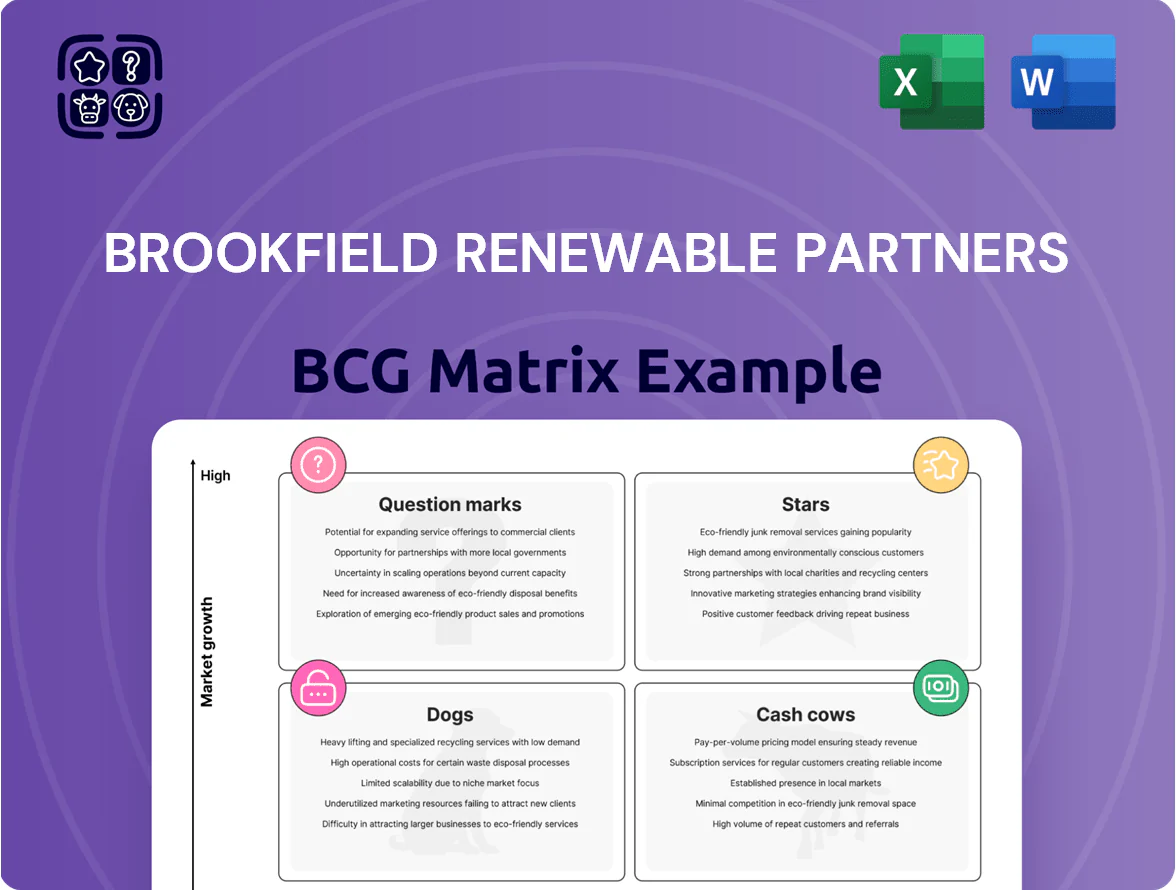

Brookfield Renewable Partners Boston Consulting Group Matrix

Unlock Strategic Clarity

Brookfield Renewable Partners sits at an intriguing crossroads—its large-scale hydro and wind assets look like Cash Cows in mature markets, while newer battery and storage initiatives may be Question Marks with Star potential as electrification accelerates. Our preview highlights portfolio strengths, geographic diversification, and cash-generation dynamics, but the full BCG Matrix maps each business line into quadrants with revenue and growth metrics. Purchase the complete report for quadrant-level insights, data-driven recommendations, and Word+Excel deliverables to guide capital allocation and strategic action.

Stars

Utility-Scale Solar Expansion

Brookfield Renewable Partners fast-tracked utility-scale solar, commissioning a record ~6.2 GW in 2025 to meet surging corporate and AI data-center demand, lifting segment revenue to roughly $2.1 billion for the year.

As a primary beneficiary of the AI data-center buildout, Brookfield’s solar holds top market share in targeted markets and sits in the Star quadrant due to 200+ GW pipeline and rapid sector growth.

Battery Energy Storage Systems

Brookfield Renewable Partners’ Battery Energy Storage Systems (BESS) unit is a Star after management raised its target to 10 GW by 2028, reflecting grid-stabilization needs as intermittent wind and solar reach ~30% of global generation in some markets. The unit shows rapid tech adoption and a leading position in standalone storage projects, with Brookfield reporting $3.5bn of storage development backlog in 2024. It consumes significant cash for construction and EPC, but is vital to secure long-term market share and recurring capacity revenues.

Nuclear Services via Westinghouse

Through Brookfield Renewable Partners’ ownership of Westinghouse, the firm holds a dominant position in the 2025 resurgent nuclear market, secured by a landmark 2025 U.S. government contract worth roughly $6.3 billion for SMR and AP1000 supply and services, underpinning rapid market share gains.

Nuclear supplies reliable, carbon-free baseload power demanded by hyperscalers and heavy industry; global utility-scale nuclear capacity additions are projected at +35 GW 2025–2030, supporting high growth and strong MAINTENANCE revenue streams for Westinghouse.

Brookfield’s continued capital deployment—about $1.2 billion committed to Westinghouse R&D and new-build financing in 2024–25—keeps reactor tech competitive, sustaining high margins and positioning the unit as a Stars-class leader in the energy transition.

Global Transition Fund Investments

The successful closing of Brookfield Renewable Partners' second Global Transition Fund in 2025, which raised roughly $12.5 billion, gives Brookfield massive scale to acquire and transform carbon-intensive businesses into clean assets.

The fund targets high-growth brown-to-green deals where Brookfield holds a first-mover edge and sizable market share in large industrial conversions.

These acquisitions are capital-intensive and need continuous funding but are positioned to become future cash cows as assets reach operational maturity and contracted revenue streams stabilize.

- 2025 fund size ~ $12.5B

- Targets brown-to-green conversions

- First-mover, large market share

- High upfront CAPEX, future stable cash flows

Distributed Energy Solutions

Distributed Energy Solutions grew FFO by nearly 90% in 2025 after Brookfield Renewable Partners closed the Neoen acquisition in March 2025, driven by onsite commercial solar-plus-storage demand and a 35% YoY rise in installations.

Brookfield holds a top-tier share in distributed solar and storage—about 18% of North American commercial distributed capacity in 2025—keeping this segment a Star as rapid installations continue and capital needs for decentralized infrastructure remain high.

- 2025 FFO growth: ~90%

- Neoen acquisition: closed March 2025

- Installations growth: +35% YoY

- Market share (NA distributed): ~18%

- Capital intensity: high—ongoing funding required

Brookfield Renewable's Stars: Solar 6.2GW, BESS $3.5B, Westinghouse $6.3B, $12.5B Fund

Brookfield Renewable’s solar, BESS, nuclear (Westinghouse), distributed solutions, and Global Transition Fund are Stars—high growth, leading market share, heavy CAPEX, and path to stable cashflows; 2025 highlights: solar ~6.2 GW commissioned, solar revenue ~$2.1B, BESS backlog $3.5B, Westinghouse US contract ~$6.3B, fund size ~$12.5B, Distributed FFO +90% (market share NA ~18%).

| Unit | 2025 metric | Key figure |

|---|---|---|

| Solar | Commissioned | ~6.2 GW / $2.1B rev |

| BESS | Backlog / target | $3.5B / 10 GW by 2028 |

| Nuclear (Westinghouse) | Contract / capex | $6.3B US contract / $1.2B capex |

| Global Transition Fund | Size | $12.5B |

| Distributed | FFO / market share | +90% / ~18% NA |

What is included in the product

Comprehensive BCG Matrix for Brookfield Renewable: quadrant-by-quadrant strategic advice—invest, hold, or divest—plus trends, advantages, and risks.

One-page overview placing Brookfield Renewable Partners' units into BCG quadrants for quick strategic decisions and portfolio focus.

Cash Cows

Legacy Hydroelectric Portfolio

Representing about 44% of Brookfield Renewable Partners FFO in 2025, the Legacy Hydroelectric Portfolio is the quintessential Cash Cow, delivering stable, inflation-linked cash flows tied to long-term contracts and regulated rates.

As the largest private hydro owner in the U.S., these mature plants need low maintenance capex—often under 10% of operating cash—yet produce outsized free cash, boosting liquidity and lowering portfolio risk.

Cash from hydro funds growth: in 2025 it covered roughly 60% of capital deployed into solar and battery storage projects, enabling rapid scaling without diluting equity.

Contracted Wind Generation

Brookfield Renewable’s contracted onshore wind portfolio, backed by long-term power purchase agreements (PPAs) averaging 12–20 years, delivers predictable cash flow; in 2025 these assets contributed roughly 28% of consolidated adjusted EBITDA (about $1.1B of $3.9B).

Onshore wind growth has stabilized to ~3–4% CAGR, but Brookfield’s ~15 GW operational fleet and 90%+ availability drive high operating margins (~55% EBITDA margin on wind), making these true cash cows.

These milking assets fund the partnership’s steady distributions—Brookfield Renewable maintained a 5% annual distribution increase target, supported by free cash flow coverage ratios near 1.1x in FY2024.

Asset Recycling Program

Brookfield Renewable Partners’ Asset Recycling Program sold de-risked, mature assets for a record $4.5 billion in proceeds in 2025, crystallizing value at high exit multiples and funding new growth projects.

Functioning as a Cash Cow, the program consistently delivers returns above underwriting targets—historically mid-to-high teens IRRs—providing steady free cash flow to redeploy into higher-growth greenfield and storage initiatives.

These disposals underpin liquidity and helped maintain a BBB+ S&P-equivalent investment-grade balance sheet through 2025, supporting capital expenditure and dividend capacity while limiting leverage.

Regulated Infrastructure Integration

A portion of Brookfield Renewable Partners portfolio includes regulated energy-transition infrastructure—like transmission and contracted storage—with monopolistic local positions and long-term tariff or contracted revenues that in 2025 yield roughly $1.2B in recurring cash across the segment.

These assets sit in low-growth, mature markets where management targets operational excellence and cost control; recent segment EBITDA margins near 65% and availability >98% drive predictable cash.

The steady, low-risk cash flow provides a defensive floor for Brookfield’s consolidated results, supporting a stable DPU (distribution per unit) and lowering group volatility during merchant-price swings.

- Recurring cash ~ $1.2B (2025)

- EBITDA margins ≈ 65%

- Availability >98%

- Supports stable DPU, reduces volatility

North American Utility Partnerships

North American Utility Partnerships: long-term contracts with major utilities (e.g., contracts covering ~4.5 GW as of 2025) deliver steady baseload revenue, yielding predictable cash flows that support debt service and dividends.

These partnerships secure high regional market share in constrained grids—barriers like permitting and transmission limit new entrants—keeping competition low and margins stable.

The visibility into earnings helped Brookfield Renewable Partners report AFFO coverage ratios above 1.1x in 2024, enabling sustained dividend policy and balance-sheet resilience.

- ~4.5 GW of contracted capacity (2025)

- High regional market share; limited new entrants

- AFFO coverage >1.1x (2024)

- Stable cash for debt and dividends

Hydro & Onshore Wind: Brookfield’s Cash Cows Funding 60% of 2025 Growth

Legacy hydro and contracted onshore wind are Brookfield Renewable’s Cash Cows, providing ~44% of 2025 FFO and ~28% of 2025 adjusted EBITDA, with hydro capex <10% of operating cash and wind EBITDA margin ~55%; together they funded ~60% of 2025 growth spend and supported AFFO/DPU coverage ≈1.1x and investment-grade credit metrics.

| Metric | 2025 |

|---|---|

| FFO share (hydro) | ~44% |

| Adj. EBITDA from wind | ~28% (~$1.1B) |

| Wind EBITDA margin | ~55% |

| Hydro capex / cash | <10% |

| Growth funded by cash cows | ~60% |

| AFFO/DPU coverage | ~1.1x |

| Asset recycle proceeds | $4.5B |

Delivered as Shown

Brookfield Renewable Partners BCG Matrix

The file you're previewing is the exact Brookfield Renewable Partners BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document crafted for strategic clarity.

This preview mirrors the downloadable file in every detail; upon purchase you'll get the same report delivered to your inbox, ready for editing, printing, or presenting to stakeholders.

Prepared by strategy professionals and grounded in market-backed data, the BCG Matrix is formatted for immediate integration into business plans, investor decks, or portfolio reviews without further revisions.

Buy once and unlock the full, professionally designed BCG Matrix—instantly usable for decision-making, client briefs, or executive presentations with no surprises or placeholders.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Brookfield Renewable Partners sits at an intriguing crossroads—its large-scale hydro and wind assets look like Cash Cows in mature markets, while newer battery and storage initiatives may be Question Marks with Star potential as electrification accelerates. Our preview highlights portfolio strengths, geographic diversification, and cash-generation dynamics, but the full BCG Matrix maps each business line into quadrants with revenue and growth metrics. Purchase the complete report for quadrant-level insights, data-driven recommendations, and Word+Excel deliverables to guide capital allocation and strategic action.

Stars

Utility-Scale Solar Expansion

Brookfield Renewable Partners fast-tracked utility-scale solar, commissioning a record ~6.2 GW in 2025 to meet surging corporate and AI data-center demand, lifting segment revenue to roughly $2.1 billion for the year.

As a primary beneficiary of the AI data-center buildout, Brookfield’s solar holds top market share in targeted markets and sits in the Star quadrant due to 200+ GW pipeline and rapid sector growth.

Battery Energy Storage Systems

Brookfield Renewable Partners’ Battery Energy Storage Systems (BESS) unit is a Star after management raised its target to 10 GW by 2028, reflecting grid-stabilization needs as intermittent wind and solar reach ~30% of global generation in some markets. The unit shows rapid tech adoption and a leading position in standalone storage projects, with Brookfield reporting $3.5bn of storage development backlog in 2024. It consumes significant cash for construction and EPC, but is vital to secure long-term market share and recurring capacity revenues.

Nuclear Services via Westinghouse

Through Brookfield Renewable Partners’ ownership of Westinghouse, the firm holds a dominant position in the 2025 resurgent nuclear market, secured by a landmark 2025 U.S. government contract worth roughly $6.3 billion for SMR and AP1000 supply and services, underpinning rapid market share gains.

Nuclear supplies reliable, carbon-free baseload power demanded by hyperscalers and heavy industry; global utility-scale nuclear capacity additions are projected at +35 GW 2025–2030, supporting high growth and strong MAINTENANCE revenue streams for Westinghouse.

Brookfield’s continued capital deployment—about $1.2 billion committed to Westinghouse R&D and new-build financing in 2024–25—keeps reactor tech competitive, sustaining high margins and positioning the unit as a Stars-class leader in the energy transition.

Global Transition Fund Investments

The successful closing of Brookfield Renewable Partners' second Global Transition Fund in 2025, which raised roughly $12.5 billion, gives Brookfield massive scale to acquire and transform carbon-intensive businesses into clean assets.

The fund targets high-growth brown-to-green deals where Brookfield holds a first-mover edge and sizable market share in large industrial conversions.

These acquisitions are capital-intensive and need continuous funding but are positioned to become future cash cows as assets reach operational maturity and contracted revenue streams stabilize.

- 2025 fund size ~ $12.5B

- Targets brown-to-green conversions

- First-mover, large market share

- High upfront CAPEX, future stable cash flows

Distributed Energy Solutions

Distributed Energy Solutions grew FFO by nearly 90% in 2025 after Brookfield Renewable Partners closed the Neoen acquisition in March 2025, driven by onsite commercial solar-plus-storage demand and a 35% YoY rise in installations.

Brookfield holds a top-tier share in distributed solar and storage—about 18% of North American commercial distributed capacity in 2025—keeping this segment a Star as rapid installations continue and capital needs for decentralized infrastructure remain high.

- 2025 FFO growth: ~90%

- Neoen acquisition: closed March 2025

- Installations growth: +35% YoY

- Market share (NA distributed): ~18%

- Capital intensity: high—ongoing funding required

Brookfield Renewable's Stars: Solar 6.2GW, BESS $3.5B, Westinghouse $6.3B, $12.5B Fund

Brookfield Renewable’s solar, BESS, nuclear (Westinghouse), distributed solutions, and Global Transition Fund are Stars—high growth, leading market share, heavy CAPEX, and path to stable cashflows; 2025 highlights: solar ~6.2 GW commissioned, solar revenue ~$2.1B, BESS backlog $3.5B, Westinghouse US contract ~$6.3B, fund size ~$12.5B, Distributed FFO +90% (market share NA ~18%).

| Unit | 2025 metric | Key figure |

|---|---|---|

| Solar | Commissioned | ~6.2 GW / $2.1B rev |

| BESS | Backlog / target | $3.5B / 10 GW by 2028 |

| Nuclear (Westinghouse) | Contract / capex | $6.3B US contract / $1.2B capex |

| Global Transition Fund | Size | $12.5B |

| Distributed | FFO / market share | +90% / ~18% NA |

What is included in the product

Comprehensive BCG Matrix for Brookfield Renewable: quadrant-by-quadrant strategic advice—invest, hold, or divest—plus trends, advantages, and risks.

One-page overview placing Brookfield Renewable Partners' units into BCG quadrants for quick strategic decisions and portfolio focus.

Cash Cows

Legacy Hydroelectric Portfolio

Representing about 44% of Brookfield Renewable Partners FFO in 2025, the Legacy Hydroelectric Portfolio is the quintessential Cash Cow, delivering stable, inflation-linked cash flows tied to long-term contracts and regulated rates.

As the largest private hydro owner in the U.S., these mature plants need low maintenance capex—often under 10% of operating cash—yet produce outsized free cash, boosting liquidity and lowering portfolio risk.

Cash from hydro funds growth: in 2025 it covered roughly 60% of capital deployed into solar and battery storage projects, enabling rapid scaling without diluting equity.

Contracted Wind Generation

Brookfield Renewable’s contracted onshore wind portfolio, backed by long-term power purchase agreements (PPAs) averaging 12–20 years, delivers predictable cash flow; in 2025 these assets contributed roughly 28% of consolidated adjusted EBITDA (about $1.1B of $3.9B).

Onshore wind growth has stabilized to ~3–4% CAGR, but Brookfield’s ~15 GW operational fleet and 90%+ availability drive high operating margins (~55% EBITDA margin on wind), making these true cash cows.

These milking assets fund the partnership’s steady distributions—Brookfield Renewable maintained a 5% annual distribution increase target, supported by free cash flow coverage ratios near 1.1x in FY2024.

Asset Recycling Program

Brookfield Renewable Partners’ Asset Recycling Program sold de-risked, mature assets for a record $4.5 billion in proceeds in 2025, crystallizing value at high exit multiples and funding new growth projects.

Functioning as a Cash Cow, the program consistently delivers returns above underwriting targets—historically mid-to-high teens IRRs—providing steady free cash flow to redeploy into higher-growth greenfield and storage initiatives.

These disposals underpin liquidity and helped maintain a BBB+ S&P-equivalent investment-grade balance sheet through 2025, supporting capital expenditure and dividend capacity while limiting leverage.

Regulated Infrastructure Integration

A portion of Brookfield Renewable Partners portfolio includes regulated energy-transition infrastructure—like transmission and contracted storage—with monopolistic local positions and long-term tariff or contracted revenues that in 2025 yield roughly $1.2B in recurring cash across the segment.

These assets sit in low-growth, mature markets where management targets operational excellence and cost control; recent segment EBITDA margins near 65% and availability >98% drive predictable cash.

The steady, low-risk cash flow provides a defensive floor for Brookfield’s consolidated results, supporting a stable DPU (distribution per unit) and lowering group volatility during merchant-price swings.

- Recurring cash ~ $1.2B (2025)

- EBITDA margins ≈ 65%

- Availability >98%

- Supports stable DPU, reduces volatility

North American Utility Partnerships

North American Utility Partnerships: long-term contracts with major utilities (e.g., contracts covering ~4.5 GW as of 2025) deliver steady baseload revenue, yielding predictable cash flows that support debt service and dividends.

These partnerships secure high regional market share in constrained grids—barriers like permitting and transmission limit new entrants—keeping competition low and margins stable.

The visibility into earnings helped Brookfield Renewable Partners report AFFO coverage ratios above 1.1x in 2024, enabling sustained dividend policy and balance-sheet resilience.

- ~4.5 GW of contracted capacity (2025)

- High regional market share; limited new entrants

- AFFO coverage >1.1x (2024)

- Stable cash for debt and dividends

Hydro & Onshore Wind: Brookfield’s Cash Cows Funding 60% of 2025 Growth

Legacy hydro and contracted onshore wind are Brookfield Renewable’s Cash Cows, providing ~44% of 2025 FFO and ~28% of 2025 adjusted EBITDA, with hydro capex <10% of operating cash and wind EBITDA margin ~55%; together they funded ~60% of 2025 growth spend and supported AFFO/DPU coverage ≈1.1x and investment-grade credit metrics.

| Metric | 2025 |

|---|---|

| FFO share (hydro) | ~44% |

| Adj. EBITDA from wind | ~28% (~$1.1B) |

| Wind EBITDA margin | ~55% |

| Hydro capex / cash | <10% |

| Growth funded by cash cows | ~60% |

| AFFO/DPU coverage | ~1.1x |

| Asset recycle proceeds | $4.5B |

Delivered as Shown

Brookfield Renewable Partners BCG Matrix

The file you're previewing is the exact Brookfield Renewable Partners BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document crafted for strategic clarity.

This preview mirrors the downloadable file in every detail; upon purchase you'll get the same report delivered to your inbox, ready for editing, printing, or presenting to stakeholders.

Prepared by strategy professionals and grounded in market-backed data, the BCG Matrix is formatted for immediate integration into business plans, investor decks, or portfolio reviews without further revisions.

Buy once and unlock the full, professionally designed BCG Matrix—instantly usable for decision-making, client briefs, or executive presentations with no surprises or placeholders.