Bell Techlogix Porter's Five Forces Analysis

Don't Miss the Bigger Picture

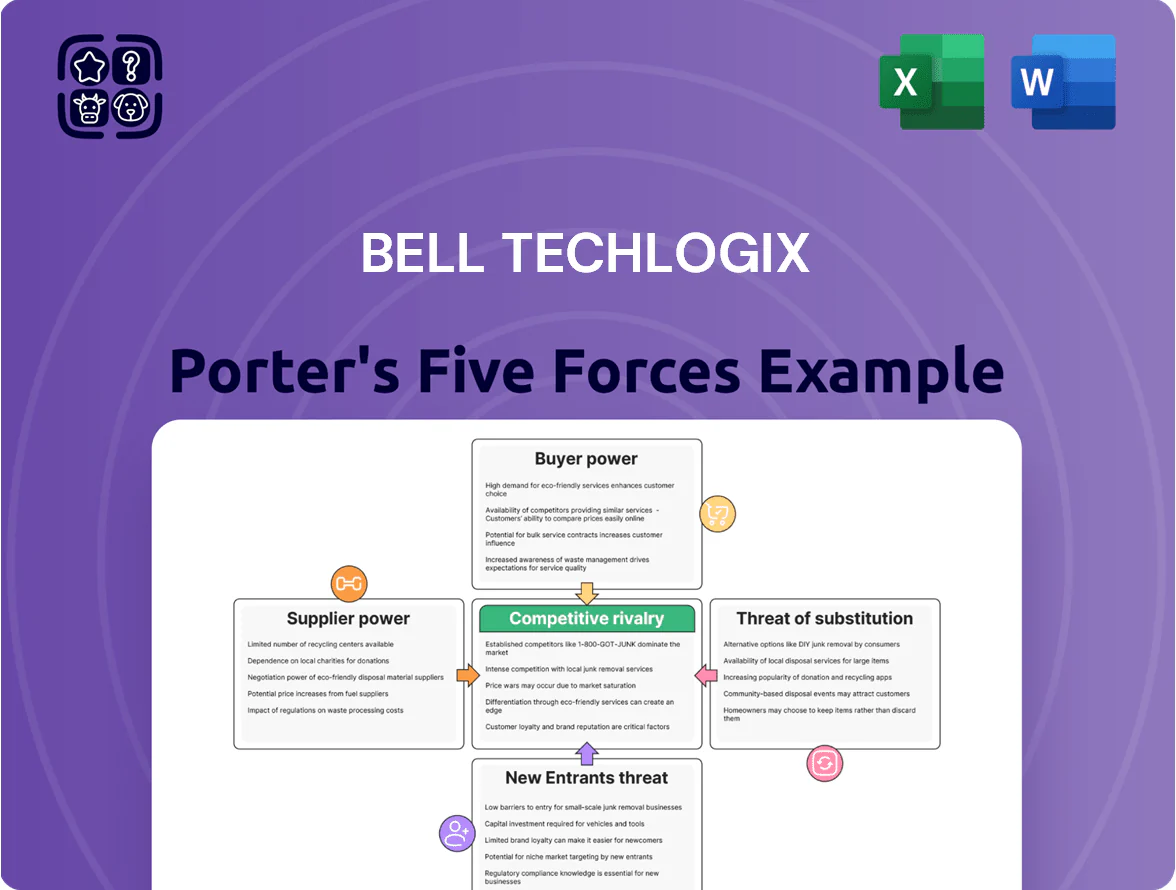

Bell Techlogix faces intense competitive rivalry from managed IT and MSP firms, moderate buyer power driven by corporate procurement, constrained supplier influence, low threat from substitutes but evolving tech risks, and a moderate threat of new entrants due to scale and certifications; this snapshot highlights key pressures shaping margins and strategy.

Suppliers Bargaining Power

Dependence on Cloud Hyperscalers

Bell Techlogix depends on AWS, Microsoft Azure, and Google Cloud for core services; these three held about 66% of global cloud IaaS/PaaS market in 2024 (AWS 32%, Azure 24%, Google 10%), giving them pricing and contract leverage over smaller integrators.

Supplier price changes flow straight to Bell Techlogix margins: a 10% cloud price rise would roughly add 3–6% to service COGS based on typical cloud cost shares in MSPs, squeezing EBITDA unless passed to clients.

Hardware OEM Relationships

Hardware OEM relationships matter because Bell Techlogix depends on steady supplies from Dell, HP, and Lenovo; in 2024 these three controlled ~60% of global PC shipments, so their pricing and availability directly affect enterprise deployments.

These OEMs wield power via brand trust and certified support contracts, making switches costly; Gartner reported 2024 enterprise support premiums rising ~8%, increasing Bell Techlogix procurement costs if OEM terms tighten.

Supply-chain shocks matter: semiconductor and logistics disruptions in 2021–22 pushed component lead times from 4 to 20+ weeks; a recurrence would force Bell Techlogix to change service SLAs or hold higher inventory, tying up working capital.

Specialized Cybersecurity Software Vendors

Specialized cybersecurity vendors supply the advanced software Bell Techlogix needs for high-tier services, and vendors’ deep integration creates high switching costs—often 12–18 months and $200k+ in migration and retraining for enterprise clients. These suppliers use tiered pricing and mandatory update cycles; in 2024 top endpoint vendors raised enterprise list prices by ~6–9%, squeezing margins Bell Techlogix must pass to customers.

Scarcity of Specialized IT Talent

In late 2025, specialized AI and cloud architects are scarce: LinkedIn data shows global demand up 42% year-over-year and average cloud architect salaries rose to about $160,000 in the US by 2025, boosting supplier power.

Bell Techlogix faces high turnover risk and must offer premium pay, signing bonuses, and benefits—adding 15–25% to labor costs—to meet managed-services SLAs and retain critical engineers.

- Demand +42% YoY (LinkedIn, 2025)

- Avg cloud architect pay ≈ $160,000 (US, 2025)

- Retention premium 15–25% on labor costs

Data Center and Connectivity Providers

Data center and telco giants like Equinix, Digital Realty, AT&T and Verizon control much of the internet backbone, leaving managed-service firms such as Bell Techlogix with limited regional alternatives; Equinix reported 228 data centers and $8.1B revenue in 2024, showing concentration.

These suppliers set SLAs and bandwidth pricing—wholesale bandwidth prices rose ~12% in 2023–2024 in parts of North America—directly driving Bell Techlogix’s cost of service and margin pressure.

What this estimate hides: localized monopoly power can force multi-year contracts, making switching costly and slow.

- High concentration: top 5 DC operators control ~40% global colocation capacity (2024)

- Revenue impact: carrier costs up ~12% (2023–24) in key markets

- Contract lock-in: multi-year SLAs common, switching friction high

Supplier Dominance: Cloud, OEMs, Data Centers & Talent Drive Costs for Bell Techlogix

Suppliers hold strong leverage over Bell Techlogix: top cloud providers (AWS 32%, Azure 24%, Google 10% of IaaS/PaaS, 2024) and top OEMs (Dell/HP/Lenovo ~60% PC shipments, 2024) drive pricing and availability, while data-center carriers (top 5 = ~40% colocation, 2024) and scarce cloud/AI talent (avg US cloud architect pay ≈ $160,000, 2025) raise costs and switching friction.

| Supplier | Key stat | Impact |

|---|---|---|

| Cloud (AWS/Azure/GCP) | 32%/24%/10% (2024) | Pricing leverage |

| OEMs | ~60% PC share (2024) | Procurement risk |

| Data centers | Top5 ~40% colocation (2024) | Capacity/price control |

| Talent | Cloud architect pay ≈ $160k (US, 2025) | Higher labor costs |

What is included in the product

Tailored exclusively for Bell Techlogix, this Porter's Five Forces overview uncovers the key drivers of competition, supplier and buyer power, substitution risks, and entry barriers that shape its market positioning and profitability.

Concise Porter's Five Forces snapshot tailored for Bell Techlogix—quickly spot competitive pressures and prioritize strategic responses.

Customers Bargaining Power

High Price Sensitivity in Managed Services

Enterprise clients treat standard IT infrastructure support as a commodity, driving high price sensitivity and forcing Bell Techlogix to compete on cost; 68% of IT buyers used formal RFPs in 2024 to compare managed services, and average contract bid discounts reached 12–18% versus list pricing.

Low Switching Costs for Standard Support

Low switching costs for standard support mean clients can move basic help-desk and workplace services with little disruption; industry surveys show 42% of enterprises switched IT support providers at least once between 2020–2024. If a customer lacks deep integration into Bell Techlogix’s proprietary platform, transition time averages under 30 days and reduces vendor lock-in, giving customers strong leverage at annual renewals and during price or SLA negotiations.

Demand for Highly Customized Solutions

Access to Comprehensive Market Intelligence

Modern procurement teams now tap benchmarking datasets—Gartner and ISG reports show MSP median hourly rates fell 6–9% from 2020–2024—so buyers know market pricing and uptime norms.

That transparency cuts providers' information advantage, shifting negotiations to buyers who demand stricter SLAs and liquidated-damage clauses; 62% of enterprise buyers (2024 Deloitte) reported tougher SLA terms.

Informed customers also push for performance KPIs tied to payments, raising penalty exposure for MSPs and compressing margins.

- Benchmarks: Gartner/ISG — median MSP rates down 6–9% (2020–2024)

- 62% of enterprises tightened SLA terms (Deloitte 2024)

- Result: higher penalty clauses, margin pressure on MSPs

Consolidation of Corporate IT Budgets

- Enterprise deals: $5–50M/year

- 62% of CIOs favor consolidation (2024)

- Bundled discounts reduce Bell Techlogix margins

- Higher client concentration raises churn risk

Buyers’ leverage soars: RFPs and tighter SLAs crush MSP rates and margins

Buyers hold strong leverage: 68% used RFPs in 2024 and median MSP rates fell 6–9% (2020–2024), while 62% of enterprises tightened SLA terms, raising penalty exposure and compressing margins; large deals ($5–50M/yr) and client concentration amplify this power.

| Metric | Value (2024) |

|---|---|

| RFP usage | 68% |

| Median MSP rate change | -6–9% |

| Enterprises tightening SLAs | 62% |

| Enterprises switching providers (2020–24) | 42% |

| Enterprise deal size | $5–50M/yr |

Preview the Actual Deliverable

Bell Techlogix Porter's Five Forces Analysis

This preview shows the exact Bell Techlogix Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final version of the deliverable; once payment is complete, you’ll get instant access to this same file. No samples or mockups—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Bell Techlogix faces intense competitive rivalry from managed IT and MSP firms, moderate buyer power driven by corporate procurement, constrained supplier influence, low threat from substitutes but evolving tech risks, and a moderate threat of new entrants due to scale and certifications; this snapshot highlights key pressures shaping margins and strategy.

Suppliers Bargaining Power

Dependence on Cloud Hyperscalers

Bell Techlogix depends on AWS, Microsoft Azure, and Google Cloud for core services; these three held about 66% of global cloud IaaS/PaaS market in 2024 (AWS 32%, Azure 24%, Google 10%), giving them pricing and contract leverage over smaller integrators.

Supplier price changes flow straight to Bell Techlogix margins: a 10% cloud price rise would roughly add 3–6% to service COGS based on typical cloud cost shares in MSPs, squeezing EBITDA unless passed to clients.

Hardware OEM Relationships

Hardware OEM relationships matter because Bell Techlogix depends on steady supplies from Dell, HP, and Lenovo; in 2024 these three controlled ~60% of global PC shipments, so their pricing and availability directly affect enterprise deployments.

These OEMs wield power via brand trust and certified support contracts, making switches costly; Gartner reported 2024 enterprise support premiums rising ~8%, increasing Bell Techlogix procurement costs if OEM terms tighten.

Supply-chain shocks matter: semiconductor and logistics disruptions in 2021–22 pushed component lead times from 4 to 20+ weeks; a recurrence would force Bell Techlogix to change service SLAs or hold higher inventory, tying up working capital.

Specialized Cybersecurity Software Vendors

Specialized cybersecurity vendors supply the advanced software Bell Techlogix needs for high-tier services, and vendors’ deep integration creates high switching costs—often 12–18 months and $200k+ in migration and retraining for enterprise clients. These suppliers use tiered pricing and mandatory update cycles; in 2024 top endpoint vendors raised enterprise list prices by ~6–9%, squeezing margins Bell Techlogix must pass to customers.

Scarcity of Specialized IT Talent

In late 2025, specialized AI and cloud architects are scarce: LinkedIn data shows global demand up 42% year-over-year and average cloud architect salaries rose to about $160,000 in the US by 2025, boosting supplier power.

Bell Techlogix faces high turnover risk and must offer premium pay, signing bonuses, and benefits—adding 15–25% to labor costs—to meet managed-services SLAs and retain critical engineers.

- Demand +42% YoY (LinkedIn, 2025)

- Avg cloud architect pay ≈ $160,000 (US, 2025)

- Retention premium 15–25% on labor costs

Data Center and Connectivity Providers

Data center and telco giants like Equinix, Digital Realty, AT&T and Verizon control much of the internet backbone, leaving managed-service firms such as Bell Techlogix with limited regional alternatives; Equinix reported 228 data centers and $8.1B revenue in 2024, showing concentration.

These suppliers set SLAs and bandwidth pricing—wholesale bandwidth prices rose ~12% in 2023–2024 in parts of North America—directly driving Bell Techlogix’s cost of service and margin pressure.

What this estimate hides: localized monopoly power can force multi-year contracts, making switching costly and slow.

- High concentration: top 5 DC operators control ~40% global colocation capacity (2024)

- Revenue impact: carrier costs up ~12% (2023–24) in key markets

- Contract lock-in: multi-year SLAs common, switching friction high

Supplier Dominance: Cloud, OEMs, Data Centers & Talent Drive Costs for Bell Techlogix

Suppliers hold strong leverage over Bell Techlogix: top cloud providers (AWS 32%, Azure 24%, Google 10% of IaaS/PaaS, 2024) and top OEMs (Dell/HP/Lenovo ~60% PC shipments, 2024) drive pricing and availability, while data-center carriers (top 5 = ~40% colocation, 2024) and scarce cloud/AI talent (avg US cloud architect pay ≈ $160,000, 2025) raise costs and switching friction.

| Supplier | Key stat | Impact |

|---|---|---|

| Cloud (AWS/Azure/GCP) | 32%/24%/10% (2024) | Pricing leverage |

| OEMs | ~60% PC share (2024) | Procurement risk |

| Data centers | Top5 ~40% colocation (2024) | Capacity/price control |

| Talent | Cloud architect pay ≈ $160k (US, 2025) | Higher labor costs |

What is included in the product

Tailored exclusively for Bell Techlogix, this Porter's Five Forces overview uncovers the key drivers of competition, supplier and buyer power, substitution risks, and entry barriers that shape its market positioning and profitability.

Concise Porter's Five Forces snapshot tailored for Bell Techlogix—quickly spot competitive pressures and prioritize strategic responses.

Customers Bargaining Power

High Price Sensitivity in Managed Services

Enterprise clients treat standard IT infrastructure support as a commodity, driving high price sensitivity and forcing Bell Techlogix to compete on cost; 68% of IT buyers used formal RFPs in 2024 to compare managed services, and average contract bid discounts reached 12–18% versus list pricing.

Low Switching Costs for Standard Support

Low switching costs for standard support mean clients can move basic help-desk and workplace services with little disruption; industry surveys show 42% of enterprises switched IT support providers at least once between 2020–2024. If a customer lacks deep integration into Bell Techlogix’s proprietary platform, transition time averages under 30 days and reduces vendor lock-in, giving customers strong leverage at annual renewals and during price or SLA negotiations.

Demand for Highly Customized Solutions

Access to Comprehensive Market Intelligence

Modern procurement teams now tap benchmarking datasets—Gartner and ISG reports show MSP median hourly rates fell 6–9% from 2020–2024—so buyers know market pricing and uptime norms.

That transparency cuts providers' information advantage, shifting negotiations to buyers who demand stricter SLAs and liquidated-damage clauses; 62% of enterprise buyers (2024 Deloitte) reported tougher SLA terms.

Informed customers also push for performance KPIs tied to payments, raising penalty exposure for MSPs and compressing margins.

- Benchmarks: Gartner/ISG — median MSP rates down 6–9% (2020–2024)

- 62% of enterprises tightened SLA terms (Deloitte 2024)

- Result: higher penalty clauses, margin pressure on MSPs

Consolidation of Corporate IT Budgets

- Enterprise deals: $5–50M/year

- 62% of CIOs favor consolidation (2024)

- Bundled discounts reduce Bell Techlogix margins

- Higher client concentration raises churn risk

Buyers’ leverage soars: RFPs and tighter SLAs crush MSP rates and margins

Buyers hold strong leverage: 68% used RFPs in 2024 and median MSP rates fell 6–9% (2020–2024), while 62% of enterprises tightened SLA terms, raising penalty exposure and compressing margins; large deals ($5–50M/yr) and client concentration amplify this power.

| Metric | Value (2024) |

|---|---|

| RFP usage | 68% |

| Median MSP rate change | -6–9% |

| Enterprises tightening SLAs | 62% |

| Enterprises switching providers (2020–24) | 42% |

| Enterprise deal size | $5–50M/yr |

Preview the Actual Deliverable

Bell Techlogix Porter's Five Forces Analysis

This preview shows the exact Bell Techlogix Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final version of the deliverable; once payment is complete, you’ll get instant access to this same file. No samples or mockups—what you see is what you get.