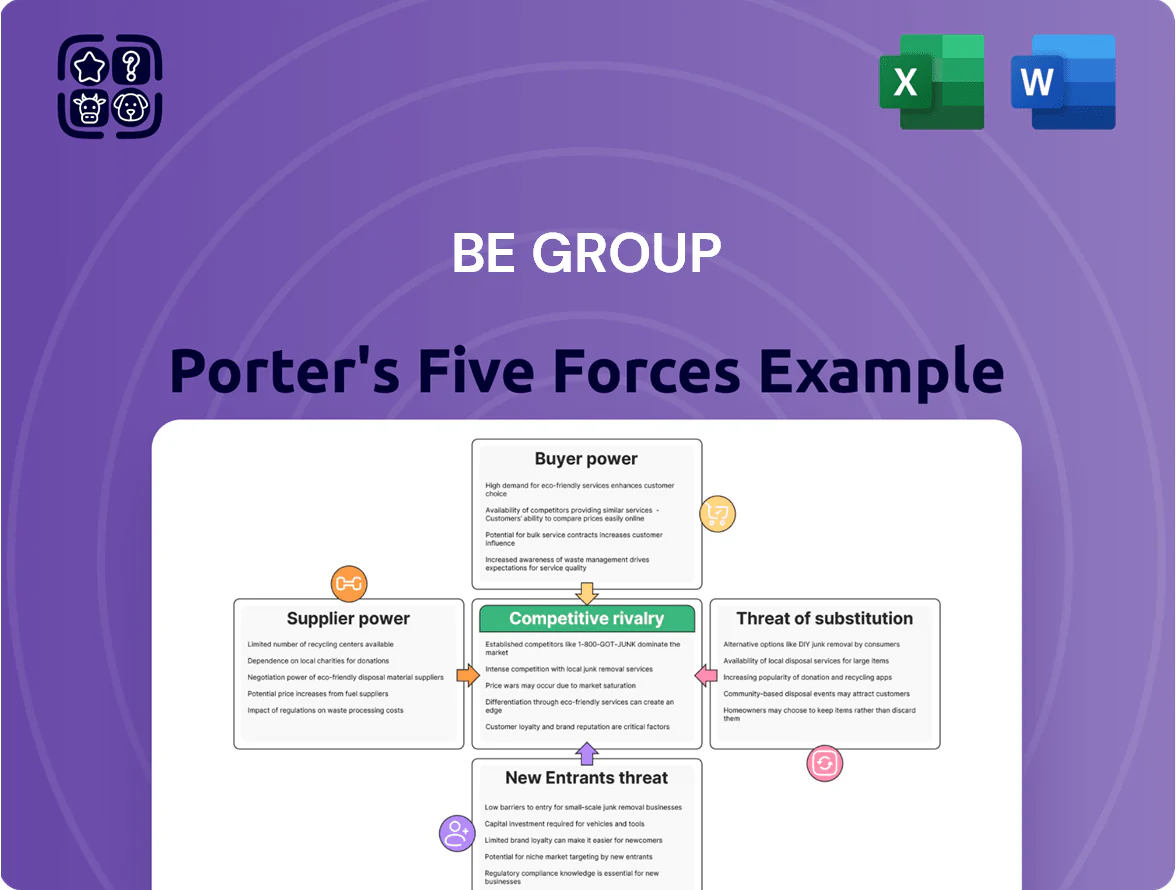

BE Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

BE Group faces moderate buyer power, steady supplier relationships, and niche competition that keeps margins under pressure; regulatory and substitution risks are manageable but require vigilance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore BE Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global Steel Producers

The upstream market is concentrated among a few large mills—SSAB and ArcelorMittal account for roughly 25–30% of European flat steel capacity in 2025—limiting BE Group’s ability to push for lower purchase prices.

These producers control supply volumes and can set terms when global demand shifts; ArcelorMittal reported 2024 crude steel output of ~55 Mt, giving it pricing power.

Post-2023 European consolidation raised supplier leverage over regional traders: fewer players mean BE Group faces higher input-cost pass-through risk and tighter contract terms.

Transition to Green and Fossil-Free Steel

As Europe shifts to low-carbon steel, suppliers of green steel (hydrogen-reduced or EAF with renewables) gain pricing power due to scarcity; European low-CO2 steel premiums reached ~€120–€200/ton in 2024 versus brown steel.

Demand in Northern Europe outpaced supply in 2024—EU emissions-compliant procurement rose 18% YoY—letting mills command higher margins.

BE Group must secure long-term contracts and strategic partnerships with certified green mills to meet customer ESG specs and avoid supply-driven margin compression.

Volatility of Raw Material and Energy Inputs

Suppliers pass iron ore, scrap and energy cost swings to traders; in 2025 European gas price volatility (TTF averaging ~35–50 EUR/MWh YTD) lifted stainless and aluminum spot prices by ~12% YoY, shrinking trading margins.

BE Group, with negligible commodity hedging power and ~5–7% trading margin historically, functions as a price taker against OECD-integrated global pricing mechanisms.

Supply Chain Logistics and Lead Times

Supply chain reliability from primary producers directly affects BE Group service centers; 2024 industry data show European mill on-time delivery rates fell to ~78%, raising stockout risk and expediting costs.

Disruptions at major mills force BE Group to hold higher safety stock—adding 1–3% to working capital—and can trigger supplier-imposed tighter credit and 10–20% stricter lead-time penalties for specialty beams and high‑grade sheets.

- 78% on-time delivery (2024)

- 1–3% extra working capital

- 10–20% stricter terms for specialized items

Impact of Trade Barriers and Import Quotas

EU safeguard tariffs and anti-dumping measures on steel (eg, 2023‑2025 provisional tariffs up to 25%) limit non‑EU suppliers to BE Group, protecting EU mills and enabling ~5–10% higher domestic steel prices versus global benchmarks in 2024.

That regulatory barrier shrinks BE Group’s supplier pool, raising supplier concentration and bargaining power of local producers, which can press for firmer prices and tighter terms.

- EU tariffs up to 25% (2023–25)

- Domestic prices ~5–10% above global levels (2024)

- Smaller supplier pool → higher supplier leverage

Mill pricing power, tariffs and low‑CO2 premiums squeeze BE Group margins and working capital

Supplier concentration (SSAB, ArcelorMittal ~25–30% EU flat steel capacity, 2025) and EU tariffs (up to 25% 2023–25) give mills pricing power; low‑CO2 steel premium €120–€200/t (2024) and on‑time delivery 78% (2024) raise BE Group’s sourcing costs, working capital (+1–3%) and contract risk.

| Metric | Value |

|---|---|

| Top‑mill share | 25–30% (2025) |

| Low‑CO2 premium | €120–€200/t (2024) |

| On‑time delivery | 78% (2024) |

| Working capital impact | +1–3% |

| EU tariffs | Up to 25% (2023–25) |

What is included in the product

Tailored Porter’s Five Forces analysis for BE Group that uncovers competitive dynamics, buyer and supplier power, entry barriers, substitutes, and emerging threats, supported by industry insights to inform strategic decisions and investor materials.

A concise Porter's Five Forces one-sheet for BE Group—instantly highlights competitive pressures and strategic levers to speed boardroom decisions.

Customers Bargaining Power

Cyclicality of Construction and Manufacturing Sectors

Demand for BE Group’s steel and metal products tracks construction and manufacturing activity in Northern and Eastern Europe, so downturns cut orders and boost buyer leverage; EU construction output fell 2.3% y/y in H1 2024, raising negotiation pressure. During slow periods customers push for price cuts and longer payment terms, squeezing BE Group’s margins. In 2025 sensitivity to ECB policy remains key: a 1 percentage-point rise in rates historically trims investment in construction ~3–4%, amplifying buyer power.

Price Sensitivity in Commodity Steel Markets

In commodity steel segments like basic tubes and bars, buyers treat products as interchangeable and switch distributors mainly on price, pushing BE Group to match market rates; Swedish steel distribution margins fell to about 3–6% in 2024 for commoditized SKUs, per industry reports.

Customization through Production Services

Customers needing precision cutting, drilling, and surface treatment at BE Group face reduced bargaining power because these advanced services raise complexity and limit supplier options; in 2024 BE Group reported 22% of revenue from value-added services, showing this shift.

Availability of Alternative Distribution Channels

The rise of digital procurement platforms and direct-to-customer steel sales gives buyers more options; global digital steel trade grew ~18% in 2024, letting large manufacturers bypass distributors for bulk orders.

That shift pushes BE Group toward mid-sized or specialized contracts, raising the need for superior logistics and local stock — BE Group reported SEK 9.2bn revenue in 2024, so margin pressure matters.

Availability of diverse channels forces BE Group to compete on speed, local availability, and value-added services to retain clients.

- Digital steel trade +18% in 2024

- Large firms buy direct, bypassing distributors

- BE Group 2024 revenue SEK 9.2bn

- Compete on logistics, local stock, services

Digitalization and Transparency in Pricing

In 2025, widespread digital price-tracking tools give buyers real-time visibility into global steel prices, and customers demand immediate cuts when iron ore and scrap prices fall—iron ore spot fell ~28% year-on-year through 2024, so buyers push hard.

That transparency raises customers’ bargaining power; BE Group must shift pricing within weeks to retain loyalty while defending margins—gross margin was 7–9% in 2024 for Nordic steel distributors, so small swings matter.

Fast, data-driven pricing, tighter hedges, and short-term contracts are needed to respond to price signals without eroding EBITDA.

- Real-time price visibility up ~65% user adoption in procurement tools (2024)

Buyers Gain Edge: Digital Procurement, Low Iron Ore Drive Margin Pressure on BE Group

Buyers have high leverage: construction downturns and digital procurement raise price pressure; BE Group SEK 9.2bn revenue (2024), Nordic distributor gross margins 7–9% (2024). Value-added services (22% revenue, 2024) reduce buyer power for specialized SKUs. Real-time price tools adoption ~65% (2024); iron ore spot -28% y/y (2024) increases demand for rapid price cuts.

| Metric | 2024 |

|---|---|

| Revenue | SEK 9.2bn |

| VAS share | 22% |

| Gross margin range | 7–9% |

| Digital procurement adoption | 65% |

| Iron ore spot change | -28% y/y |

What You See Is What You Get

BE Group Porter's Five Forces Analysis

This preview shows the exact BE Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples, fully formatted and ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

BE Group faces moderate buyer power, steady supplier relationships, and niche competition that keeps margins under pressure; regulatory and substitution risks are manageable but require vigilance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore BE Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global Steel Producers

The upstream market is concentrated among a few large mills—SSAB and ArcelorMittal account for roughly 25–30% of European flat steel capacity in 2025—limiting BE Group’s ability to push for lower purchase prices.

These producers control supply volumes and can set terms when global demand shifts; ArcelorMittal reported 2024 crude steel output of ~55 Mt, giving it pricing power.

Post-2023 European consolidation raised supplier leverage over regional traders: fewer players mean BE Group faces higher input-cost pass-through risk and tighter contract terms.

Transition to Green and Fossil-Free Steel

As Europe shifts to low-carbon steel, suppliers of green steel (hydrogen-reduced or EAF with renewables) gain pricing power due to scarcity; European low-CO2 steel premiums reached ~€120–€200/ton in 2024 versus brown steel.

Demand in Northern Europe outpaced supply in 2024—EU emissions-compliant procurement rose 18% YoY—letting mills command higher margins.

BE Group must secure long-term contracts and strategic partnerships with certified green mills to meet customer ESG specs and avoid supply-driven margin compression.

Volatility of Raw Material and Energy Inputs

Suppliers pass iron ore, scrap and energy cost swings to traders; in 2025 European gas price volatility (TTF averaging ~35–50 EUR/MWh YTD) lifted stainless and aluminum spot prices by ~12% YoY, shrinking trading margins.

BE Group, with negligible commodity hedging power and ~5–7% trading margin historically, functions as a price taker against OECD-integrated global pricing mechanisms.

Supply Chain Logistics and Lead Times

Supply chain reliability from primary producers directly affects BE Group service centers; 2024 industry data show European mill on-time delivery rates fell to ~78%, raising stockout risk and expediting costs.

Disruptions at major mills force BE Group to hold higher safety stock—adding 1–3% to working capital—and can trigger supplier-imposed tighter credit and 10–20% stricter lead-time penalties for specialty beams and high‑grade sheets.

- 78% on-time delivery (2024)

- 1–3% extra working capital

- 10–20% stricter terms for specialized items

Impact of Trade Barriers and Import Quotas

EU safeguard tariffs and anti-dumping measures on steel (eg, 2023‑2025 provisional tariffs up to 25%) limit non‑EU suppliers to BE Group, protecting EU mills and enabling ~5–10% higher domestic steel prices versus global benchmarks in 2024.

That regulatory barrier shrinks BE Group’s supplier pool, raising supplier concentration and bargaining power of local producers, which can press for firmer prices and tighter terms.

- EU tariffs up to 25% (2023–25)

- Domestic prices ~5–10% above global levels (2024)

- Smaller supplier pool → higher supplier leverage

Mill pricing power, tariffs and low‑CO2 premiums squeeze BE Group margins and working capital

Supplier concentration (SSAB, ArcelorMittal ~25–30% EU flat steel capacity, 2025) and EU tariffs (up to 25% 2023–25) give mills pricing power; low‑CO2 steel premium €120–€200/t (2024) and on‑time delivery 78% (2024) raise BE Group’s sourcing costs, working capital (+1–3%) and contract risk.

| Metric | Value |

|---|---|

| Top‑mill share | 25–30% (2025) |

| Low‑CO2 premium | €120–€200/t (2024) |

| On‑time delivery | 78% (2024) |

| Working capital impact | +1–3% |

| EU tariffs | Up to 25% (2023–25) |

What is included in the product

Tailored Porter’s Five Forces analysis for BE Group that uncovers competitive dynamics, buyer and supplier power, entry barriers, substitutes, and emerging threats, supported by industry insights to inform strategic decisions and investor materials.

A concise Porter's Five Forces one-sheet for BE Group—instantly highlights competitive pressures and strategic levers to speed boardroom decisions.

Customers Bargaining Power

Cyclicality of Construction and Manufacturing Sectors

Demand for BE Group’s steel and metal products tracks construction and manufacturing activity in Northern and Eastern Europe, so downturns cut orders and boost buyer leverage; EU construction output fell 2.3% y/y in H1 2024, raising negotiation pressure. During slow periods customers push for price cuts and longer payment terms, squeezing BE Group’s margins. In 2025 sensitivity to ECB policy remains key: a 1 percentage-point rise in rates historically trims investment in construction ~3–4%, amplifying buyer power.

Price Sensitivity in Commodity Steel Markets

In commodity steel segments like basic tubes and bars, buyers treat products as interchangeable and switch distributors mainly on price, pushing BE Group to match market rates; Swedish steel distribution margins fell to about 3–6% in 2024 for commoditized SKUs, per industry reports.

Customization through Production Services

Customers needing precision cutting, drilling, and surface treatment at BE Group face reduced bargaining power because these advanced services raise complexity and limit supplier options; in 2024 BE Group reported 22% of revenue from value-added services, showing this shift.

Availability of Alternative Distribution Channels

The rise of digital procurement platforms and direct-to-customer steel sales gives buyers more options; global digital steel trade grew ~18% in 2024, letting large manufacturers bypass distributors for bulk orders.

That shift pushes BE Group toward mid-sized or specialized contracts, raising the need for superior logistics and local stock — BE Group reported SEK 9.2bn revenue in 2024, so margin pressure matters.

Availability of diverse channels forces BE Group to compete on speed, local availability, and value-added services to retain clients.

- Digital steel trade +18% in 2024

- Large firms buy direct, bypassing distributors

- BE Group 2024 revenue SEK 9.2bn

- Compete on logistics, local stock, services

Digitalization and Transparency in Pricing

In 2025, widespread digital price-tracking tools give buyers real-time visibility into global steel prices, and customers demand immediate cuts when iron ore and scrap prices fall—iron ore spot fell ~28% year-on-year through 2024, so buyers push hard.

That transparency raises customers’ bargaining power; BE Group must shift pricing within weeks to retain loyalty while defending margins—gross margin was 7–9% in 2024 for Nordic steel distributors, so small swings matter.

Fast, data-driven pricing, tighter hedges, and short-term contracts are needed to respond to price signals without eroding EBITDA.

- Real-time price visibility up ~65% user adoption in procurement tools (2024)

Buyers Gain Edge: Digital Procurement, Low Iron Ore Drive Margin Pressure on BE Group

Buyers have high leverage: construction downturns and digital procurement raise price pressure; BE Group SEK 9.2bn revenue (2024), Nordic distributor gross margins 7–9% (2024). Value-added services (22% revenue, 2024) reduce buyer power for specialized SKUs. Real-time price tools adoption ~65% (2024); iron ore spot -28% y/y (2024) increases demand for rapid price cuts.

| Metric | 2024 |

|---|---|

| Revenue | SEK 9.2bn |

| VAS share | 22% |

| Gross margin range | 7–9% |

| Digital procurement adoption | 65% |

| Iron ore spot change | -28% y/y |

What You See Is What You Get

BE Group Porter's Five Forces Analysis

This preview shows the exact BE Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples, fully formatted and ready for use.