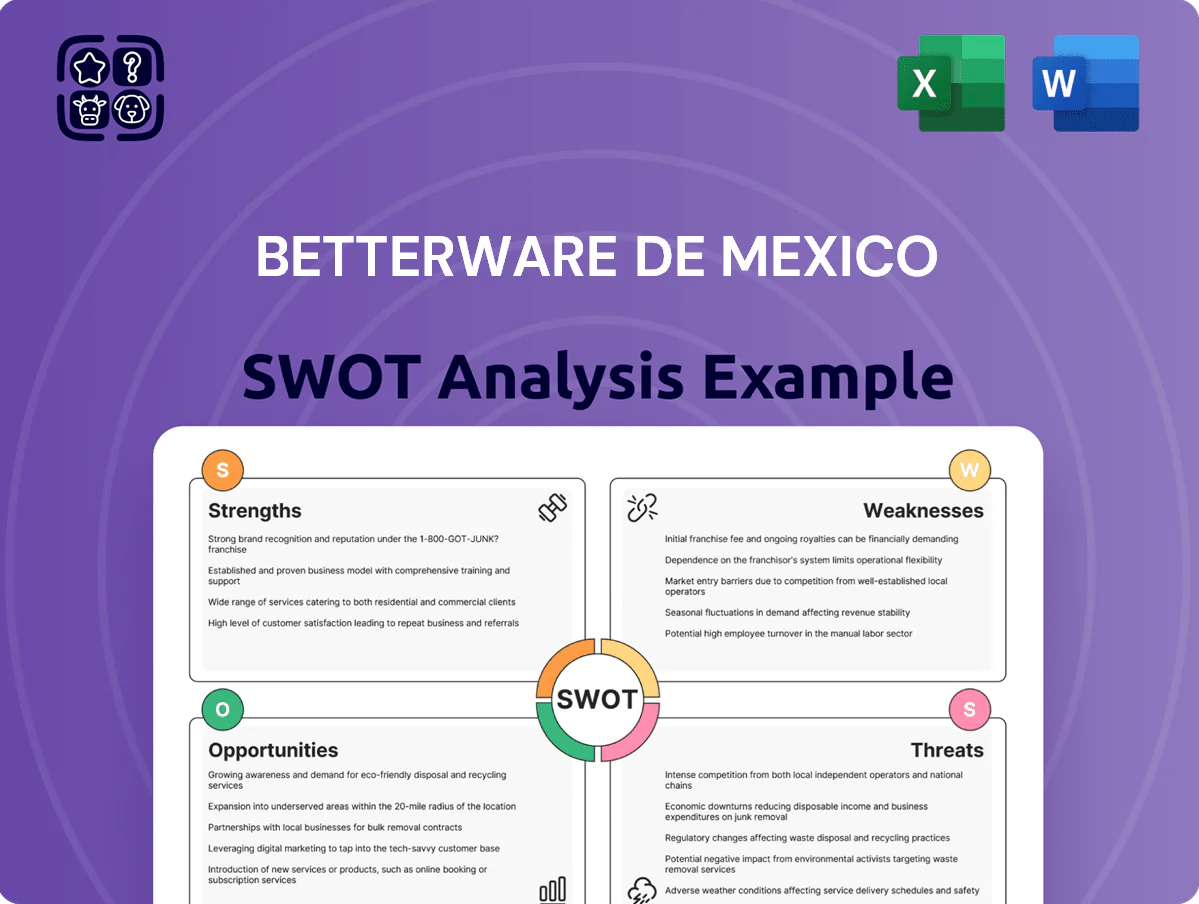

Betterware de Mexico SWOT Analysis

Your Strategic Toolkit Starts Here

Betterware de México combines strong direct-sales heritage and a loyal customer base with omni-channel growth potential, yet faces margin pressure, competitive retail shifts, and supply-chain risks—our full SWOT unpacks these forces and strategic options. Purchase the complete SWOT analysis to get a professionally formatted Word report plus an editable Excel matrix with actionable insights for investors, consultants, and managers.

Strengths

Dominant Market Penetration in Mexico

Betterware de México reaches over 1.1 million active distributors and associates, giving it top penetration in Mexico’s home solutions segment and access to low-income and rural customers often missed by stores and upscale e-commerce.

This field network helped generate MXN 5.8 billion in revenue in 2024, and the brand’s household recognition creates a strong moat that deters new direct-to-consumer entrants.

Efficient Asset-Light Business Model

Betterware de Mexico runs an asset-light logistics and distribution network that cuts capex on physical stores, keeping store-related fixed costs near zero and SG&A lean; in 2024 cost of goods sold fell 2.1% y/y while operating margin stayed around 18.5%. By using ~90,000 independent associates for last-mile delivery, the company preserves high gross margins and a variable cost base, enabling rapid scale—revenues rose 12% in FY2024. Strong free cash flow generation (MXN 420m in 2024) funded a consistent dividend yield near 4% that year, underscoring the model’s cash-conversion efficiency.

Successful Integration of Jafra

The Jafra acquisition has shifted Betterware de Mexico into beauty and personal care, raising gross margins: combined gross margin improved to ~39.5% in 2025 from 34.2% in 2023, per company filings.

Integration broadened the customer base—active clients rose 28% to 2.1 million in 2025—and added a counter-cyclical product cadence that smooths seasonal dips in home goods.

By end-2025 Betterware reported MXN 420 million in cost synergies and a 15% uplift in cross-sell revenue between sales forces, lowering combined SGA as a percent of sales by 320 bps.

Advanced Digital Transformation

Betterware de México shifted from catalog sales to a tech-enabled platform, equipping ~80,000 associates with mobile apps that cut order processing time by ~40% and raised monthly active users 22% in 2024.

Digital tools handle orders, performance metrics, and payments, lowering administrative costs and improving associate retention by an estimated 12% year-over-year.

Real-time sales data now informs assortments and promotions, with digital transactions reaching ~55% of total sales in FY2024.

- 80,000 associates on mobile apps

- -40% order processing time

- +22% MAUs in 2024

- 55% sales via digital payments (FY2024)

- +12% associate retention YoY

Robust Supply Chain and Logistics Hub

- 98% fulfillment accuracy

- 24–48 hr turnaround

- Weekly launches

- ~12,000 SKUs managed

- ~10,000 consultant network

Betterware+Jafra: Asset‑light MXN 5.8B biz—1.1M distributors, 2.1M clients, MXN 420M FCF

Betterware de México’s 1.1M+ active distributors and 2.1M clients (2025) drive MXN 5.8B revenue (2024) with ~18.5% operating margin; Jafra raised combined gross margin to ~39.5% (2025). Asset-light model, 90k associates and 80k mobile-enabled reps cut order time ~40%, digital sales ~55% (FY2024), FCF MXN 420M (2024), and MXN 420M cost synergies (end-2025).

| Metric | Value |

|---|---|

| Active distributors | 1.1M |

| Active clients (2025) | 2.1M |

| Revenue (2024) | MXN 5.8B |

| Operating margin | ~18.5% |

| Gross margin (post‑Jafra 2025) | ~39.5% |

| Free cash flow (2024) | MXN 420M |

| Digital sales (FY2024) | ~55% |

| Order time cut | ~40% |

| Cost synergies (end‑2025) | MXN 420M |

What is included in the product

Delivers a strategic overview of Betterware de Mexico’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and future growth prospects.

Delivers a concise SWOT matrix for Betterware de México that speeds stakeholder alignment and decision-making.

Weaknesses

High Associate Turnover Rates

Significant Geographic Concentration

Despite international efforts, over 90% of Betterware de México’s 2024 revenue remained Mexico-linked, concentrating risk in one economy.

Mexican GDP growth slowed to 2.0% in 2024 and regulatory shifts or political volatility could hit Betterware’s margins and cash flow sharply.

Limited geographic diversification raises stock volatility; Betterware’s 3-year beta near 1.8 exceeds global consumer-staples peers around 0.8–1.1.

Dependence on Chinese Manufacturing

Betterware de Mexico sources a large share of products from third-party manufacturers in China, exposing it to supply disruptions and US-China tensions; in 2024 about 60% of imports for similar Mexican housewares firms came from China, raising risk.

Rising freight rates—average spot container rates rose ~35% in 2023 vs 2022—and tariff shifts can compress gross margins (Betterware reported 2023 gross margin ~28%); stockouts would hit sales.

Nearshoring pilots exist, but moving production requires capital and time; shifting even 30% of volumes could take 24+ months and substantial capex, limiting short-term flexibility.

Sensitivity to Consumer Purchasing Power

Betterware’s core customers are middle-to-low-income households whose discretionary spend fell sharply after Mexico’s 2022–2023 inflation spikes; real wages declined ~2.5% in 2023 and Mexico CPI was 4.9% in 2024, squeezing budgets and cutting non-essentials like home organization and beauty products.

During 2020–2024 earnings, Betterware showed revenue cyclicality with gross margin swings of ~200–400 bps across macro shocks, highlighting vulnerability to interest-rate driven consumption slowdowns in Latin America.

- High share of low-income customers — demand elastic

- Mexico CPI 4.9% in 2024 — real-wage pressure

- Revenue and gross-margin cyclicality: ~200–400 bps swings

- First-to-cut SKUs: non-essential home and beauty items

Complex Brand Management Requirements

Managing Betterware and Jafra forces complex marketing and cultural trade-offs; in 2024 Betterware Group reported MXN 4.1bn revenue and Jafra added MXN 0.9bn, raising risks of brand dilution and distributor overload across ~120,000 active consultants.

Failure to keep distinct identities can cut conversion and loyalty, so integrated governance is essential.

- Two-brand mix: MXN 5.0bn combined 2024 revenue

- 120,000 distributors risk overload

- Possible brand dilution lowers lifetime value

High churn, China reliance and rising costs squeeze Mexico-centric distributor model

Same Document Delivered

Betterware de Mexico SWOT Analysis

This is the actual Betterware de México SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Betterware de México combines strong direct-sales heritage and a loyal customer base with omni-channel growth potential, yet faces margin pressure, competitive retail shifts, and supply-chain risks—our full SWOT unpacks these forces and strategic options. Purchase the complete SWOT analysis to get a professionally formatted Word report plus an editable Excel matrix with actionable insights for investors, consultants, and managers.

Strengths

Dominant Market Penetration in Mexico

Betterware de México reaches over 1.1 million active distributors and associates, giving it top penetration in Mexico’s home solutions segment and access to low-income and rural customers often missed by stores and upscale e-commerce.

This field network helped generate MXN 5.8 billion in revenue in 2024, and the brand’s household recognition creates a strong moat that deters new direct-to-consumer entrants.

Efficient Asset-Light Business Model

Betterware de Mexico runs an asset-light logistics and distribution network that cuts capex on physical stores, keeping store-related fixed costs near zero and SG&A lean; in 2024 cost of goods sold fell 2.1% y/y while operating margin stayed around 18.5%. By using ~90,000 independent associates for last-mile delivery, the company preserves high gross margins and a variable cost base, enabling rapid scale—revenues rose 12% in FY2024. Strong free cash flow generation (MXN 420m in 2024) funded a consistent dividend yield near 4% that year, underscoring the model’s cash-conversion efficiency.

Successful Integration of Jafra

The Jafra acquisition has shifted Betterware de Mexico into beauty and personal care, raising gross margins: combined gross margin improved to ~39.5% in 2025 from 34.2% in 2023, per company filings.

Integration broadened the customer base—active clients rose 28% to 2.1 million in 2025—and added a counter-cyclical product cadence that smooths seasonal dips in home goods.

By end-2025 Betterware reported MXN 420 million in cost synergies and a 15% uplift in cross-sell revenue between sales forces, lowering combined SGA as a percent of sales by 320 bps.

Advanced Digital Transformation

Betterware de México shifted from catalog sales to a tech-enabled platform, equipping ~80,000 associates with mobile apps that cut order processing time by ~40% and raised monthly active users 22% in 2024.

Digital tools handle orders, performance metrics, and payments, lowering administrative costs and improving associate retention by an estimated 12% year-over-year.

Real-time sales data now informs assortments and promotions, with digital transactions reaching ~55% of total sales in FY2024.

- 80,000 associates on mobile apps

- -40% order processing time

- +22% MAUs in 2024

- 55% sales via digital payments (FY2024)

- +12% associate retention YoY

Robust Supply Chain and Logistics Hub

- 98% fulfillment accuracy

- 24–48 hr turnaround

- Weekly launches

- ~12,000 SKUs managed

- ~10,000 consultant network

Betterware+Jafra: Asset‑light MXN 5.8B biz—1.1M distributors, 2.1M clients, MXN 420M FCF

Betterware de México’s 1.1M+ active distributors and 2.1M clients (2025) drive MXN 5.8B revenue (2024) with ~18.5% operating margin; Jafra raised combined gross margin to ~39.5% (2025). Asset-light model, 90k associates and 80k mobile-enabled reps cut order time ~40%, digital sales ~55% (FY2024), FCF MXN 420M (2024), and MXN 420M cost synergies (end-2025).

| Metric | Value |

|---|---|

| Active distributors | 1.1M |

| Active clients (2025) | 2.1M |

| Revenue (2024) | MXN 5.8B |

| Operating margin | ~18.5% |

| Gross margin (post‑Jafra 2025) | ~39.5% |

| Free cash flow (2024) | MXN 420M |

| Digital sales (FY2024) | ~55% |

| Order time cut | ~40% |

| Cost synergies (end‑2025) | MXN 420M |

What is included in the product

Delivers a strategic overview of Betterware de Mexico’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and future growth prospects.

Delivers a concise SWOT matrix for Betterware de México that speeds stakeholder alignment and decision-making.

Weaknesses

High Associate Turnover Rates

Significant Geographic Concentration

Despite international efforts, over 90% of Betterware de México’s 2024 revenue remained Mexico-linked, concentrating risk in one economy.

Mexican GDP growth slowed to 2.0% in 2024 and regulatory shifts or political volatility could hit Betterware’s margins and cash flow sharply.

Limited geographic diversification raises stock volatility; Betterware’s 3-year beta near 1.8 exceeds global consumer-staples peers around 0.8–1.1.

Dependence on Chinese Manufacturing

Betterware de Mexico sources a large share of products from third-party manufacturers in China, exposing it to supply disruptions and US-China tensions; in 2024 about 60% of imports for similar Mexican housewares firms came from China, raising risk.

Rising freight rates—average spot container rates rose ~35% in 2023 vs 2022—and tariff shifts can compress gross margins (Betterware reported 2023 gross margin ~28%); stockouts would hit sales.

Nearshoring pilots exist, but moving production requires capital and time; shifting even 30% of volumes could take 24+ months and substantial capex, limiting short-term flexibility.

Sensitivity to Consumer Purchasing Power

Betterware’s core customers are middle-to-low-income households whose discretionary spend fell sharply after Mexico’s 2022–2023 inflation spikes; real wages declined ~2.5% in 2023 and Mexico CPI was 4.9% in 2024, squeezing budgets and cutting non-essentials like home organization and beauty products.

During 2020–2024 earnings, Betterware showed revenue cyclicality with gross margin swings of ~200–400 bps across macro shocks, highlighting vulnerability to interest-rate driven consumption slowdowns in Latin America.

- High share of low-income customers — demand elastic

- Mexico CPI 4.9% in 2024 — real-wage pressure

- Revenue and gross-margin cyclicality: ~200–400 bps swings

- First-to-cut SKUs: non-essential home and beauty items

Complex Brand Management Requirements

Managing Betterware and Jafra forces complex marketing and cultural trade-offs; in 2024 Betterware Group reported MXN 4.1bn revenue and Jafra added MXN 0.9bn, raising risks of brand dilution and distributor overload across ~120,000 active consultants.

Failure to keep distinct identities can cut conversion and loyalty, so integrated governance is essential.

- Two-brand mix: MXN 5.0bn combined 2024 revenue

- 120,000 distributors risk overload

- Possible brand dilution lowers lifetime value

High churn, China reliance and rising costs squeeze Mexico-centric distributor model

Same Document Delivered

Betterware de Mexico SWOT Analysis

This is the actual Betterware de México SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.