BEKB-BCBE Business Model Canvas

BEKB-BCBE Business Model Canvas: How the Bank Creates Value & Profits

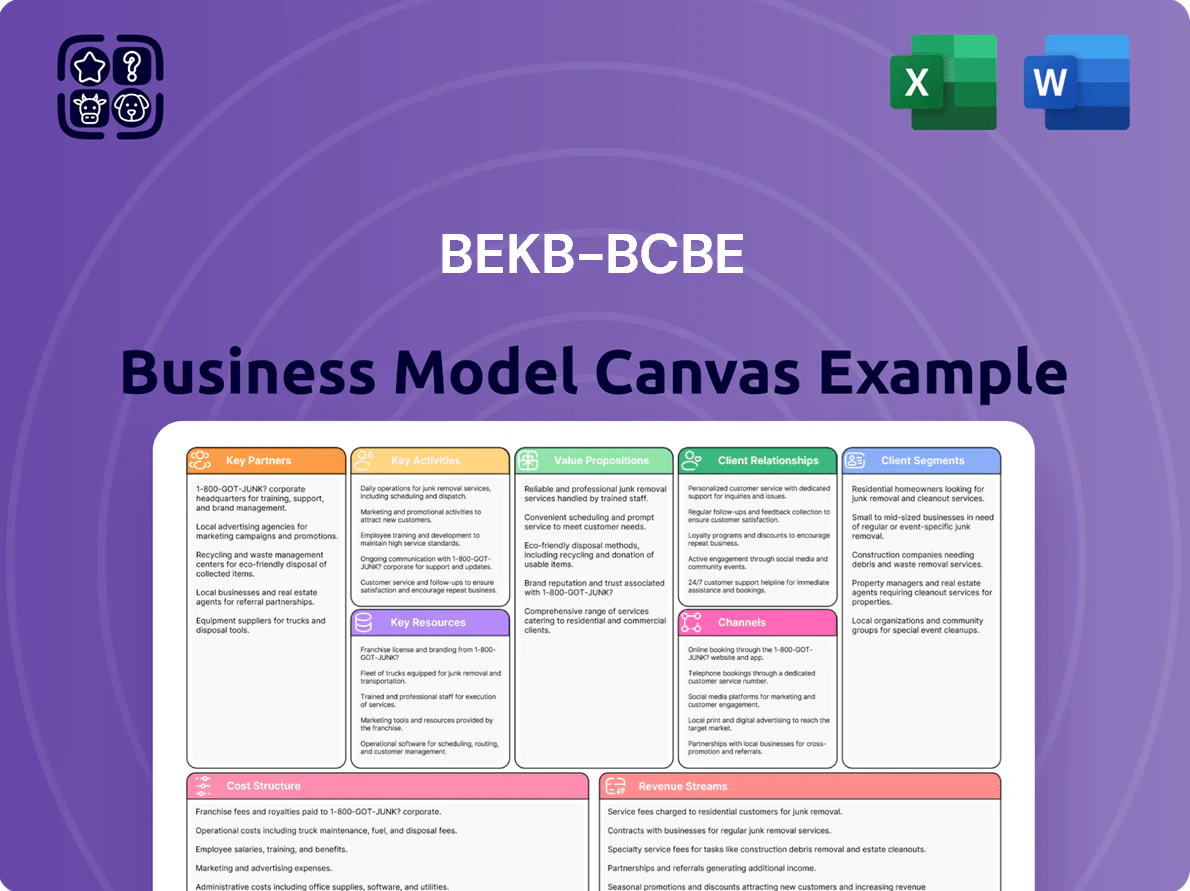

Unlock the full strategic blueprint behind BEKB-BCBE’s business model—this concise Business Model Canvas reveals how the bank creates customer value, monetizes services, and sustains competitive advantage across retail and commercial segments.

Partnerships

Canton of Bern State Guarantee

The Canton of Bern is anchor shareholder and provides a statutory state guarantee for BEKB-BCBE liabilities, underpinning depositor trust and a top-tier Swiss credit rating (Aa2/A+ range as of Dec 31, 2025).

This guarantee supports low-cost refinancing—net interest expense ~15–25 bps lower versus peers—and remains central to regional stability and access to CHF liquidity markets through 2025.

Finnova Banking Software Integration

Finnova supplies BEKB-BCBE with the core banking engine that runs payments, lending, and deposits, enabling automation that cut back-office processing time by ~35% and reduced operational costs by ~18% in 2024. The integration supports continuous digital-suite updates and helps the bank meet 2025 cybersecurity mandates (SWIFT CSP alignment and ISO 27001 controls), keeping system uptime above 99.95%.

Swiss Cantonal Banks Network

Through the Association of Swiss Cantonal Banks BEKB-BCBE shares costs and clout with 24 cantonal banks, supporting joint payment platforms, pension solutions and a 2,500+ ATM network; in 2024 cantonal-bank cooperation handled ~CHF 45bn in collective payment volumes and cut unit costs by an estimated 12%, letting BEKB offer national services while keeping its Bern mandate.

Strategic Fintech and Startup Alliances

By 2025 BEKB-BCBE partners with ~25 fintechs, integrating robo-advisory and digital mortgage processing to speed product rollout and cut internal dev costs by an estimated 40% vs in-house builds.

Since 2023 alliances now include sustainable finance platforms that track portfolio carbon footprints, covering ~15% of AUM (~CHF 3.2bn) and supporting SFDR-aligned reporting.

- ~25 fintech partners

- 40% estimated dev cost savings

- ~15% AUM tracked for carbon (~CHF 3.2bn)

Insurance and Real Estate Service Providers

The bank partners with insurers and local real estate agencies to cross-sell mortgage insurance and provide property valuations, driving a 12% increase in mortgage-linked fee income in 2024 and reducing default loss given default by ~0.4 percentage points.

The ecosystem delivers integrated advice across banking, protection, and property, shortening mortgage processing times by 18% and raising customer NPS; partners cover ~70% of Swiss cantonal markets.

- 12% jump in mortgage fee income (2024)

- 0.4 pp lower loss given default

- 18% faster mortgage processing

- Partners span ~70% of cantons

Bern-backed fintech network cuts costs, speeds mortgages, boosts fees & tracks CHF3.2bn carbon

The Canton of Bern guarantor status and Finnova core banking, plus cantonal-bank cooperation, ~25 fintechs, insurers and real-estate partners, jointly reduce funding costs (~15–25 bps), cut ops costs (~18%), speed mortgage processing (−18%), lift mortgage fee income (+12% in 2024) and track ~15% AUM for carbon (~CHF 3.2bn).

| Metric | Value (2024–25) |

|---|---|

| Funding spread benefit | 15–25 bps |

| Ops cost reduction | ~18% |

| Mortgage fee income | +12% |

| Mortgage processing | −18% |

| Fintech partners | ~25 |

| AUM tracked for carbon | ~15% (CHF 3.2bn) |

What is included in the product

A practical, pre-written Business Model Canvas for BEKB-BCBE detailing customer segments, channels, value propositions, revenue streams and key resources across the nine BMC blocks, with competitive analysis, SWOT-linked insights and real-world operational context to support presentations, funding discussions and strategic decision-making.

Condenses BEKB-BCBE’s strategy into a digestible one-page Business Model Canvas, saving hours of formatting while enabling quick comparison, team collaboration, and rapid executive summaries.

Activities

Mortgage and Credit Financing

The primary activity is originating and managing mortgages for private homeowners and credit lines for local SMEs, with a loan book of CHF 22.4 billion at end‑2024; risk models (PD/LGD) keep nonperforming loans near 0.9%. In 2025 BEKB-BCBE shifts lending toward energy-efficient renovations and sustainable construction, targeting CHF 400–600 million in green loans and aiming to cut portfolio CO2 intensity by 25% by 2030.

Asset Management and Investment Advisory

BEKB-BCBE manages about CHF 28.4 billion in client assets (2025), focusing on long-term capital preservation and targeted growth; advisors perform quarterly portfolio reviews and tailor strategies to risk profiles and market conditions, aiming for a 4–6% annual real return for balanced mandates. This includes proprietary funds (~CHF 3.1bn) and curated third-party instruments, with active fund selection and compliance-driven due diligence.

Digital Banking Platform Development

Continuous improvement of BEKB-BCBE’s mobile app and online portal is core: the bank reported 62% digital active customers in 2024 and invests ~CHF 45m annually in UX and platform upgrades to support 24/7 access. Integrating instant payments and digital wallets, while keeping a secure, intuitive interface, cuts churn and scales operations—incident rate under 0.02% in 2024 and app NPS of 38.

Risk Management and Regulatory Compliance

- AML screening: ~1.2M checks/year

- CET1 ratio: 14.2% (2025)

- AI automation reduced reviews 45%

- Real-time alerts: latency <60s

Corporate Advisory and Succession Planning

The bank offers corporate advisory and succession planning to SMEs in the Canton of Bern, guiding business expansion and ownership transitions; in 2024 BEKB advised on 112 succession cases, preserving estimated CHF 480m in local revenues.

Advisors co-structure financing and corporate restructurings—47% of engagements in 2024 included tailored loan packages averaging CHF 1.2m per deal, reducing failure risk for family firms.

- 112 succession cases advised (2024)

- CHF 480m estimated preserved local revenues

- 47% engagements included tailored loans

- Average loan size CHF 1.2m

CHF 22.4bn loan book, CHF 28.4bn AUM — targeting CHF 400–600m green loans & −25% CO2

Originate/manage mortgages & SME credit (loan book CHF 22.4bn end‑2024; NPL ~0.9%); target CHF 400–600m green loans in 2025 and −25% CO2 intensity by 2030. Manage CHF 28.4bn client assets (2025) with CHF 3.1bn proprietary funds; aim 4–6% real return. Digital: 62% active users (2024), CHF 45m capex, app NPS 38; AML ~1.2M checks/yr, CET1 14.2% (2025), AI cut reviews 45%.

| Metric | Value |

|---|---|

| Loan book | CHF 22.4bn (2024) |

| Client assets | CHF 28.4bn (2025) |

| Green loans target | CHF 400–600m (2025) |

| CET1 | 14.2% (2025) |

| App users | 62% active (2024) |

Delivered as Displayed

Business Model Canvas

The preview you see is the exact BEKB-BCBE Business Model Canvas you’ll receive after purchase—not a sample or mockup—and it’s fully formatted and ready to use. Upon completing your order, you’ll get this same document in its complete form, editable and downloadable for presentation or analysis. What you see is what you’ll own—no surprises, just the full, professional deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

BEKB-BCBE Business Model Canvas: How the Bank Creates Value & Profits

Unlock the full strategic blueprint behind BEKB-BCBE’s business model—this concise Business Model Canvas reveals how the bank creates customer value, monetizes services, and sustains competitive advantage across retail and commercial segments.

Partnerships

Canton of Bern State Guarantee

The Canton of Bern is anchor shareholder and provides a statutory state guarantee for BEKB-BCBE liabilities, underpinning depositor trust and a top-tier Swiss credit rating (Aa2/A+ range as of Dec 31, 2025).

This guarantee supports low-cost refinancing—net interest expense ~15–25 bps lower versus peers—and remains central to regional stability and access to CHF liquidity markets through 2025.

Finnova Banking Software Integration

Finnova supplies BEKB-BCBE with the core banking engine that runs payments, lending, and deposits, enabling automation that cut back-office processing time by ~35% and reduced operational costs by ~18% in 2024. The integration supports continuous digital-suite updates and helps the bank meet 2025 cybersecurity mandates (SWIFT CSP alignment and ISO 27001 controls), keeping system uptime above 99.95%.

Swiss Cantonal Banks Network

Through the Association of Swiss Cantonal Banks BEKB-BCBE shares costs and clout with 24 cantonal banks, supporting joint payment platforms, pension solutions and a 2,500+ ATM network; in 2024 cantonal-bank cooperation handled ~CHF 45bn in collective payment volumes and cut unit costs by an estimated 12%, letting BEKB offer national services while keeping its Bern mandate.

Strategic Fintech and Startup Alliances

By 2025 BEKB-BCBE partners with ~25 fintechs, integrating robo-advisory and digital mortgage processing to speed product rollout and cut internal dev costs by an estimated 40% vs in-house builds.

Since 2023 alliances now include sustainable finance platforms that track portfolio carbon footprints, covering ~15% of AUM (~CHF 3.2bn) and supporting SFDR-aligned reporting.

- ~25 fintech partners

- 40% estimated dev cost savings

- ~15% AUM tracked for carbon (~CHF 3.2bn)

Insurance and Real Estate Service Providers

The bank partners with insurers and local real estate agencies to cross-sell mortgage insurance and provide property valuations, driving a 12% increase in mortgage-linked fee income in 2024 and reducing default loss given default by ~0.4 percentage points.

The ecosystem delivers integrated advice across banking, protection, and property, shortening mortgage processing times by 18% and raising customer NPS; partners cover ~70% of Swiss cantonal markets.

- 12% jump in mortgage fee income (2024)

- 0.4 pp lower loss given default

- 18% faster mortgage processing

- Partners span ~70% of cantons

Bern-backed fintech network cuts costs, speeds mortgages, boosts fees & tracks CHF3.2bn carbon

The Canton of Bern guarantor status and Finnova core banking, plus cantonal-bank cooperation, ~25 fintechs, insurers and real-estate partners, jointly reduce funding costs (~15–25 bps), cut ops costs (~18%), speed mortgage processing (−18%), lift mortgage fee income (+12% in 2024) and track ~15% AUM for carbon (~CHF 3.2bn).

| Metric | Value (2024–25) |

|---|---|

| Funding spread benefit | 15–25 bps |

| Ops cost reduction | ~18% |

| Mortgage fee income | +12% |

| Mortgage processing | −18% |

| Fintech partners | ~25 |

| AUM tracked for carbon | ~15% (CHF 3.2bn) |

What is included in the product

A practical, pre-written Business Model Canvas for BEKB-BCBE detailing customer segments, channels, value propositions, revenue streams and key resources across the nine BMC blocks, with competitive analysis, SWOT-linked insights and real-world operational context to support presentations, funding discussions and strategic decision-making.

Condenses BEKB-BCBE’s strategy into a digestible one-page Business Model Canvas, saving hours of formatting while enabling quick comparison, team collaboration, and rapid executive summaries.

Activities

Mortgage and Credit Financing

The primary activity is originating and managing mortgages for private homeowners and credit lines for local SMEs, with a loan book of CHF 22.4 billion at end‑2024; risk models (PD/LGD) keep nonperforming loans near 0.9%. In 2025 BEKB-BCBE shifts lending toward energy-efficient renovations and sustainable construction, targeting CHF 400–600 million in green loans and aiming to cut portfolio CO2 intensity by 25% by 2030.

Asset Management and Investment Advisory

BEKB-BCBE manages about CHF 28.4 billion in client assets (2025), focusing on long-term capital preservation and targeted growth; advisors perform quarterly portfolio reviews and tailor strategies to risk profiles and market conditions, aiming for a 4–6% annual real return for balanced mandates. This includes proprietary funds (~CHF 3.1bn) and curated third-party instruments, with active fund selection and compliance-driven due diligence.

Digital Banking Platform Development

Continuous improvement of BEKB-BCBE’s mobile app and online portal is core: the bank reported 62% digital active customers in 2024 and invests ~CHF 45m annually in UX and platform upgrades to support 24/7 access. Integrating instant payments and digital wallets, while keeping a secure, intuitive interface, cuts churn and scales operations—incident rate under 0.02% in 2024 and app NPS of 38.

Risk Management and Regulatory Compliance

- AML screening: ~1.2M checks/year

- CET1 ratio: 14.2% (2025)

- AI automation reduced reviews 45%

- Real-time alerts: latency <60s

Corporate Advisory and Succession Planning

The bank offers corporate advisory and succession planning to SMEs in the Canton of Bern, guiding business expansion and ownership transitions; in 2024 BEKB advised on 112 succession cases, preserving estimated CHF 480m in local revenues.

Advisors co-structure financing and corporate restructurings—47% of engagements in 2024 included tailored loan packages averaging CHF 1.2m per deal, reducing failure risk for family firms.

- 112 succession cases advised (2024)

- CHF 480m estimated preserved local revenues

- 47% engagements included tailored loans

- Average loan size CHF 1.2m

CHF 22.4bn loan book, CHF 28.4bn AUM — targeting CHF 400–600m green loans & −25% CO2

Originate/manage mortgages & SME credit (loan book CHF 22.4bn end‑2024; NPL ~0.9%); target CHF 400–600m green loans in 2025 and −25% CO2 intensity by 2030. Manage CHF 28.4bn client assets (2025) with CHF 3.1bn proprietary funds; aim 4–6% real return. Digital: 62% active users (2024), CHF 45m capex, app NPS 38; AML ~1.2M checks/yr, CET1 14.2% (2025), AI cut reviews 45%.

| Metric | Value |

|---|---|

| Loan book | CHF 22.4bn (2024) |

| Client assets | CHF 28.4bn (2025) |

| Green loans target | CHF 400–600m (2025) |

| CET1 | 14.2% (2025) |

| App users | 62% active (2024) |

Delivered as Displayed

Business Model Canvas

The preview you see is the exact BEKB-BCBE Business Model Canvas you’ll receive after purchase—not a sample or mockup—and it’s fully formatted and ready to use. Upon completing your order, you’ll get this same document in its complete form, editable and downloadable for presentation or analysis. What you see is what you’ll own—no surprises, just the full, professional deliverable.