Bechtle PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a competitive advantage with our targeted PESTLE Analysis of Bechtle—uncover how political shifts, economic cycles, tech disruption, social trends, and regulatory pressures will shape its trajectory; ideal for investors and strategists. Purchase the full, ready-to-use report to access deep-dive insights, actionable risks/opportunities, and editable charts for immediate decision-making.

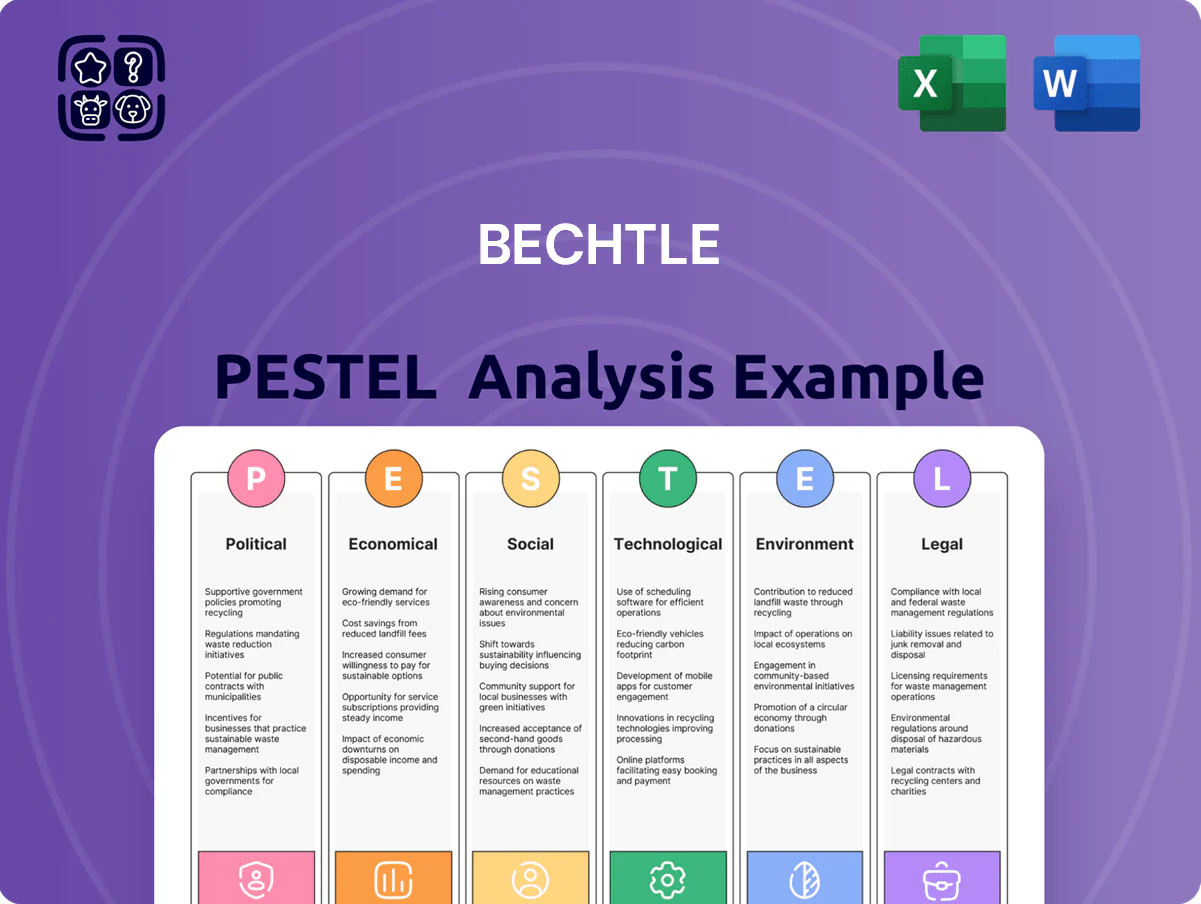

Political factors

EU Digital Sovereignty Initiatives

The EU's digital sovereignty drive boosts demand for localized cloud and EU-sourced IT infrastructure, benefiting Bechtle as customers favor regional suppliers; EU cloud market projected at €70–90bn by 2030 supports this shift. As governments cut reliance on non-EU tech, Bechtle is well-placed as a trusted partner for public sector digital transformation, already serving hundreds of public clients. Policy incentives are spurring investments in sovereign data centers and specialized software services across Europe, expanding addressable market and recurring revenue opportunities for Bechtle.

Public Sector Procurement Budgets

Bechtle's high exposure to public sector clients makes revenue sensitive to government spending cycles across Germany and Europe; public-sector sales accounted for about 48% of FY2024 revenue (€6.1bn of €12.7bn). By late 2025, increased defense budgets—Germany's defense spending rose to ~2.5% of GDP in 2024—and administrative IT modernization projects are primary IT procurement drivers. Political shifts toward national security and infrastructure resilience directly affect the pipeline and scale of large tenders available to Bechtle.

Geopolitical Trade Tensions

Ongoing trade disputes and export controls—notably 2024 restrictions on advanced chips from China and periodic US-EU measures—have increased lead times for servers and network gear by up to 25%, complicating Bechtle’s global IT supply chain. Political bans on specific vendors for critical infrastructure force Bechtle to pivot procurement and consulting approaches, affecting margin and vendor mix. Managing these geopolitical risks is essential to ensure hardware availability and meet compliance for regulated clients.

European Defense and Security Policy

The EU increased defense spending to an estimated 2.2% of GDP in 2024 across member states, boosting cybersecurity and military IT budgets; Bechtle captures this via sales of secure servers, encrypted communication systems and certified endpoint solutions to defense agencies.

Political alignment on cross-border security initiatives—NATO-EU cooperation and Permanent Structured Cooperation (PESCO) projects—creates multi-year procurement pipelines; Bechtle reported 9% growth in public sector IT revenue in FY 2024, reflecting this demand.

- EU defense spend ~2.2% of GDP (2024)

- Bechtle public sector IT revenue growth 9% FY2024

- Stable multi-year contracts from PESCO/NATO collaborations

Digitalization of Government Services

- Public IT spend ~€45.6bn (2023)

- Bechtle public-sector revenue ~€1.1bn (2024)

- OZG-driven demand across federal/state/municipal levels

Bechtle cashes in on EU digital sovereignty—public IT fuels growth despite longer lead times

EU digital sovereignty and rising defense/administrative IT budgets drive demand for Bechtle’s localized cloud, secure infrastructure and public-sector services; public-sector revenue ~48% of FY2024 (€6.1bn of €12.7bn) with 9% public IT growth in 2024. Supply-chain controls and export restrictions lengthen lead times ~25%, affecting margins and vendor mix.

| Metric | Value |

|---|---|

| FY2024 revenue | €12.7bn |

| Public-sector share | 48% (€6.1bn) |

| Public IT growth 2024 | 9% |

| Lead-time increase | ~25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bechtle across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, PESTLE-segmented summary of Bechtle’s external environment that can be dropped into presentations or shared across teams for rapid alignment during strategy and risk discussions.

Economic factors

European Economic Growth Trends

Economic growth in the DACH region and EU influences Bechtle’s medium-sized clients; Eurostat GDP data show Germany grew 0.5% in 2024 and euro area 0.6%, constraining large IT spends. Public sector demand remains stable, supported by 2024 EU ICT budgets up 3%, while private IT spending closely tracks industrial production, which rose 1.2% in Germany in 2024. By end-2025, cautious recovery sees firms favoring efficiency-focused software and services over major hardware refresh cycles.

Inflationary Pressure and Cost Management

Persistent inflation—Eurozone HICP at 3.4% in 2025 vs 7.2% in 2022—pushes Bechtle to tighten pricing and cut costs; FY2024 gross margin of 21.6% and operating margin of 5.4% show limited buffer, so wage inflation for skilled IT staff (German average IT salary growth ~4–6% in 2024–25) risks squeezing margins unless service rates rise.

Interest Rate Environment

The 2024 euro-area rate hiking cycle—ECB deposit rate at 4.00% (Dec 2024)—raises Bechtle’s weighted average cost of capital, increasing acquisition financing costs and pressuring margins on large deals.

Higher rates shift customer preference toward leasing and Device-as-a-Service; in 2024 leasing demand rose ~8% in European IT procurement surveys.

Bechtle Financial Services expands flexible credit and leasing options, helping convert capex projects into service-based revenue and sustaining deal flow.

Currency Exchange Rate Volatility

As an international IT reseller, Bechtle faces currency exchange volatility—hardware procured in USD and sold in EUR can compress gross margins; a 10% USD appreciation versus EUR in 2024 would have raised COGS materially for e‑commerce sales.

The firm uses hedging (forwards/options) and natural hedges via local sourcing, but extreme swings in 2023–2025 FX markets remain a downside risk to consolidated EBIT.

- 2024 FX: EUR/USD averaged ~1.09; 2023 saw swings >8% intra‑year

- Hedging in place, but residual exposure affects e‑commerce gross margin

Labor Market Shortages

The scarcity of qualified IT specialists in Europe has pushed median IT salaries up about 8–12% in 2024, raising Bechtle’s recruitment and contractor costs and slowing expansion of its services arm.

Intense competition for talent forces Bechtle to increase training and retention spending—HR costs rose ~6% YoY in 2024—creating an economic bottleneck that constrains the company’s ability to meet growing customer demand.

- Qualified IT shortage raises recruitment/contractor costs ~8–12%

- HR/training spend up ~6% YoY (2024)

- Talent shortfall limits services scaling and fulfillment speed

Moderate DACH growth, rising IT wages and ECB rates squeeze margins—leasing and hedging up

Moderate DACH/EU growth (Germany GDP +0.5% 2024; euro area +0.6%) constrains big IT spend while EU ICT budgets +3% support public demand; inflation eased to 3.4% (2025) but wage growth 4–6%/IT median +8–12% (2024) squeezes margins; ECB rate 4.00% (Dec 2024) raises financing costs, boosting leasing/Daas uptake; EUR/USD ~1.09 (2024) creates FX risk mitigated by hedging.

| Metric | Value |

|---|---|

| Germany GDP 2024 | +0.5% |

| Euro area GDP 2024 | +0.6% |

| Eurozone HICP 2025 | 3.4% |

| ECB deposit rate Dec 2024 | 4.00% |

| EUR/USD 2024 avg | ~1.09 |

| IT salary rise 2024 | 8–12% |

Full Version Awaits

Bechtle PESTLE Analysis

The preview shown here is the exact Bechtle PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

What you’re previewing is the actual file: the layout, content, and structure match the downloadable product exactly, with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a competitive advantage with our targeted PESTLE Analysis of Bechtle—uncover how political shifts, economic cycles, tech disruption, social trends, and regulatory pressures will shape its trajectory; ideal for investors and strategists. Purchase the full, ready-to-use report to access deep-dive insights, actionable risks/opportunities, and editable charts for immediate decision-making.

Political factors

EU Digital Sovereignty Initiatives

The EU's digital sovereignty drive boosts demand for localized cloud and EU-sourced IT infrastructure, benefiting Bechtle as customers favor regional suppliers; EU cloud market projected at €70–90bn by 2030 supports this shift. As governments cut reliance on non-EU tech, Bechtle is well-placed as a trusted partner for public sector digital transformation, already serving hundreds of public clients. Policy incentives are spurring investments in sovereign data centers and specialized software services across Europe, expanding addressable market and recurring revenue opportunities for Bechtle.

Public Sector Procurement Budgets

Bechtle's high exposure to public sector clients makes revenue sensitive to government spending cycles across Germany and Europe; public-sector sales accounted for about 48% of FY2024 revenue (€6.1bn of €12.7bn). By late 2025, increased defense budgets—Germany's defense spending rose to ~2.5% of GDP in 2024—and administrative IT modernization projects are primary IT procurement drivers. Political shifts toward national security and infrastructure resilience directly affect the pipeline and scale of large tenders available to Bechtle.

Geopolitical Trade Tensions

Ongoing trade disputes and export controls—notably 2024 restrictions on advanced chips from China and periodic US-EU measures—have increased lead times for servers and network gear by up to 25%, complicating Bechtle’s global IT supply chain. Political bans on specific vendors for critical infrastructure force Bechtle to pivot procurement and consulting approaches, affecting margin and vendor mix. Managing these geopolitical risks is essential to ensure hardware availability and meet compliance for regulated clients.

European Defense and Security Policy

The EU increased defense spending to an estimated 2.2% of GDP in 2024 across member states, boosting cybersecurity and military IT budgets; Bechtle captures this via sales of secure servers, encrypted communication systems and certified endpoint solutions to defense agencies.

Political alignment on cross-border security initiatives—NATO-EU cooperation and Permanent Structured Cooperation (PESCO) projects—creates multi-year procurement pipelines; Bechtle reported 9% growth in public sector IT revenue in FY 2024, reflecting this demand.

- EU defense spend ~2.2% of GDP (2024)

- Bechtle public sector IT revenue growth 9% FY2024

- Stable multi-year contracts from PESCO/NATO collaborations

Digitalization of Government Services

- Public IT spend ~€45.6bn (2023)

- Bechtle public-sector revenue ~€1.1bn (2024)

- OZG-driven demand across federal/state/municipal levels

Bechtle cashes in on EU digital sovereignty—public IT fuels growth despite longer lead times

EU digital sovereignty and rising defense/administrative IT budgets drive demand for Bechtle’s localized cloud, secure infrastructure and public-sector services; public-sector revenue ~48% of FY2024 (€6.1bn of €12.7bn) with 9% public IT growth in 2024. Supply-chain controls and export restrictions lengthen lead times ~25%, affecting margins and vendor mix.

| Metric | Value |

|---|---|

| FY2024 revenue | €12.7bn |

| Public-sector share | 48% (€6.1bn) |

| Public IT growth 2024 | 9% |

| Lead-time increase | ~25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bechtle across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, PESTLE-segmented summary of Bechtle’s external environment that can be dropped into presentations or shared across teams for rapid alignment during strategy and risk discussions.

Economic factors

European Economic Growth Trends

Economic growth in the DACH region and EU influences Bechtle’s medium-sized clients; Eurostat GDP data show Germany grew 0.5% in 2024 and euro area 0.6%, constraining large IT spends. Public sector demand remains stable, supported by 2024 EU ICT budgets up 3%, while private IT spending closely tracks industrial production, which rose 1.2% in Germany in 2024. By end-2025, cautious recovery sees firms favoring efficiency-focused software and services over major hardware refresh cycles.

Inflationary Pressure and Cost Management

Persistent inflation—Eurozone HICP at 3.4% in 2025 vs 7.2% in 2022—pushes Bechtle to tighten pricing and cut costs; FY2024 gross margin of 21.6% and operating margin of 5.4% show limited buffer, so wage inflation for skilled IT staff (German average IT salary growth ~4–6% in 2024–25) risks squeezing margins unless service rates rise.

Interest Rate Environment

The 2024 euro-area rate hiking cycle—ECB deposit rate at 4.00% (Dec 2024)—raises Bechtle’s weighted average cost of capital, increasing acquisition financing costs and pressuring margins on large deals.

Higher rates shift customer preference toward leasing and Device-as-a-Service; in 2024 leasing demand rose ~8% in European IT procurement surveys.

Bechtle Financial Services expands flexible credit and leasing options, helping convert capex projects into service-based revenue and sustaining deal flow.

Currency Exchange Rate Volatility

As an international IT reseller, Bechtle faces currency exchange volatility—hardware procured in USD and sold in EUR can compress gross margins; a 10% USD appreciation versus EUR in 2024 would have raised COGS materially for e‑commerce sales.

The firm uses hedging (forwards/options) and natural hedges via local sourcing, but extreme swings in 2023–2025 FX markets remain a downside risk to consolidated EBIT.

- 2024 FX: EUR/USD averaged ~1.09; 2023 saw swings >8% intra‑year

- Hedging in place, but residual exposure affects e‑commerce gross margin

Labor Market Shortages

The scarcity of qualified IT specialists in Europe has pushed median IT salaries up about 8–12% in 2024, raising Bechtle’s recruitment and contractor costs and slowing expansion of its services arm.

Intense competition for talent forces Bechtle to increase training and retention spending—HR costs rose ~6% YoY in 2024—creating an economic bottleneck that constrains the company’s ability to meet growing customer demand.

- Qualified IT shortage raises recruitment/contractor costs ~8–12%

- HR/training spend up ~6% YoY (2024)

- Talent shortfall limits services scaling and fulfillment speed

Moderate DACH growth, rising IT wages and ECB rates squeeze margins—leasing and hedging up

Moderate DACH/EU growth (Germany GDP +0.5% 2024; euro area +0.6%) constrains big IT spend while EU ICT budgets +3% support public demand; inflation eased to 3.4% (2025) but wage growth 4–6%/IT median +8–12% (2024) squeezes margins; ECB rate 4.00% (Dec 2024) raises financing costs, boosting leasing/Daas uptake; EUR/USD ~1.09 (2024) creates FX risk mitigated by hedging.

| Metric | Value |

|---|---|

| Germany GDP 2024 | +0.5% |

| Euro area GDP 2024 | +0.6% |

| Eurozone HICP 2025 | 3.4% |

| ECB deposit rate Dec 2024 | 4.00% |

| EUR/USD 2024 avg | ~1.09 |

| IT salary rise 2024 | 8–12% |

Full Version Awaits

Bechtle PESTLE Analysis

The preview shown here is the exact Bechtle PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

What you’re previewing is the actual file: the layout, content, and structure match the downloadable product exactly, with no placeholders or surprises.