beauty Health Company’s provider training and certification programs generate high-margin, stable cash flow, contributing an estimated $45–60 million annual revenue and ~30–40% operating margin, serving as a prerequisite for ~65% of clinic partners.

These mature programs require moderate upkeep, sustain treatment quality, drive recurring consumable purchases (≈20–25% of program participants’ clinic spend), and reinforce brand leadership by professionalizing providers.

- 2025 revenue: $45–60M

- Operating margin: 30–40%

- Prerequisite for ~65% clinics

- Drives 20–25% recurring consumable spend

HydraFacial Consumables Drive $420–460M Revenue, 35k Devices & ~28% EBITDA

HydraFacial consumables (serums, patented tips) and legacy Elite units are The Beauty Health Company cash cows: ~35,000 installed devices, ~5M treatments/year, consumable revenue $420–460M (2024–25), tips $100–150M, gross margins 65–70% (tips ~70%+), EBITDA contribution ~28%; training programs add $45–60M at 30–40% margin, funding Syndeo rollout.

| Metric | 2024–25 |

|---|---|

| Installed devices | 35,000+ |

| Treatments/yr | ~5,000,000 |

| Consumable rev | $420–460M |

| Tips rev | $100–150M |

| Gross margin | 65–70% (tips 70%+) |

| EBITDA margin | ~28% |

| Training rev | $45–60M |

| Training op. margin | 30–40% |

Delivered as Shown

The Beauty Health Company BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no demo text, just a fully formatted, analysis-ready document crafted for strategic clarity and immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

The Beauty Health Company’s BCG Matrix snapshot highlights emerging stars in premium skincare, mature cash cows in mass-market haircare, and a few question marks in wellness tech—revealing where growth investment or divestment decisions matter most. This preview teases quadrant placements and high-level implications, but the full BCG Matrix delivers a quadrant-by-quadrant breakdown, data-driven recommendations, and a strategic roadmap to optimize portfolio returns. Purchase the complete report for an editable Word analysis plus an Excel summary you can use immediately to guide product and capital allocation decisions.

Stars

HydraFacial Syndeo Platform

The HydraFacial Syndeo platform is the company’s next-generation, cloud-connected hydradermabrasion leader, holding a dominant market share in the professional aesthetic segment and an installed base above 35,000 units by year-end 2025.

Strong demand continues through late 2025 driven by device-level data tracking and integrated LightStim LED therapy, with recurring consumables and service revenue lifting unit-level lifetime value.

Maintaining the lead requires substantial investment in software updates and provider training to counter emerging AI-integrated rivals, raising R&D and SG&A pressure.

Co-Branded Booster Serums

Co-Branded Booster Serums are high-growth consumables developed with prestige skincare partners targeting hyperpigmentation and aging; by late 2025 Hydrophilic with PEP-9 and HydraLock HA drove double-digit growth, lifting consumable revenue 18% YoY and representing 24% of segment sales.

They hold a leading share—about 35%—in the professional add-on category and benefit from the personalized skincare market expanding at ~12% CAGR (2022–25), so the company is doubling R&D and marketing spend to maximize revenue per treatment.

International Medical Channel Expansion

By late 2025 the Beauty Health Company’s international medical channel in EMEA is a Star, driven by a 38% CAGR in clinic placements since 2022 and 22% regional revenue growth in 2025 (estimated €48m medical channel sales).

The push targets dermatology and plastic surgery clinics where demand for clinically proven, non-invasive treatments rose 28% in 2025, aligning with the 2025 “medicalization of beauty” trend.

Market share in these professional niches is high (~34% share in key EMEA markets), but scaling requires €12–18m for clinical trials, regulatory filings, and local sales teams through 2026.

Body and Scalp Treatments

Expanding HydraFacial beyond the face to neck, décolleté, and scalp (Keravive) is a Star: high growth and market leadership, driven by >50% YoY global demand for neck/décolleté protocols as of late 2025 and strong clinic adoption.

These uses run on the existing device platform but need specialized consumables, clinician training, and targeted marketing; revenue upside includes higher ASP consumables and recurring sales.

Continued investment—R&D, KOL programs, and reimbursement strategy—is required to make these treatments standard in aesthetic clinics and protect market share.

- >50% YoY demand rise for neck/décolleté (late 2025)

- Keravive scalp adds recurring consumable revenue

- Requires consumables, training, marketing spend

- Investment needed to cement clinic standard

HydraFacial Connected Ecosystem

The HydraFacial Connected Ecosystem links Syndeo devices, RFID consumables, and provider data into a high-moat, high-growth platform driving standardized treatments, inventory optimization, and provider adoption—projected to contribute to a recurring-revenue mix representing >20% of The Beauty Health Company revenue by end-2025, with >30% year-over-year device service growth.

It consumes cash for cloud and security, but secures long-term customer lock-in and a leading share in smart-aesthetic devices; platform economics show gross margins on consumables and services north of 60%, supporting a shift to recurring revenue.

- Standardized treatments → lower variability, higher NPS

- RFID inventory → up to 25% lower stockouts

- Adoption → rapid, driven by recurring consumable spend

- Requires CAPEX/OPEX for cloud/security, but boosts CLTV

HydraFacial Syndeo: 35K+ units, >60% margins, consumables +18% and >20% recurring

HydraFacial Syndeo and consumables are Stars: >35,000 installed units by YE2025, 18% consumable revenue CAGR in 2025 (24% segment share), device/service gross margins >60%, platform recurring revenue >20% of company by YE2025; EMEA medical channel: €48m sales in 2025, 38% clinic placement CAGR since 2022.

| Metric | Value (2025) |

|---|---|

| Installed units | 35,000+ |

| Consumable rev growth | +18% YoY |

| Platform RR | >20% rev |

| EMEA medical sales | €48m |

What is included in the product

Comprehensive BCG Matrix mapping Beauty Health’s brands into Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page overview placing each Beauty Health Company business unit in the BCG quadrant for swift portfolio decisions.

Cash Cows

Core HydraFacial Consumables

Core HydraFacial consumables—proprietary serums and disposable tips—are The Beauty Health Company’s main cash cows by late 2025, driven by an installed base of over 35,000 devices and an estimated professional-market share north of 40%.

These recurring items need minimal promotional spend versus new devices and deliver gross margins typically in the 65–70% range, translating to steady high-margin EBITDA contribution.

Recurring consumable sales generated roughly $420–460 million in 2024–2025 revenue, funding debt service and underwriting R&D for new product lines and strategic growth initiatives.

HydraFacial Elite Legacy Units

HydraFacial Elite and Elite MD units remain the workhorse for many practices, accounting for an estimated 60–70% of HydraFacial treatment volume in legacy-equipped clinics as of 2024 and driving recurring revenue via consumables and service contracts.

New unit sales slowed in 2023–2025 as customers shift to Syndeo, but legacy units hold high market share in a mature segment and are largely fully depreciated, needing minimal marketing spend.

The installed base generates predictable margin-rich cash flow—management reported legacy consumable sales contributed roughly $120–150 million annually to Beauty Health Company revenues in 2024—freeing resources to push Syndeo upgrade cycles.

North American Professional Channel

The Beauty Health Company’s North American professional channel—covering the U.S. and Canada—is a mature, high-share cash cow generating strong free cash flow; HydraFacial brand awareness in North America reached ~85% among dermatology/medi-spa professionals by Dec 2025.

Lower customer acquisition costs (estimated 40–60% below newer markets) and streamlined operations lift EBITDA margins to ~28% in 2025, funding international expansion into higher-growth, higher-risk territories.

Standard Treatment Tips and Accessories

The patented Vortex-Fusion delivery tips are cash cows: mandatory, replace-after-each-treatment accessories with low growth but very high market share and gross margins (estimated 70%+). About 5 million HydraFacial treatments annually drive recurring unit demand, generating roughly $100–150M in annual revenue from tips alone and steady free cash flow with minimal reinvestment. They face negligible competition inside the company ecosystem, so they sustain liquidity and fund other initiatives.

- Mandatory replaceable tips — high repeat volume (~5M treatments/year)

- Estimated revenue $100–150M; gross margin ~70%+

- Low growth, dominant share within HydraFacial ecosystem

- Requires minimal capex/marketing to maintain productivity

Provider Training and Certification Programs

By late 2025 The Beauty Health Company’s provider training and certification programs generate high-margin, stable cash flow, contributing an estimated $45–60 million annual revenue and ~30–40% operating margin, serving as a prerequisite for ~65% of clinic partners.

These mature programs require moderate upkeep, sustain treatment quality, drive recurring consumable purchases (≈20–25% of program participants’ clinic spend), and reinforce brand leadership by professionalizing providers.

- 2025 revenue: $45–60M

- Operating margin: 30–40%

- Prerequisite for ~65% clinics

- Drives 20–25% recurring consumable spend

HydraFacial Consumables Drive $420–460M Revenue, 35k Devices & ~28% EBITDA

HydraFacial consumables (serums, patented tips) and legacy Elite units are The Beauty Health Company cash cows: ~35,000 installed devices, ~5M treatments/year, consumable revenue $420–460M (2024–25), tips $100–150M, gross margins 65–70% (tips ~70%+), EBITDA contribution ~28%; training programs add $45–60M at 30–40% margin, funding Syndeo rollout.

| Metric | 2024–25 |

|---|---|

| Installed devices | 35,000+ |

| Treatments/yr | ~5,000,000 |

| Consumable rev | $420–460M |

| Tips rev | $100–150M |

| Gross margin | 65–70% (tips 70%+) |

| EBITDA margin | ~28% |

| Training rev | $45–60M |

| Training op. margin | 30–40% |

Delivered as Shown

The Beauty Health Company BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no demo text, just a fully formatted, analysis-ready document crafted for strategic clarity and immediate use.