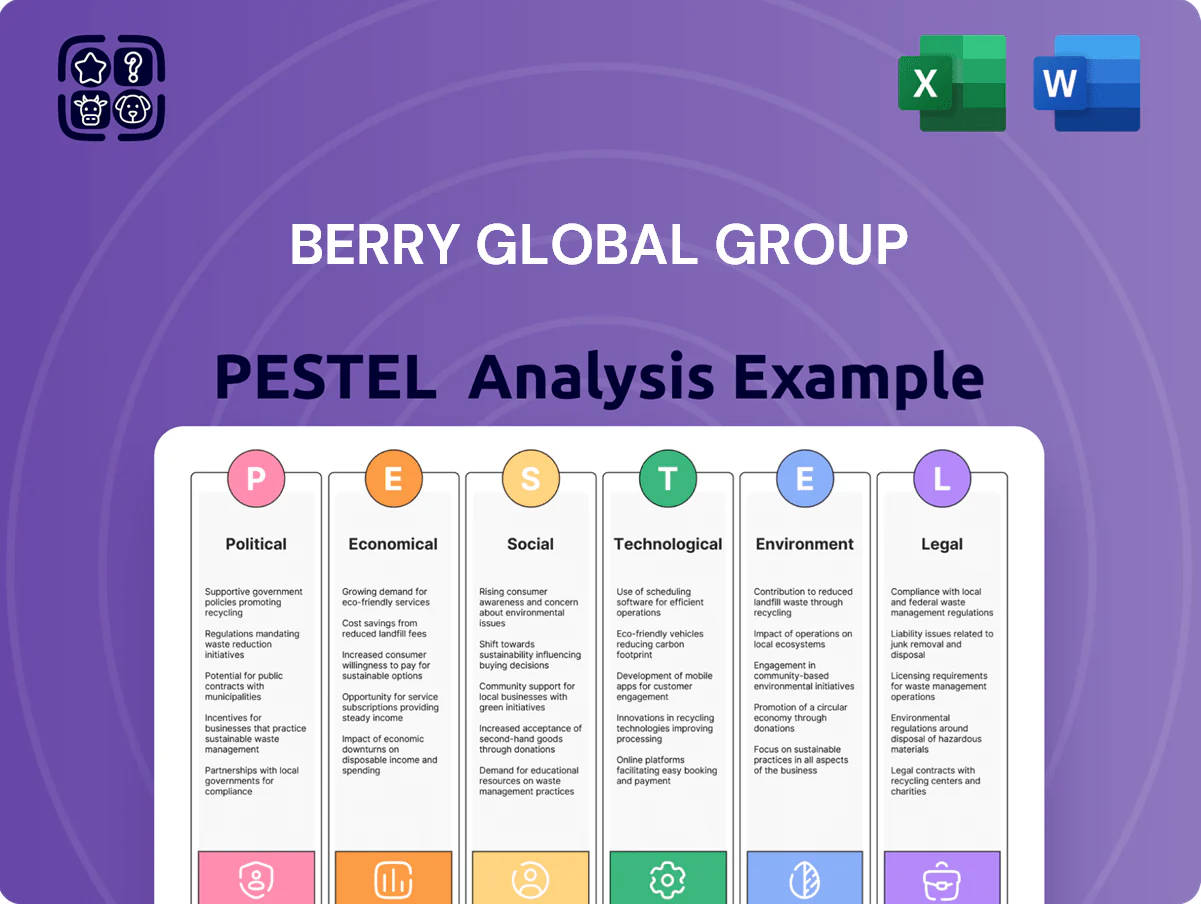

Berry Global Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Uncover how geopolitical shifts, supply-chain pressures, and sustainability regulations are reshaping Berry Global Group’s strategic outlook—our concise PESTLE snapshot highlights the risks and opportunities you need to know; purchase the full analysis for actionable, board-ready insights and downloadable templates to drive smarter investment and strategy decisions.

Political factors

Geopolitical Trade Relations

Berry Global Group's global manufacturing footprint across 36 countries exposes it to shifts in trade agreements and tariffs; in 2024 resin costs rose ~18% YoY, pressuring margins amid $11.2B net sales (FY2024).

Escalating US-China and Russia-EU tensions risk supply-chain disruptions and freight cost spikes—Berry reported logistics costs up ~12% in 2023—forcing pricing and sourcing adjustments.

Management must hedge geopolitical risk via diversified sourcing, regional pricing strategies, and contractual pass-throughs to protect operating EPS, which was $2.10 in FY2024.

Global Packaging Regulations

Governments increasingly mandate recycled content and plastic limits, with the EU requiring 30% recycled PET in beverage bottles by 2030 and 2024 US state laws (e.g., California SB 54) pushing similar targets that affect Berry Global’s $13.6B 2023 revenue mix.

Political shifts toward circular economy models force Berry to align strategies with national sustainability agendas to avoid fines and retain procurement contracts in markets representing over 40% of its sales.

Varying support for plastic alternatives across jurisdictions—subsidies in Germany versus restrictions in parts of Latin America—creates compliance and supply-chain complexity impacting capital allocation and R&D spend.

Governmental Subsidies and Incentives

Political support for green energy and sustainable manufacturing can unlock tax credits and capital subsidies for Berry Global; for example, U.S. clean energy tax incentives under the Inflation Reduction Act could reduce capital costs by up to 30% on qualifying facility upgrades.

Access to government R&D grants—U.S. SBIR/STTR, EU Horizon Europe funds (2021–2027 budget €95.5bn)—can accelerate Berry’s biodegradable materials pipeline and lower incremental R&D spend.

Conversely, weak political will in regions without strong green policies risks delaying facility retrofits and raises stranded-capital risk, potentially increasing compliance and transition costs for Berry in those markets.

Regional Stability in Key Markets

Berry Global operates in emerging markets where political instability threatens asset security and continuity, with roughly 28% of 2024 revenues tied to international regions exposed to higher geopolitical risk.

Sudden government changes or civil unrest can disrupt production and distribution of healthcare and hygiene products, evidenced by 2023 supply interruptions that raised logistics costs by an estimated 4-6% in affected regions.

Continuous monitoring of regional political climates is therefore essential for strategic planning, insurance coverage adjustments, and contingency allocation within capital expenditure budgets.

- 28% of 2024 revenues from higher-risk international markets

- 2023 supply disruptions increased logistics costs ~4-6%

- Requires active political monitoring, insurance, CAPEX contingency

Public Health Policy Influence

As a major supplier of healthcare and personal care packaging, Berry Global is directly tied to government healthcare spending—US federal health outlays reached about $1.9 trillion in 2024, influencing demand for medical-grade packaging.

Political focus on pandemic preparedness and supply-chain resilience (e.g., US CHIPS/HELP acts and EU health security plans) boosts demand for protective and sterile packaging solutions.

Berry must remain agile to shifting public-health priorities and expedited regulatory approvals for medical plastics to capture contracts; healthcare packaging was ~18% of Berry’s 2024 net sales (~$2.6bn of $14.5bn).

- Healthcare policy shifts directly affect demand and contract timing

- Pandemic preparedness increases need for sterile/protective packaging

- Regulatory approvals for medical-grade plastics are critical to revenue capture

Berry Faces Margin Strain: Trade, rPET Rules & Rising Logistics Lift FY24 Costs

Political risks—trade tensions, tariffs, and regional regulations on recycled content (EU 30% rPET by 2030; CA SB 54)—pressure Berry’s margins and capex; FY2024 sales $11.2B–$14.5B (healthcare ~$2.6B) with ~28% revenue in higher-risk markets, logistics costs up ~12% (2023) and supply disruptions adding ~4–6%.

| Metric | Value |

|---|---|

| FY2024 net sales | $11.2B–$14.5B |

| Healthcare sales | $2.6B (~18%) |

| Revenues in high-risk markets | 28% |

| Logistics cost change (2023) | +12% |

| Supply disruption impact | +4–6% logistics |

What is included in the product

Explores how external macro-environmental factors uniquely affect Berry Global Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors, and strategists on risks, opportunities, and scenario planning.

A concise, shareable PESTLE summary of Berry Global Group that’s visually segmented for quick meetings, editable for local or business-line notes, and written in clear language to support fast alignment on external risks and strategic positioning.

Economic factors

Raw Material Price Volatility

The cost of plastic resins—about 30–40% of Berry Global Group's COGS—tracks oil and natural gas prices; Brent crude rose ~20% in 2024, pressuring margins. Volatile energy markets in 2024–2025 forced more active hedging and selective price pass-through; Berry reported resin cost inflation contributing to its 2024 gross margin decline of ~150 basis points. Petroleum supply shifts directly compress EBITDA when pass-through is delayed.

Inflationary Pressures and Interest Rates

Persistent US inflation—3.4% year-over-year in 2024 (BLS)—raises Berry Global Group's labor and logistics costs, pressuring its goal to improve adjusted EBITDA margins (2023 pro forma margin ~11.5%).

Higher interest rates (US 10-year at ~4.5% in early 2025) increase Berry's cost of debt; long-term net leverage stood near 4.0x in 2024, elevating financing costs for capex and M&A.

Berry must reprioritize capital allocation—balancing necessary investments and debt reduction—to sustain growth while containing high-cost borrowing impacts.

Currency Exchange Rate Fluctuations

With roughly 45% of 2024 revenue generated outside the United States, Berry Global faces material foreign exchange risk as USD moves versus the euro, pound and MXN; a 5% USD appreciation could reduce reported international revenue by an estimated $200–250 million annually.

Currency translation hit 2024 adjusted operating income by about $60 million, highlighting sensitivity to FX swings. Berry pursues geographic diversification and active hedging—noting $1.2 billion of hedged exposure in 2024—to stabilize reported results and cash flows.

Consumer Spending Patterns

Consumer spending shifts reduce demand for premium personal-care packaging; US household disposable income fell 0.5% real in 2023 versus 2022, pressuring premium segments.

Berry’s exposure to essentials—food, healthcare, hygiene—accounted for ~70% of 2024 sales, cushioning revenue in downturns and supporting stable EBITDA margin (2024 adj. EBITDA margin ~10.8%).

Monitoring macro indicators lets Berry reweight product mix toward value and high-turn essentials aligned to consumer purchasing power.

- Disposable income decline 0.5% (2023)

- Essentials ~70% of 2024 sales

- 2024 adj. EBITDA margin ~10.8%

Global Supply Chain Dynamics

Global shipping rates fell from a 2022 peak (Harpex index down ~60% by end-2024) but remain 20–30% above 2019 levels, affecting Berry Global’s COGS and lead times; port congestion variability (e.g., LA/Long Beach dwell times down 15% in 2024) still risks delays to international customers.

Berry must weigh higher unit costs from localized plants against inventory and tariff savings from centralized hubs; nearshoring could raise manufacturing opex by ~5–12% but cut transit times by weeks.

Efficient logistics—route optimization, carrier diversification, 3PL partnerships—reduces volatility impact; logistics drive a material portion of SG&A and margin resilience in a global economy with fluctuating fuel surcharges and freight surcharges.

- Harpex index down ~60% from 2022 peak; freight ~20–30% above 2019

- Port dwell times improved ~15% at major US ports (2024)

- Nearshoring may increase opex ~5–12% but trims transit weeks

- Logistics optimization directly supports SG&A and margins

Rising resin, inflation and FX squeeze margins as leverage and rates bite

Resin costs (30–40% of COGS) tied to oil; Brent +~20% in 2024 hit gross margin (~150 bps headwind). US inflation 3.4% (2024) raised labor/logistics; 2024 adj. EBITDA margin ~10.8% with pro forma 2023 margin ~11.5%. US 10y ~4.5% (early 2025) and net leverage ~4.0x increased financing costs. FX: 45% revenue ex-US; 5% USD up ≈ -$200–250M revenue; $1.2B hedged 2024.

| Metric | 2024 |

|---|---|

| Resin % COGS | 30–40% |

| Adj. EBITDA margin | 10.8% |

| US inflation | 3.4% |

| Net leverage | ~4.0x |

| Intl revenue | 45% |

Preview Before You Purchase

Berry Global Group PESTLE Analysis

The preview shown here is the exact Berry Global Group PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in this preview are identical to the downloadable file you’ll get immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Uncover how geopolitical shifts, supply-chain pressures, and sustainability regulations are reshaping Berry Global Group’s strategic outlook—our concise PESTLE snapshot highlights the risks and opportunities you need to know; purchase the full analysis for actionable, board-ready insights and downloadable templates to drive smarter investment and strategy decisions.

Political factors

Geopolitical Trade Relations

Berry Global Group's global manufacturing footprint across 36 countries exposes it to shifts in trade agreements and tariffs; in 2024 resin costs rose ~18% YoY, pressuring margins amid $11.2B net sales (FY2024).

Escalating US-China and Russia-EU tensions risk supply-chain disruptions and freight cost spikes—Berry reported logistics costs up ~12% in 2023—forcing pricing and sourcing adjustments.

Management must hedge geopolitical risk via diversified sourcing, regional pricing strategies, and contractual pass-throughs to protect operating EPS, which was $2.10 in FY2024.

Global Packaging Regulations

Governments increasingly mandate recycled content and plastic limits, with the EU requiring 30% recycled PET in beverage bottles by 2030 and 2024 US state laws (e.g., California SB 54) pushing similar targets that affect Berry Global’s $13.6B 2023 revenue mix.

Political shifts toward circular economy models force Berry to align strategies with national sustainability agendas to avoid fines and retain procurement contracts in markets representing over 40% of its sales.

Varying support for plastic alternatives across jurisdictions—subsidies in Germany versus restrictions in parts of Latin America—creates compliance and supply-chain complexity impacting capital allocation and R&D spend.

Governmental Subsidies and Incentives

Political support for green energy and sustainable manufacturing can unlock tax credits and capital subsidies for Berry Global; for example, U.S. clean energy tax incentives under the Inflation Reduction Act could reduce capital costs by up to 30% on qualifying facility upgrades.

Access to government R&D grants—U.S. SBIR/STTR, EU Horizon Europe funds (2021–2027 budget €95.5bn)—can accelerate Berry’s biodegradable materials pipeline and lower incremental R&D spend.

Conversely, weak political will in regions without strong green policies risks delaying facility retrofits and raises stranded-capital risk, potentially increasing compliance and transition costs for Berry in those markets.

Regional Stability in Key Markets

Berry Global operates in emerging markets where political instability threatens asset security and continuity, with roughly 28% of 2024 revenues tied to international regions exposed to higher geopolitical risk.

Sudden government changes or civil unrest can disrupt production and distribution of healthcare and hygiene products, evidenced by 2023 supply interruptions that raised logistics costs by an estimated 4-6% in affected regions.

Continuous monitoring of regional political climates is therefore essential for strategic planning, insurance coverage adjustments, and contingency allocation within capital expenditure budgets.

- 28% of 2024 revenues from higher-risk international markets

- 2023 supply disruptions increased logistics costs ~4-6%

- Requires active political monitoring, insurance, CAPEX contingency

Public Health Policy Influence

As a major supplier of healthcare and personal care packaging, Berry Global is directly tied to government healthcare spending—US federal health outlays reached about $1.9 trillion in 2024, influencing demand for medical-grade packaging.

Political focus on pandemic preparedness and supply-chain resilience (e.g., US CHIPS/HELP acts and EU health security plans) boosts demand for protective and sterile packaging solutions.

Berry must remain agile to shifting public-health priorities and expedited regulatory approvals for medical plastics to capture contracts; healthcare packaging was ~18% of Berry’s 2024 net sales (~$2.6bn of $14.5bn).

- Healthcare policy shifts directly affect demand and contract timing

- Pandemic preparedness increases need for sterile/protective packaging

- Regulatory approvals for medical-grade plastics are critical to revenue capture

Berry Faces Margin Strain: Trade, rPET Rules & Rising Logistics Lift FY24 Costs

Political risks—trade tensions, tariffs, and regional regulations on recycled content (EU 30% rPET by 2030; CA SB 54)—pressure Berry’s margins and capex; FY2024 sales $11.2B–$14.5B (healthcare ~$2.6B) with ~28% revenue in higher-risk markets, logistics costs up ~12% (2023) and supply disruptions adding ~4–6%.

| Metric | Value |

|---|---|

| FY2024 net sales | $11.2B–$14.5B |

| Healthcare sales | $2.6B (~18%) |

| Revenues in high-risk markets | 28% |

| Logistics cost change (2023) | +12% |

| Supply disruption impact | +4–6% logistics |

What is included in the product

Explores how external macro-environmental factors uniquely affect Berry Global Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors, and strategists on risks, opportunities, and scenario planning.

A concise, shareable PESTLE summary of Berry Global Group that’s visually segmented for quick meetings, editable for local or business-line notes, and written in clear language to support fast alignment on external risks and strategic positioning.

Economic factors

Raw Material Price Volatility

The cost of plastic resins—about 30–40% of Berry Global Group's COGS—tracks oil and natural gas prices; Brent crude rose ~20% in 2024, pressuring margins. Volatile energy markets in 2024–2025 forced more active hedging and selective price pass-through; Berry reported resin cost inflation contributing to its 2024 gross margin decline of ~150 basis points. Petroleum supply shifts directly compress EBITDA when pass-through is delayed.

Inflationary Pressures and Interest Rates

Persistent US inflation—3.4% year-over-year in 2024 (BLS)—raises Berry Global Group's labor and logistics costs, pressuring its goal to improve adjusted EBITDA margins (2023 pro forma margin ~11.5%).

Higher interest rates (US 10-year at ~4.5% in early 2025) increase Berry's cost of debt; long-term net leverage stood near 4.0x in 2024, elevating financing costs for capex and M&A.

Berry must reprioritize capital allocation—balancing necessary investments and debt reduction—to sustain growth while containing high-cost borrowing impacts.

Currency Exchange Rate Fluctuations

With roughly 45% of 2024 revenue generated outside the United States, Berry Global faces material foreign exchange risk as USD moves versus the euro, pound and MXN; a 5% USD appreciation could reduce reported international revenue by an estimated $200–250 million annually.

Currency translation hit 2024 adjusted operating income by about $60 million, highlighting sensitivity to FX swings. Berry pursues geographic diversification and active hedging—noting $1.2 billion of hedged exposure in 2024—to stabilize reported results and cash flows.

Consumer Spending Patterns

Consumer spending shifts reduce demand for premium personal-care packaging; US household disposable income fell 0.5% real in 2023 versus 2022, pressuring premium segments.

Berry’s exposure to essentials—food, healthcare, hygiene—accounted for ~70% of 2024 sales, cushioning revenue in downturns and supporting stable EBITDA margin (2024 adj. EBITDA margin ~10.8%).

Monitoring macro indicators lets Berry reweight product mix toward value and high-turn essentials aligned to consumer purchasing power.

- Disposable income decline 0.5% (2023)

- Essentials ~70% of 2024 sales

- 2024 adj. EBITDA margin ~10.8%

Global Supply Chain Dynamics

Global shipping rates fell from a 2022 peak (Harpex index down ~60% by end-2024) but remain 20–30% above 2019 levels, affecting Berry Global’s COGS and lead times; port congestion variability (e.g., LA/Long Beach dwell times down 15% in 2024) still risks delays to international customers.

Berry must weigh higher unit costs from localized plants against inventory and tariff savings from centralized hubs; nearshoring could raise manufacturing opex by ~5–12% but cut transit times by weeks.

Efficient logistics—route optimization, carrier diversification, 3PL partnerships—reduces volatility impact; logistics drive a material portion of SG&A and margin resilience in a global economy with fluctuating fuel surcharges and freight surcharges.

- Harpex index down ~60% from 2022 peak; freight ~20–30% above 2019

- Port dwell times improved ~15% at major US ports (2024)

- Nearshoring may increase opex ~5–12% but trims transit weeks

- Logistics optimization directly supports SG&A and margins

Rising resin, inflation and FX squeeze margins as leverage and rates bite

Resin costs (30–40% of COGS) tied to oil; Brent +~20% in 2024 hit gross margin (~150 bps headwind). US inflation 3.4% (2024) raised labor/logistics; 2024 adj. EBITDA margin ~10.8% with pro forma 2023 margin ~11.5%. US 10y ~4.5% (early 2025) and net leverage ~4.0x increased financing costs. FX: 45% revenue ex-US; 5% USD up ≈ -$200–250M revenue; $1.2B hedged 2024.

| Metric | 2024 |

|---|---|

| Resin % COGS | 30–40% |

| Adj. EBITDA margin | 10.8% |

| US inflation | 3.4% |

| Net leverage | ~4.0x |

| Intl revenue | 45% |

Preview Before You Purchase

Berry Global Group PESTLE Analysis

The preview shown here is the exact Berry Global Group PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in this preview are identical to the downloadable file you’ll get immediately after checkout.